India's startup ecosystem has come a long way. From Bengaluru's crowded co-working spaces to Mumbai's investor boardrooms, the term ‘VC funding’ has become part of everyday conversation. We hear about startups raising Series A or Series B rounds, valuations touching hundreds of crores, and founders ringing the bell at IPOs. But there is a question that rarely gets answered simply: how does a Venture Capital firm actually make money?

The vibrant startup ecosystem India boasts is now recognized on a global scale.

This post breaks it down… no jargon, no fluff.

But first, if you want to understand the basics of venture capital firms and venture capital explained india

Catch up with our article on Venture Capital in India to see how VC funds operate in the Indian market.

The growth of venture capital in India has transformed the domestic business environment.

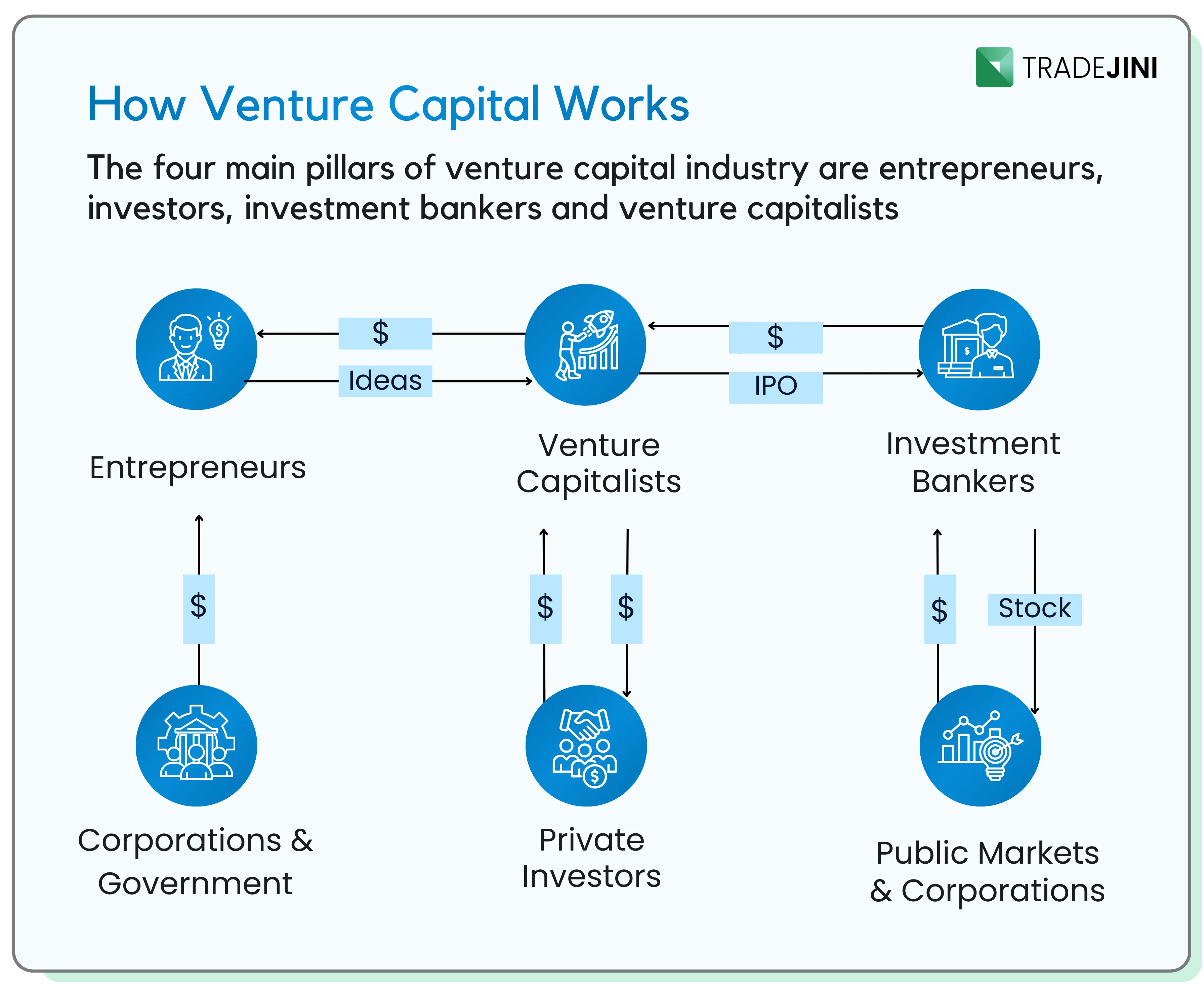

A venture capital (VC) firm is a professional money manager that raises capital from investors, called Limited Partners (LPs), and invests it in early- or growth-stage startups in exchange for equity.

The role of limited partners in venture capital relies on is providing the underlying capital for the ecosystem.

In India, LPs are usually institutions such as pension funds, family offices, high-net-worth individuals, and government-backed funds like SIDBI’s Fund of Funds, along with global investors.

The firm is run by General Partners (GPs), who manage the fund and make investment decisions. Simply put, a VC firm raises money from LPs, invests it in startups, and aims to generate strong returns.

The expertise of general partners of venture capital funds dictates the success of the investments.

Founders must learn exactly how VC firms work behind the scenes.

Management Fees and Carried Interest

A VC firm has two core ways it earns money. Understanding these two mechanisms explains almost everything about how the industry operates.

1. Management Fees

Every year, the VC firm charges its LPs a management fee typically 2% of the total fund size annually.

Let's put this in an Indian context. Suppose a fund raises ₹400 crore. At a 2% annual management fee, the firm earns about ₹8 crore per year to cover salaries, office expenses, travel, due diligence costs, and other operational expenses. This fee is paid regardless of whether any startup succeeds or fails.

Management fees are not the jackpot. They are operational income enough to run the firm professionally, but not the reason GPs get into the business.

The typical fee is charged over the investment period (usually the first 5 years of a 10-year fund), and may taper down in the later years.

2. Carried Interest (‘Carry’)

This is where the real wealth is created and where incentives align between the VC and the startup ecosystem.

Carried interest is the VC firm's share of the profits generated from successful investments. The standard is 20% of the profits though top-tier funds sometimes negotiate higher.

Here is how it works in practice:

Suppose a fund raises ₹500 crore from LPs. Over its lifetime, the fund's investments generate ₹2,000 crore in returns. The profit is ₹1,500 crore.

Of that ₹1,500 crore profit:

- 80% goes to LPs that's ₹1,200 crore

- 20% (the carry) goes to the VC firm's GPs that's ₹300 crore

That ₹300 crore is split among the GP partners and this is why joining a successful VC firm as a partner can be extraordinarily lucrative.

The Hurdle Rate

Most funds have a hurdle rate (also called a preferred return) typically around 8% per annum. This means the VC firm only begins earning carry after the LPs have already received an 8% annual return on their capital.

This structure protects LPs. The GPs are motivated to generate returns above and beyond the baseline only then does their own wealth-building begin.

In India, as the market matures, LP sophistication has grown. Many institutional LPs negotiating with fund managers now scrutinize hurdle rates, carry structures, and clawback provisions carefully before committing capital.

How Returns Are Actually Generated

VCs make carry only if their portfolio companies generate exits. There are three primary exit routes:

IPO (Initial Public Offering)

When a startup goes public on BSE or NSE, early investors can sell their shares. Think of Zomato, Paytm, Nykaa, or Mamaearth; each of these gave early-stage VCs an opportunity to partially or fully exit.

An IPO is considered the most prestigious exit, though the lock-up period (often around 6 months for pre-IPO investors in India) means VCs cannot immediately liquidate all their holdings.

Also Read: How Inflation Impacts Your Retirement Corpus Over Time

Strategic Acquisition (M&A)

A larger company acquires the startup. This is common in sectors like fintech, SaaS, and logistics. The acquirer pays a premium, the VC gets cash or stock in the acquirer, and the investment is realised.

In India, we have seen acquisitions by both domestic conglomerates (Reliance, Tata) and global technology companies looking to enter or expand in the Indian market.

Secondary Sales

A VC can sell its stake to another investor either a later-stage VC, a private equity firm, or a strategic investor without the company going public. This gives early funds liquidity before an IPO and has become increasingly common in the Indian startup market.

The Power Law

Here is the uncomfortable truth about venture capital: most investments fail or return very little. As per data, out of 20 bets in a portfolio, a VC typically expects:

- 10–12 startups to fail or return less than invested

- 5–6 to return the capital or generate modest returns

- 2–3 to do reasonably well

- 1 to be the ‘fund returner’ a single investment that returns more than the entire fund

This is called the power law distribution of returns. For instance, Flipkart, Zomato, or Freshworks-type investment in the early years could return 50x or 100x, compensating for the many smaller failures.

This explains why VCs chase hypergrowth opportunities and large addressable markets. A safe, steady business might be a good investment for a bank or an angel but a VC needs to find companies that have the potential to become very large, very fast.

A Simple VC Fund Example

Let us walk through a hypothetical Indian VC fund:

| Item | Details |

|---|---|

| Fund Size | ₹400 crore |

| Management Fee | 2% per year for 5 years = ₹40 crore total |

| Portfolio | 20 startups |

| Outcome | 14 fail, 4 modest returns, 1 returns ₹200 crore, 1 returns ₹600 crore |

| Total Returns | ₹900 crore |

| Profit for LPs | ₹900 crore - ₹400 crore = ₹500 crore |

| LP Share (80%) | ₹400 crore |

| Carry to GPs (20%) | ₹100 crore |

The GP partners share ₹100 crore in carry in addition to the management fees they collected over the years to run the firm.

Why This Matters for Indian Founders

VCs need big outcomes. They are not looking for a business that makes ₹10 crore profit in year three. They need companies that can potentially return the entire fund which means billion-dollar outcomes are not optional, they are the target.

Timeline matters. VC funds have a defined life typically 10 years. This creates pressure to exit. A founder should understand that their VC partner is not a permanent shareholder. At some point, a liquidity event is expected.

Alignment of incentives. The VC's carry is tied entirely to your success. When a VC really believes in your startup, it is not just enthusiasm; their financial future depends on your outcome.

Not all money is the same. A VC fund that is in year 8 of a 10-year life will think very differently from one in year 2. The older fund may push harder for an early exit, while the newer one may be comfortable with a longer growth runway.

The broader ecosystem of startup funding in India continues to attract global attention. Navigating the landscape of VC funding in India requires a deep understanding of market dynamics. Securing Series A funding in India has become highly competitive for early-stage companies. Companies seeking Series B funding in India must demonstrate strong, scalable revenue metrics. Navigating startup fundraising in India requires resilience and a compelling pitch deck.

The Indian VC Landscape Today

India is home to a growing number of domestic VC funds Blume Ventures, Kalaari Capital, Nexus Venture Partners, Stellaris, and many others alongside India-focused vehicles of global funds like Sequoia (Peak XV), Lightspeed, and Accel. The ecosystem has also seen the rise of micro-VCs and sector-specific funds focused on areas like climate tech, deep tech, and agritech.

Domestic pioneers like Blume Ventures India have laid the groundwork for early-stage investing.

Firms such as Kalaari Capital India continue to champion domestic innovation.

The presence of Lightspeed India VC highlights the global interest in Indian tech startups.

SEBI's Alternative Investment Fund (AIF) framework, particularly Category I and Category II AIFs, governs how VC funds are structured and operated in India. This regulatory clarity has helped bring more institutional capital into the asset class domestically.

Choosing the correct SEBI AIF category is a critical step in legally structuring a fund.

Registering as an alternative investment fund in India ensures compliance with federal financial laws.

Closing Thoughts

Venture capital is, at its core, a business of patient capital, calculated risk, and asymmetric returns. The management fee keeps the firm running. The carried interest is the prize.

Grasping these venture capital basics is the first step toward successful fundraising.

Understanding how do venture capitalists make money, the mechanics of venture capital profits, and the realities of VC investment strategy helps founders, aspiring investors, and policymakers engage more meaningfully with the capital shaping India's next generation of companies.

Start your smart investing on CubePlus and take control of your financial goals.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.