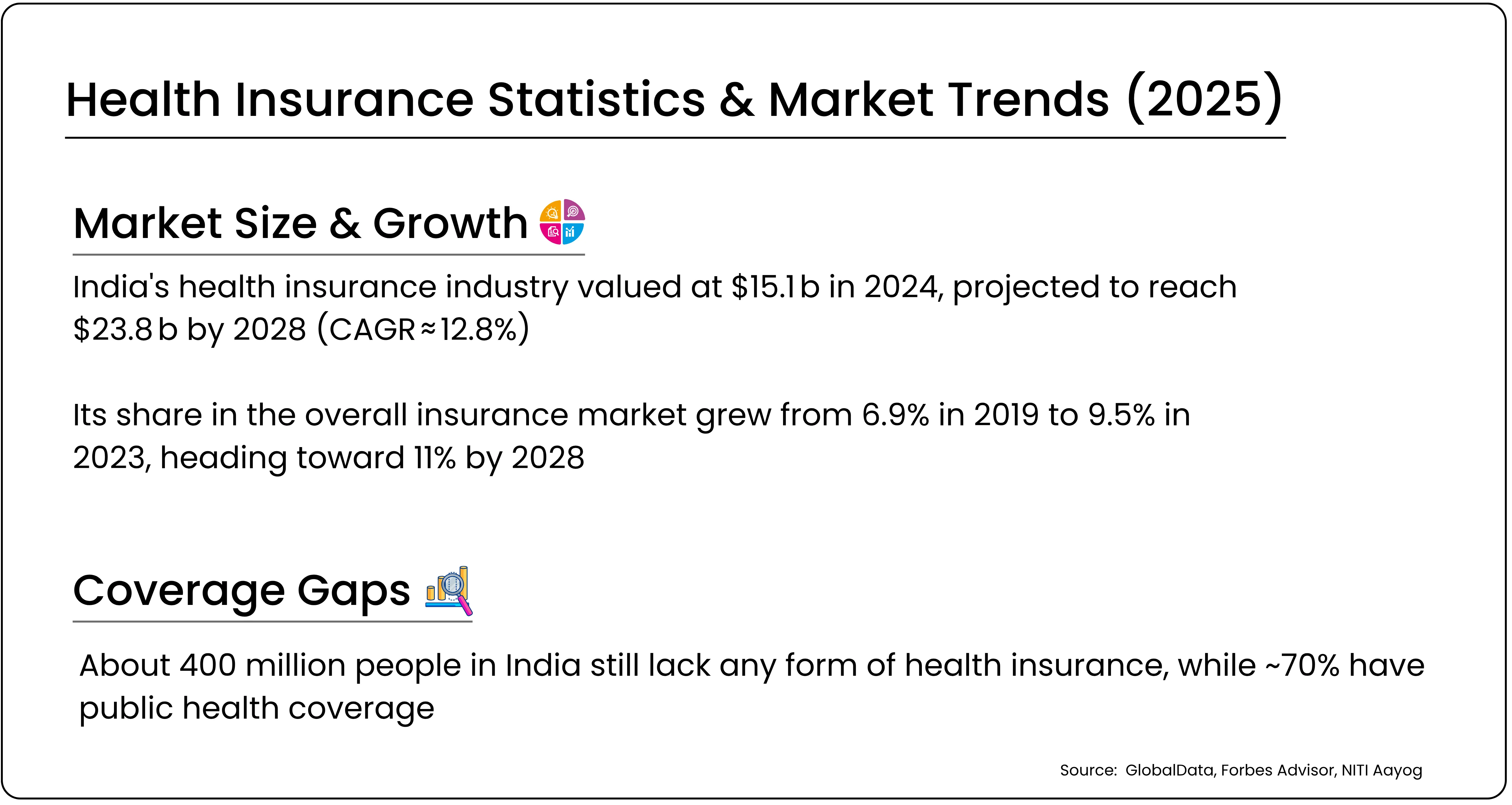

When we discuss financial planning, our minds typically jump to investments, taxes, loans, or retirement. But there’s one crucial area that still doesn’t get the attention it deserves, such as health risk planning, particularly for life-threatening illnesses like cancer.

Cancer care insurance might not be the first product you think of when building your financial portfolio, but given today’s rising cancer cases and treatment costs, it absolutely should be.

The harsh reality

Let’s start with a hard truth. According to data from the Indian Council of Medical Research (ICMR), one in nine Indians is at risk of developing cancer in their lifetime. Add to that the rising cost of treatment, ranging anywhere between ₹5 lakh to ₹50 lakh depending on the stage and type, and it quickly becomes clear why cancer care insurance is no longer optional.

Relying solely on standard health insurance can lead to underinsurance, leaving you vulnerable to significant out-of-pocket expenses.

While traditional health insurance does cover critical illnesses to an extent, the extent is often limited. There are caps, co-pay clauses, and sub-limits that can erode your savings. A dedicated cancer insurance policy, on the other hand, is tailor-made to provide financial relief through every phase, from diagnosis to treatment and recovery.

At Tradejini, we often talk about managing market risks. But managing life risks is just as important. If an unexpected illness like cancer strikes, your investments and trading capital could be forced into liquidation. Cancer insurance helps ensure that it doesn't happen.

How cancer insurance works

Unlike standard health plans that may reimburse you after submitting bills, most cancer-specific policies offer lump sum payouts on diagnosis. This means you get immediate access to a large sum of money, which can be used flexibly, whether it’s for hospitalization, chemotherapy, radiation, alternative treatments, wellness programs, or even income replacement during recovery.

Here's a simplified example of how it plays out:

| Scenario | Without Cancer Insurance | With Cancer Insurance |

|---|---|---|

| Diagnosis of Stage II Breast Cancer | ₹12–₹15 lakh out-of-pocket expenses |

₹15 lakh lump sum payout from the insurer |

| Loss of Income during 6-month recovery |

The entire burden is on savings or family |

Covered through income benefit |

| Post-hospital care and second opinions |

Often excluded or limited |

Covered under most cancer-specific plans |

What’s even more encouraging is that many cancer policies cover all stages of cancer, early, major, and advanced. Some even waive future premiums if you're diagnosed early.

Is your health insurance enough?

One common misconception is that a regular health policy will suffice in case of cancer. While they do cover hospitalization and some treatment costs, the reality is that cancer care often involves a long recovery window, multiple types of therapy, and ongoing expenses beyond hospital bills.

Standard policies may have sub-limits on room rent, chemotherapy sessions, or radiation sessions. Some don’t cover second opinions, which are crucial in a complex disease like cancer. And if the insured sum is already consumed for other illnesses in the family (in the case of a floater plan), there might be little left for cancer treatment.

This is where a cancer insurance policy steps in. It doesn’t replace your existing plan; it complements it with specific inclusions like coverage for second opinions, advanced therapies, and long-term care not typically covered by standard health policies. Think of it as a financial firewall exclusively for one of the costliest medical emergencies you could face.

How premium varies between men and women in 2025

When it comes to health insurance and, more specifically, cancer insurance, gender does play a subtle yet important role in how premiums are priced. In 2025, insurers continue to follow a risk-based pricing model known as gender rating, where male and female applicants may be charged differently based on health patterns, lifestyle habits, and medical history.

For women, premiums may be slightly higher during their reproductive years, typically late 20s to late 30s, especially if they opt for maternity coverage or have a family history of illnesses like breast or cervical cancer. Medical expenses associated with pregnancy, childbirth, and postnatal care increase claims, prompting insurers to factor in higher risks. Women also tend to make more frequent doctor visits for preventive screenings and gynaecological consultations, which is reflected in their claim patterns.

On the other hand, men are more likely to face increased premiums as they age, particularly after 50. This is due to a higher incidence of lifestyle diseases such as heart disease, diabetes, and hypertension. According to surveys, smoking and alcohol consumption remain significantly higher among Indian men, factors that sharply increase the likelihood of future claims. Additionally, shorter life expectancy and higher accident risk among men also impact their pricing.

Simply put, while younger women may pay more during their childbearing years, men often face higher premiums in their later decades due to elevated long-term health risks. As insurers refine their data models in 2025, the premium gap continues to reflect these evolving gender-based risk profiles.

Also Read: How Women Are Taking Charge of Financial Futures

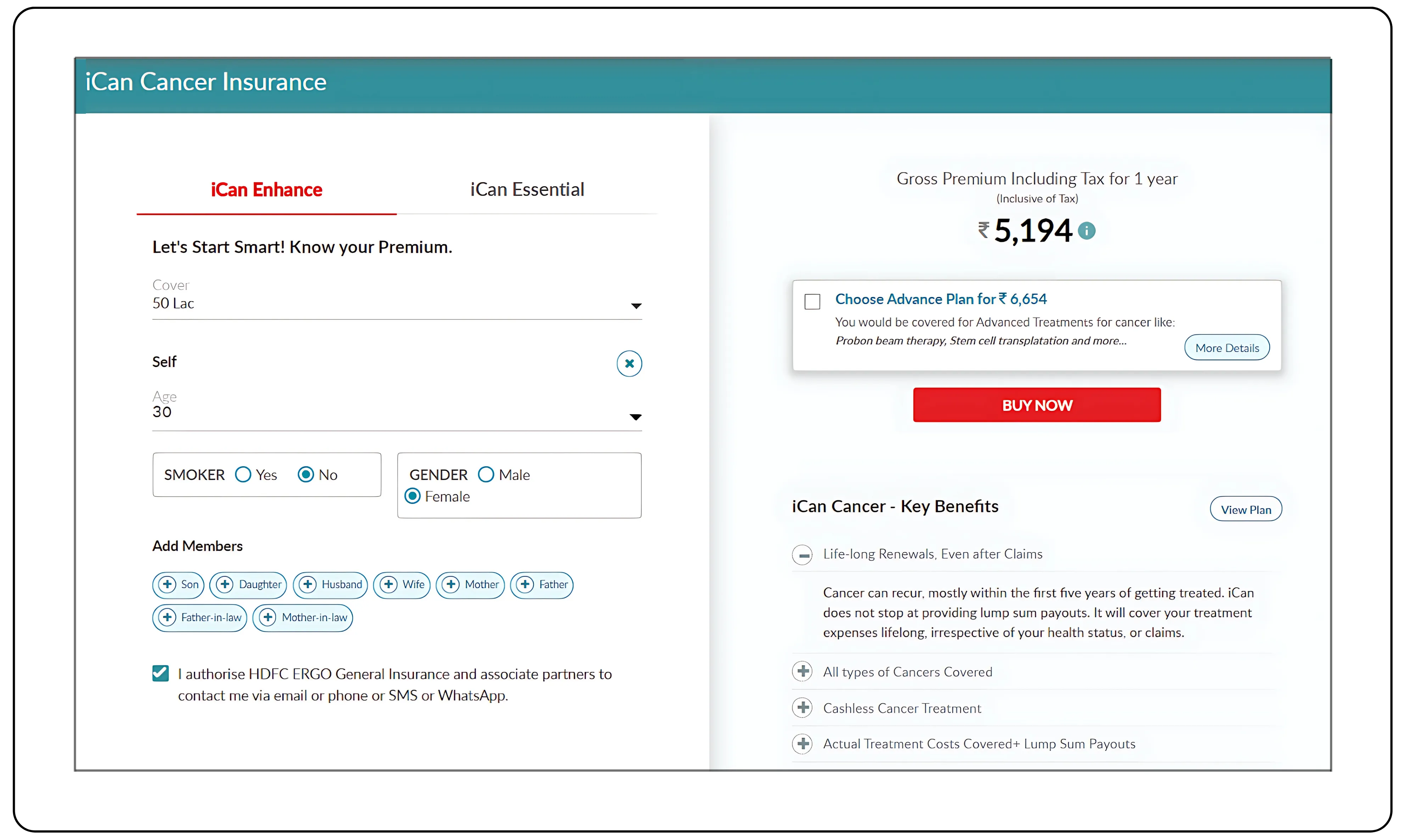

Choosing the right cancer insurance plan

Cancer insurance is not a one-size-fits-all product. Depending on your age, lifestyle, family history, and income level, the right plan could vary. A good rule of thumb is to select a sum insured that’s 1.25x the average treatment cost in your city. This not only covers current costs but also helps you stay ahead of medical inflation.

Here’s a glance at a few plans currently available:

| Plan Name | Entry Age | Sum Insured | Waiting Period | Highlight |

|---|---|---|---|---|

| Aditya Birla Cancer Secure |

18–65 yrs | ₹5L–₹1Cr | 90–180 days | Covers all cancer stages |

| Niva Bupa CritiCare |

18–65 yrs | ₹3L–₹3Cr | 90 days | Covers 19 critical illnesses |

| Tata AIG Criti-Medicare |

91 days–65 yrs | ₹5L–₹2Cr | 90 days | Includes pre-cancerous lesions |

| Care Cancer Mediclaim |

5–50 yrs | ₹10L–₹2Cr | 90 days | Covers chemo and radiotherapy |

Don’t forget to compare waiting periods, co-payment clauses, and exclusions like pre-existing conditions or claims within the first 90 days. These can affect your payout eligibility.

More than just money

Let’s face it, fighting cancer isn’t just a medical battle. It’s emotionally and financially draining. Having a cancer care insurance plan doesn’t just pay for treatment, it buys peace of mind.

It assures you that you won’t need to dip into your child’s education fund or sell your long-term investments. It allows you or your family to focus on recovery, not repayments.