_11zon.webp%3Falt%3Dmedia%26token%3D92dfac50-382c-43d9-a2ac-d00ef586a496&w=3840&q=85)

Walk into a supermarket in Mumbai or Bengaluru, and you will notice something interesting. A packet of biscuits priced at ₹20 in one shop may cost ₹22 in another. The biscuits are the same, but the price difference comes from the margins retailers add for their service. This is a simple way to think of mutual fund expenses explained in daily life.

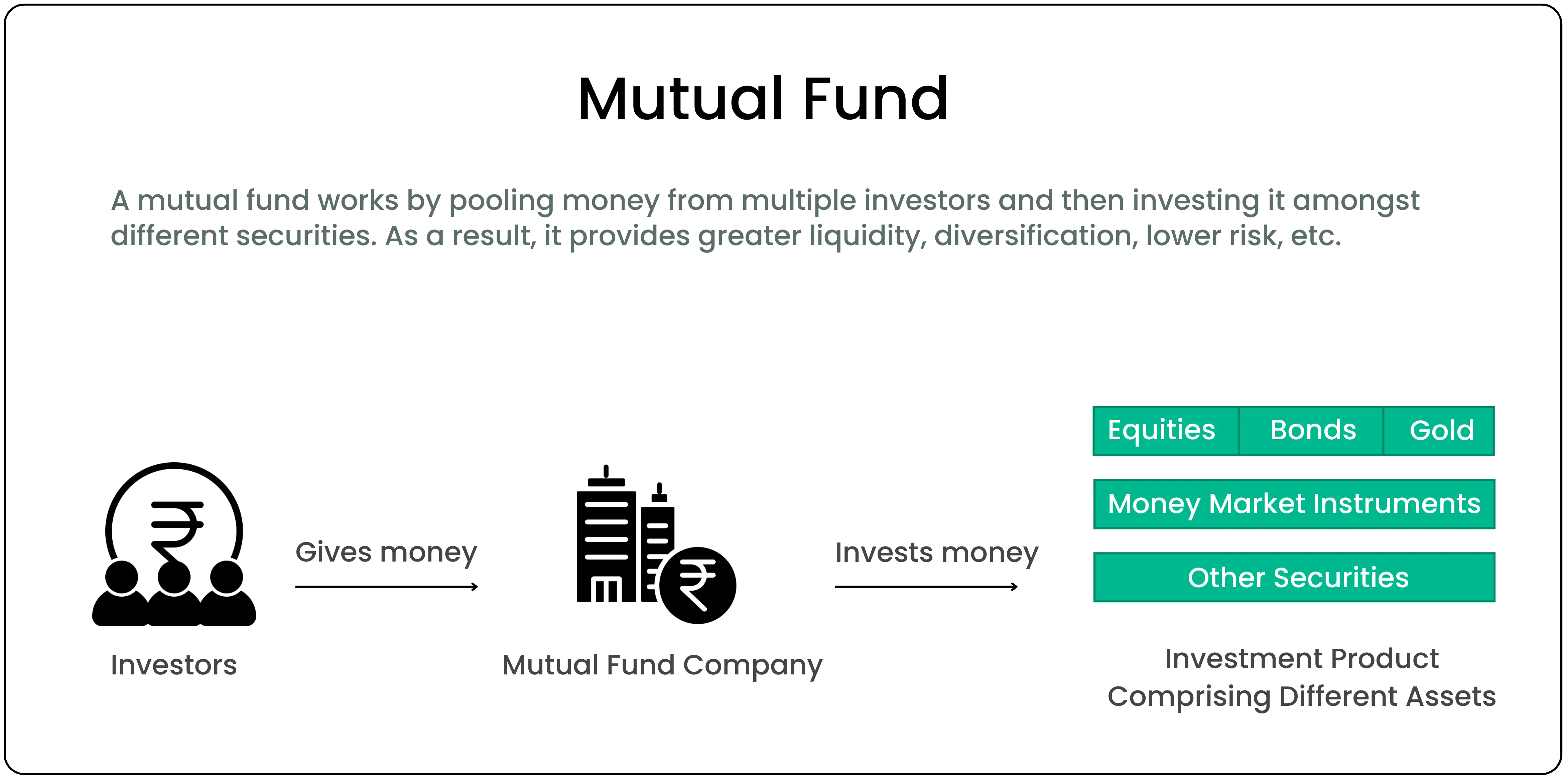

Mutual funds operate on a similar principle. Running a fund is not free. There are research analysts, fund managers, compliance staff, custodians, and brokers to ensure your money is invested effectively. To recover these costs, mutual funds charge investors a fee known as the Total Expense Ratio (TER).

What does TER cover?

The TER is not just about paying the fund manager. It includes brokerage on trades, fees paid to custodians who hold the securities, technology infrastructure, employee salaries, and marketing expenses. The idea is simple: managing thousands of crores of investor money requires an entire ecosystem, and this system has to be funded. This is essentially mutual fund expense ratio India in action.

Total Expense Ratio (TER) Formula

The Total Expense Ratio shows how much of a mutual fund’s assets are used to cover its expenses. It is calculated as:

TER = (Total Expenses ÷ Total Fund Assets) × 100

- Total expenses are all costs involved in running the fund, such as fund manager’s fees, administration charges, audit fees, marketing expenses, and transaction costs.

- Total fund assets are the market value of all investments (stocks, bonds, etc.) held by the mutual fund.

Curious about what a Registrar and Transfer Agent does? Here’s a quick read:

The Importance of RTA Agents in Mutual Fund Management

How do you pay this fee?

Here’s the part that often surprises new investors. You never see an invoice for TER. The AMC adjusts it quietly from the mutual fund NAV and expenses every day.

For example, if a fund has an expense ratio of 1% and you’ve invested ₹1 lakh, about ₹1,000 a year goes towards expenses. But instead of deducting it in one go, the AMC spreads it across 365 days, so roughly ₹2.7 is adjusted daily. This is why the NAV you track is always after expenses have been accounted for.

Direct vs Regular

Every mutual fund is offered in two formats: Direct and Regular.

- Direct Plans: You invest straight with the AMC, and no commissions are paid out. The TER here is lower.

- Regular Plans: You invest via a distributor or advisor, and part of the TER goes towards their commission.

To put this into perspective: in 2025, the TER of large-cap equity funds is around 0.9%–1.1% for Direct Plans and 1.6%–2% for Regular Plans. A gap of 0.7% may look small, but over 15 years, it can translate into lakhs of rupees in difference.

Take HDFC Top 100 Fund, for instance. As of August 2025, its Direct Plan NAV is significantly higher than its Regular Plan NAV, not because it’s ‘costlier to buy,’ but because investors in Direct Plans have saved more by avoiding distributor commissions.

A 10-year SIP example

To see the difference clearly, consider this illustration:

| **Monthly SIP | Tenure | Assumed Return (before expenses) | Direct Plan (TER 1%) | Regular Plan (TER 1.7%) | Difference** |

|---|---|---|---|---|---|

| ₹10,000 | 10 years | 12% per annum | ₹23.2 lakh | ₹21.6 lakh | ~₹1.6 lakh |

Even with the same portfolio, the higher expense ratio in a Regular Plan quietly eats into long-term wealth. The longer the tenure and the higher the investment, the bigger the gap becomes.

Should you always choose Direct?

Not necessarily.

If you are confident in choosing funds and tracking them, Direct Plans help you save costs. But if you are unsure, an advisor through a Regular Plan can be valuable. They guide you on asset allocation, review your portfolio, and keep you invested during market downturns, something many investors struggle with.

The regulatory push for transparency

In the past, many investors weren’t even aware of the difference between Direct and Regular Plans. But SEBI has tightened rules in recent years. AMCs must now disclose TERs prominently on their websites, along with distributor commissions. This transparency helps investors make more informed choices.

Small fees, big impact

Mutual funds don’t charge you separately the way Ola or Amazon does. Instead, they recover costs quietly by adjusting the NAV. Whether you choose Direct or Regular plans depends on how much guidance you need. But understanding TER and how it affects your long-term wealth is key to being a smarter investor.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.