In our previous blogs, we went deep into each of these five companies, examining what drives their businesses and where their growth was supposed to come from. With Q2 FY26 results now available, this review reconnects those original insights with the actual numbers to understand who’s delivering and who still has work to do. Now the overall story is still the same, but the confidence level varies from stock to stock. Three companies have clear validation in the numbers, one needs H2 execution, and Laurus has reinforced its thesis with scale and a clear CDMO momentum.

1) Entero Healthcare Solutions

To understand the full thesis behind Entero Healthcare Solutions, revisit our complete fundamental report here.

Earlier thesis: Entero was positioned as a scale-driven healthcare distributor with improving margins, aided by higher-value categories like MedTech, trade generics, and a steady inorganic strategy. The core expectations were improved operating cash flow, reduced working capital days, and faster market share capture.

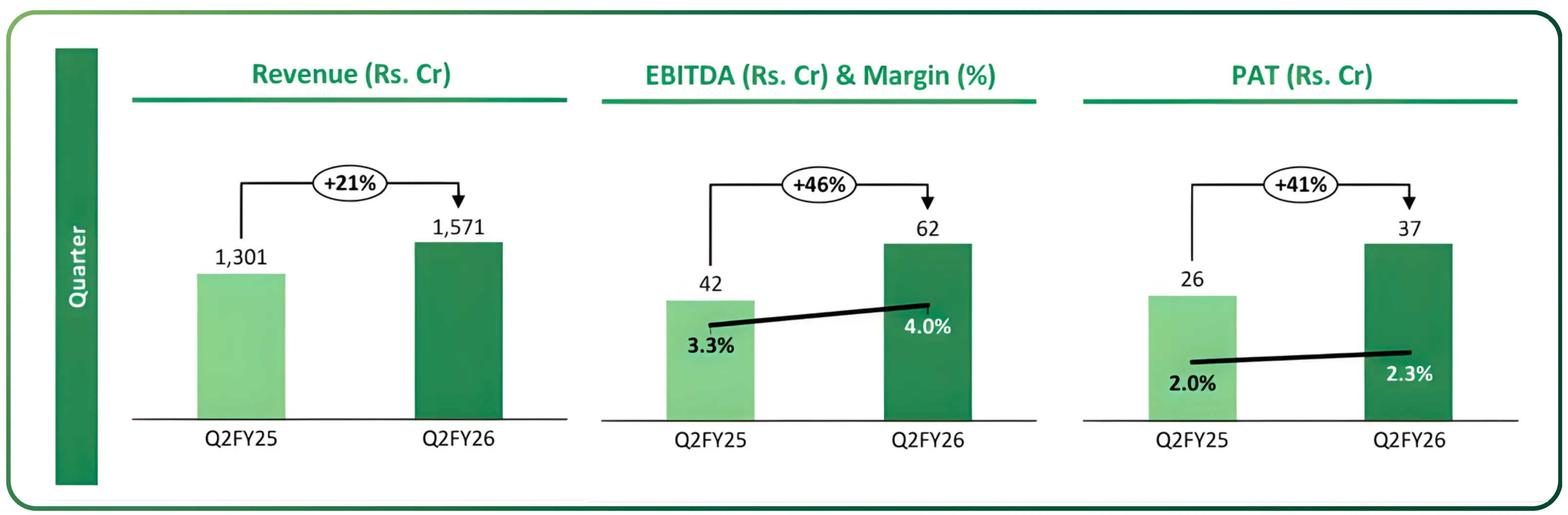

Q2 FY26 performance

- Revenue came in at ₹1,571 crore, up 20.8% YoY, with organic growth at 13%.

- EBITDA margin improved to 4%, up both sequentially and YoY.

- PAT grew to 37 crores, aided by operational improvements.

- Working-capital days reduced to 63, the best improvement trend since listing.

- MedTech expansion continues: seven acquisitions in motion, expected to add over ₹1,000 crore proforma revenue.

Are they delivering what they projected?

Entero Healthcare’s revenue growth is good but short of the full-year guidance unless the inorganic deals close on time. Margin improvement is clearly visible, but the larger margin jump expected from MedTech will only kick in after integration.

What to watch in H2:

- Speed of deal closures and integration

- GST-related cash flow benefits

- Entry barriers in MedTech and whether the portfolio lifts EBITDA as guided

2) Senores Pharmaceuticals

To understand the full thesis behind Senores Pharmaceuticals, revisit our complete fundamental report here.

Earlier thesis: Senores was emerging as a high-growth CDMO + ANDA-led player with early signs of operating leverage. Strong US presence, a rising ANDA pipeline, and branded generics in India were expected to propel FY26 and FY27 growth.

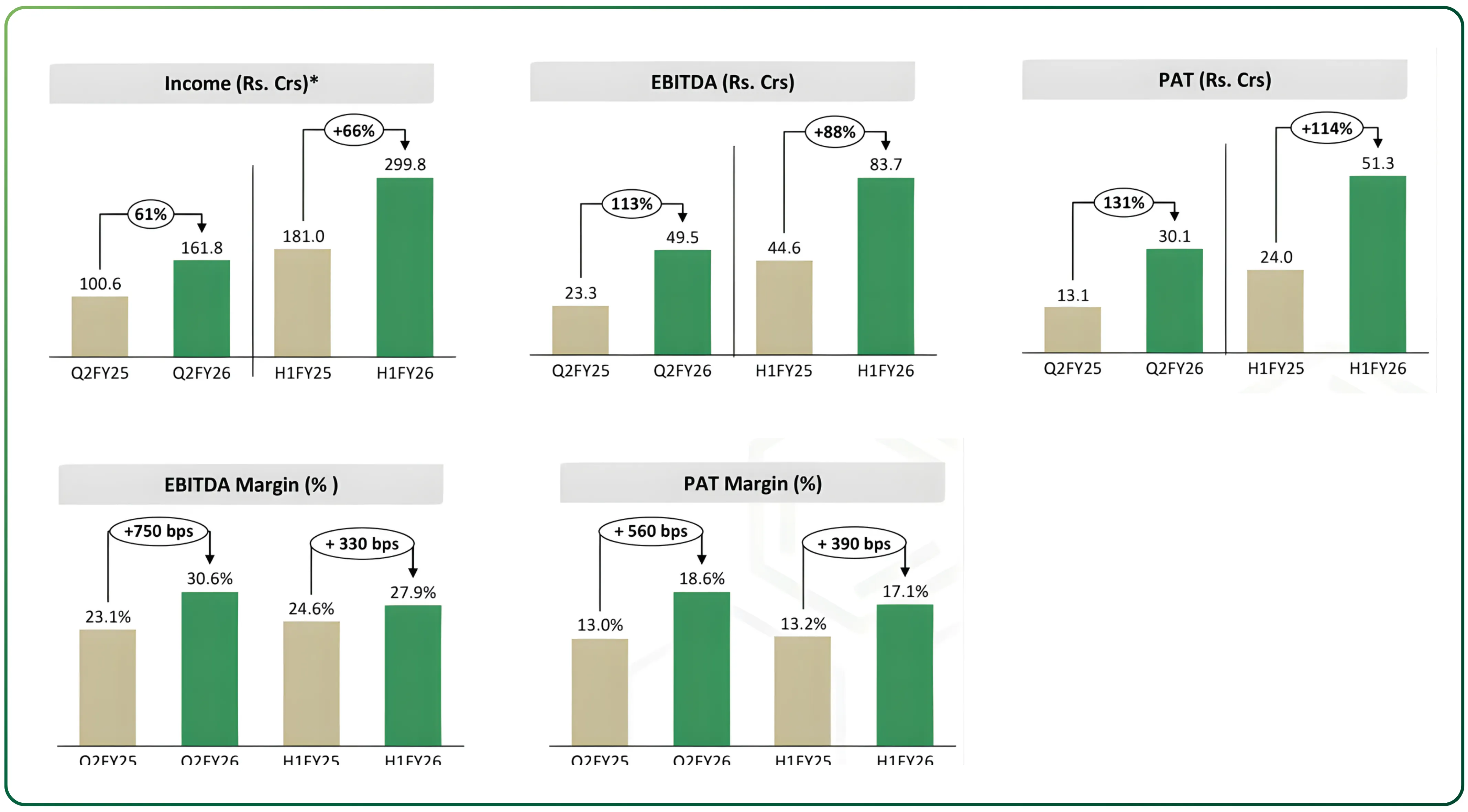

Q2 FY26 performance

- Revenue at ₹162 crore, up 61% YoY. - EBITDA margin at 31%, a steep jump driven by owned products and CDMO.

- PAT is ₹30 crore, with better-than-expected product traction.

- Regulated markets grew 87% YoY, backed by 8 successful product launches.

- Operating cash flow for H1 at ₹31 crore (vs ₹9 crore last year).

- Management reaffirmed their FY26 guidance: ≥50% revenue growth, ≥100% PAT growth.

Are they delivering what they projected? Senores Pharmaceuticals’ Q2 numbers match (and in some parts exceed) what we had expected when we originally analyzed the company. The margin trajectory, the ANDA scale-up, CDMO visibility, and domestic branded generics momentum are all aligned with the thesis.

What to watch in H2:

Pace of ANDA launches (6–8 more expected) Commercialisation from the large Emerging Markets registration base US manufacturing capacity ramp to 2 billion units

3) Acutaas Chemicals

To understand the full thesis behind Acutaas Chemicals, revisit our complete fundamental report here.

Earlier thesis: The story centered on advanced pharma intermediates, a growing CDMO pipeline, and diversification into battery chemicals and semiconductor chemicals. FY26 was expected to be the year of margin recovery and visibility-building, while FY27 would be the first real year of contribution from new verticals.

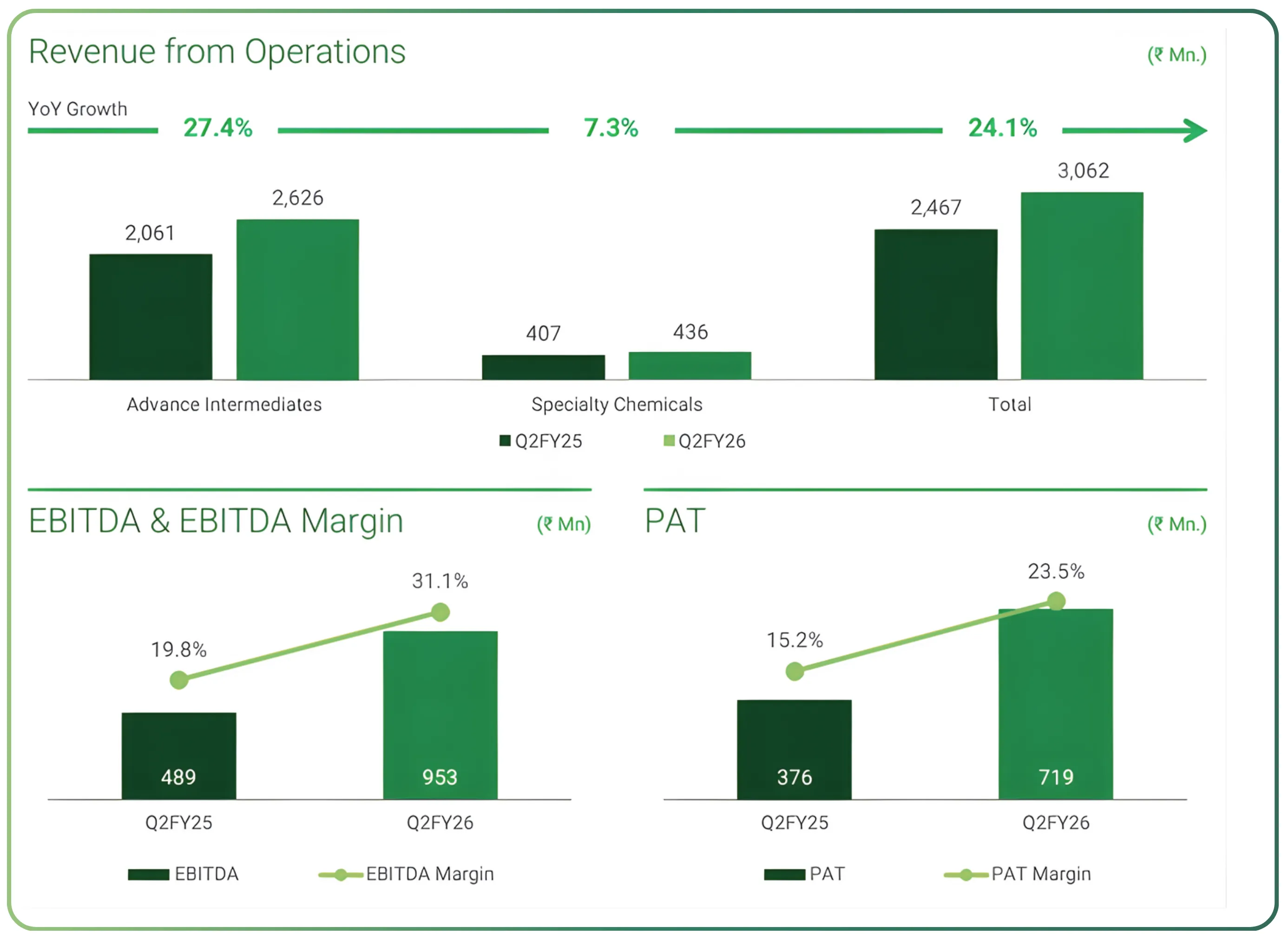

Q2 FY26 performance:

- Revenue at ₹306 crore, up 24.1% YoY.

- EBITDA at ₹95 crore, with a 31.1% margin (vs. 20% last year).

- PAT at ₹71.9 crore, up 91% YoY.

- Gross margin expanded by more than 1,200 bps, driven by better mix and process efficiencies.

- CDMO projects continue to ramp up, with validation batches already dispatched.

- Battery chemical capex is on track for Q4 FY26 commissioning.

- The Korean semiconductor JV is progressing toward H2 FY27 commercialisation.

- H1 operating cash flow is strong at ₹136 crore.

Are they delivering what they projected?

Acutaas Chemicals is tracking its guidance almost point-for-point. The margin rebound, CDMO momentum, and disciplined product-mix realignment have shown up clearly in the numbers. The battery chemical and semiconductor verticals aren’t moving revenue yet, but visibility is growing, and capex is on schedule.

What to watch in H2:

- Electrolyte additive plant commissioning and initial shipments

- CDMO regulatory approvals

- Early signs of semicon commercial traction

- Working-capital discipline (target: 95–105 days)

4) Alkem Laboratories

To understand the full thesis behind Alkem Laboratories, revisit our complete fundamental report here.

Earlier thesis: Alkem was expected to maintain its domestic leadership while benefiting from a strong US portfolio. The thesis leaned on stable India growth, improving international sales, and margin resilience.

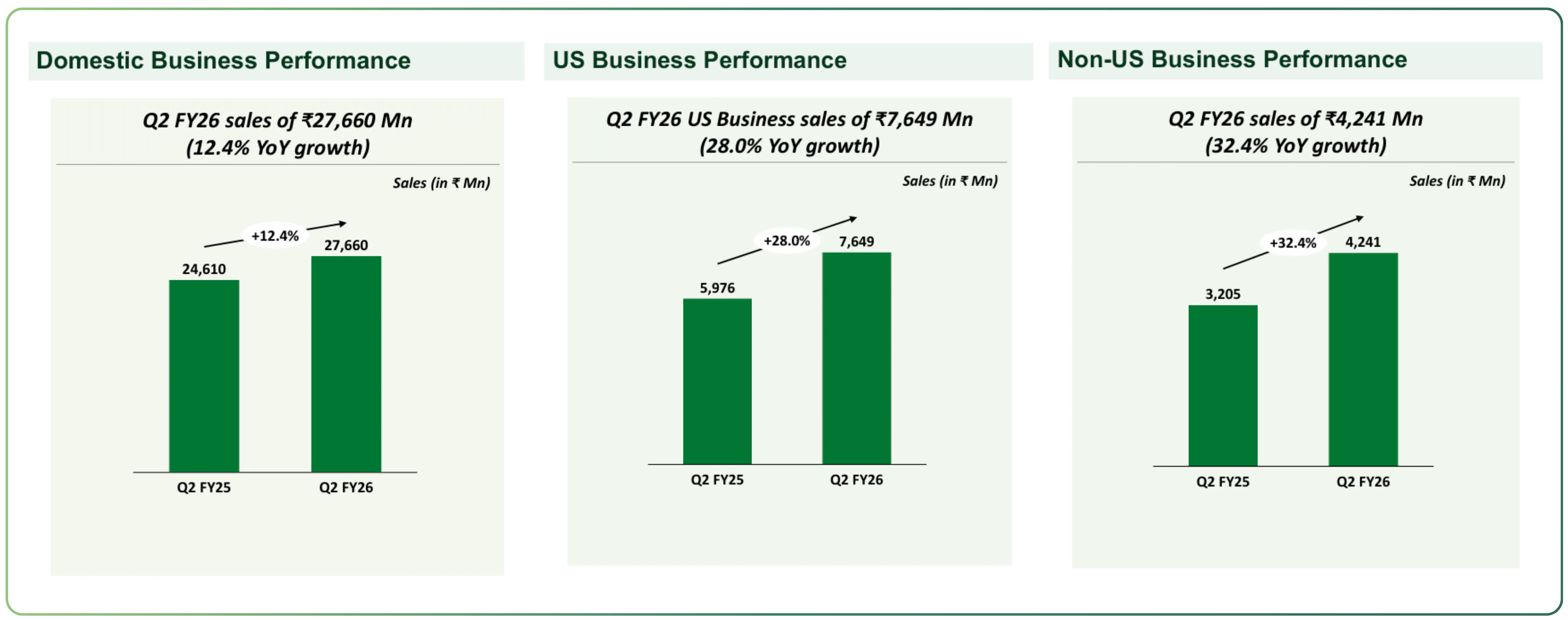

Q2 FY26 performance:

- Revenue grew 17.2% YoY, supported by both India and the US markets.

- India's business grew 12.4%, tracking in line with IPM outperformance.

- US sales grew 28%, driven by key molecules and CDMO traction.

- EBITDA margin remained strong, consistent with management commentary.

- Management reiterated a clear margin and growth outlook for the rest of the year.

Are they delivering what they projected?

Alkem continues to execute the steady, predictable growth pattern we had highlighted earlier. Nothing dramatic, but extremely reliable.

What to watch in H2:

- US market dynamics for key molecules

- India's speciality portfolio expansion

- Margin sustainability above guided levels

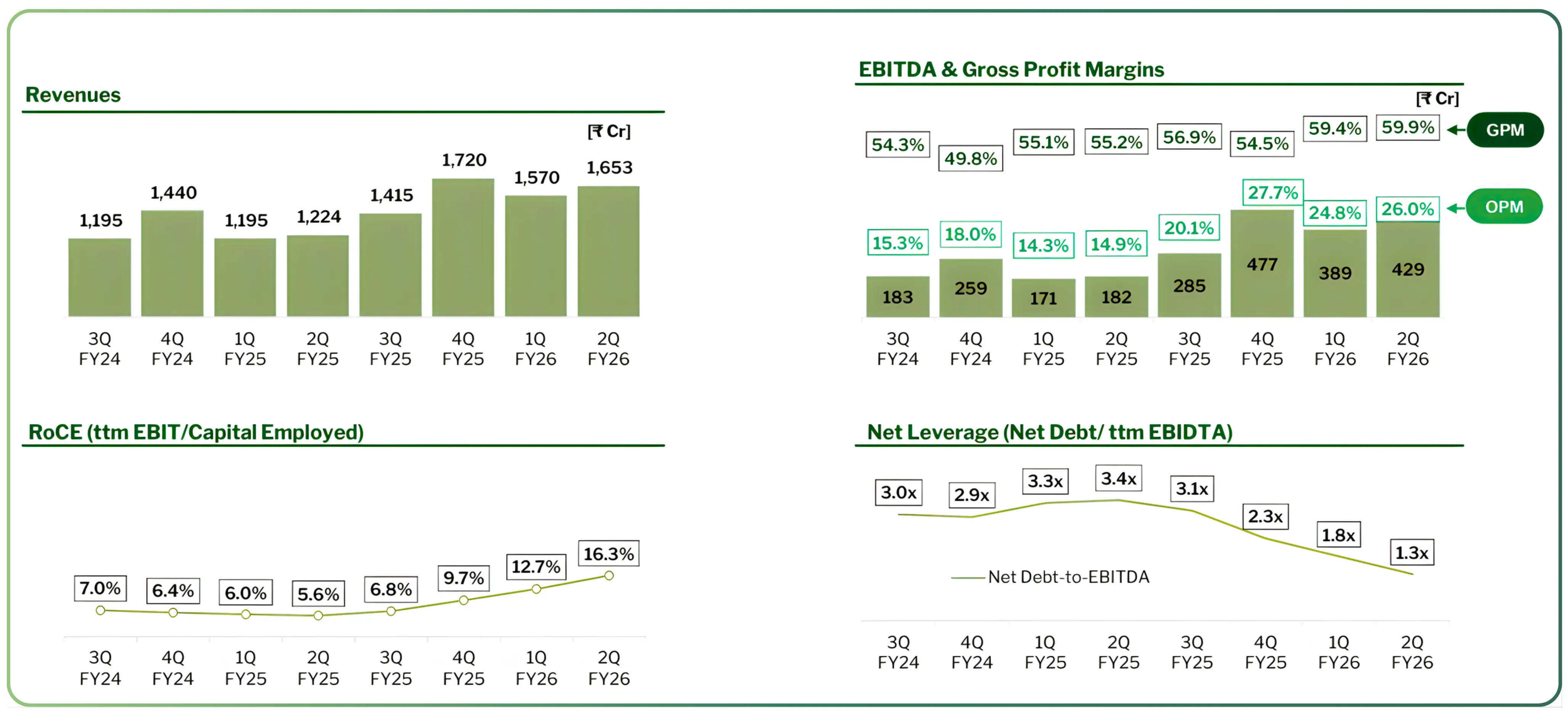

5) Laurus Labs

To understand the full thesis behind Laurus Labs, revisit our complete fundamental report here.

Earlier thesis:

In our original report, we described Laurus Labs as a company in the middle of a strategic transition. It was coming off an ARV down-cycle and entering a capex-heavy rebuilding phase designed to strengthen its position in high-value CDMO, advanced synthesis, biotech, and fermentation. We expected margins to gradually recover as new capacities ramped up, the product mix improved, and CDMO contributions scaled. The long-term upside was tied to the company’s ability to diversify beyond ARVs into complex chemistry and biologics while expanding its global customer base.

Q2 FY26 performance:

- Revenue stood at ₹1,653 crore in Q2, with H1 revenue at ₹3,223 crore, representing 33% YoY growth.

- Gross margin improved to 60%, supported by a richer mix of CDMO and high-value synthesis projects.

- EBITDA margin came in at 26%, reflecting the early impact of operating leverage.

- CDMO contributed 31% of total revenue, with H1 CDMO revenue growing 74% YoY, indicating strong demand from late-stage and commercial programs.

- H1 operating cash flow increased sharply, driven by improved profitability and tighter working-capital discipline.

- Capex remained elevated at ₹489 crore in H1, as Laurus continued expanding capacity in synthesis, fermentation, biologics, and formulations.

- Management announced the allotment of 532 acres in Vizag for a multi-year pharma complex, with a planned investment of around US$600 million covering fermentation, gene/ADC facilities, and backward integration assets.

Reality check:

The Q2 FY26 results show that Laurus Labs is firmly on track with the rebuilding story we had outlined earlier. CDMO growth is accelerating, margins are recovering as the product mix shifts upward, and operating leverage is beginning to show through. The company is also setting up a long runway with large-scale investments in fermentation and biologics. At the same time, the aggressive capex cycle means utilization, cash flows, and asset turns must be watched closely over the next few quarters. Overall, Laurus has reinforced the original thesis: the transition phase is progressing, and the building blocks for the next multi-year growth cycle are falling into place.

Pharma CDMO: Core insights and watchpoints

Margin expansion emerged as the strongest common theme. Acutaas, Senores and Laurus all delivered notable margin improvements, largely driven by a more favourable product mix and clear operating leverage as volumes scaled.

CDMO continues to be the key multiplier across the portfolio. In every company where CDMO projects transitioned into commercial execution, specifically Senores, Laurus and Acutaas, both revenue growth and margin expansion accelerated meaningfully.

Execution risk now sits in different places for different companies. Entero needs successful closure and integration of its M&A pipeline, while Laurus and Acutaas must translate their heavy capex cycles into timely offtake, improving utilization and predictable cash flows. Monitoring these factors over the next two quarters will be essential.

Bottom line

Senores, Acutatas, and Laurus provided solid numeric evidence supporting our initial thesis, reflected in strong growth and better profitability. Alkem continued to behave as expected, reinforcing its position as a dependable compounding story. Entero showed progress, but the full thesis will only come together if it executes its inorganic strategy effectively in the second half of the year.

Turn research into action, and trade smarter on CubePlus

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.