Building on the Dynamics of Gold, we now turn to how gold is actively traded in India, primarily through the Multi Commodity Exchange (MCX). In this part, we explore the structure and features of MCX gold futures and options, how delivery works, and why traders use these contracts for hedging, speculation, or investment. With concepts like margin, volatility, and liquidity at play, understanding the mechanics of gold derivatives is essential for anyone navigating the Indian commodities market.

Gold futures contracts

MCX Gold Futures are standardized contracts traded on the Multi Commodity Exchange (MCX) in India, allowing participants to buy or sell gold at a predetermined price on a future date. These contracts come in various lot sizes, such as 1 kg (Gold Futures) and 100 grams (Gold Mini Futures), making them accessible to both institutional and retail investors. Prices are mainly influenced by a range of factors, including the global gold rate (LBMA), currency fluctuations, and domestic market demand. The volatility of these factors, particularly in times of geopolitical unrest or economic shifts, can create significant price swings, attracting both hedgers and speculators to MCX Gold Futures. MCX Gold Futures serve as a valuable tool for hedging price risk, especially for jewellers, importers, and investors during periods of inflation or economic uncertainty.

(Traders often engage in speculation, using MCX Gold Futures to capitalize on anticipated price movements driven by global economic trends or currency fluctuations.)

Trading is regulated by SEBI and typically involves a margin deposit, ensuring transparency and fair market practices. The high liquidity of MCX Gold Futures, facilitated by active participation from institutional and retail investors, ensures efficient price discovery and ease of entering or exiting positions.

MCX gold delivery process for futures contracts

Delivery process

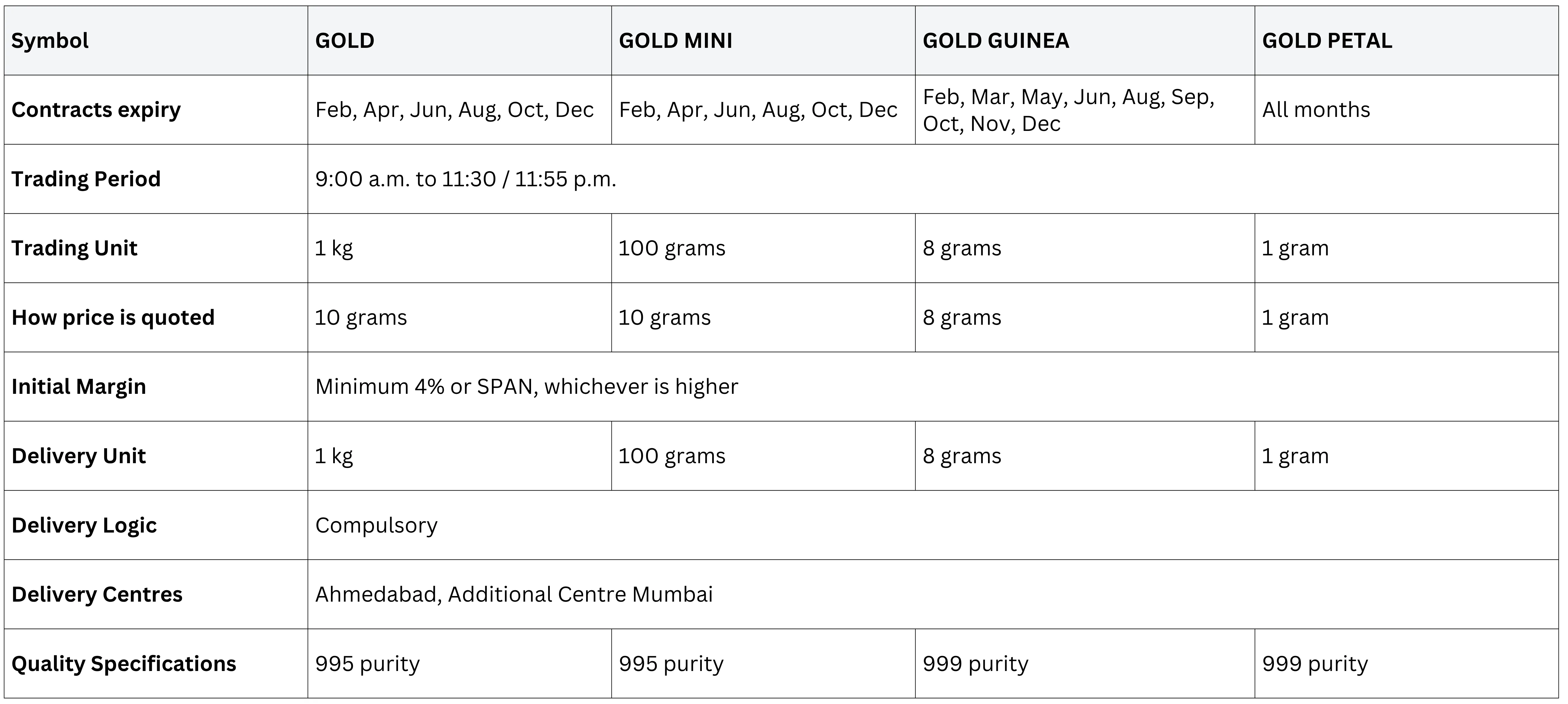

MCX offers several variants of gold futures contracts, including Gold (1 kg), Gold Mini (100 grams), Gold Guinea (8 grams), and Gold Petal (1 gram), all of which are physically settled with a compulsory delivery mechanism during the tender period, typically around 5 days before the contract’s expiry date. The delivery process is as follows:

Intention to deliver: The seller initiates the delivery process by submitting a formal notice of intention to deliver to the clearinghouse during the tender period. This notice specifies the warrant (a legal document of title) for the gold to be delivered, which must meet MCX’s quality standards (minimum fineness of 995 parts per thousand, or 99.5%).

Delivery location: Physical delivery must be taken at MCX-approved warehouses or delivery centers, such as those in Mumbai, New Delhi, or Ahmedabad. The gold must be deposited in these designated depositories by an exchange-approved carrier to maintain the chain of integrity.

Transfer of ownership: Delivery occurs two business days after the seller’s notice of intent, with the transfer of the warrant at the settlement price set by MCX on the notice day. The buyer is obligated to take delivery of the specified quantity of gold (e.g., 1 kg for Gold, 10 grams for Gold Ten, 8 grams for Gold Guinea, or 1 gram for Gold Petal).

Charges and taxes: Buyers must pay additional charges, including:

GST: 3% on the settlement price.

Making charges: ₹200 per 8 grams for Gold Guinea and ₹100 per 1 gram for Gold Petal for converting demat-held contracts into physical gold (e.g., bars or coins).

Warehousing and logistics: ₹35 per day per kg for storage, plus handling and logistics charges that vary by location.

Quality Assurance: The gold delivered must be accompanied by a certificate of assay to confirm its purity and must meet MCX’s specifications for size and brand.

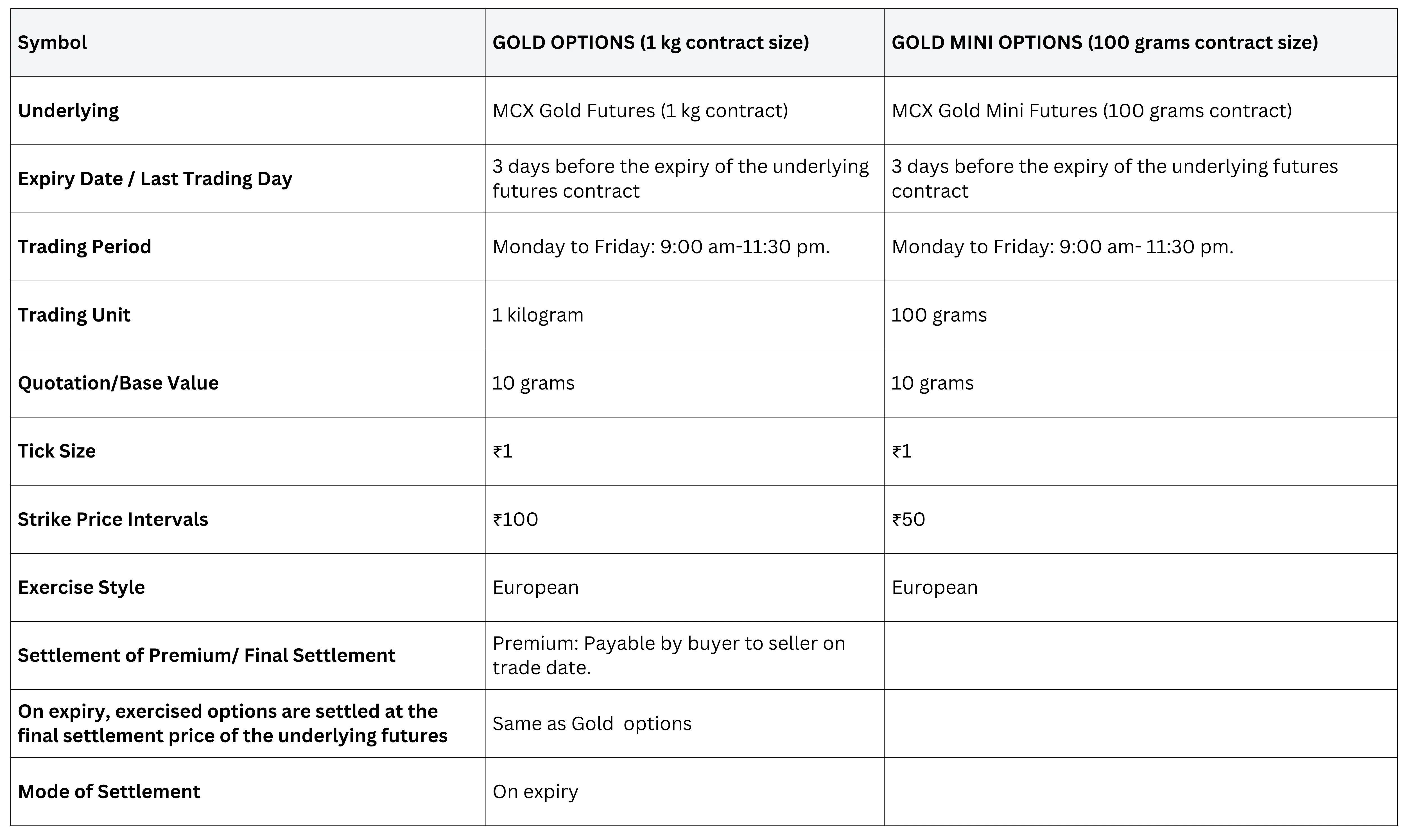

Gold options contracts

Delivery Process

MCX introduced options on gold futures in October 2017, which are settled by devolving into the underlying futures contract if they expire in-the-money (ITM). The delivery process for ITM gold options is as follows:

Devolution into Futures: On the expiry day, ITM options contracts automatically devolve into the corresponding gold futures contract of the current month. For example, if gold is trading at ₹31,500 per 10 grams, a GOLD 19JAN 31000 CE (call option) will devolve into a GOLD 19FEB FUT contract with a buy average of ₹31,000.

Margin Requirements: Upon devolvement, the buyer must maintain margins equivalent to those required for the futures contract on the next trading day. (Leverage in MCX Gold Options allows traders to gain exposure to larger positions with a relatively small premium, amplifying potential returns while increasing risk).

*Failure to maintain sufficient margins may lead to the broker squaring off the position.

Physical Delivery: Since the devolved futures contract is subject to MCX’s physical delivery rules, the buyer must follow the same delivery process as described for futures contracts (i.e., taking delivery at an MCX-approved warehouse, paying GST, making charges, and logistics costs). The delivery occurs during the tender period of the futures contract, as outlined above.

Charges and Taxes: Similar to futures, buyers of ITM options that devolve into futures must pay 3% GST, making charges (e.g., ₹100 for 1 gram of Gold Petal), and warehousing/logistics fees if physical delivery is taken.

Also Read: Discover Smarter Investing Through Exchange Traded Funds (ETF)

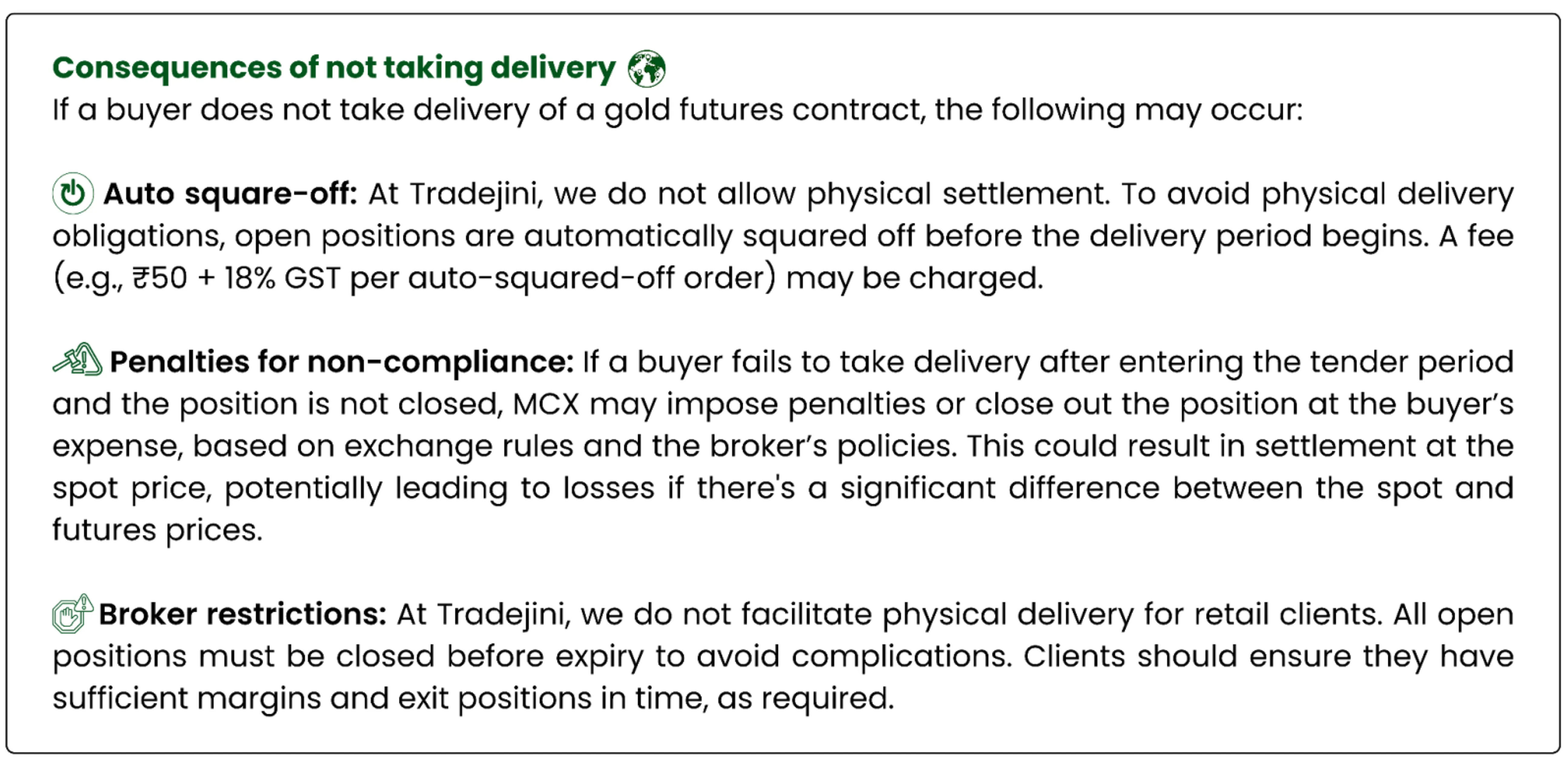

Consequences of Not Taking Delivery

If a buyer does not take delivery of an ITM options contract that has devolved into a futures contract:

Cash Settlement (if no counterparty): If MCX cannot match the ITM options contract with a counterparty, the contract is cash-settled instead of devolving into a futures contract. The settlement is based on the difference between the strike price and the spot price at expiry, credited or debited to the buyer’s account.

Broker Auto Square-Off: Similar to futures, Tradejini square offs devolved futures positions before the tender period to avoid physical delivery, incurring a fee (e.g., ₹50 + 18% GST per order). This ensures retail investors avoid unintended physical delivery obligations.

Margin Shortfall: If the buyer lacks sufficient margins to support the devolved futures contract, the broker may close the position, potentially at a loss, depending on market conditions.

Penalties: If the buyer enters the tender period for the devolved futures contract and fails to take delivery, MCX or the broker may impose penalties or close the position at the buyer’s expense, similar to futures contracts.

Why does gold still matter?

Gold remains a unique asset with enduring relevance across time. From its cosmic formation to its diverse roles in finance, technology, and culture, gold continues to attract attention from investors, governments, and industries alike. As global dynamics evolve, gold’s significance may shift, but its role as a symbol of value, stability, and utility is likely to persist.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.

%252FAnalysis%2520of%2520FII%2520Positioning%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D1405f6f4-6738-4f13-99c7-288e6fede0b6&w=3840&q=75)

%2520Every%2520Trader%2520Should%2520Know%252FCAS%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D397e2566-b93f-4420-b41d-378b1483f837&w=3840&q=75)