When exploring mutual funds, one key decision you will need to make is whether to choose a direct plan or a regular plan. While the difference may seem technical at first, it can have a significant impact on your returns, the kind of advice you receive, and how involved you want to be in managing your investments

Difference Between Direct and Regular Mutual Fund:

What is a direct mutual fund?

A direct mutual fund is a type of plan where you invest directly with the mutual fund company or an asset management company, without involving any brokers, advisors, or distributors. This is known as a direct mutual fund plan or direct fund, where the investor deals directly with the fund house. Since there are no distribution or marketing costs, the expense ratio is lower compared to regular mutual fund plans.

And that’s where the real benefit lies. In the long run, even a slight variation in the expense ratio of a mutual fund can lead to a significant jump in your overall investment value, especially in actively managed and equity funds. Direct plans can be accessed conveniently through direct plans online, making mutual fund investment easier and more cost-effective for tech-savvy investors.

What is a regular mutual fund?

A regular mutual fund is what you get when you invest in a mutual fund scheme through a broker, advisor, or distributor. These intermediaries, such as a mutual fund distributor or a bank's relationship manager, play a key role in advising investors and providing ongoing services like portfolio monitoring and support.

But their support doesn’t come free. The mutual fund company pays them a fee, which is a commission paid to the distributor or advisor and is deducted from the fund’s assets and built into the overall expense ratio. This commission covers services such as generating account statements, processing transactions, and maintaining investor communication.

That means your investment will have a higher expense ratio compared to the same mutual fund scheme under a direct plan. This slightly higher expense ratio results in marginally lower returns for regular funds. However, many investors value the ongoing services and personalized advice provided by investment advisors and mutual fund distributors, especially during market volatility.

Why does the expense ratio matter?

Formula:

Expense Ratio (%) = (Total Operating Expenses ÷ Average Net Assets) × 100

This ratio varies depending on whether the plan is direct or regular. Direct mutual funds have a lower expense ratio, as they don’t include distribution expenses or brokerage fees.

According to limits set by SEBI (Securities and Exchange Board of India), fund houses are capped on what they can charge. But even within those limits, regular funds are costlier.

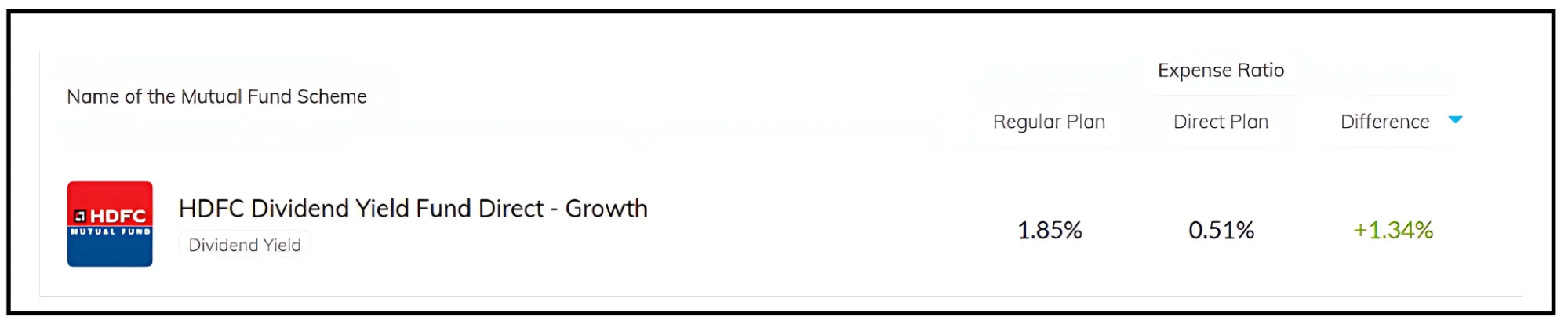

The difference in expense ratios between direct and regular plans is shown below.

Who is investing in direct mutual funds?

All major fintech brokerage houses are promoting direct mutual funds for the benefit of investors

Return on direct mutual fund i much higher than regular mutual fund due to its lesser expense ratio.

The trend towards direct mutual funds is gaining traction. Look at some major asset management companies that hold a major percentage of holdings through direct plans.

SBI Mutual Fund: 56% of AUM is in direct mutual fund plans

ICICI Prudential: 48% in direct plans

HDFC MF: 42% in direct plans

Overall, around 45% of mutual fund investments are now through direct plans, with that portion steadily increasing. Most of these come from investors who prefer to make their own decisions and align their investments with personal goals, often because they have the market knowledge required to select suitable funds without external guidance.

Which one is better?

While direct mutual funds may seem like an easy win due to their lower expense ratio, it is not a one-size-fits-all situation.

With regular mutual funds, you don’t just buy a product, but you also get support. A distributor or advisor can:

Help define your financial goals

Assist with goal-based planning

Evaluate your risk appetite

Help select a suitable mutual fund scheme

Build a diversified mutual fund portfolio

Advise on asset allocation across various asset classes for effective risk management

Guide you through choosing the right fund mix

This guidance can be especially helpful when choosing between debt funds, liquid funds, or equity funds, or when trying to understand NAV changes. Advisors also help diversify your investments across asset classes, which is a key part of effective risk management.

Without support, DIY investors may choose volatile schemes like small-cap or sectoral funds without realizing the risks. A market dip can then derail long-term goals.

Still paying for advice, just differently

Even though direct mutual fund plans don’t involve a distributor, in cases where you need help, you might end up hiring a financial advisor on a fee basis. Alternatively, investors can seek advisory services from SEBI-registered investment Advisors (RIAs), who charge a fee for their expertise and facilitate direct investments without involving distributors.

So while you save on embedded commissions, you may still bear advisory costs. The total cost might be similar to regular mutual fund investments when analyzed; only the structure will remain different.

Who should go for direct mutual funds?

Direct plans are great for:

Experienced investors (well-suited for direct plan investments)

Those who understand how mutual funds work

People are comfortable evaluating NAVs and fund strategies

Investors who regularly review and rebalance portfolios

These individuals can align their investments with their financial goals and take full control of fund selection, making direct plan investments directly from the Asset Management Company (AMC) without intermediaries.

Who should stick with regular mutual funds?

Regular plans are a better fit for:

People unfamiliar with mutual fund choices

Those seeking guidance for complex decisions

Investors who prefer structured, goal-based investment support

Such investors benefit from the personalized service offered by mutual fund advisors, distributors, and financial advisors.

Switching isn’t always free

Switching between direct and regular plans isn’t seamless. It is treated as a redemption and a fresh investment, which means:

You might have to pay capital gains tax

Your investment holding period resets, affecting long-term tax benefits

Investors should carefully consider the tax implications before making a switch between direct and regular plans, as this can impact capital gains tax, lock-in periods, and exit loads.

While the mutual fund industry is working with SEBI to simplify this, the rule currently still applies.

Also Read: Are Mutual Funds Safe? Who’s Handling My Money, And Can I Trust Them?

Know yourself first

Whether you choose direct funds or stick with regular plans, it comes down to your comfort and expertise. The choice between regular and direct mutual fund options depends on your familiarity with investing and how much guidance you need.

If you are confident about making investment decisions, comparing expense ratios, and managing your portfolio, direct mutual fund plans are the more cost-effective choice.

But if you value ongoing advice and handholding, a regular mutual fund plan suits you despite the higher expense ratio. They offer peace of mind and a guided approach. Whether you choose a direct or regular plan, both regular and direct plans have their advantages based on investor needs.

Understanding Net Asset Value (NAV)

Net Asset Value (NAV) is a fundamental concept in mutual fund investing, representing the per-unit value of a mutual fund scheme at any given time. Simply put, NAV is calculated by dividing the total value of a mutual fund’s assets by the number of outstanding units. This figure gives investors a clear snapshot of what each unit of the mutual fund is currently worth in the market.

When comparing direct mutual funds and regular mutual funds, NAV becomes an important indicator of how your investment is performing. One of the key differences between direct and regular mutual funds lies in their expense ratios. Direct mutual funds have lower expense ratios because they do not include distribution expenses or commissions paid to intermediaries. As a result, the costs deducted from the fund’s assets are lower, which means the NAV of direct mutual funds is typically higher than that of regular mutual funds for the same mutual fund scheme.

On the other hand, regular mutual funds have higher expense ratios due to the inclusion of distribution expenses and commissions paid to mutual fund distributors. These higher costs are subtracted from the fund’s assets, resulting in a slightly lower NAV compared to direct mutual funds. Over time, this difference in NAV can have a significant impact on the value of your mutual fund investments, especially when compounded over the long term.

Understanding NAV is crucial for making informed investment decisions. A higher NAV in direct mutual funds reflects the benefit of lower expense ratios, allowing your investment to grow more efficiently. However, NAV should not be the only factor you consider. It’s also important to evaluate the total expense ratio, the investment process, your risk appetite, and your overall investment strategy when choosing between direct and regular mutual funds.

By comparing the NAVs of direct and regular mutual funds, along with other key factors, you can select the mutual fund option that best aligns with your financial interests, investment goals, and risk tolerance. Whether you prefer the cost efficiency of direct mutual funds or the value-added services of regular mutual funds, understanding how NAV works will help you optimize your investment portfolio and achieve your long-term objectives.

Corpus Comparison Over 10 Years in Direct plan vs Regular plan

Assuming

SIP ₹2 Lakh per year

Direct Plan Total Expense Ratio (TER): 1.0%

Regular Plan Total Expense Ratio (TER): 1.75% (i.e., 0.75% higher than direct)

| Year | Total Invested | Regular Plan (16.25% return) | Direct Plan (17% return) | Additional return in direct plan |

|---|---|---|---|---|

| 1 | ₹2,00,000 | ₹2,32,500 | ₹2,34,000 | ₹1,500 |

| 2 | ₹4,00,000 | ₹5,02,781 | ₹5,07,780 | ₹4,999 |

| 3 | ₹6,00,000 | ₹8,16,983 | ₹8,28,103 | ₹11,119 |

| 4 | ₹8,00,000 | ₹11,82,243 | ₹12,02,880 | ₹20,637 |

| 5 | ₹10,00,000 | ₹16,06,857 | ₹16,41,370 | ₹34,513 |

| 6 | ₹12,00,000 | ₹21,00,472 | ₹21,54,402 | ₹53,931 |

| 7 | ₹14,00,000 | ₹26,74,298 | ₹27,54,651 | ₹80,352 |

| 8 | ₹16,00,000 | ₹33,41,372 | ₹34,56,942 | ₹1,15,570 |

| 9 | ₹18,00,000 | ₹41,16,845 | ₹42,78,622 | ₹1,61,777 |

| 10 | ₹20,00,000 | ₹50,18,332 | ₹52,39,987 | ₹2,21,655 |

Over 10 years, assuming a CAGR of around 17% return on the scheme, just a 0.75% higher expense ratio in the regular plan results in a loss of ₹2.2 lakh in returns. This highlights how even a small difference in costs, such as the TER, can have a significant impact on the final corpus due to the power of compounding over the long term.

Making the right choice for your portfolio

Choosing between direct and regular mutual funds is not just about cutting costs. It is about choosing what aligns better with your financial goal and investment horizon.

Whether you are looking at actively managed funds, equity schemes, or debt options, always factor in the expense ratio and your ability to stay invested during market ups and downs. Investors should also compare different mutual fund schemes offered by each mutual fund house to find the most suitable investment scheme for their goals.

If you want to make your investments more cost-efficient, investing through Tradejini can help. Tradejini offers direct mutual fund plans, which means zero distributor commissions and lower expense ratios, allowing you to earn more over time from the same fund compared to a regular plan.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

©️ 2025 — Tradejini. All Rights Reserved.