For an updated look at FY26 performance trends, read our latest analysis – A Performance Review of Gravita India, VA Tech Wabag, and Deep Industries. It revisits these companies’ financials, margins, and strategic progress since our previous analyses.

Gravita India Ltd. is one of India’s leading recycling companies, operating across lead, aluminium, plastic, and turnkey solutions. With integrated operations and a growing global presence, the company has built a resilient and scalable business model. Its mission to lead India’s recycling sector aligns with global sustainability goals by converting over 250,000 MT of scrap annually into valuable raw materials.

Business Structure and Strategy

Gravita operates across four verticals: lead (its core business), aluminium, plastic, and turnkey recycling projects. It recycles used batteries, aluminium and plastic scrap, and is expanding into rubber and tyre recycling. The product portfolio includes value-added offerings like lead alloys, red lead, aluminium alloys, PET flakes, and tyre oil. The company’s operations support the circular economy by maximizing resource recovery through innovative recycling technologies.

| Segment | Revenue Contribution |

|---|---|

| Lead | 88% |

| Aluminium | 8% |

| Plastics | 3% |

| Turnkey Projects | 1% |

| Value-Added Products | 45% of Total Revenue |

The company aims to increase the contribution of value-added products to over 50% by FY27, reflecting a strategic shift toward higher-margin offerings through its integrated recycling processes.

Financial performance and operational metrics

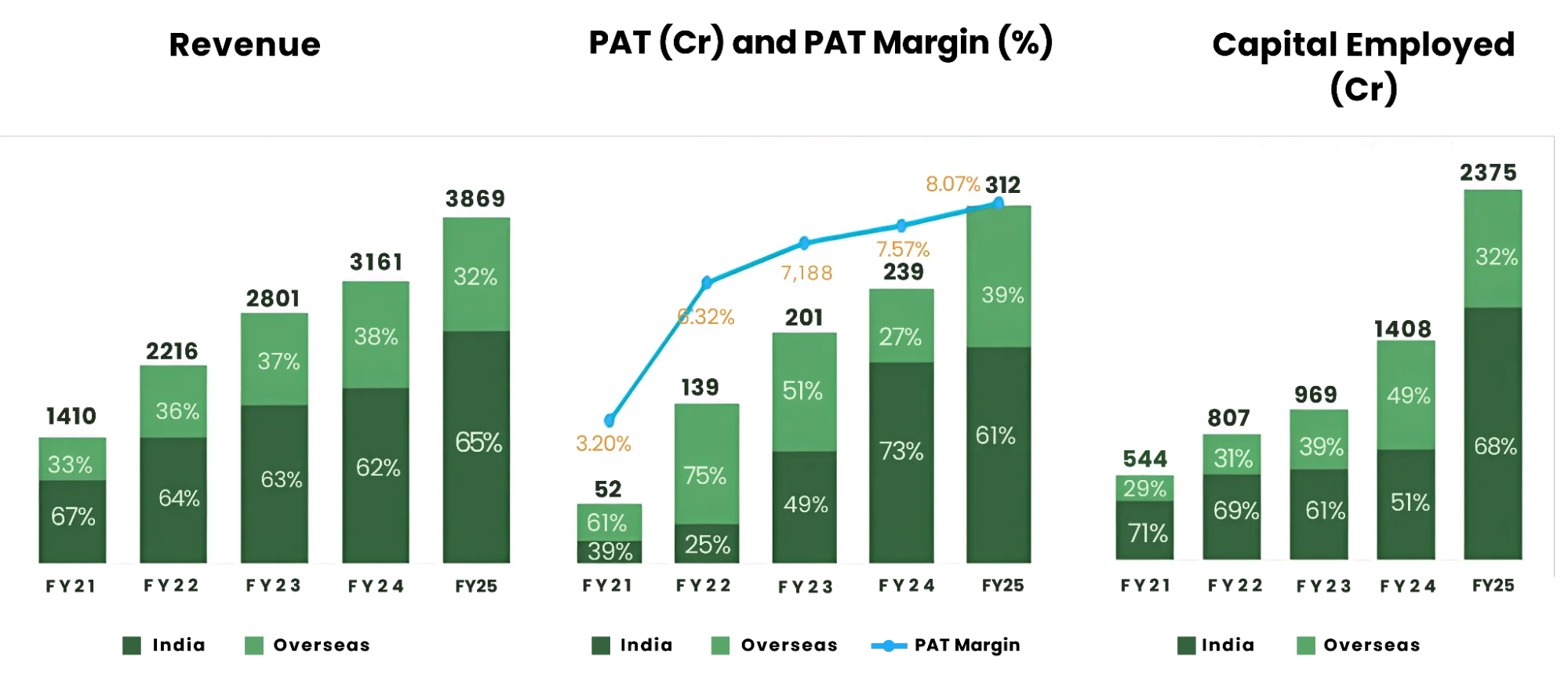

FY25 marked a milestone year for Gravita, with record highs in revenue, EBITDA, and PAT. Revenue grew by 22% to ₹3,869 crore, while adjusted EBITDA rose 22% to ₹404 crore, maintaining a strong margin of 10.43%. PAT increased by 31% to ₹312 crore, with a PAT margin of 8%. The company’s 5-year CAGR stands at 23% for revenue and an impressive 57% for PAT, underscoring strong operating leverage and margin expansion.

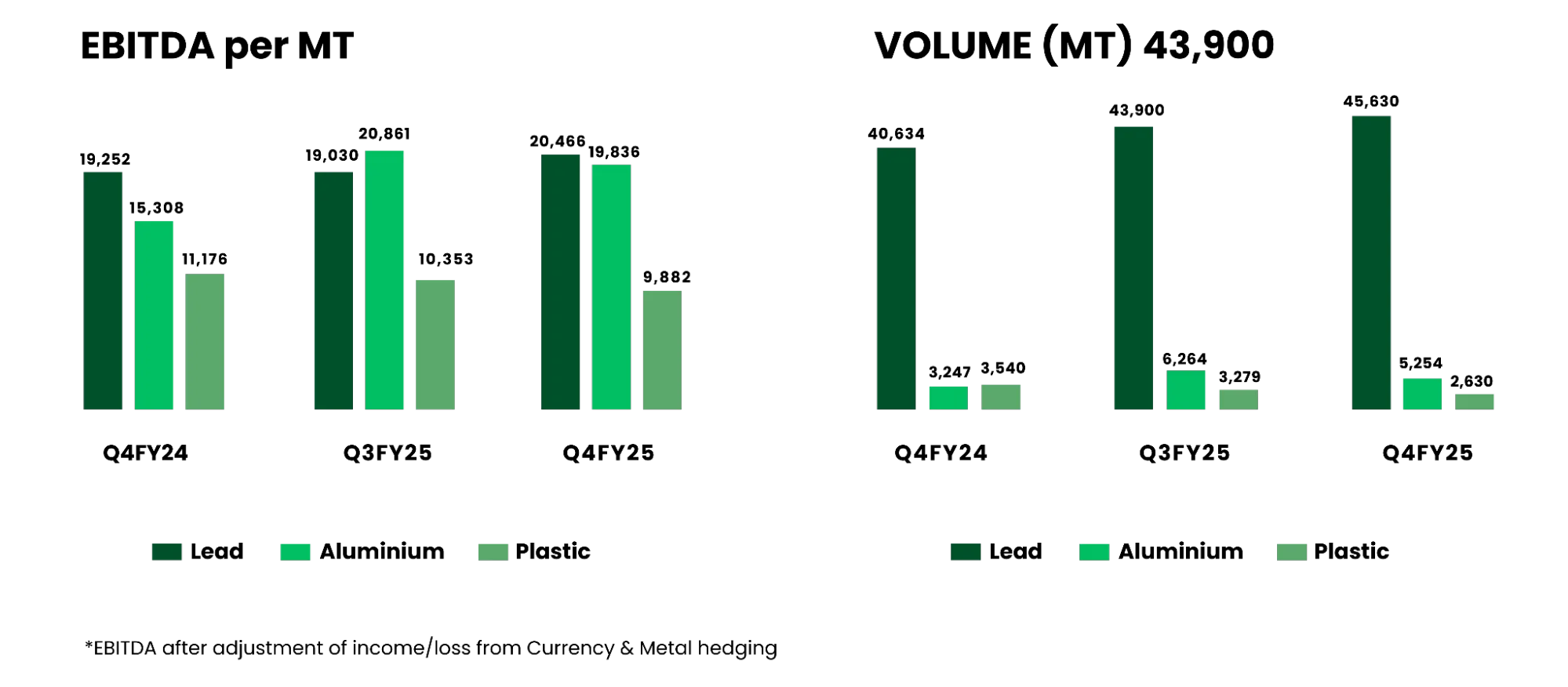

EBITDA per ton in Q3 FY25 was ₹19,030 for lead, ₹10,353 for aluminium, and ₹20,861 for plastics. The strong margins in the aluminium and plastic verticals demonstrate the scalability and profit potential of Gravita’s diversified operations.. The company’s ROIC pre-tax for FY25 was 27%, in line with its long-term benchmark of maintaining ROIC above 25%.

Gravita’s balance sheet is notably strong, with the company achieving net debt-free status and generating operating cash flows of ₹282 crore in FY25, up sharply from ₹42 crore the prior year. The company also raised ₹1,000 crore through a QIP in H1 FY25, allocating ₹245 crore for debt repayment and working capital, The ₹1,000 crore equity investment supports Gravita’s aggressive capex plans while reinforcing its path to sustained profit generation. The focus on value-added products and expansion into new materials supports Gravita’s long-term profitability and sustainability

Growth initiatives

The company has embarked on an aggressive capacity expansion plan, targeting over 500,000 MTPA by FY27 and 700,000+ MTPA by FY28, supported by a planned capex of ₹1,500 crore over the next three years. Of this, ₹1,000 crore is allocated for existing verticals, with the remainder allocated to new ventures into lithium-ion battery and tyre recycling to support India’s transition to electric vehicles and a sustainable future.

Recent acquisitions, such as the waste tyre recycling plant in Romania (18,000 MTPA capacity), and the development of a lithium-ion battery recycling project and a rubber recycling facility in Mundra underscore Gravita’s strategy to diversify its product mix and expand its global footprint. The company’s upcoming recycling facilities in India and abroad enhance its ability to meet global waste management needs.

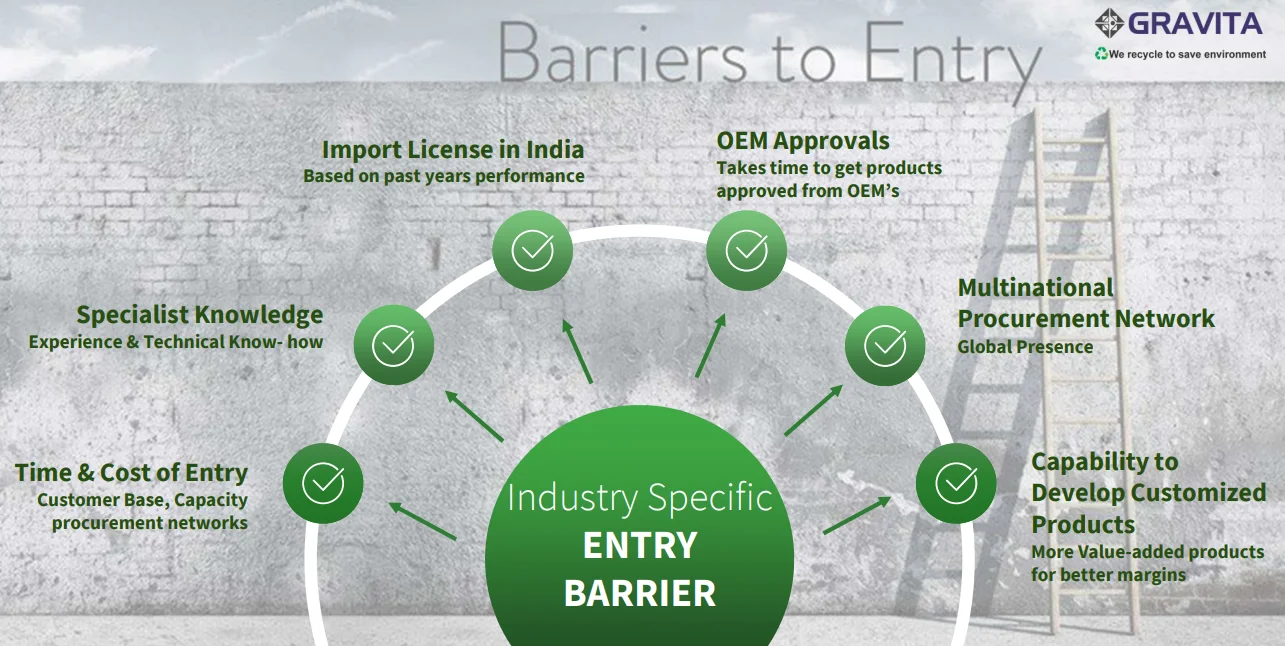

Market position, client base, and distribution

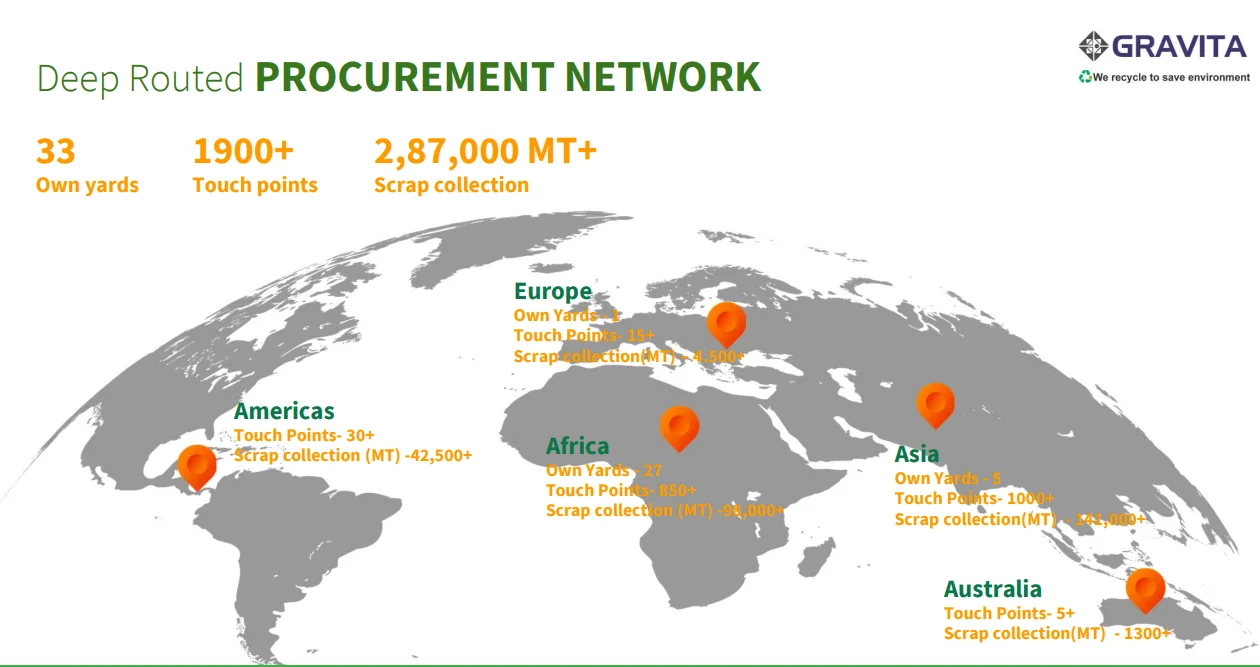

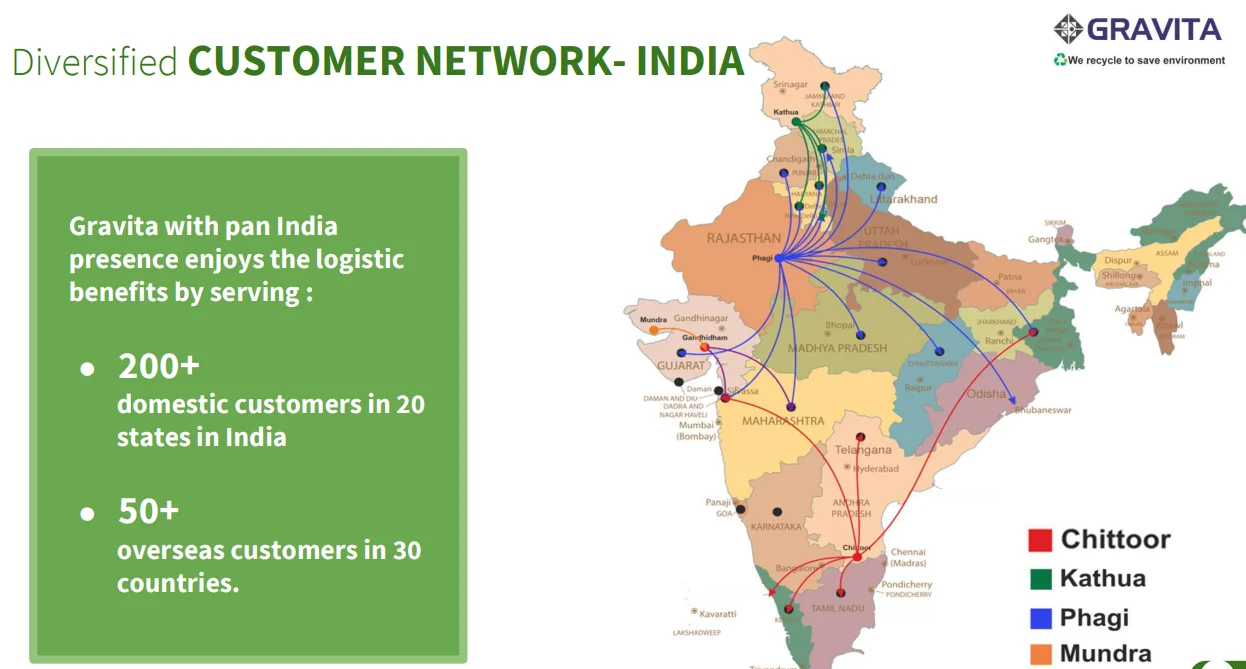

Gravita serves a diversified client base of over 325 global customers in 32+ countries and 200+ domestic clients across 20 Indian states. Its distribution network includes 31 owned yards and 1,700+ touchpoints. Its vast sourcing network processes over 250,000 MT of scrap annually, fueling its integrated recycling operations across continents. The company’s manufacturing presence spans India and international locations, including Ghana, Senegal, Mozambique, Tanzania, Togo, Sri Lanka, Oman, the Dominican Republic, and Romania.

The geographical revenue split for FY24 was 68% India and 32% overseas, with international operations contributing 53% to overall profits, reflecting higher margins in certain overseas markets. Its strong presence in international markets is driven by high recycling rates and robust demand for post-consumer scrap solutions.

Regulatory and sustainability drivers

With a strong emphasis on sustainability and adherence to ESG frameworks, Gravita is well-positioned to thrive under India's evolving regulatory ecosystem.

1. BWMR (Battery Waste Management Rules)

These are rules set by the Indian government to ensure that companies properly collect, recycle, or dispose of used batteries, which can be harmful to the environment if thrown away carelessly. For recycling companies like Gravita, this means more responsibility but also more opportunities to collect and recycle battery waste locally, boosting business and reducing dependency on imported scrap. By increasing local sourcing and using renewable energy, Gravita strengthens its mission to protect the environment.

2.EPR (Extended Producer Responsibility)

This rule says that companies that make or sell products (like batteries, electronics, or packaging) must also take responsibility for what happens to those products after use. So, they must collect and recycle a certain amount of their waste. This creates steady demand for recycling services, helping companies like Gravita grow sustainably. Under Extended Producer Responsibility (EPR), Gravita partners with companies to recycle end-of-life products in a closed-loop system.

Stringent government regulations, such as BWMR and EPR, have driven a shift towards domestically sourced scrap (43% in FY25, up from 30% the previous year), improving supply chain security and supporting margin resilience. Gravita is also advancing its ESG agenda, aiming to source over 30% of its energy from renewables and reduce energy consumption by over 10%. India’s regulations around battery and plastic production ensure a steady supply of recyclable material, supporting long-term business stability.

Future outlook

Management has articulated a clear growth roadmap, targeting a volume CAGR of over 25%, profitability growth exceeding 35%, and maintaining ROIC above 25%. The company is committed to increasing the contribution of non-lead businesses to over 30% and value-added products to over 50% by FY28. New verticals such as lithium and rubber recycling, backed by ₹1,500 crore in investment and capex, are expected to accelerate profit growth and support Gravita’s sustainability agenda.

The company’s strong order book (60,000+ MT as of April 2024), ambitious capex pipeline, and proven execution capability position it well for sustained growth. Management guidance indicates a 25–30% annual capacity and revenue growth for the next three years, with the pace of growth contingent on timely capex execution and regulatory approvals.

Valuation perspective

Driven by high profit margins, strong investment returns, and a forward-looking ESG strategy, Gravita presents a compelling long-term opportunity. With a 5-year PAT CAGR of 57%, ROIC consistently above 25%, and a net debt-free balance sheet, the company is well-placed to command a premium valuation relative to peers in the recycling and speciality materials sector.

The company’s forward strategy-pivoting towards higher-margin value-added products, expanding into new recycling verticals, and leveraging global scale-should support further re-rating. Assuming management delivers on its guidance of 25–30% annual growth and maintains its margin profile, Gravita’s earnings trajectory is likely to remain strong.

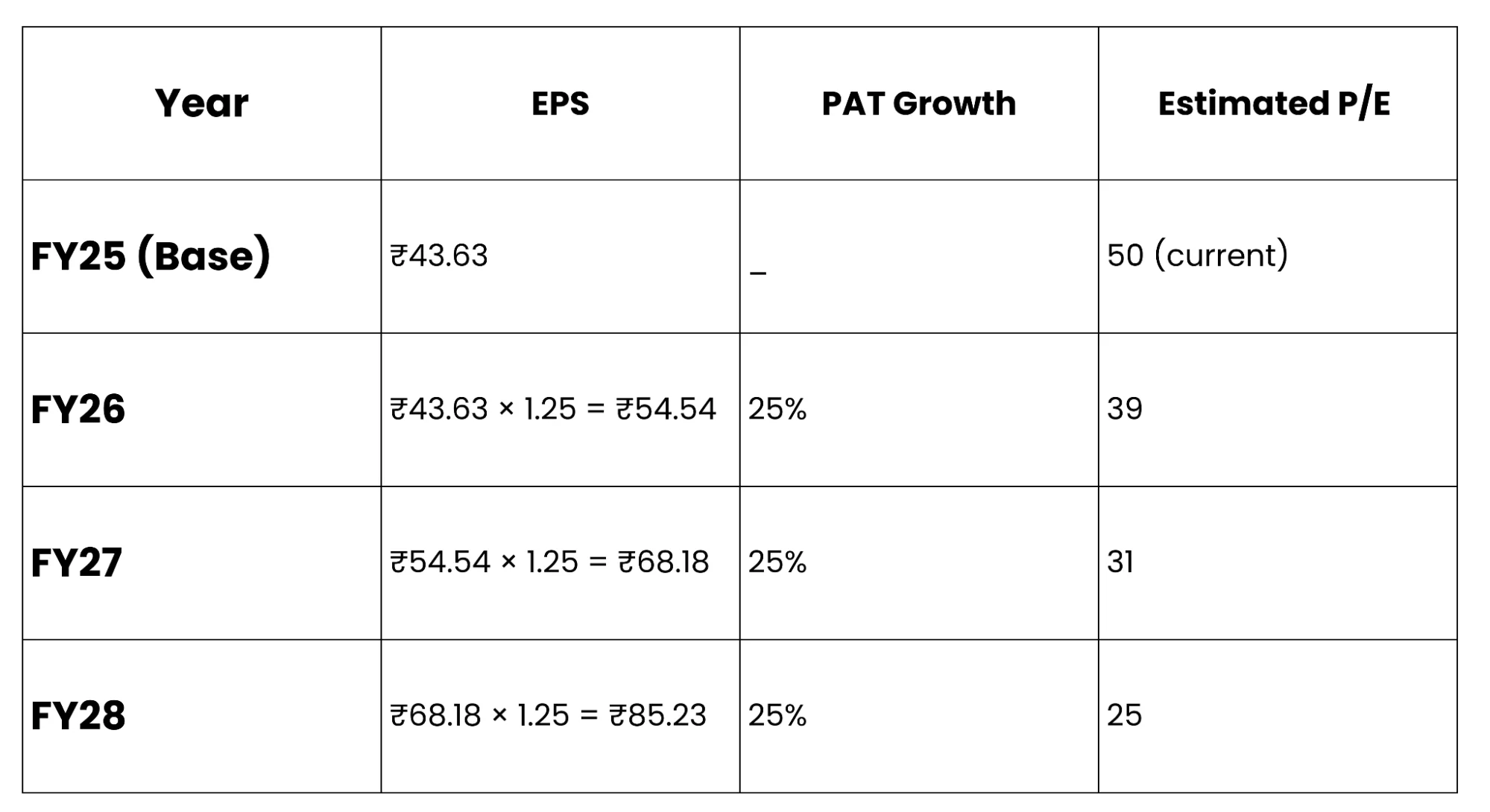

Valuation based on P/E

Assuming Gravita maintains a 25–30% annual PAT growth rate and trades at its current P/E:

Projected EPS (Next 3 Years):

If Gravita continues to deliver ₹100 crore+ in annual profit and maintains its high-return investment profile, the stock could command premium valuations

Valuation View

Gravita offers a mix of strong growth, high margins, and capital efficiency. Its consistent ROIC above 25%, net debt-free status, and focus on value-added products support the potential for further valuation upside.

If the company executes as guided, achieving 25–30% annual growth and maintaining margins, its earnings trajectory appears robust. Gravita is emerging as a leading player in India’s circular economy and sustainable materials space.