Mutual funds have become a cornerstone of investment portfolios in India, offering a blend of professional management, diversification, and the potential for attractive returns. However, understanding how mutual fund returns are calculated and interpreted is crucial for making informed decisions and aligning investments with financial goals. Let’s explore the various facets of mutual fund returns, demystifying key concepts and methodologies.

What are mutual fund returns?

Mutual fund returns represent the profit or loss generated from an investment in a mutual fund scheme over a specific period. These returns reflect the change in the value of your investment, factoring in market performance, dividends, and interest income. They serve as a critical metric for evaluating the effectiveness of a fund manager and the suitability of a fund for your investment objectives.

Best mutual fund returns and types explained

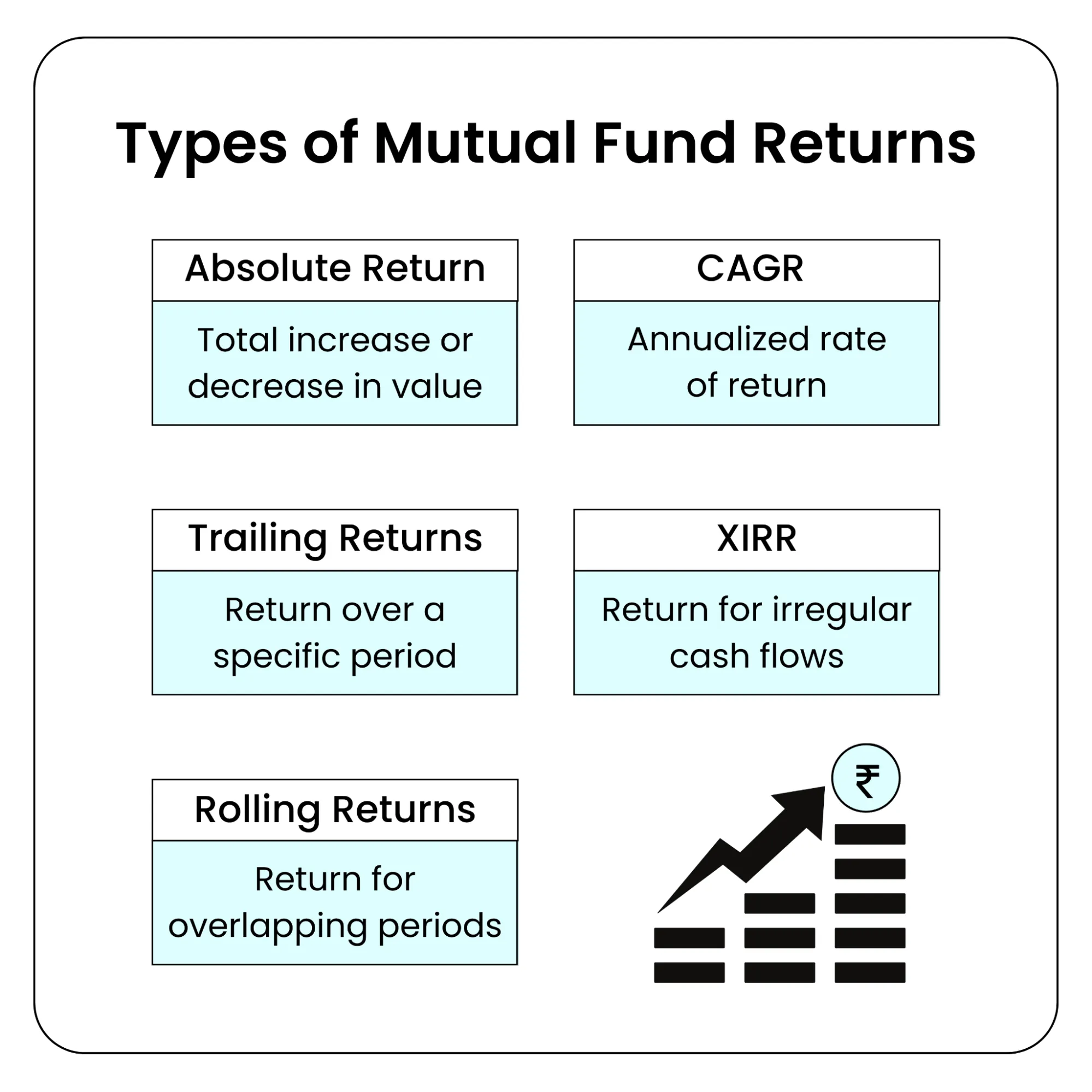

1) Absolute Returns

Absolute return is the simplest measure, representing the total percentage change in your investment over a given period, without considering the time frame. Investors are often attracted to absolute returns because they seek high returns even over short periods, making this metric relevant. It is calculated as:

.webp?alt=media&token=8ccae7e7-47e5-428b-aeed-d519b2a5a12f)

This method is most appropriate for investment periods of less than one year. For example, if you invested ₹1,00,000 and it grows to ₹1,20,000, your absolute return is 20%. Absolute returns are particularly useful for evaluating short-term investments or those made with a low amount of capital.

1.1 Understanding Absolute Returns

Absolute returns represent the total gain or loss on an investment, including dividends, interest, and capital gains, over a specific period. This metric gives investors a straightforward view of how much their investment has grown, without adjusting for the time taken. When assessing a mutual fund, it’s important to look at its absolute returns in relation to its benchmark and similar funds in the same category. This comparison helps investors determine whether a fund is truly performing well or simply riding market trends. However, while a higher absolute return is attractive, investors should also consider the level of risk taken to achieve those returns. Calculating absolute return is simple: (End Value - Beginning Value + Dividends) / Beginning Value.

1.2 Investment considerations

Before investing in mutual funds, it’s essential to weigh several key factors to ensure the investment matches your needs and expectations. Start by checking the minimum investment required for the fund, as this can vary across schemes. The expense ratio, or the fee charged by the fund house for managing your money, directly impacts your net returns lower expense ratios are generally preferable. Your risk appetite plays a crucial role: investors with a high risk appetite may seek funds with higher risk for the potential of higher returns, while those with lower risk tolerance might prefer more stable, conservative funds. Professional management is another important aspect; a skilled fund manager with a strong track record and relevant expertise can make a significant difference in the fund’s performance.

1.3 Evaluating fund performance

Evaluating the performance of a mutual fund is crucial for predicting its future potential and making informed investment choices. Investors should review the fund’s returns over different time periods such as one, three, and five years to gauge its consistency and ability to handle market volatility. Comparing a mutual fund’s performance to its benchmark and peer group helps determine whether the fund is outperforming or lagging behind similar options. A strong track record of delivering higher returns than both the benchmark and category average is a positive sign of effective management. It’s also important to consider the expense ratio and any other fees charged, as these can eat into your returns over time. By thoroughly evaluating a fund’s performance, including its volatility and consistency across various time periods, investors can identify the right fund that aligns with their financial goals, risk tolerance, and desire for higher returns.

1.4 Selecting the Right Investment

Choosing the right mutual fund investment involves aligning your financial goals, risk appetite, and investment horizon with the fund’s characteristics. Start by assessing your risk tolerance if you have a high risk appetite and a long-term outlook, equity funds may offer the potential for higher returns, while those with a lower risk tolerance might find debt funds more suitable. Consider the fund’s investment objective and ensure it matches your desired return and time frame. It’s also important to review the fund’s portfolio, including the types of assets and stocks it holds, to ensure they fit your investment strategy. Professional management can add value, so look for funds managed by experienced professionals with a proven track record.

1.5 Long-term strategy

Adopting a long-term strategy is key to successful investing in mutual funds. By staying invested over several years, investors can ride out short-term market volatility and harness the power of compounding to grow their wealth. It’s important to have a clear understanding of your financial goals and risk tolerance to develop a strategy that’s both suitable and sustainable. Systematic Investment Plans (SIPs) are an effective way to invest regularly, regardless of market conditions, helping to average out purchase costs and reduce the impact of market fluctuations. Regularly evaluating your fund’s performance and rebalancing your portfolio as needed ensures your investments remain aligned with your goals and risk tolerance. With a thoughtful long-term strategy, investors can maximize the potential of mutual funds and build a secure financial future.

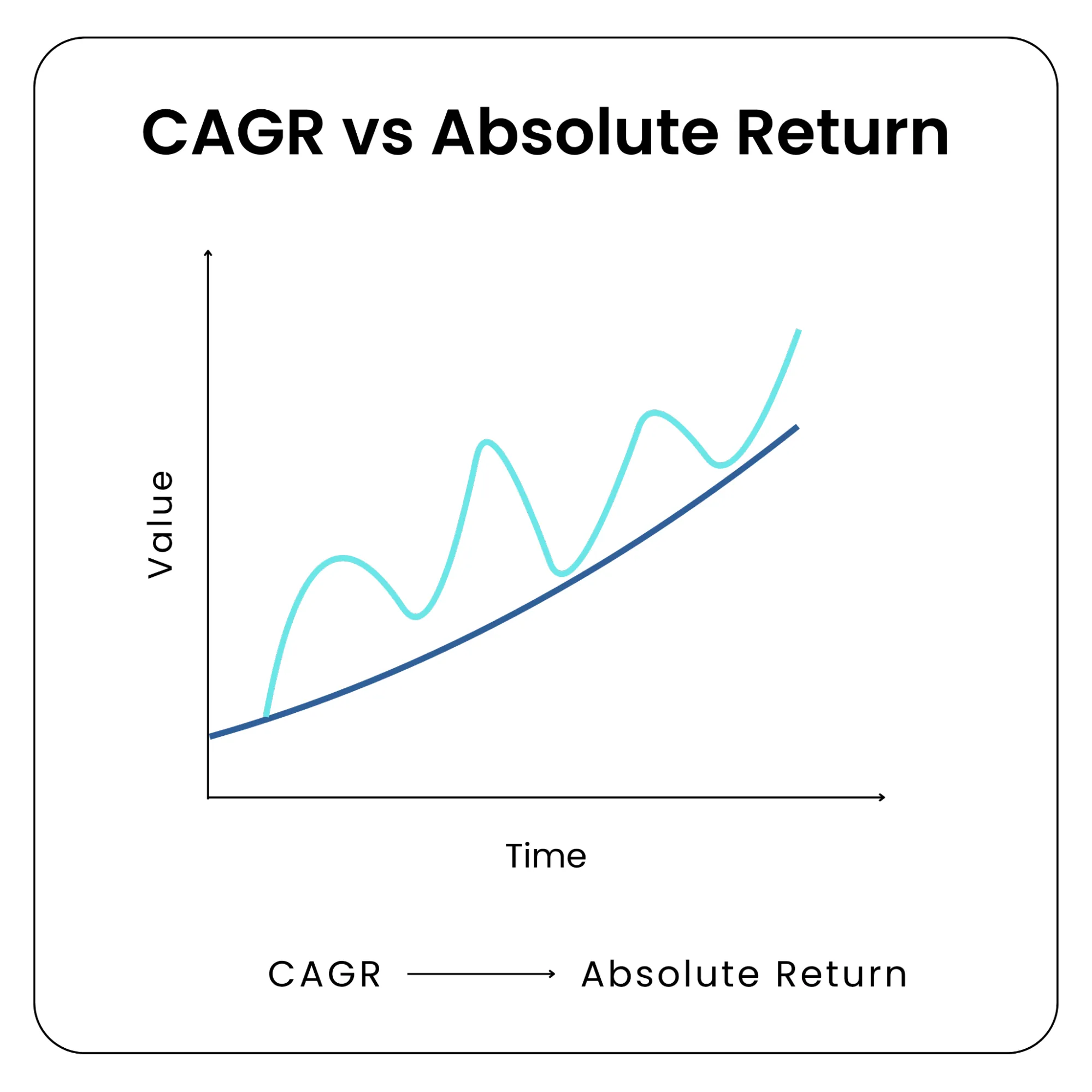

2. Annualised Returns

When investments span multiple years, annualized returns provide a more accurate picture by converting total returns into an average yearly rate. These returns take into account the effect of compounding and the time period, providing a more accurate comparison across funds. This enables comparison across different funds and timeframes. The most common form is the Compounded Annual Growth Rate (CAGR):

.webp?alt=media&token=8849d520-31f8-46d1-ade2-8c0ec96df5c3)

Where n is the number of years, CAGR smooths out fluctuations, giving a consistent annual growth rate.

3. Trailing and Point-to-Point Returns

Trailing Returns: Trailing and point-to-point returns are important tools for assessing a fund's performance over different periods. Trailing returns measure the fund’s performance over a specified period ending on the current date (e.g., 1-year, 3-year, 5-year trailing returns). Point-to-Point Returns: These are calculated between two fixed dates, useful for comparing a fund's performance during specific market cycles.

4. Rolling Returns

Rolling returns provide insights into a fund’s consistency by calculating returns for overlapping periods (e.g., 3-year returns calculated every month over the last 10 years). This helps assess how often a fund has delivered expected returns, smoothing out market volatility, and is especially useful for identifying funds with reliable performance over time.

5. Total Returns

Total returns take into account both capital appreciation (NAV growth) and any dividends distributed by the fund, offering a holistic view of overall gains.

6. XIRR (Extended Internal Rate of Return)

XIRR is used to calculate returns in cases of multiple investments or SIPs (Systematic Investment Plans) over time. It factors in the irregularity of cash flows, making it a more accurate return metric for most retail investors. When investing through SIPs, investors contribute a fixed amount at regular intervals. SIPs allow investors to start with a low investment amount, making them accessible to a wide range of people.

Calculating mutual fund returns: Lumpsum vs SIP

For example, if you invest ₹2,000 every month for 5 years and the fund grows at an average rate of 12% per annum, the XIRR method will help you determine your actual annualized return. To achieve the full benefit of SIPs, investors need to stay invested for the long term to realize steady returns.

Lump Sum Investments

For one-time investments, returns are typically calculated using absolute or CAGR methods. Online mutual fund calculators simplify this process: input your investment amount, duration, and expected rate of return to estimate future value.

Additionally, regulatory oversight in India ensures a high level of security for investors making lump sum investments, providing transparency and protection in the mutual fund environment.

Systematic Investment Plan (SIP)

SIPs, where investors contribute a fixed amount at regular intervals, require a different approach due to the effect of compounding on multiple cash flows. The Extended Internal Rate of Return (XIRR) method is commonly used for SIPs, as it accounts for the timing and amount of each investment. Most mutual fund calculators in India offer SIP-specific calculations to estimate maturity amounts.

Example: Investing ₹10,000 per month for 5 years at an expected 12% annual return can yield approximately ₹8.11 lakh at maturity, demonstrating the power of regular investing and compounding

Factors affecting mutual fund returns

Market Conditions: Returns vary with equity market trends, interest rates, and -economic cycles. Equity funds in India have historically delivered 10–15% annual returns over the long term, while debt funds offer 6–8%. Fund Type: Equity, debt, hybrid, and sectoral funds all have different risk-return profiles.

Fund Manager’s Skill: The fund manager’s experience, including their track record and professional background, plays a crucial role in delivering consistent returns and building investor confidence.

Expense Ratio: Higher fund management fees can reduce net returns.

Taxation: Returns are subject to capital gains tax, with different rules for equity and debt funds. Equity Linked Savings Schemes (ELSS) also offer tax benefits under Section 80C.

Interpreting fund returns: Benchmarks and peer comparison

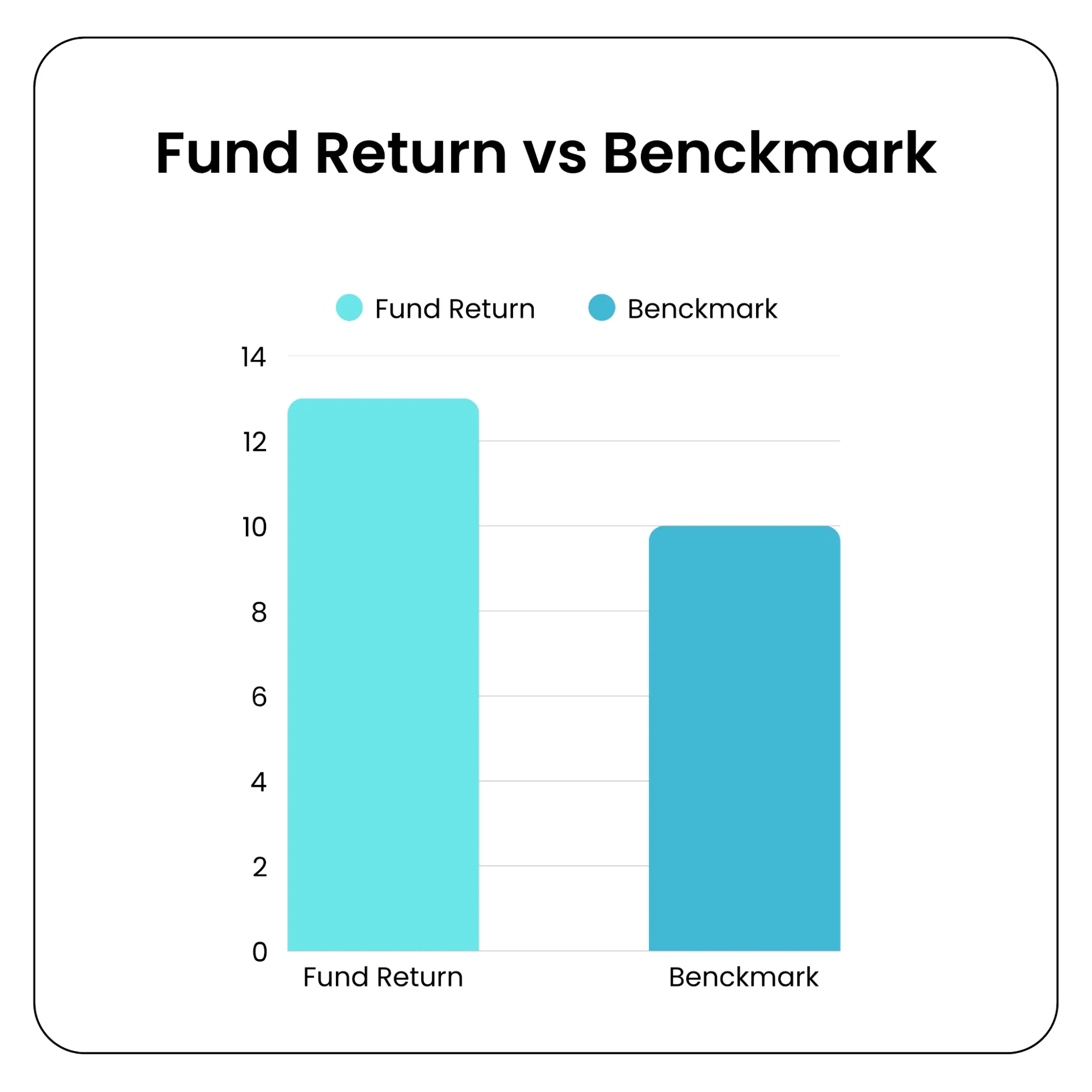

1. Benchmark comparison

Every mutual fund is benchmarked against an index (e.g., Nifty 50, Nifty Small Cap 150, etc.). Comparing fund returns to its benchmark helps assess outperformance (alpha) or underperformance.

2. Category averages

Comparing a fund’s return with peers in the same category (like large-cap equity, ELSS, or short-term debt funds) helps evaluate relative performance.

3. Risk-adjusted returns

Ratios like Sharpe Ratio, Sortino Ratio, and Alpha are used to evaluate returns in the context of risk taken. A fund delivering higher returns with lower volatility is generally more desirable.

Key considerations for investors: When choosing mutual funds, investors should keep several important factors in mind:

Align with Financial Goals: Investors should choose funds based on their goals, risk tolerance, and investment horizon. For example, young investors with long-term goals like retirement may opt for equity funds, while those saving for short-term goals may prefer debt or liquid funds.

Evaluate Past Performance: While past returns are not a guarantee of future results, they provide insights into a fund’s consistency. Compare a fund’s performance against its benchmark and peers.

Understand Risk: Higher returns often come with higher risks. Tools like standard deviation and Sharpe ratio can help assess a fund’s risk-adjusted returns.

Systematic Investment Plans (SIPs): SIPs are a popular way to invest in mutual funds in India, allowing investors to benefit from rupee cost averaging and compounding. For instance, a monthly SIP of ₹5,000 in an equity fund with a 12% CAGR could grow to over ₹23 lakh in 20 years.

Stay Informed: Monitor macroeconomic factors, such as interest rate changes by the Reserve Bank of India (RBI), which can impact debt funds, or corporate earnings trends affecting equity funds.

Understanding mutual fund returns is essential for every Indian investor aiming to build wealth and achieve financial goals. By grasping the different methods of calculating returns, using online calculators, and interpreting performance in the context of market dynamics and personal risk tolerance, investors can make informed decisions. A disciplined, long-term approach supported by a clear understanding of returns remains the key to successful investing in India’s vibrant mutual fund landscape.

Also Read: Investing in Precious Metals Through ETFs in India

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

©️ 2025 — Tradejini. All Rights Reserved.