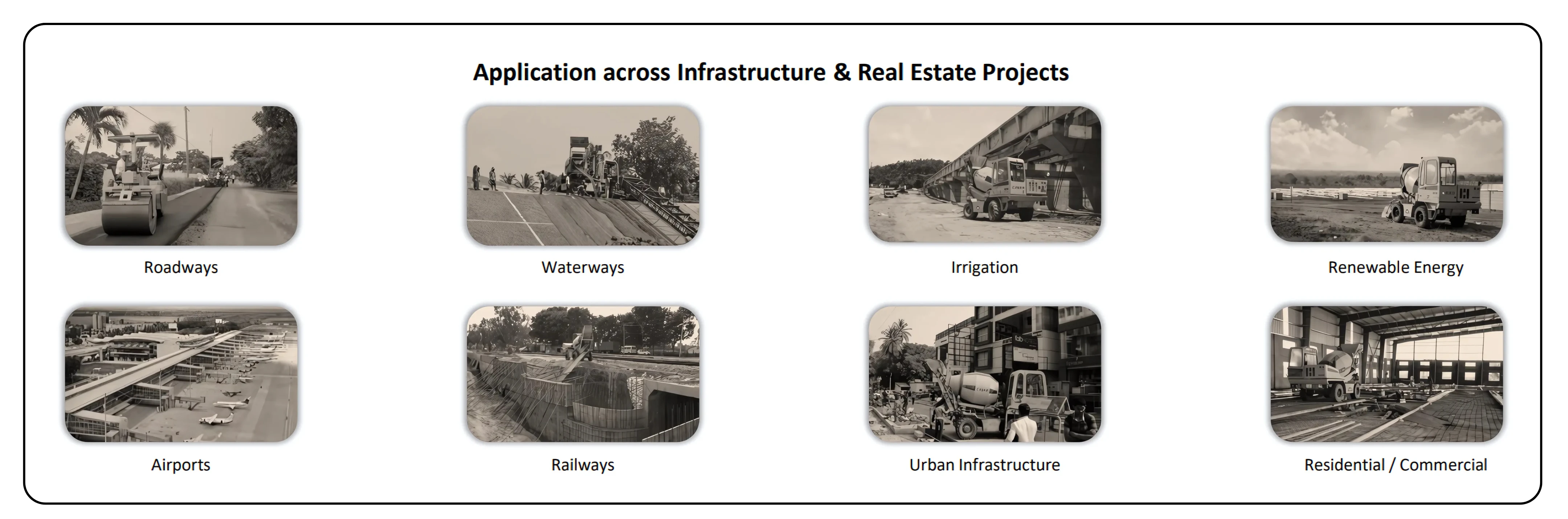

Ajax Engineering Limited plays a crucial role in India’s construction ecosystem, enabling the development of highways, irrigation canals, and housing projects with its advanced concrete machinery. Whether it’s a national highway being built under strict timelines, an irrigation project delivering water to rural areas, or a housing development in a rapidly expanding city, Ajax’s equipment is at the core. Its self-loading concrete mixers, batching plants, pumps, and slip-form pavers ensure concrete is produced, transported, and placed with precision and efficiency.

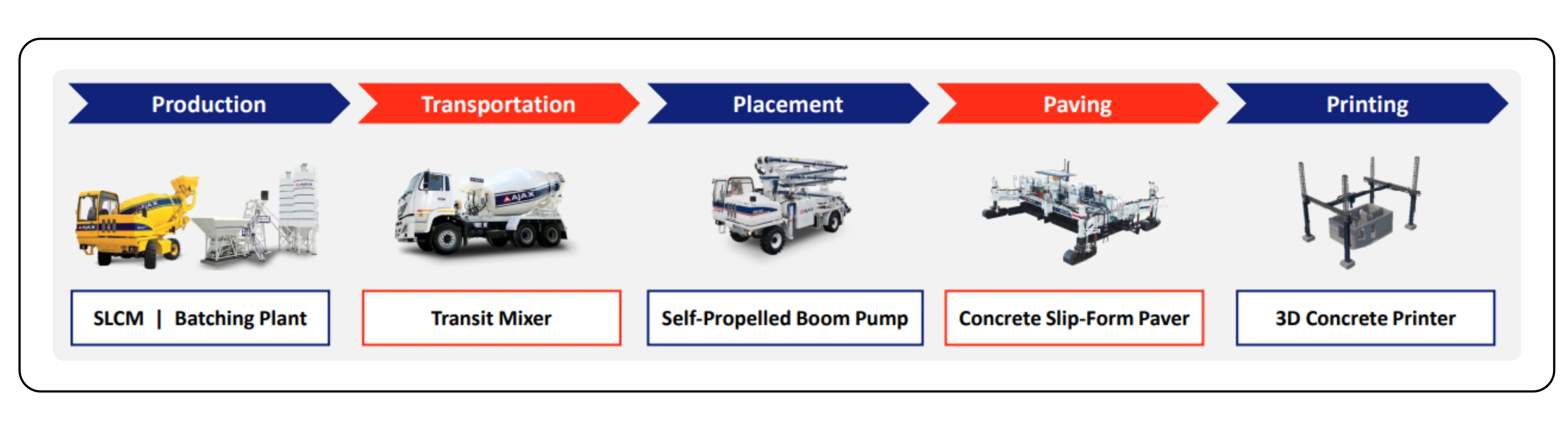

Ajax pioneered self-loading concrete mixers (SLCMs) in India in 1992 and currently holds nearly a 70% market share, with over 32,000 units sold in the last decade. Approximately 12% of India’s concrete production comes from Ajax SLCMs. Building on this leadership, the company has expanded its portfolio to include batching plants, transit mixers, boom pumps, and even 3D concrete printers. Its strong dealer and service network — 52 dealers, 114 touchpoints, and 28 international distributors- reinforces its reach and fosters long-term customer loyalty.

Ajax is widely regarded as the backbone of mechanised concrete construction in India. With the construction industry moving rapidly toward mechanization, the company is well-positioned to capture the benefits of this structural shift.

Business Model and Revenue Streams

Ajax’s business model focuses on delivering a complete concrete equipment ecosystem rather than limiting itself to machine sales. It combines equipment offerings with spare parts, service, and end-to-end lifecycle support, ensuring continuous engagement with customers. This approach not only strengthens customer retention but also generates a steady stream of recurring revenue.

SLCM (Self-Loading Concrete Mixers) is the core business segment and the largest contributor to Ajax Engineering’s revenue, accounting for over 80%. It is a self-contained machine that can batch, mix, transport, and place concrete at project sites without requiring additional equipment. This solution enhances cost efficiency by reducing dependency on batching plants and manual labor. SLCMs are widely used in rural, semi-urban, and infrastructure projects such as roads, irrigation canals, housing, and government works. They are also recognized by government agencies like the PWD, Irrigation Department, and Border Roads Organization as a reliable solution for quality-assured concrete production.

The Non-SLCM segment represents Ajax’s diversified machinery portfolio beyond concrete mixers. It includes equipment such as concrete pumps, boom pumps, batching plants, and slip-form pavers. These machines are designed to serve large-scale, complex infrastructure projects requiring higher precision and efficiency. This segment is growing steadily, supported by rising investments in urban infrastructure, highways, and smart city projects. It complements the SLCM segment by positioning Ajax as a comprehensive concrete solutions provider.

Domestic sales remain the primary revenue driver for Ajax, but exports are emerging as a significant growth lever, contributing around 6% of revenue in Q1 FY26. The company now serves over 50 countries and is steadily expanding its presence across South Asia, Africa, and the Middle East. This expansion strategy is measured and deliberate, aimed at capturing new market opportunities while mitigating country-specific and currency-related risks.

Also read: Jyoti CNC Poised for the Next Growth Phase

Industry Overview

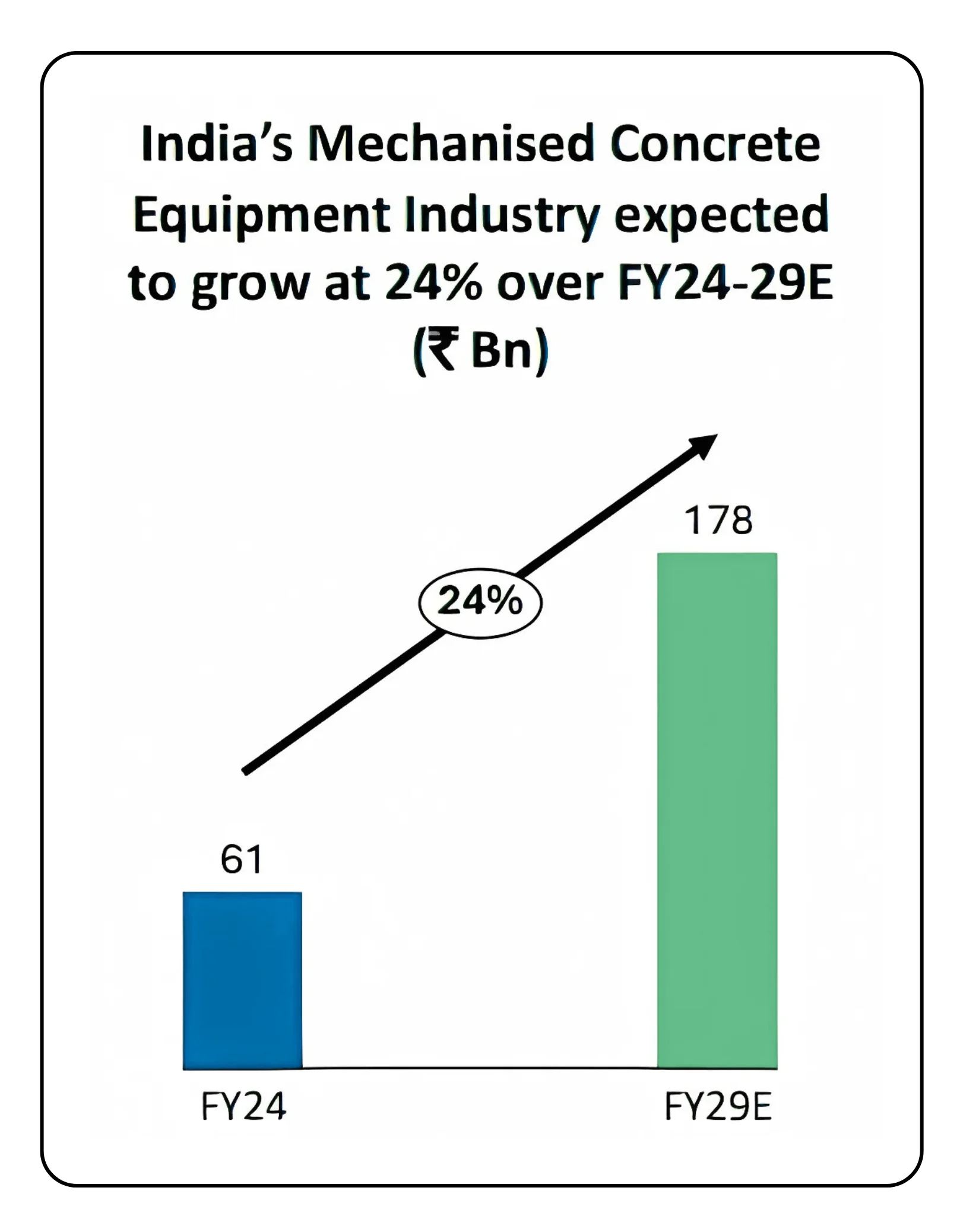

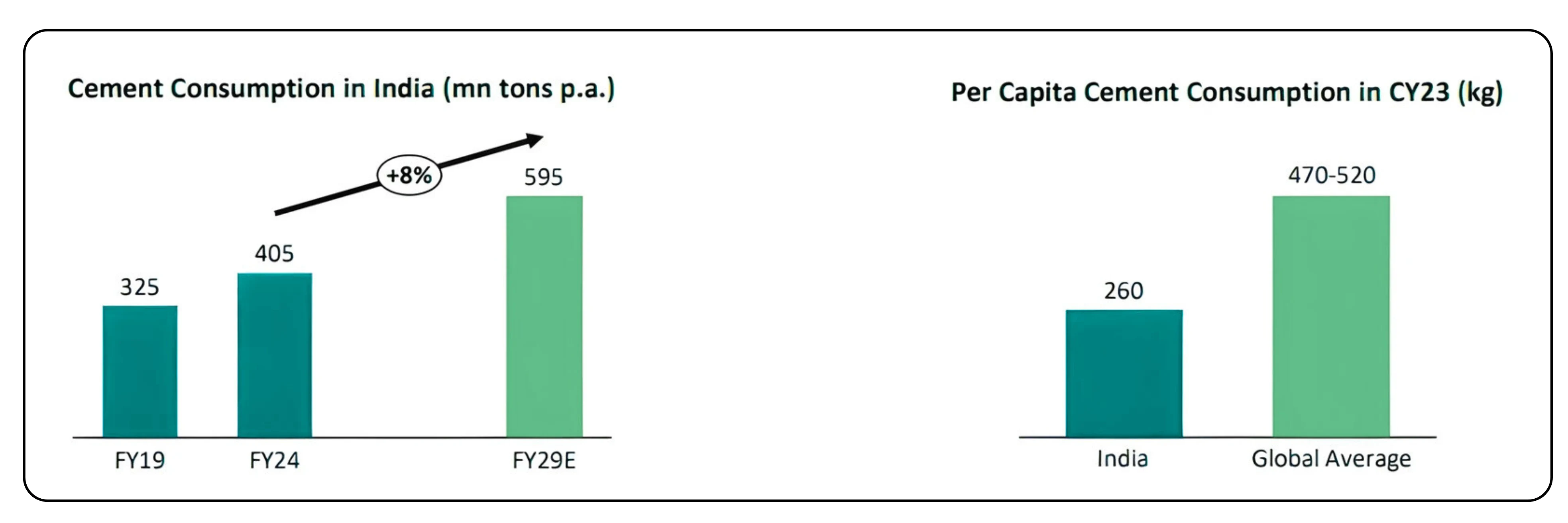

India’s cement and concrete consumption is projected to grow at about 8% CAGR through FY29. What’s more significant is the rapid shift in the concreting process. Mechanized equipment, which accounted for just 17% of concrete equipment sales in FY24, is expected to climb to 28% by FY29. This change is fueled by the growing demand for efficiency, speed, and quality in large-scale infrastructure and housing projects.

Ajax sits at the centre of this transition. As the market leader in SLCMs, it has already established dominance and is now expanding its presence in non-SLCM categories. Its equipment is deployed across highways, irrigation canals, airports, urban infrastructure, and residential projects, giving the firm exposure to multiple growth drivers. Strong brand equity, a wide distribution network, and a robust after-sales service framework make its leadership position hard to challenge.

Manufacturing and R&D Capabilities

Ajax operates three major manufacturing facilities in Karnataka, Obadenahalli, Bashettihalli, and Gowribidanur, with an installed SLCM capacity of 7,200 units per single shift, running at 79% utilization in FY25. A fourth facility at Adinarayanahosahalli is scheduled to go live in the second half of FY26, adding fungible capacity across multiple product categories.

R&D is a key differentiator for Ajax. The company has a track record of innovation, having developed India’s first slip-form paver in-house in 2019, commercialized a 3D concrete printer in 2023, and introduced load-cell-based SLCMs for superior accuracy. These innovations not only reinforce Ajax’s leadership but also open up new revenue streams.

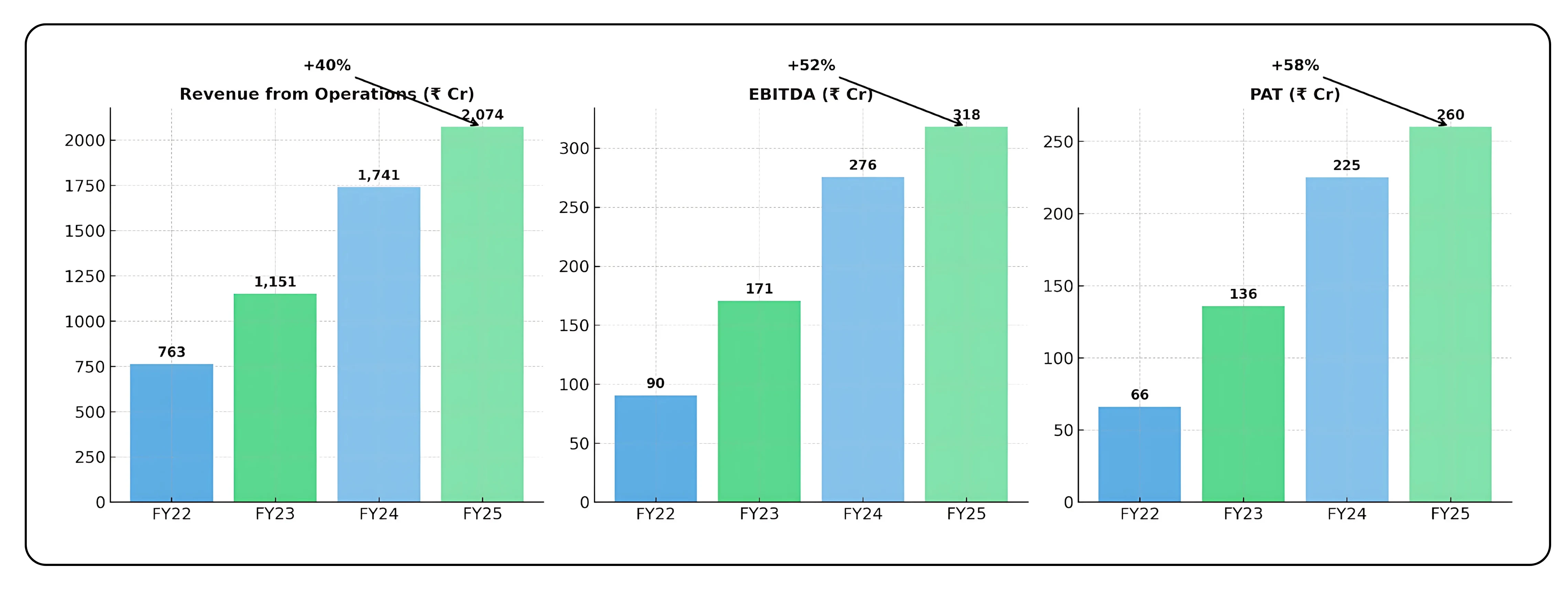

Financial Performance (FY22–FY25)

Over the last four years, Ajax has delivered exceptional growth. Sales increased from ₹7,633 crore in FY22 to ₹20,739 crore in FY25, a compound annual growth rate of 40%. EBITDA rose from ₹905 crore to ₹3,181 crore (52% CAGR), while net profit surged from ₹662 crore to ₹2,601 crore (58% CAGR).

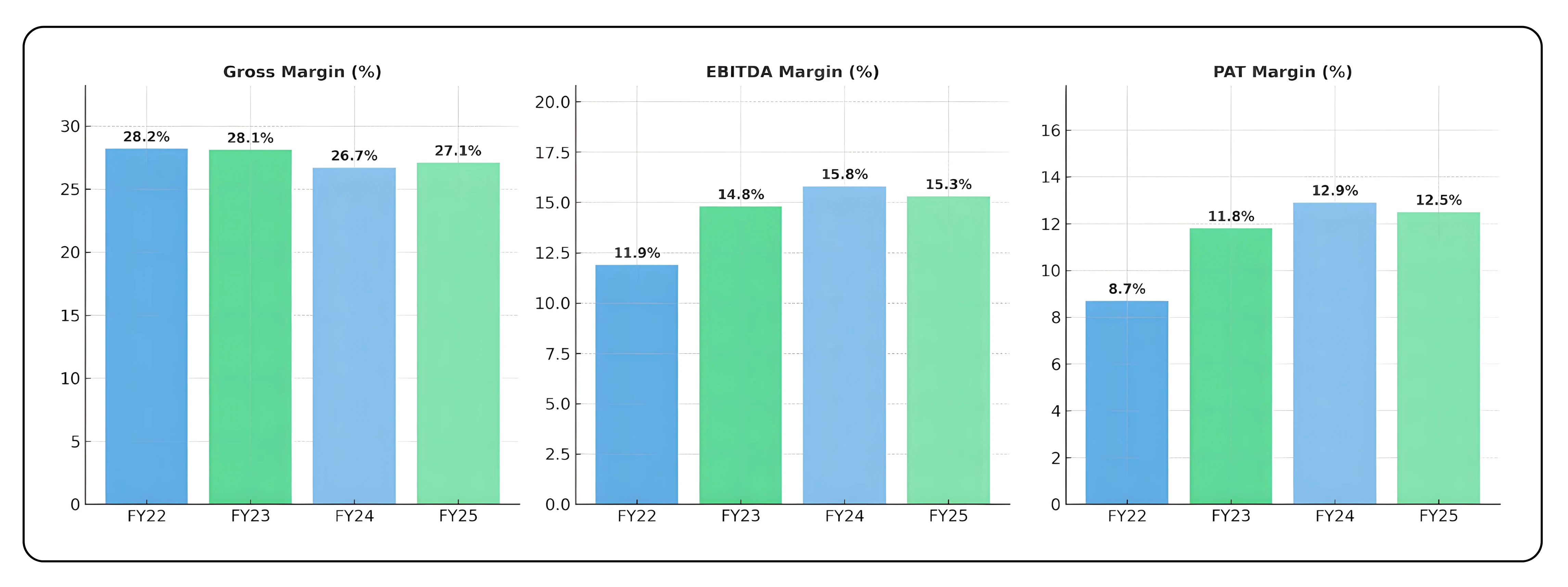

Margins have been steady, with gross margins at 27% and EBITDA margins at around 15%. PAT margins improved from 8.7% in FY22 to 12.5% in FY25. The company’s returns are equally impressive: ROCE stood at 30.2% and ROE at 22.5% in FY25. The balance sheet is debt-free, backed by ₹650 crore in cash and current investments at the end of Q1 FY26.

Cash flow from operations, however, fell to ₹427 crore in FY25 from over ₹2,000 crore in FY24 due to working capital absorption. Inventories and receivables rose alongside sales growth, a factor investors should monitor as Ajax scales further.

The financial trajectory shows a company that has grown rapidly while maintaining capital efficiency, a hallmark of a high-quality compounder.

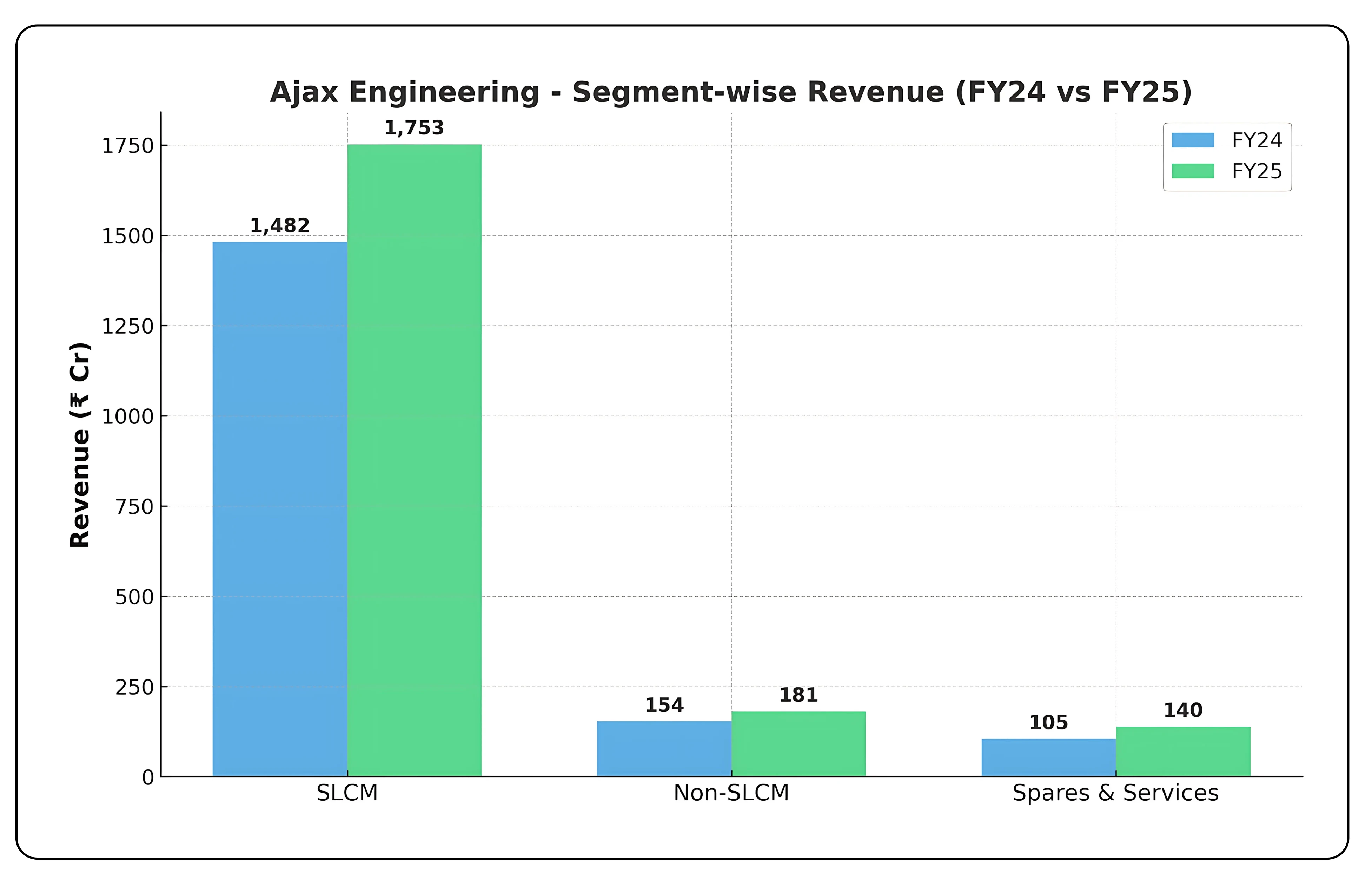

Segment-wise Revenue Breakup

| Segment | FY24 Revenue (₹ Cr) | FY25 Revenue (₹ Cr) | YoY Growth |

|---|---|---|---|

| SLCM | 1,482 | 1,753 | +18.3% |

| Non-SLCM | 154 | 181 | +17.7% |

| Spares & Services | 105 | 140 | +33.0% |

Growth was broad-based across all segments, but SLCM remained the dominant business (85% of revenue), while Spares & Services showed the strongest percentage growth, highlighting an expanding aftermarket/maintenance opportunity.

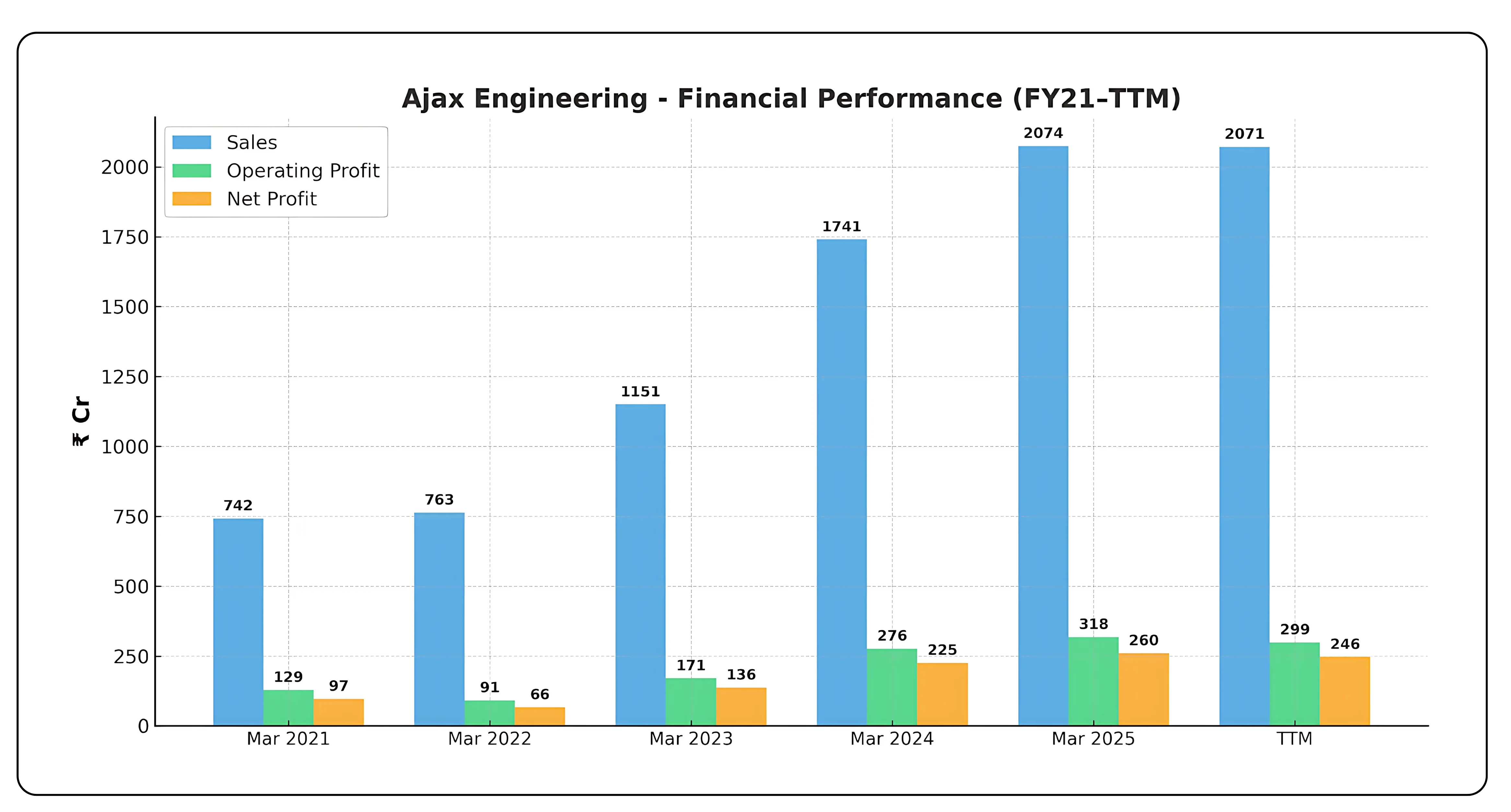

5-year and Q1 FY26 Performance

Sales have shown a consistent upward trend, rising from ₹742 crore in March 2021 to over ₹2,070 crore by March 2025, before stabilizing marginally in the TTM period. Operating profit has followed a similar trajectory, expanding from ₹129 crore in FY21 to ₹318 crore in FY25, though slightly easing to ₹299 crore in the TTM due to recent cost pressures. Net profit has more than doubled over the period, climbing from ₹97 crore in FY21 to ₹260 crore in FY25, with a small drop to ₹246 crore in the TTM.

The first quarter of FY26 reflected transition pressures. Revenue was stable at ₹4,665 crore, but EBITDA was ₹614 (Gross Profit ) crore and PAT₹529 crore. EBITDA margin compressed to 13.2%.

Management attributed the decline in profitability to two key factors. First, the absence of slip-form paver sales, which are high-value and margin-accretive products, impacted overall margins. Second, the transition from CEV-4 to CEV-5 emission norms resulted in an additional 4% increase in direct material costs. The management noted that pricing adjustments would begin toward the end of Q2 FY26, after clearing the CEV-4 inventory, to recover margins.

Also read : Honeywell Automation India Positioned for Long-Term Value Creation

Valuation and Market View

At a market capitalisation of ₹7,858 crore and a current price of ₹687, Ajax trades at 32 times earnings and 22.8 times EV/EBITDA, compared with industry averages of 38x and 25.7x. On FY25 EPS of ₹22.7, the stock’s trailing P/E is around 30x.

While not cheap, Ajax’s valuation reflects its strong market position, superior returns, and growth runway. The company’s high RoCE, debt-free balance sheet, and structural positioning in India’s mechanisation theme justify a premium. However, near-term risks around margin recovery and project execution temper the outlook.

Forward Outlook & Valuation Compression Analysis

Assumptions based on management’s discussion:

- Base FY25 EPS: ₹22.7

- Volume growth in FY26: early double digits (10–12%)

- Margin recovery through calibrated price hikes in H2 FY26

- Net profit margins stabilising near 12–13% by FY27

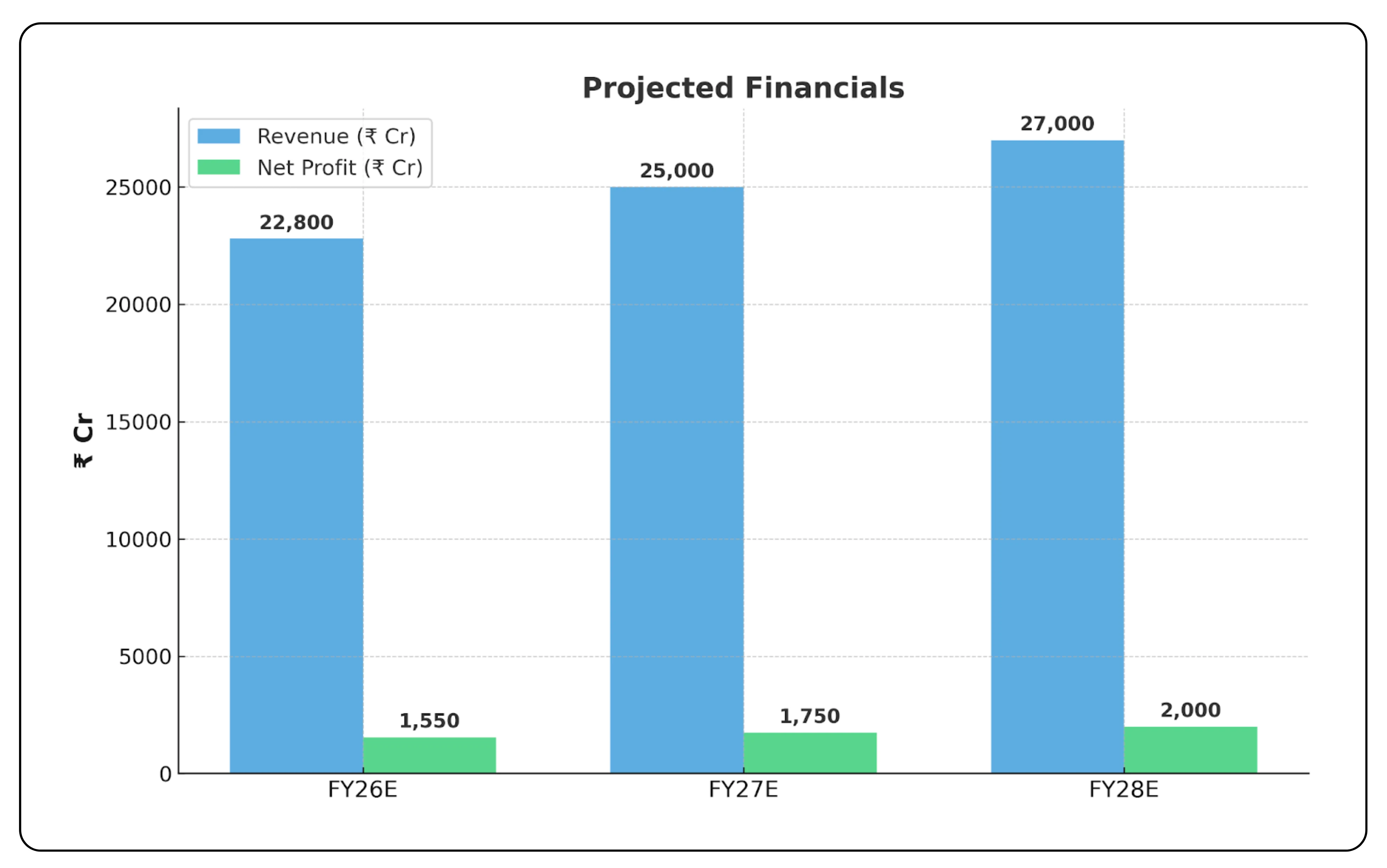

| Year | Revenue (₹ Cr) | Net Profit (₹ Cr) | EPS (₹) | Forward P/E (at ₹687) |

|---|---|---|---|---|

| FY26E | 22,800 | 1,500–1,600 | 24–26 | 26–29x |

| FY27E | 25,000+ | 1,700–1,800 | 27–29 | 24–25x |

| FY28E | 27,000+ | 2,000 | 31–33 | 20–22x |

Interpretation:

In the base case, Ajax’s earnings growth drives a natural compression in P/E multiples from the current 30x to the mid-20s by FY27. In a bull case, with stronger demand and better price realisation, EPS could exceed ₹33, pulling forward P/E closer to 20x. In a bear case, where margins remain weak and growth slows, EPS may stay closer to ₹21–22, keeping the forward multiple high at over 30x.

This analysis suggests that while the stock is not inexpensive, sustained growth and margin recovery could justify valuations, with scope for re-rating if execution surprises positively.

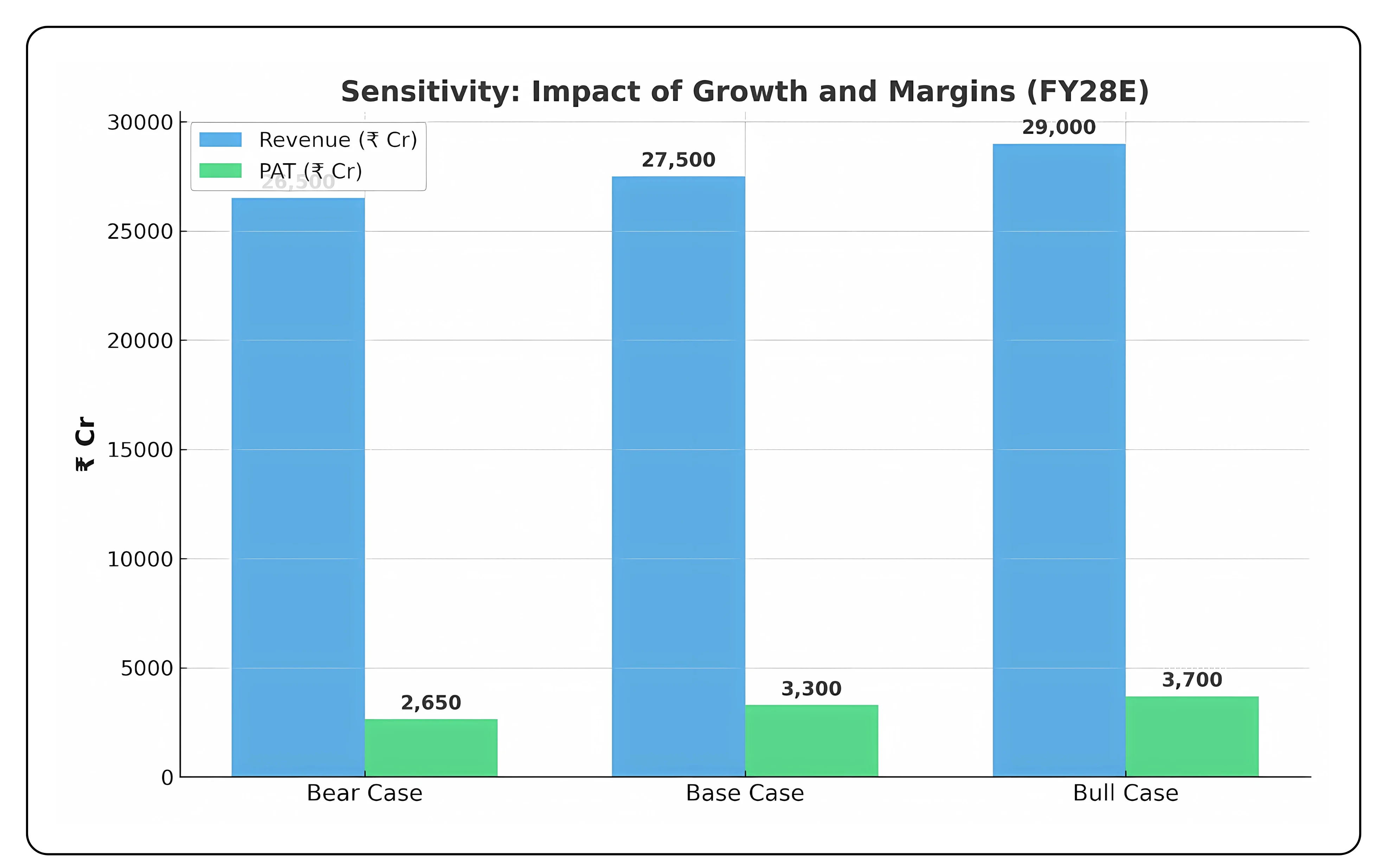

Sensitivity: Impact of Growth and Margins

| Scenario | Revenue CAGR (FY25–FY28) | Net Margin | FY28E Revenue (₹ Cr) | FY28E PAT (₹ Cr) | EPS (₹) | Forward P/E (at ₹687) |

|---|---|---|---|---|---|---|

| Bear Case | 7% | 10% | 26,500 | 2,650 | 21–22 | 31–33x |

| Base Case | 9% | 12% | 27,500 | 3,300 | 27–29 | 24–25x |

| Bull Case | 11% | 13% | 29,000+ | 3,700+ | 31–33 | 20–22x |

What This Shows

If growth slows and margins slip, Ajax’s forward P/E remains elevated above 30x, leaving little scope for re-rating. In the base case, moderate execution drives EPS higher, compressing P/E into the mid-20s, a level more aligned with peers. In the bull case, strong demand, price hikes, and a richer non-SLCM mix could push EPS beyond ₹30, bringing forward P/E closer to 20x and supporting a re-rating.

Risks and Challenges

The key risk for Ajax is margin pressure stemming from the CEV-5 transition. If competitive pricing limits the company’s ability to pass on higher costs, profitability could remain under pressure. Demand risk also exists from slower infrastructure execution, such as the reduced pace of PMGSY(Pradhan Mantri Gram Sadak Yojana) road construction in FY25. Product mix volatility, particularly in high-value categories like slip-form pavers, can lead to quarterly fluctuations. Additionally, while exports offer growth potential, they bring exposure to currency and geopolitical risks.

Strategic Outlook

Ajax enters FY26 from a position of strength, despite near-term challenges. The company is well-placed to benefit from India’s infrastructure push and the accelerating shift toward mechanized concreting. The upcoming Adinarayanahosahalli facility will enhance capacity, while the expanding non-SLCM portfolio broadens revenue streams. With a debt-free balance sheet, strong return ratios, and disciplined execution, Ajax has the resilience to manage short-term pressures.

For long-term investors, Ajax provides exposure to one of India’s most critical infrastructure themes through a capital-efficient, market-leading business. While valuations aren’t inexpensive, they reflect a high-quality franchise with a track record of consistent growth and strong returns.

Investment Perspective

Ajax Engineering is the hidden force behind India’s infrastructure growth. Its self-loading mixers, batching plants, and pavers are integral to the way the country builds. With market leadership, a growing product portfolio, and strong returns on capital, Ajax stands out as a high-quality compounder. The near term may bring volatility as margins adjust to new emission norms, but the long-term growth story remains intact.

At current valuations, Ajax trades at a premium, but not an unreasonable one compared to peers. Investors should track margin recovery, momentum in non-SLCM products, and working capital discipline. For those looking to participate in India’s infrastructure mechanization theme, Ajax continues to be a compelling opportunity.

Start your trading journey with CubePlus today and stay in control of your investments. [Sign up now] and trade smarter.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.