Before diving in, you can see how this company is doing now by reading our updated Q2 FY26 performance review — click here.

Alkem Laboratories is a leading pharmaceutical company in India, trusted by millions for both acute and chronic therapies, ranked fifth in the domestic formulations market. With a legacy spanning over five decades, Alkem has established itself as a trusted brand in both acute and chronic therapy segments. The company’s footprint spans 50+ countries, with a notable presence in the US, Australia, Europe, and other emerging markets. Its operations are supported by 19 state-of-the-art manufacturing facilities and strong R&D infrastructure across India and the US.

Business model and verticals

Alkem Laboratories Limited operates on a vertically integrated model encompassing development, manufacturing, and marketing of generics and biosimilars. Alkem company’s business is broadly segmented into Domestic Formulations, and CDMO (Contract Development and Manufacturing Organization) services. It has a well-diversified portfolio with a strong presence in therapy areas like anti-infectives, gastrointestinal, pain management, vitamins/minerals/nutrients (VMN), and expanding capabilities in chronic segments including anti-diabetic, neuro/CNS, dermatology, and urology. Additionally, the company has made strategic moves into biosimilars through Enzene and orthopaedic implants via Bombay Ortho.

Growth drivers

Alkem’s domestic growth was driven by tactical and structural changes including better field force deployment, therapy focus realignment, and improved coverage in high-potential geographies. Notably, it outperformed the Indian Pharmaceutical Market (IPM) in six of the top 11 therapies in FY25.

In the US, although price erosion and supply disruptions affected overall growth, the company expects mid-single-digit recovery in FY26 supported by 5–6 product launches and stabilized inventory levels. The biosimilar CDMO unit in the US is set to go operational by Q2 FY26 and is expected to generate ₹100 crore in revenue this year with full capacity potential of ₹450–₹500 crore in the next three years. Every department of Alkem lab involved in R&D and CDMO is equipped with global-standard capabilities, driving future innovations.

Strategic acquisitions like Adroit Biomed (derma) and Bombay Ortho (MedTech) are expected to strengthen Alkem’s footprint in chronic and specialty verticals.

Industry outlook

The Indian pharmaceutical market is projected to grow 7–8% annually, supported by rising healthcare access, chronic disease burden, and higher penetration of branded generics. While the acute segment is showing cyclical recovery, chronic therapies continue to gain structural tailwinds. Globally, generic drug makers face pricing pressure, but opportunities in complex generics, biosimilars, and CDMO services offer long-term potential.

Also read: Biocon Limited’s Strategic Growth in Generics, Biosimilars & Research Services

Competitive advantage

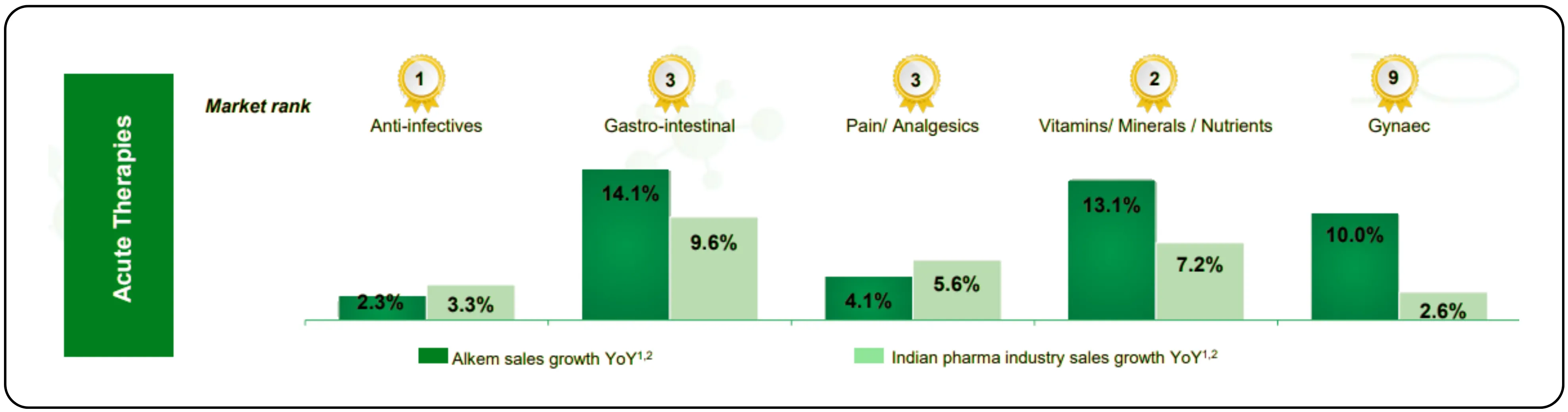

Acute Therapies

| Segment | Alkem Sales Growth | Est. Profit Margin | Margin Comments |

|---|---|---|---|

| Anti-infectives (Rank #1) | 2.3% | 12–15% | Highly competitive, margin-eroding due to commoditization |

| Gastro-intestinal (Rank #3) | 14.1% | 18–22% | Strong margin segment due to chronic usage & brand stickiness |

| Pain/Analgesics (Rank #3) | 4.1% | 14–17% | Generic-heavy, moderate margin with volume play |

| Vitamins/Minerals/Nutrients (Rank #2) | 13.1% | 25–30% | Excellent margins, often sold as branded supplements/OTC |

| Gynaec (Rank #9) | 10.0% | 18–20% | Good margins due to brand loyalty and niche formulations |

Alkem’s edge lies in its leadership in acute therapies (rank #1 in anti-infectives) and growing strength in chronic categories. The company is ranked third in prescription share among Indian doctors and has improved rankings in anti-diabetic, respiratory, and urology segments. Its balance sheet strength and cash reserves provide flexibility to invest in innovation and inorganic opportunities.

The company's wide domestic distribution network (13,000 medical representatives), therapeutic depth, strong compliance record (no critical observations across USFDA sites), and focus on high-margin specialty products and international diversification are structural strengths.

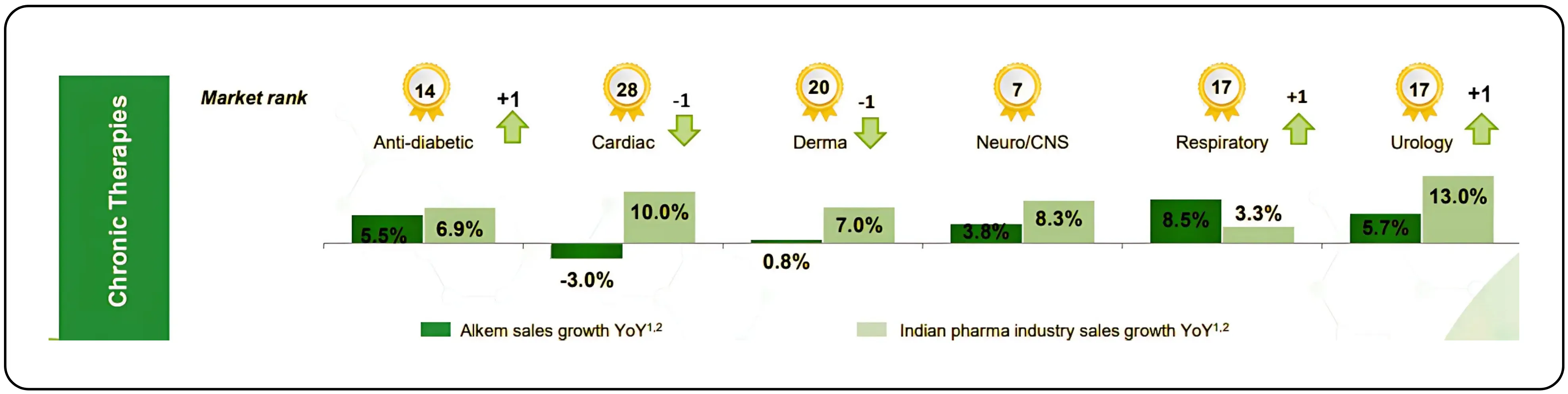

Chronic Therapies

| Segment | Alkem Sales Growth | Est. Profit Margin | Margin Comments |

|---|---|---|---|

| Anti-diabetic (Rank #14) | 5.5% | 16–20% | Moderate margin, branded generics facing pricing pressure |

| Cardiac (Rank #28) | -3.0% | 12–15% | Very competitive, branded generics with price control challenges |

| Derma (Rank #20) | 8.0% | 25–35% | High margins due to cosmetic/OTC overlap and low price regulation |

| Neuro/CNS (Rank #7) | 3.8% | 18–22% | Long-term therapy, moderately good margin |

| Respiratory (Rank #17) | 8.5% | 22–26% | Inhaler/device-based therapies fetch higher margins |

| Urology (Rank #17) | 5.7% | 20–24% | Specialty drugs with relatively high pricing flexibility |

FY25 financial highlights

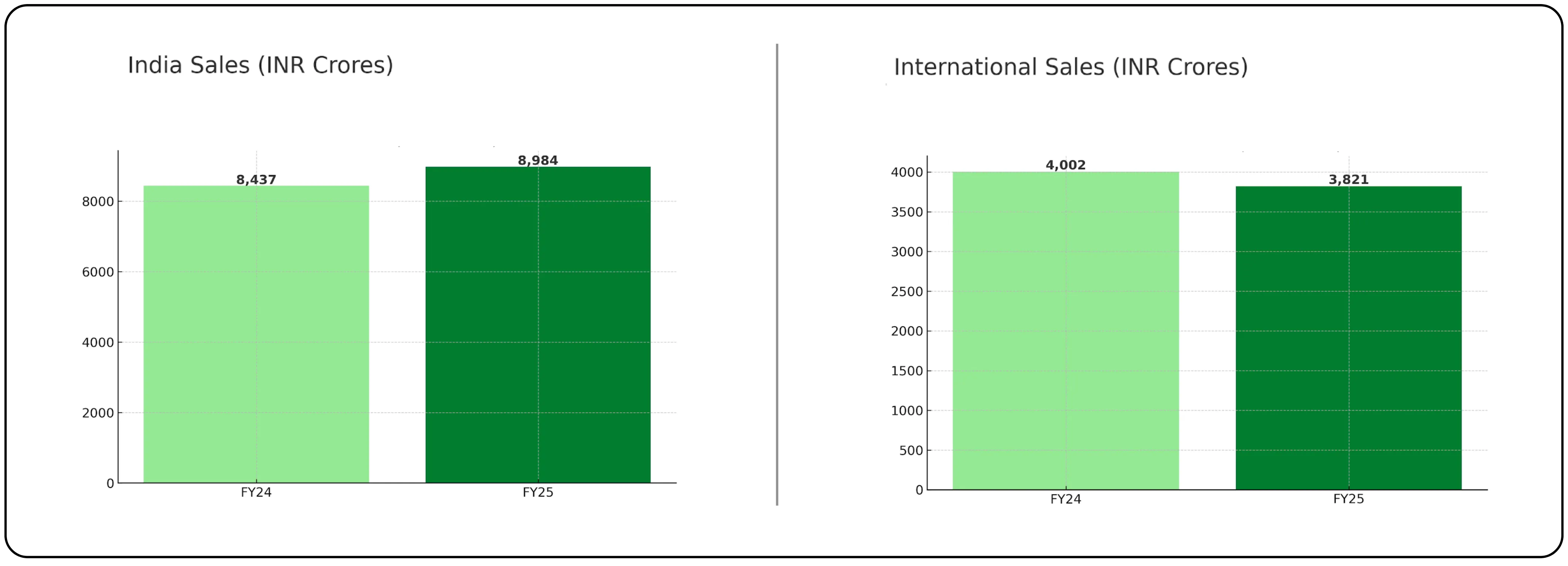

Alkem Labs Ltd reported a 2.3% year-on-year growth in revenue from operations at ₹12,965 crore in FY25. India business, which contributes over 70% of total revenue, grew 6.5% YoY, supported by improved performance in key therapies like gastrointestinal (11.4%), VMN (12.7%), and neuro/CNS (11.4%). International business saw a 4.5% decline, primarily driven by a 10.4% de-growth in the US. However, ex-US markets like Australia and Europe delivered good growth of 8.7%.

EBITDA grew to ₹2,512 crore, with margin expansion to 19.4% (which means for every 100 sales company earned operating profit of Rs 19) driven by better operational leverage and cost control. Net profit rose to ₹2,215 crore. R&D investments stood at ₹562 crore (4.3% of revenue), reflecting the company’s focus on pipeline development across regulated and emerging markets.

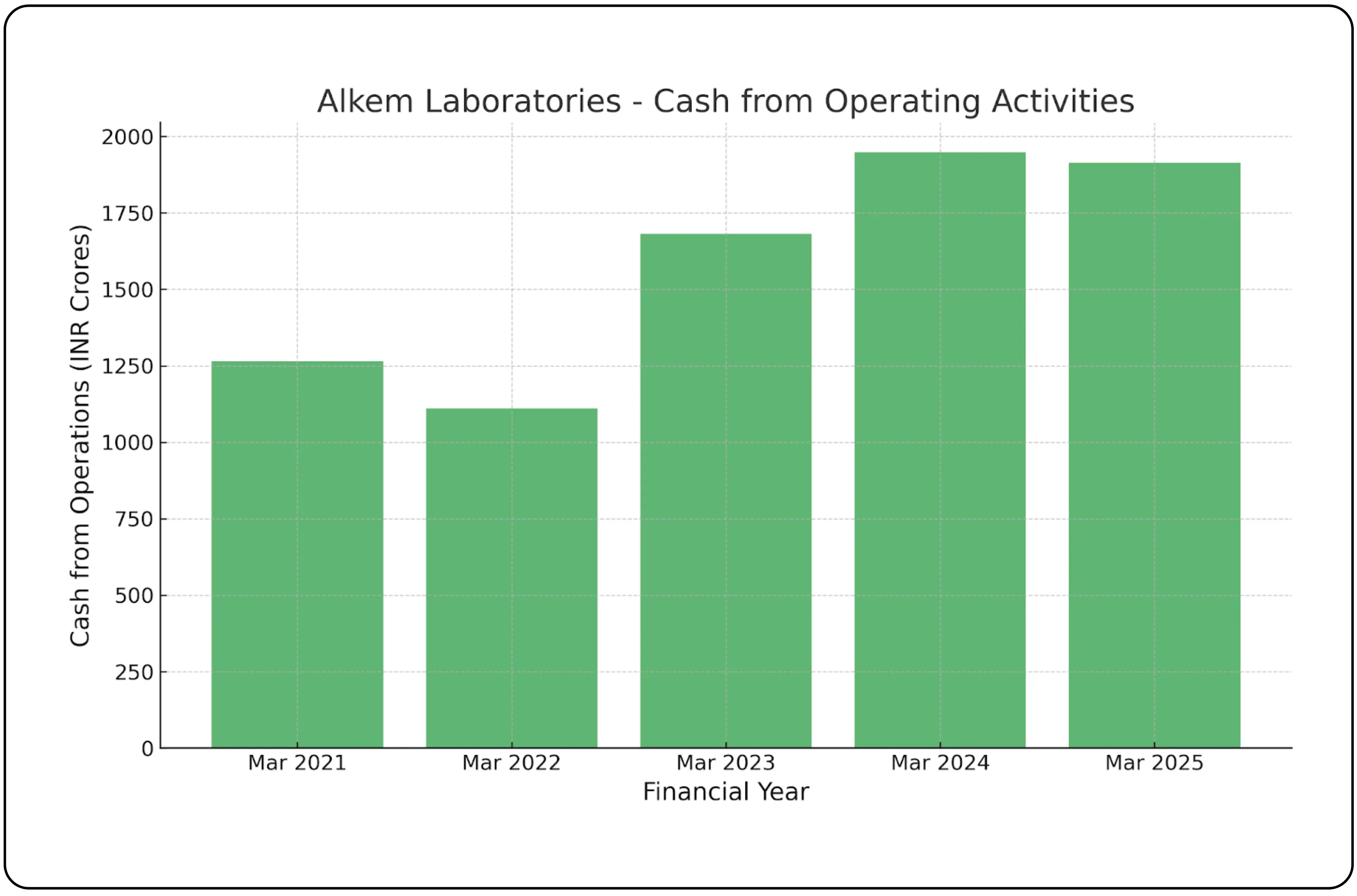

Cash flows from operating activities have been steady and growing for Alkem Laboratories.

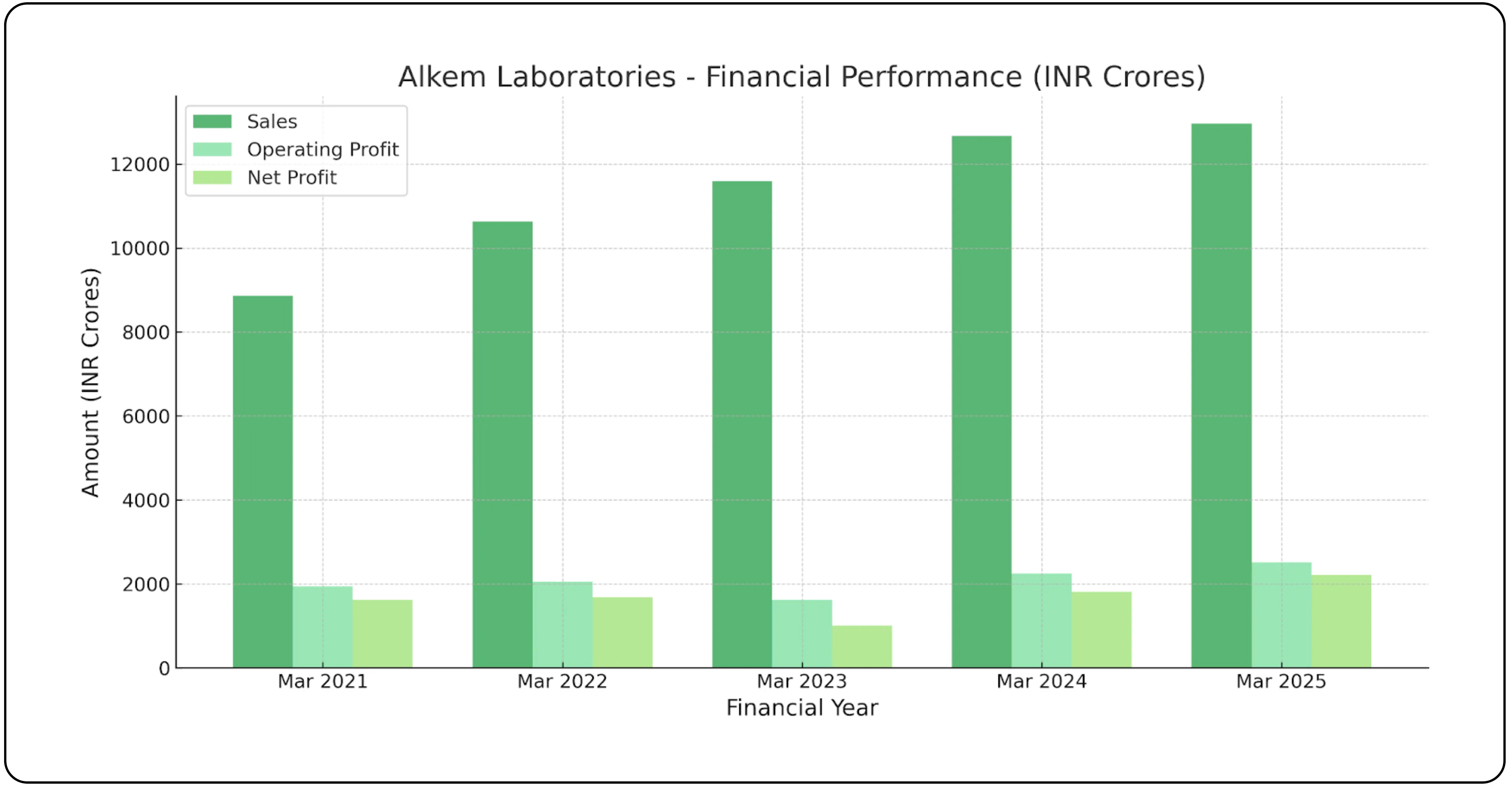

Five years financial snapshot

| Year | Sales (₹ Cr) | Operating Profit (₹ Cr) | Net Profit (₹ Cr) |

|---|---|---|---|

| Mar 2025 | 12,965 | 2,510 | 2,215 |

| Mar 2024 | 12,668 | 2,249 | 1,811 |

| Mar 2023 | 11,599 | 1,622 | 1,007 |

| Mar 2022 | 10,634 | 2,054 | 1,680 |

| Mar 2021 | 8,865 | 1,945 | 1,618 |

The financial performance of Alkem Laboratories over the last five years reflects consistent growth in topline and a notable recovery in profitability in the most recent fiscal year.

In FY25, the company reported sales of ₹12,965 crore, a modest increase from ₹12,668 crore in FY24. While revenue growth has moderated in recent years compared to the sharp rise during FY21 to FY23, the company has managed to improve its operating and net profitability significantly. Operating profit stood at ₹2,510 crore in FY25, marking the highest level in five years and a meaningful jump from ₹2,249 crore in FY24. This expansion in operating profit is driven by better cost efficiencies and improved product mix.

Net profit also showed a sharp recovery, increasing to ₹2,215 crore in FY25 from ₹1,811 crore in FY24 and more than doubling from ₹1,007 crore in FY23. This rebound in bottom-line performance highlights improved operational leverage and better margin control, especially after a relatively weak FY23, which saw a dip in both operating and net profit.

Also read: Assessing Valuation and Opportunity in Tata Chemicals

Valuation perspective

Alkem is currently trading at a trailing P/E of 27.1x, which is at a discount to the industry average of 32.6x. Given the management’s commentary of sustaining EBITDA margins at 19.5%, and targeting mid- to high-single-digit growth in FY26 and the company aims to move towards double-digit growth in FY27.

Assuming an 8% growth in earnings for FY26, Alkem’s net profit is projected to reach approximately ₹2,392 crore, translating to an estimated EPS of ₹191.2. At the current market price, this implies a forward P/E of about 25.1x for FY26. Looking ahead to FY27, with a 12% growth over FY26, net profit could rise to ₹2,679 crore, leading to an EPS of ₹214.1 and an implied P/E of roughly 22.4x, assuming the share price remains constant. What this indicates is a clear trajectory of valuation compression over the next two years. As earnings expand and the price holds steady, Alkem becomes relatively cheaper on a forward basis. The drop in implied P/E from 27.1x in FY25 to 22.4x by FY27 suggests that much of the anticipated growth is not yet fully priced in, offering a reasonable margin of safety for long-term investors if the company delivers on its earnings trajectory.

The bottom line

Alkem labs stands on solid ground with a strong domestic franchise, improving margins, and a well-diversified product mix across acute and chronic therapies. Despite near-term headwinds in the US generics business, the company's focus on operational efficiency, portfolio expansion, and investments in biosimilars and CDMO are likely to drive medium- to long-term growth. With consistent cash generation, minimal leverage, and a forward valuation that looks increasingly attractive, Alkem offers a compelling case for investors seeking steady earnings growth with downside protection. If the management delivers on its growth outlook, the stock’s valuation could re-rate, or at the very least, offer meaningful returns through earnings compounding.

Alkem Laboratories continues to make waves in the market. Don’t miss out on the opportunities ahead. Start your trading journey with CubePlus today and stay in control of your investments. [Sign up now] and trade smarter.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.