Before diving in, you can see how this company is doing now by reading our updated Q2 FY26 performance review — click here.

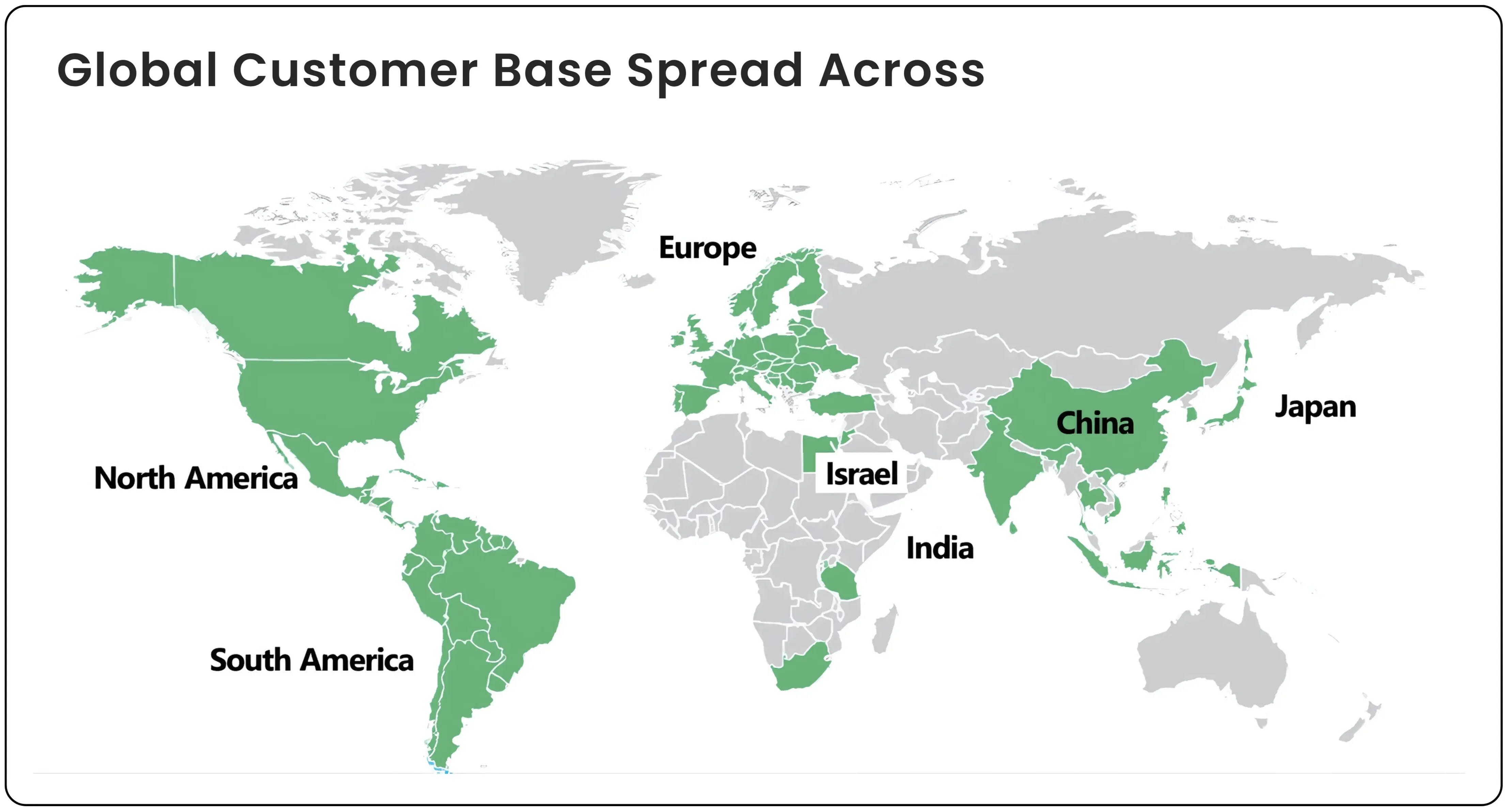

Acutaas Chemicals Ltd, formerly known as Ami Organics, is a manufacturer of specialty chemicals and pharmaceutical intermediates (key ingredients used in drug production). Its portfolio includes custom synthesis (creating molecules tailored to specific customer needs), contract manufacturing, and New Chemical Entities (NCEs are innovative compounds that can lead to the development of future drugs), which support innovation in future drug development. Through the acquisition of Gujarat Organics’ facilities in Ankleshwar and Jhagadia, the company has also entered the agrochemical, cosmetics, and polymer segments. With exports to over 27 countries across the Americas, Europe, and Asia. Acutaas continues to support global healthcare by delivering advanced intermediates and building long-term partnerships through flexible, quality-focused operations.

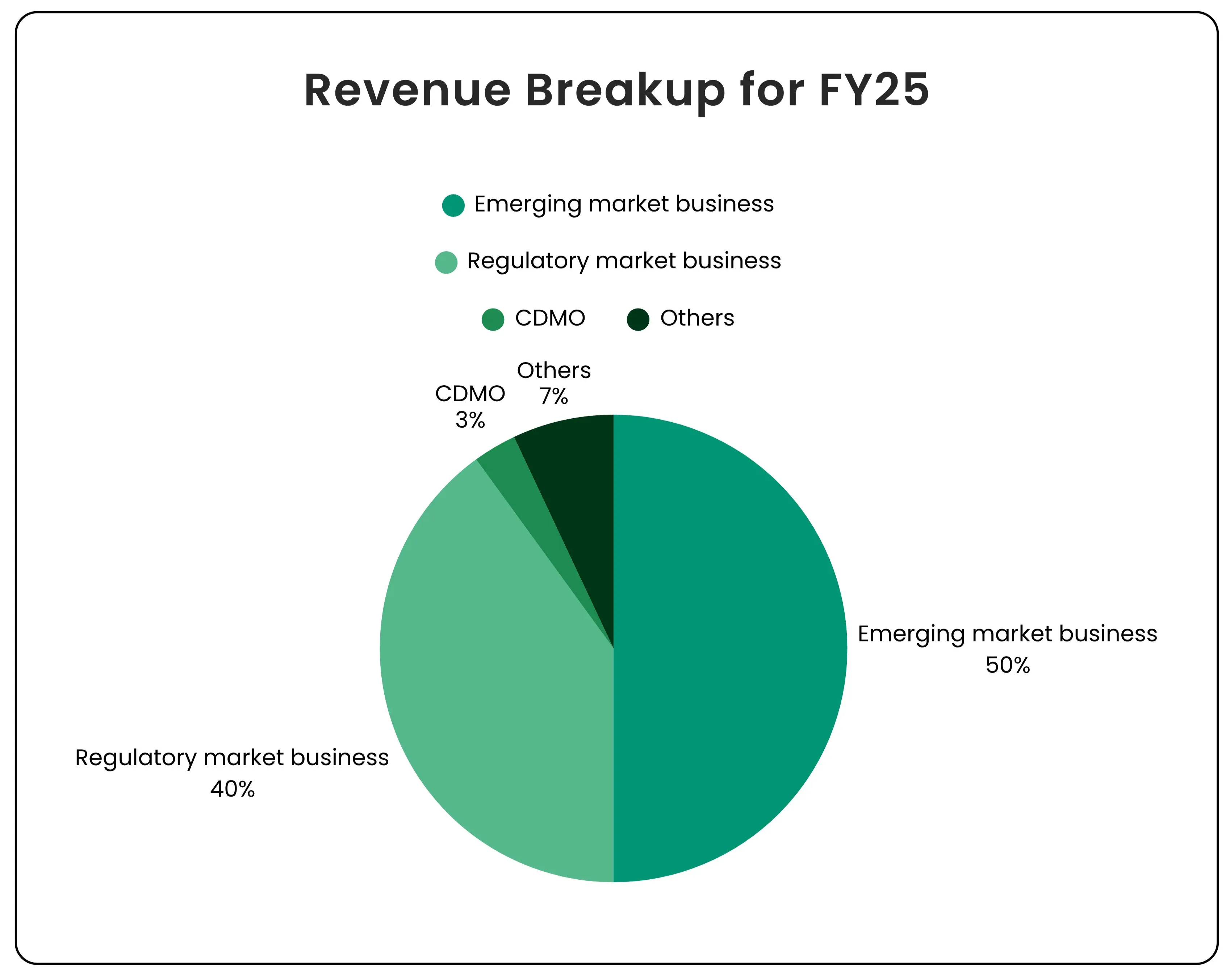

Revenue mix

Emerging Markets (50%) Supplies intermediates to generic API makers. Leverages cost efficiency and first-mover advantage in competitive regions.

Regulated Markets (40%) Supplies NCEs and intermediates to innovator pharma companies for patented and off-patent drugs, ensuring a strong presence in regulated geographies.

CDMO (3%) Engages in contract manufacturing through long-term deals with large pharma players. Strategic segment with high growth potential.

Others (7%) Comprises ancillary activities that support core operations.

Core business activities

Pharma Intermediates Develops and manufactures high-value intermediates for regulated and generic APIs across therapies like HIV, oncology, CNS disorders, and cardiovascular diseases. Also supports New Chemical Entities (NCEs) for innovator pharma clients.

Specialty Chemicals Offers chemicals used in agro, cosmetics, and polymer industries—including parabens, salicylic acid, and additives for personal care, dyes, animal feed and other industrial chemicals.

Export-driven Significant global footprint with strong exports across North America, Europe, and Asia, alongside domestic sales.

Revenue streams

Product sales: Revenue is primarily generated through the sale of pharmaceutical intermediates and specialty chemicals to pharma companies, agrochemical firms, and consumer goods manufacturers.

Custom synthesis and contract manufacturing: Acutaas also offers custom synthesis and contract manufacturing services, particularly for pharma companies developing new drugs or requiring specialized chemical intermediates.

Also read: Senores Pharma Capitalizing on CDMO Tailwinds for Global Ascent

Key business model features

R&D focus: A significant part of Acutaas’s business model is its investment in research and development, enabling the company to develop high-value, complex intermediates and specialty chemicals, often for niche or high-growth therapeutic areas including biotech-driven formulations.

Diversification: While pharma intermediates are the core, diversification into specialty chemicals for other industries (agro, cosmetics, polymers) helps mitigate sector-specific risks.

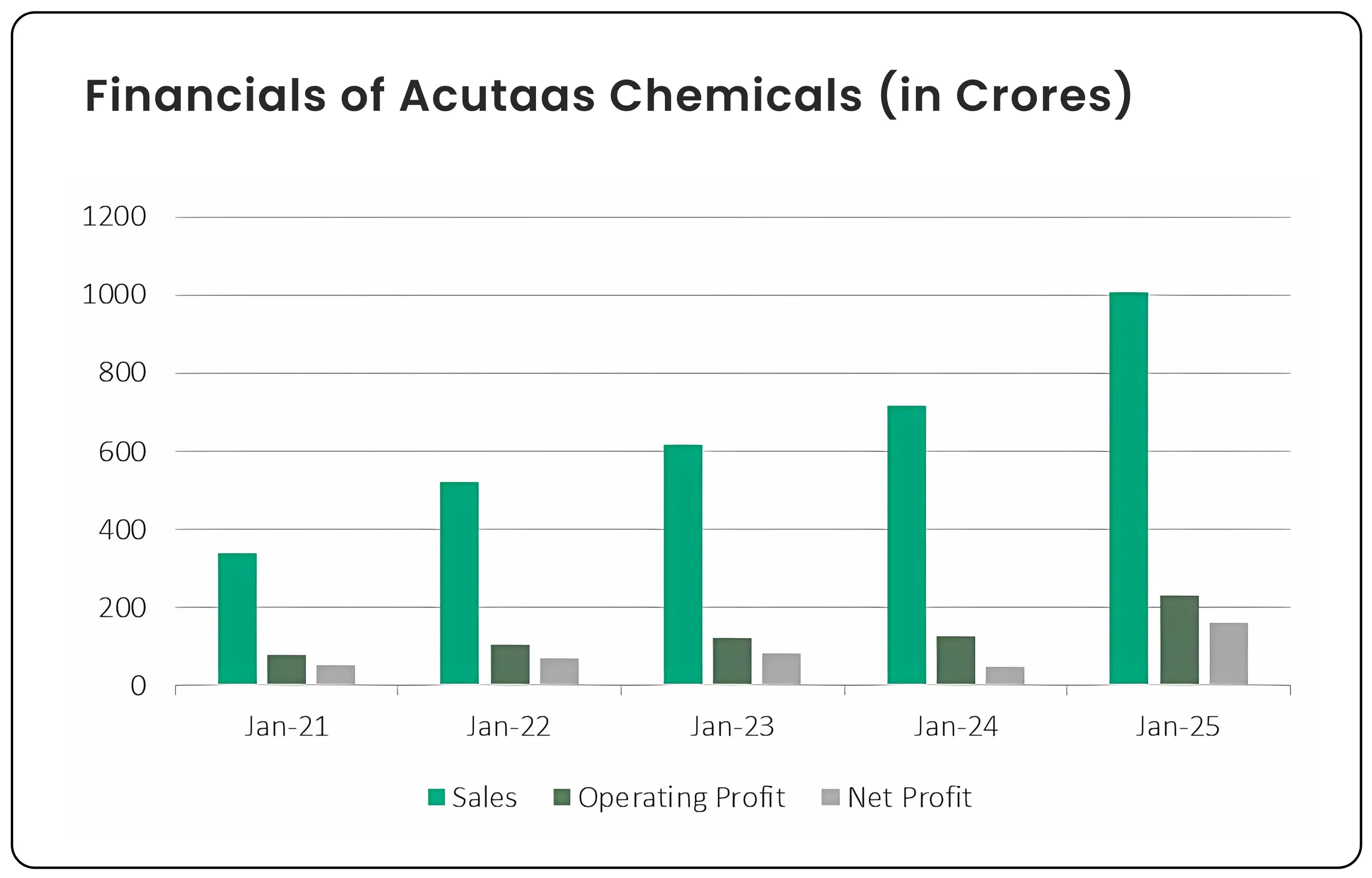

Consolidated financial performance (FY21–FY25)

Operational efficiency: Acutaas Chemicals has demonstrated good financial growth, with net sales growing from ₹340.61 crores in March 2021 to ₹1,006.88 crore in March 2025, and net profit rising from ₹54 crores to ₹158.71 crores in the same period. This reflects both expansion and improved operational efficiency.

Low leverage: The company operates with a low debt-to-equity ratio, indicating a conservative approach to financial risk.

Strong institutional support: The company has high institutional holdings (over 30%), which suggests confidence from mutual funds and foreign institutional investors.

Acutaas Chemicals delivered consistent growth across key metrics:

Revenue rose from ₹341 Cr in FY21 to ₹1,007 Cr in FY25 — a ~195% increase.

Operating Profit grew from ₹80 Cr to ₹232 Cr (~190%), driven by better cost control and efficiency.

Net Profit surged from ₹54 Cr to ₹160 Cr (~196%), despite a dip in FY24 (₹49 Cr). The company bounced back sharply in FY25 with a 226% YoY jump in profit.

The numbers reflect expanding scale, margin discipline, and resilience in navigating short-term challenges.

Industry outlook

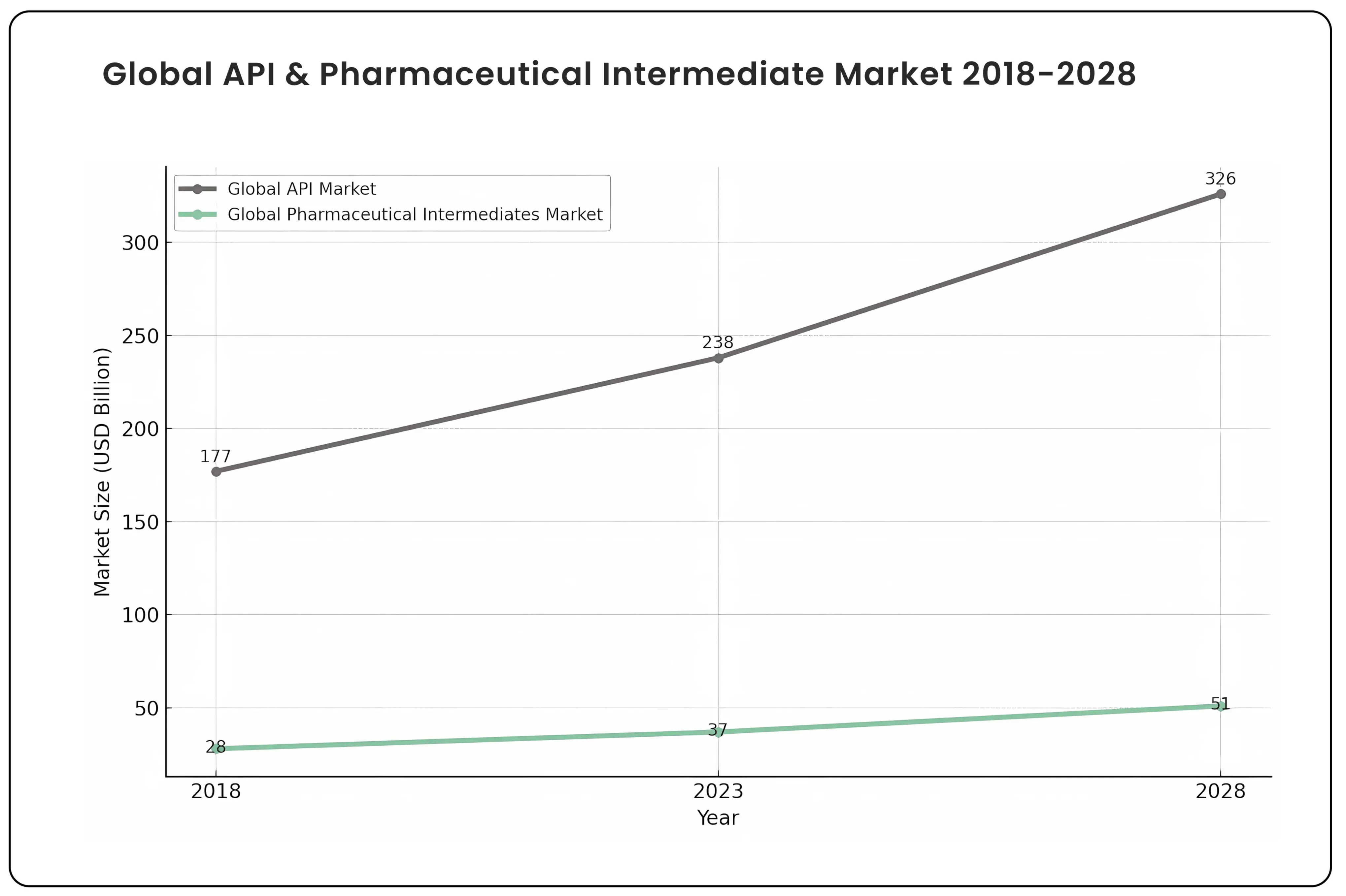

Global API market

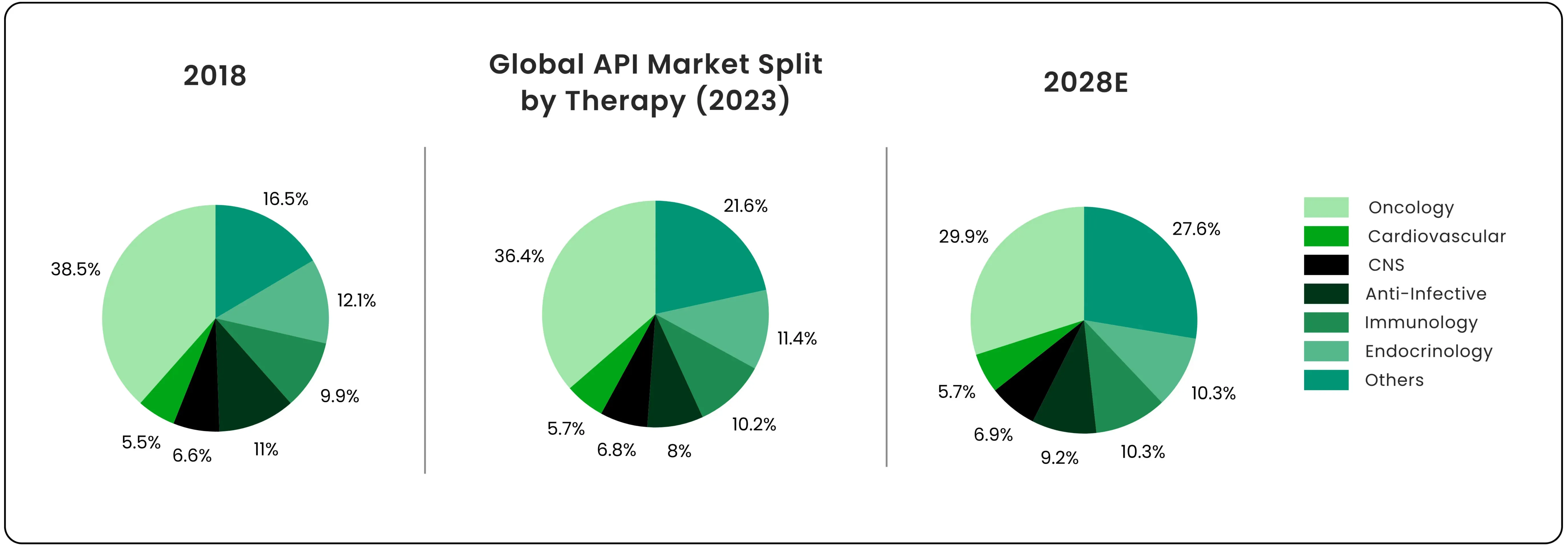

The Active Pharmaceutical Ingredients (API) market is witnessing steady growth, rising from USD 177 billion in 2018 to USD 238 billion in 2023, and projected to reach USD 326 billion by 2028 (CAGR: 6.5%). This growth reflects increasing global demand for drug formulations, especially in oncology, cardiovascular, and neurological therapies.

Pharmaceutical Intermediates—the building blocks of APIs—also show consistent growth, expanding from USD 28 billion in 2018 to USD 51 billion by 2028 (CAGR: ~6.2%).

Key Therapy Trends

Oncology leads the API market with double-digit growth (CAGR: 11%), expected to remain dominant despite slight market share reduction.

Cardiovascular, CNS, immunology, and Parkinson’s therapies are gaining momentum with stable to rising CAGRs (5–9%).

There's a visible shift from generic APIs toward targeted and specialized therapies.

Specialty Chemicals market

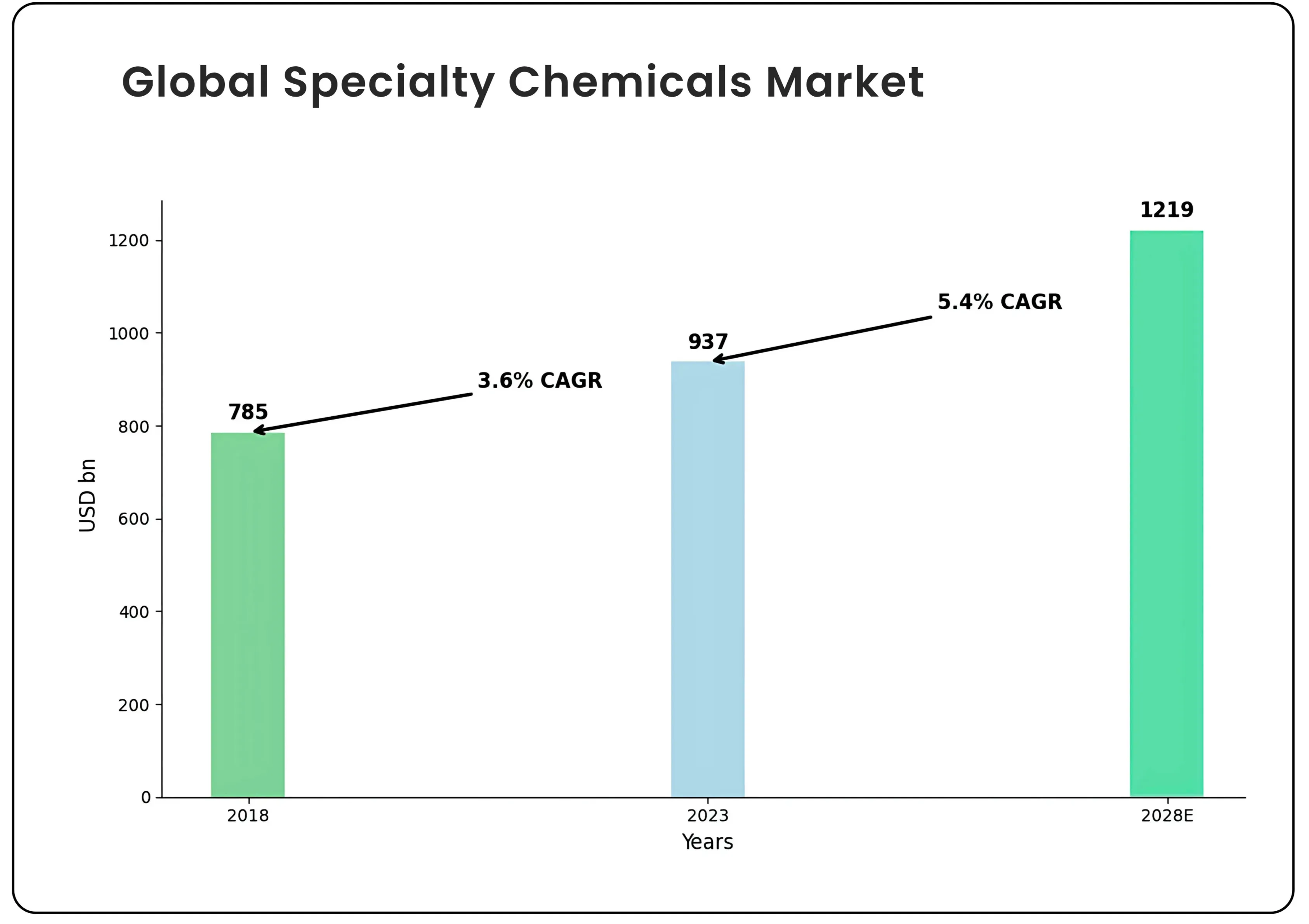

The global specialty chemicals industry grew from USD 785 billion in 2018 to USD 937 billion in 2023, and is expected to touch USD 1,219 billion by 2028 (CAGR: 5.4%). This reflects broad-based demand across pharmaceuticals, electronics, and energy sectors.

Emerging segments

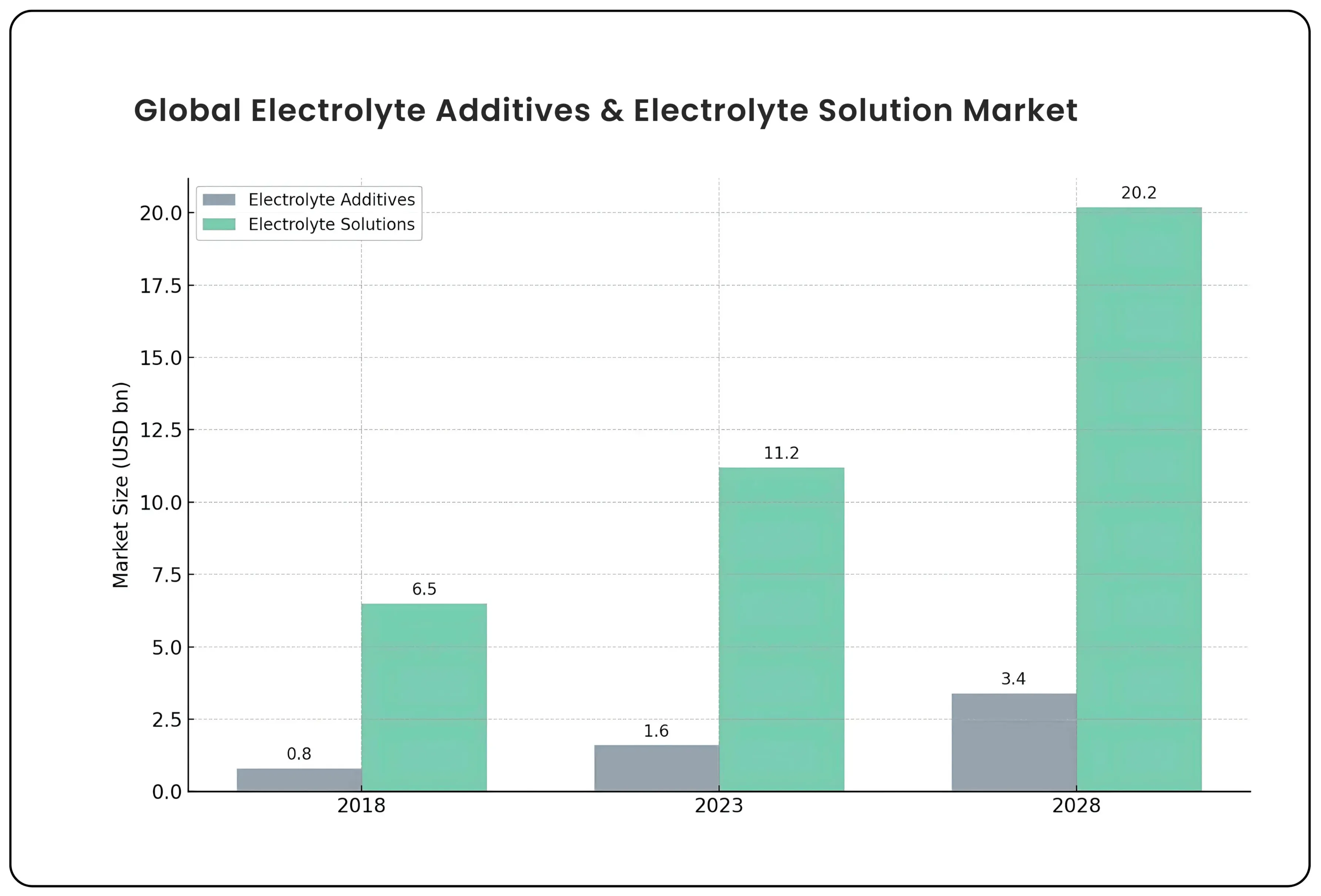

- Electrolyte Solutions & Additives (used in batteries) are among the fastest-growing sub-sectors, with CAGRs of 11–16% driven by EV and energy storage demand

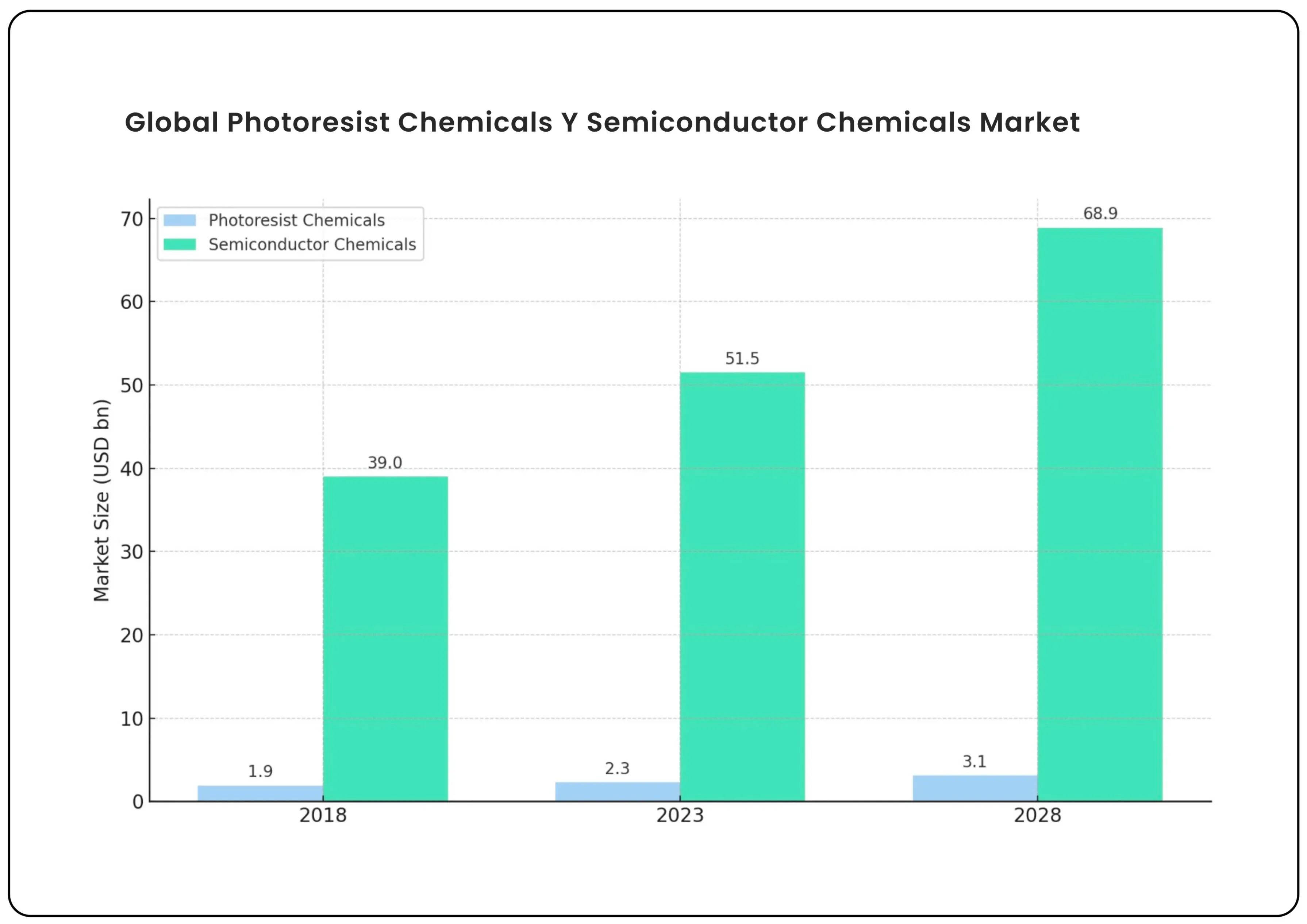

- Semiconductor Chemicals and Photoresists are also expanding steadily (CAGR: ~5–6%), supporting the digital and electronics boom.

Also read: Praveg Ltd. Positioned for Margin Expansion and Long-Term Profitability

Acutaas’ growth outlook (FY26–FY28)

Sales growth:

FY25 Sales: ₹1,006.9 Cr

Guided FY26 Sales Growth: 25% YoY, continuing a consistent long-term trend.

- This implies FY26E Sales ≈ ₹1,258 Cr

Management reaffirmed its track record of 15 years of maintaining this CAGR.

Growth to be driven by:

Expansion in the CDMO (Contract Development and Manufacturing) business.

Operational ramp-up at chemical plants at Ankleshwar and Jhagadia plants.

Electrolyte additives and semiconductor chemicals are expected to contribute from H2 FY26 onwards.

Profitability outlook:

FY25 PAT: ₹160.4 Cr (YoY growth: nearly 2×)

Expected margin expansion in FY26, though H1 will be seasonally softer.

EBITDA margins in FY25: 23% overall

FY26 margins are expected to be higher, supported by improved operating leverage and a more favorable product mix.

Valuation: Implied PE estimation based on growth

Current market metrics

| Metric | Value |

|---|---|

| Market Cap | ₹9,188 Cr |

| PAT (FY25) | ₹160.4 Cr |

| Reported PE | ~57.9x |

| Industry PE | ~33.3x |

Projected PAT for FY26 (Assuming 25% Growth)

Estimated PAT FY26E ≈ ₹200.5 Cr

Implied Forward PE (Based on Current Price):

Forward PE = ₹9,188 Cr / ₹200.5 Cr = 45.8 x

Interpretation:

Even after assuming 25% PAT growth, the forward PE remains elevated at ~46x.

This implies premium valuation, reflecting:

High earnings visibility.

Strong CDMO growth trajectory.

Expansion into high-value specialty chemicals like electrolytes and semiconductors.

If industry mean PE (33.3x) is applied to FY26E PAT, the fair value market cap would be:

₹200.5 x 33.3 = ₹6,676 Cr

Current valuation suggests ~38% premium to peers, which would be justified only if the 25%+ CAGR sustains beyond FY26 into FY28, particularly from CDMO and specialty chemical ramp-up.

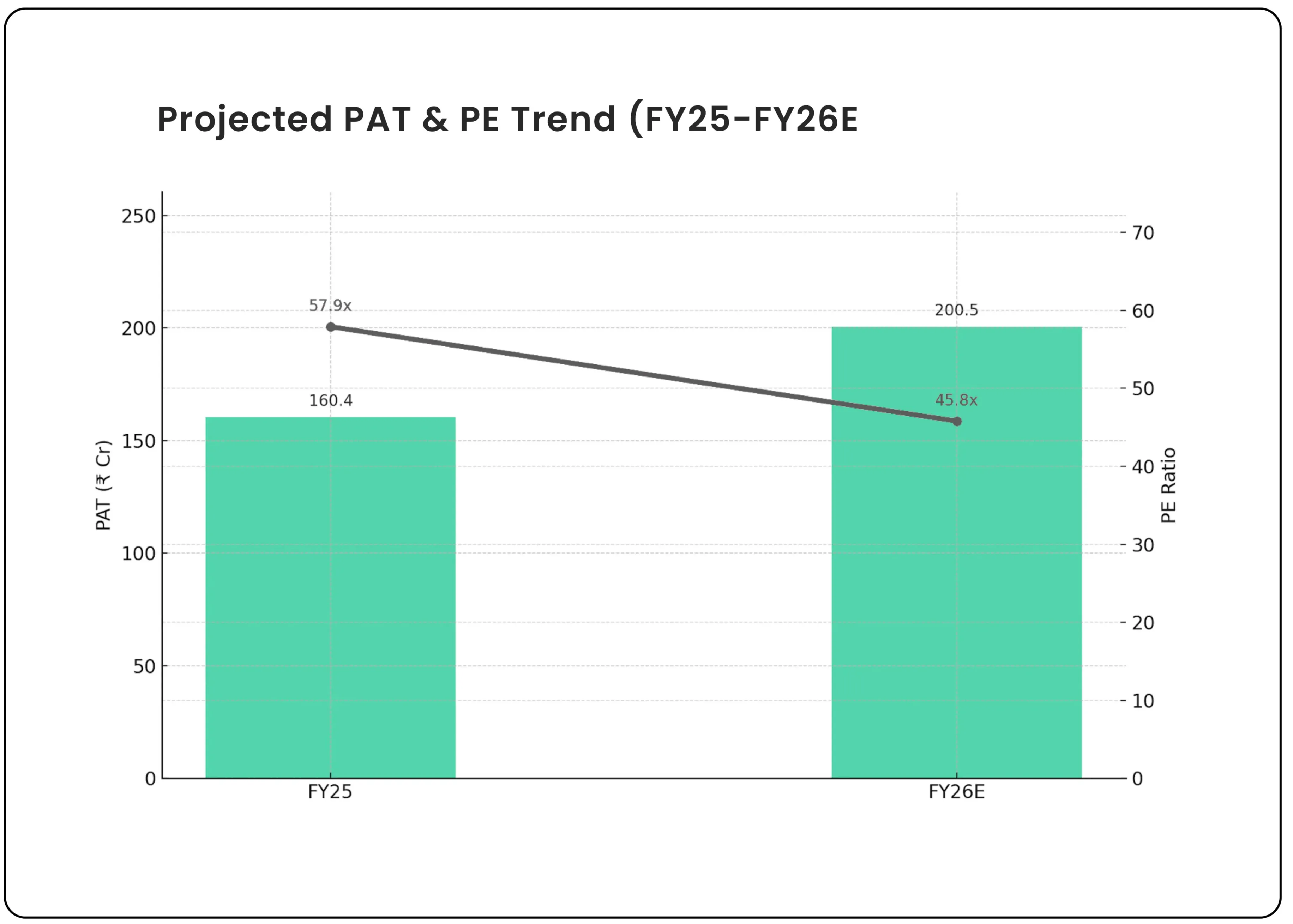

Here is the graphical representation of PAT and PE trends for Acutaas Chemicals Ltd:

The blue bars represent Profit After Tax (PAT), rising from ₹160.4 Cr in FY25 to a projected ₹200.5 Cr in FY26.

The orange line shows the corresponding PE ratio, which is expected to decline from 57.9× to 45.8×, indicating valuation compression as earnings catch up to the stock price.

Acutaas Chemicals Ltd is steadily building a strong position in the specialty chemicals and CDMO space. With a proven track record in pharmaceutical intermediates, the company is now expanding into fast-growing areas like electrolyte additives and semiconductor chemicals. Its consistent sales growth, focus on R&D, and low debt levels reflect solid execution. The company is emerging as one of India’s high-potential specialty chemical companies, backed by a diversified model, expanding R&D, and global market access.

While current valuations are on the higher side, continued performance through plant ramp-ups, margin improvement, and CDMO expansion will be key. Overall, Acutaas presents a promising long-term growth story backed by a diversified business model and increasing global relevance.

Also read: Capacit’e Infraprojects Unlocking Urban Growth

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.