Honeywell Automation India Ltd. (HAIL) is not the kind of company most people deal with directly, but its presence is deeply embedded in industries and infrastructure that touch everyday life. Imagine a refinery running 24/7 with thousands of control points, an airport with ideal lighting, cooling, fire safety, and security all running seamlessly, or a hospital with dependable air quality, temperature, and backup power. All this is made possible by HAIL, which provides the automation backbone powering these capabilities.

In essence, HAIL is the “brain and nervous system” of critical industries. Its portfolio includes software that provides managers with real-time data, controllers that react instantly, and sensors that identify changes. Over time, the company ensures these systems remain reliable through upgrades, services, and long-term maintenance.

Established in 1984, HAIL is part of Honeywell International, a global leader in technology and manufacturing. Accessing Honeywell’s worldwide R&D and innovation ecosystem, coupled with strong local execution in India, is its double advantage. This enables HAIL to bring advanced global technology to Indian customers while also serving as a delivery hub for Honeywell affiliates globally.

Business Model and Revenue Streams

HAIL’s business model is built on providing end-to-end automation solutions. Instead of selling one-off products, it integrates hardware, software, and services into long-term contracts. This approach generates recurring revenue and strengthens customer stickiness.

- Products & Systems – The foundation of automation consists of industrial sensors, controllers, switches, and building management systems.

Software & Platforms – Proprietary software for process optimization, safety monitoring, and data analytics.

Engineering & Integration Services – These services deliver custom-built automation systems for refineries, factories, data centers, airports, and other vital infrastructure.

- Aftermarket Services – These services include maintenance, spares, and lifecycle management, which generate steady recurring revenue.

The blend of products, projects, and services ensures that HAIL is not just dependent on one-time sales. Long project cycles and service contracts keep revenue visibility high.

Honeywell Automation’s Industry Positioning

Automation is no longer optional; it is essential. Hence, efficiency and reliability have become critical due to rising energy costs, labor challenges, and stricter safety standards. And HAIL sits at the intersection of these trends, with strong positions in:

- Industrial Automation – Oil & gas, petrochemicals, power generation, and manufacturing plants.

- Building Automation – Airports, healthcare, data centers, and smart commercial facilities.

- Defence and Infrastructure – Safety, security, and monitoring systems for mission-critical operations.

Its presence across industries acts as a natural hedge, with sectors such as data centers or healthcare providing growth opportunities when other sectors experience a downturn.

Manufacturing and R&D Capabilities

HAIL operates with a high level of vertical integration in its Indian facilities, giving it tighter control over quality and delivery. This includes in-house design, assembly, and testing for its hardware and software solutions.

Most importantly, Honeywell International's worldwide R&D network is beneficial to HAIL. While local R&D teams adapt solutions for Indian customers, global expertise ensures that it remains at the cutting edge of technologies such as IoT-driven automation, AI-powered predictive analytics, and energy efficiency platforms.

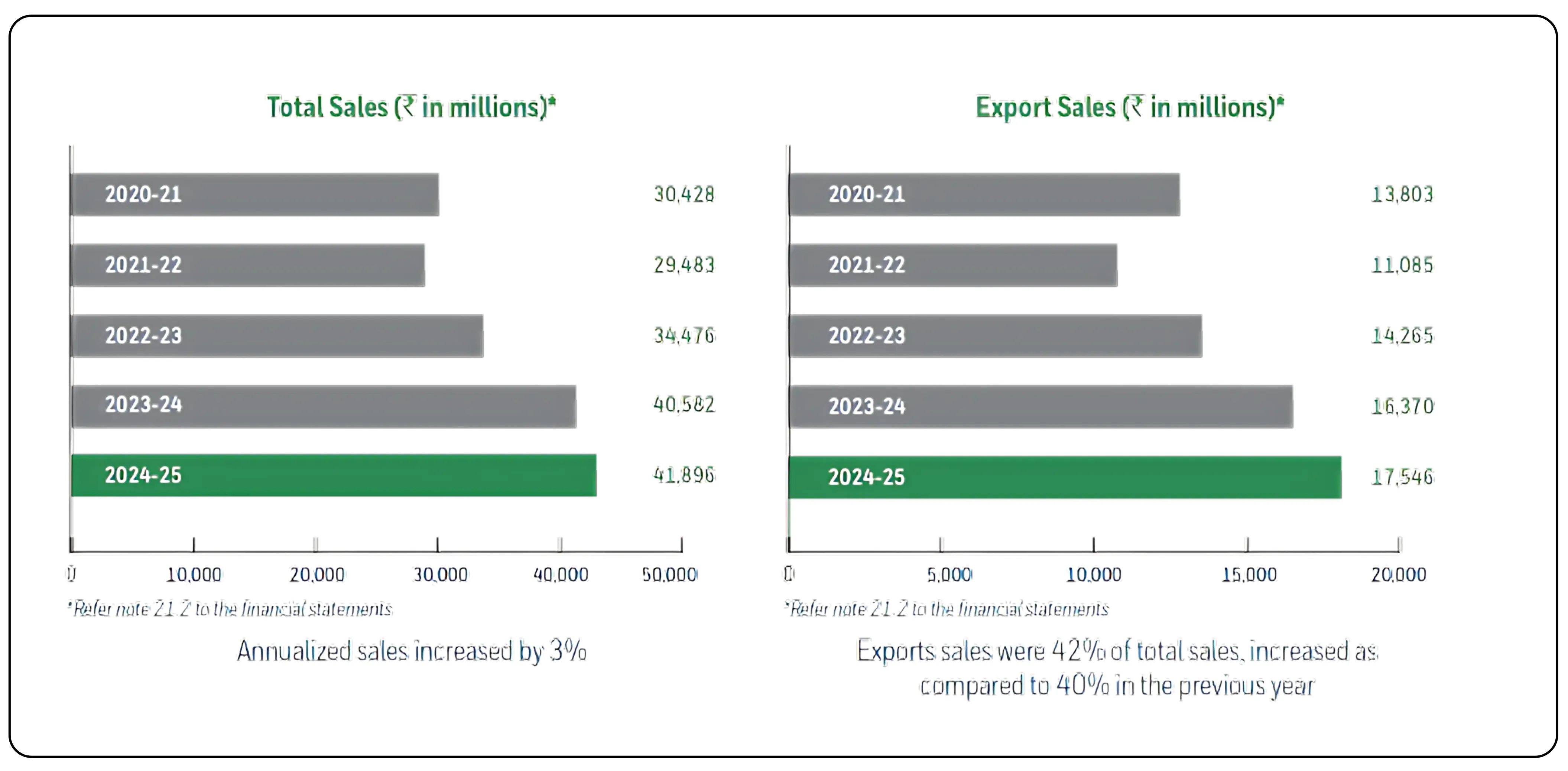

HAIL’s Financial Performance (FY21–FY25)

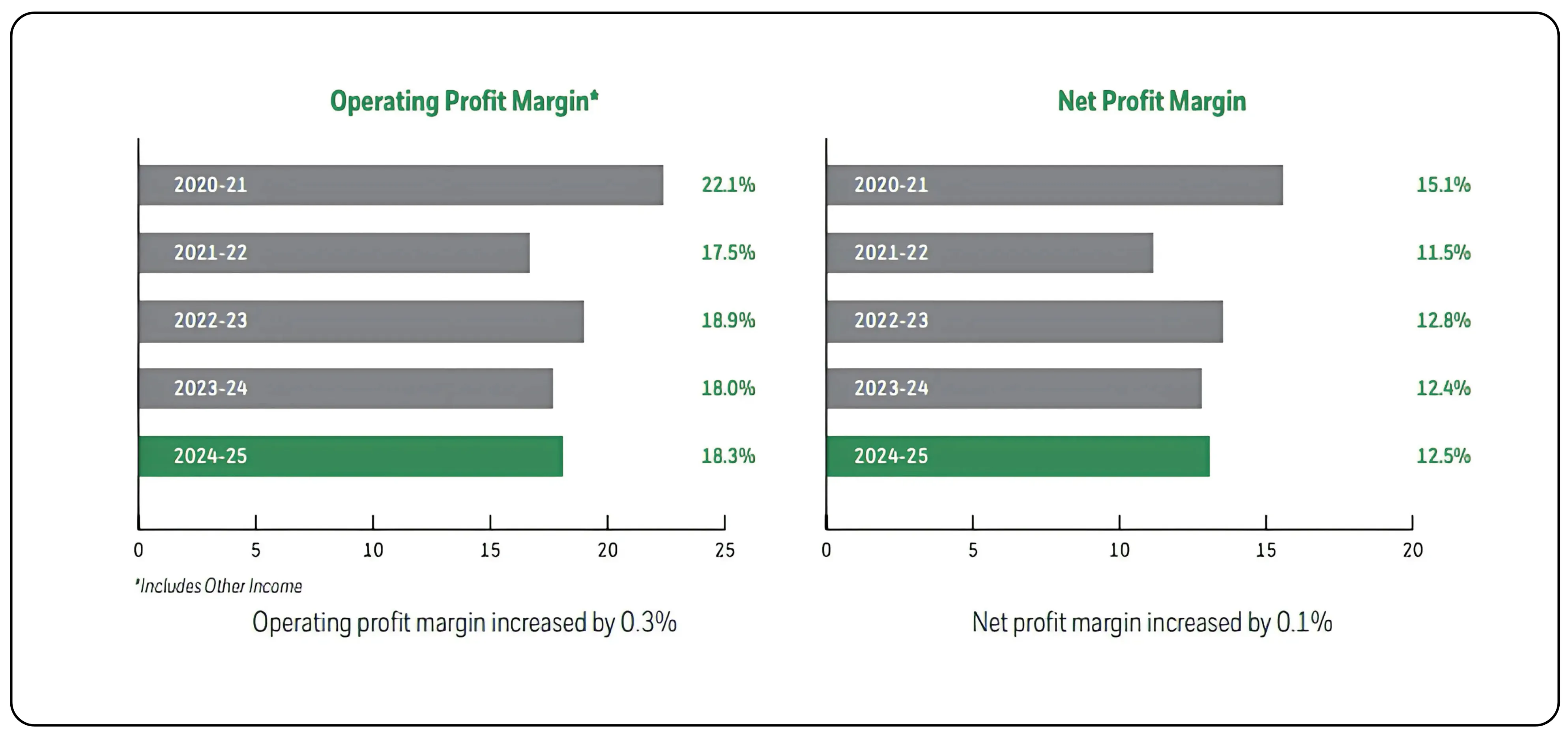

Honeywell Automation India has maintained consistent revenue growth over the past five years. Sales increased from ₹3,043 crore in FY21 to ₹4,412 crore on a trailing twelve-month (TTM) basis. Net profit has also remained strong, improving from ₹460 crore in FY21 to ₹524 crore in FY25.

However, the operating profit margin (OPM) has been under pressure. Margins declined from 19% in FY21 to 18% in FY25, reflecting rising input costs, wage inflation, and competitive pricing dynamics in the automation industry. Despite this, Honeywell’s solid product mix and recurring revenue-generating service contracts allow it to maintain healthy profitability levels when compared to its peers.

The chart highlights three aspects: steady sales growth, stable yet slightly moderating profit levels, and a clear downward trend in margins. This combination suggests that maintaining margins will be Honeywell’s primary area of focus moving forward, even as the company continues to grow its top line.

Returns: The ROCE at 18.4% and ROE at 13.7% highlight efficient capital usage.

Balance Sheet Strength: Debt-to-equity stands at just 0.02, with a current ratio of 3.57, underlining financial conservatism.

Although cash flow has shown volatility due to project cycles, the company’s strong balance sheet provides an ample buffer.

Also read : Jyoti CNC Poised for the Next Growth Phase

Valuation and Market View

At the current price of ₹38,170, HAIL trades at a P/E of 65.9, nearly double the industry average of 36.9. Its Price-to-sales ratio is also high at 7.65, and P/B at 8.34. These multiples suggest that the market already prices in strong growth and premium positioning.

While valuations appear stretched, two factors justify this premium:

High-Quality Business Model – Sticky service contracts, strong entry barriers, and critical system integration.

Global-Local Advantage – Access to Honeywell’s technology plus deep Indian execution capabilities.

That said, sustaining this premium will require consistent earnings growth, continued expansion in high-margin software and services, and deeper penetration into industries like healthcare and data centers.

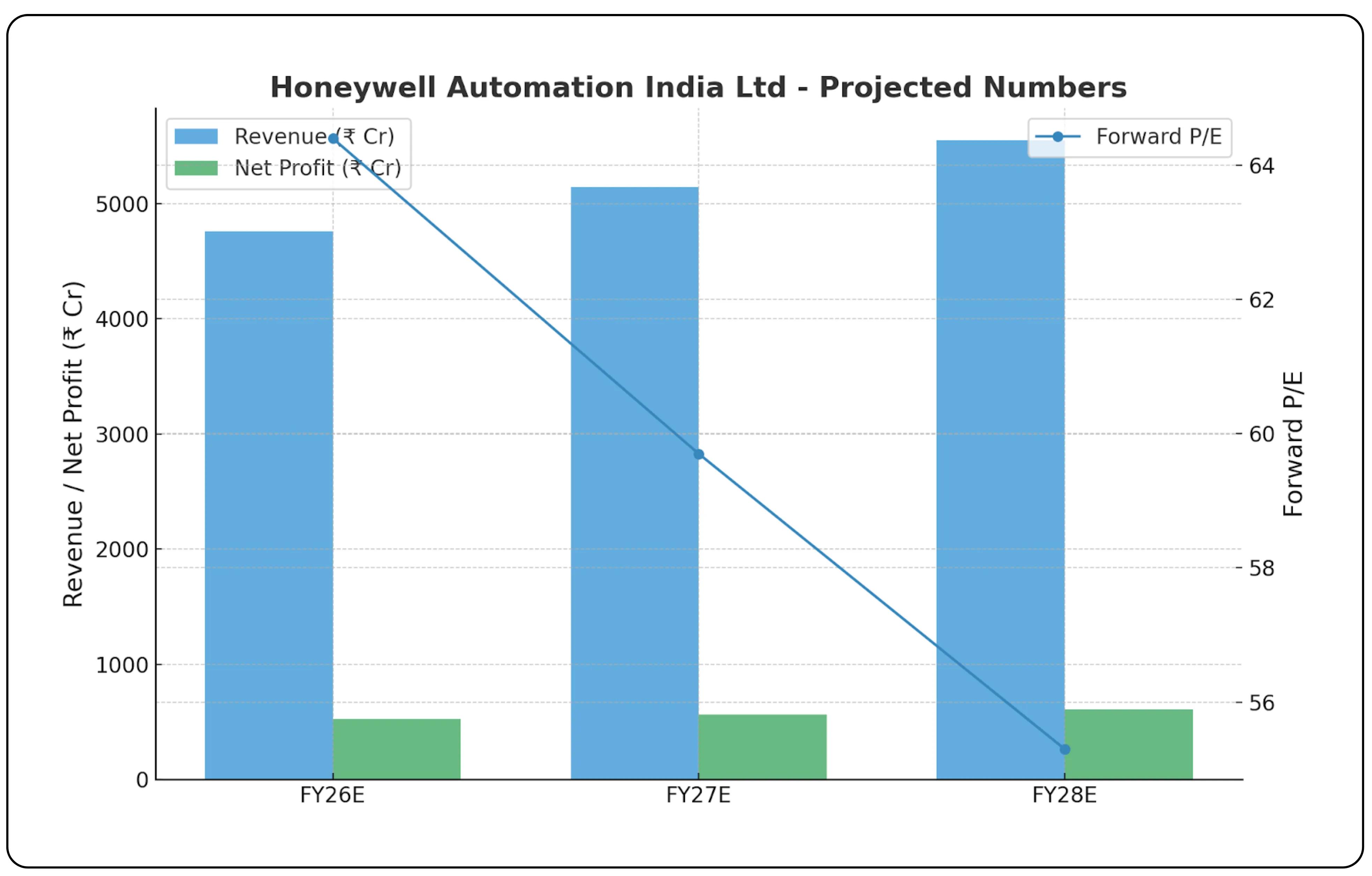

Forward Outlook & Valuation Compression Analysis

Assumptions:

Base FY25 sales: ₹4,190 crore; TTM: ₹4,412 crore

Conservative revenue growth: 8% CAGR over the next three years, increasing as digital and building automation take off

Operating margin recovery to stabilize at 14% by FY28 (vs 13% TTM)

Net profit margin steady near 11% by FY28

Constant current market price: ₹38,170

Projected Numbers:

| Year | Revenue (₹ Cr) | Net Profit (₹ Cr) | EPS (₹) | Forward P/E (at ₹38,170) |

|---|---|---|---|---|

| FY26E | 4,760 | 524 | 593 | 64.4x |

| FY27E | 5,141 | 565 | 639 | 59.7x |

| FY28E | 5,552 | 610 | 690 | 55.3x |

FY26E: Revenue grows ~8%, modest margin still, EPS yields a forward P/E near 64.4x.

FY27E: Mid-point revenue projection; margin improvement boosts net profit; forward P/E compresses to 59.7x.

FY28E: If growth and margins align, forward P/E would fall to 55.3x—much closer to, but still above the industry average.

Interpretation:

Honeywell usually trades at a premium given its moat. Despite current rich multiples, execution with sustained top-line growth and margin discipline could bring forward P/E down, making the valuation more reasonable, without requiring a share-price drop. Investors who pay today for structural quality would see a multiple re-rating purely from improved earnings.

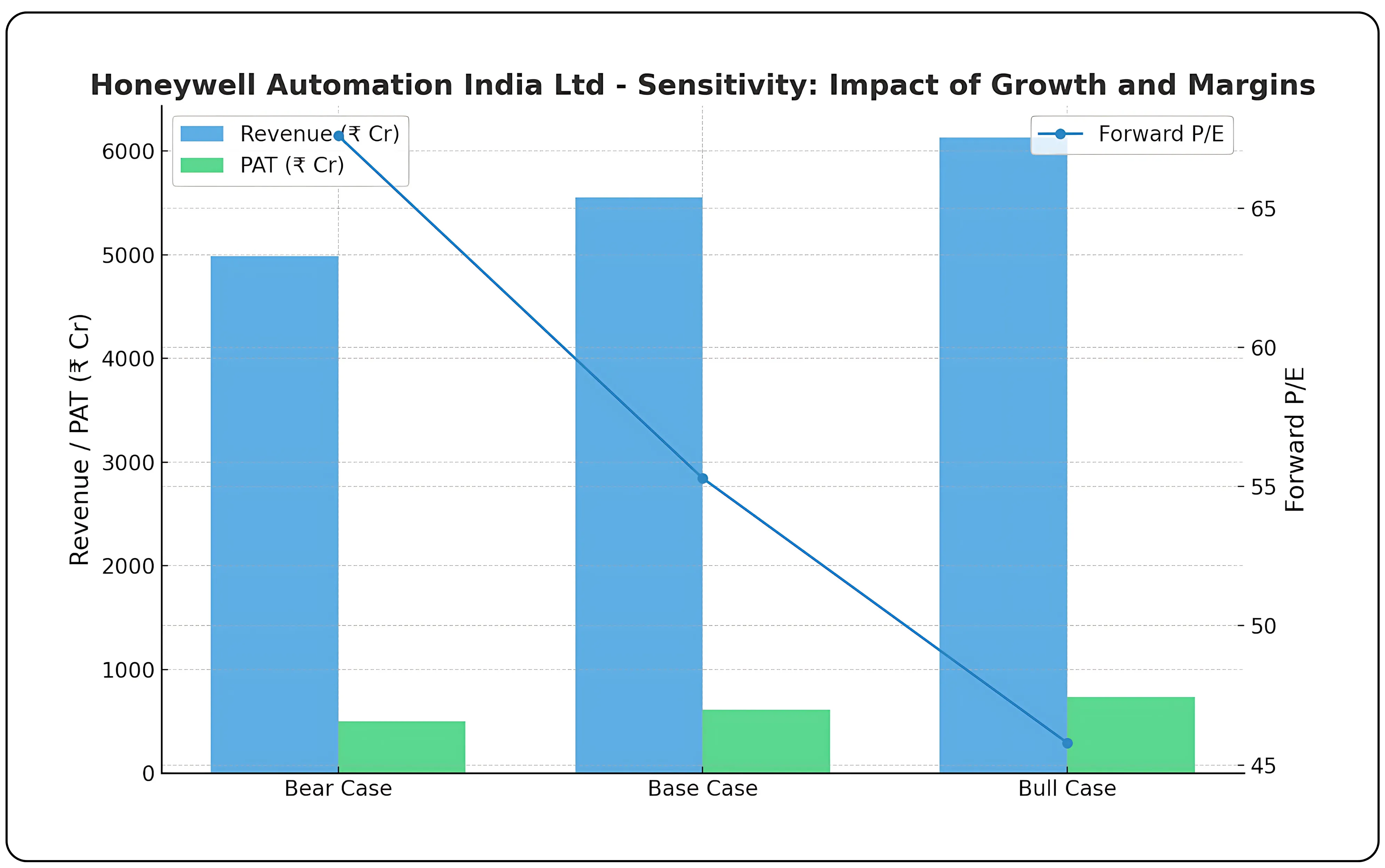

Sensitivity: Impact of Growth and Margins

| Scenario | Revenue CAGR (FY25–FY28) | Net Margin | FY28E Revenue (₹ Cr) | FY28E PAT (₹ Cr) | EPS (₹) | Forward P/E (₹38,170) |

|---|---|---|---|---|---|---|

| Bear Case | 6% | 10% | 4,988 | 499 | 565 | 67.6x |

| Base Case | 8% | 11% | 5,552 | 610 | 690 | 55.3x |

| Bull Case | 10% | 12% | 6,135 | 736 | 833 | 45.8x |

What this shows

If growth slows and margins slip (Bear Case), P/E stays high (~68x), leaving little room for rerating.

In the Base Case, execution drives EPS up, and valuation naturally compresses.

In a Bull Case, faster growth + better margins push EPS above ₹800, compressing P/E to below 46x, which could justify continued premium pricing.

Also read : Alkem Laboratories Riding on Resilient Growth

Risks and Challenges

High Valuation Risk: At ~66x earnings, any slip in execution could trigger valuation compression.

Project Cyclicality: Revenue depends on large industrial and infrastructure projects, which can face delays.

Competition: Global automation leaders and emerging Indian players are intensifying competition in key verticals.

Dependence on Parent: While Honeywell’s global ecosystem is a strength, it also creates dependence on group strategy and approvals.

Strategic Outlook

Looking ahead, three themes stand out for HAIL:

Digital Transformation – Rising demand for IoT, AI, and cloud-based automation creates opportunities for HAIL’s software-led solutions.

Green Energy & Sustainability – Efficiency, emissions reduction, and sustainable infrastructure will keep automation demand high.

India as a Hub – With local capacity, HAIL can serve both Indian customers and global affiliates more efficiently.

The capacity to scale software-driven revenues and leverage Honeywell’s global R&D will determine how far HAIL can stretch its already high valuations.

Key Takeaways

Honeywell Automation India is not a mass-market company, but it plays a critical role behind the scenes of India’s industrial and infrastructure backbone. Its technology makes airports safer, factories more efficient, and hospitals more reliable. The combination of global R&D access, local execution, and sticky service revenues gives it a durable competitive advantage.

At current levels, the stock reflects high growth expectations, leaving little room for error in the short-term. And for long-term investors focused on high-quality automation leaders, HAIL remains one of the strongest plays on India’s transition to smarter, safer, and more efficient industries.

Start your trading journey with CubePlus today and stay in control of your investments. [Sign up now] and trade smarter.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.