Mutual funds are popular for many reasons, but one of the biggest draws is easy access to your money. Still, a common question remains: Can I pull out my investment whenever I want?

The short answer is yes, but there are a few key points to understand before you hit the redeem button. Here is what you should know before withdrawing your mutual fund investment.

Understanding the right way to withdraw mutual fund units

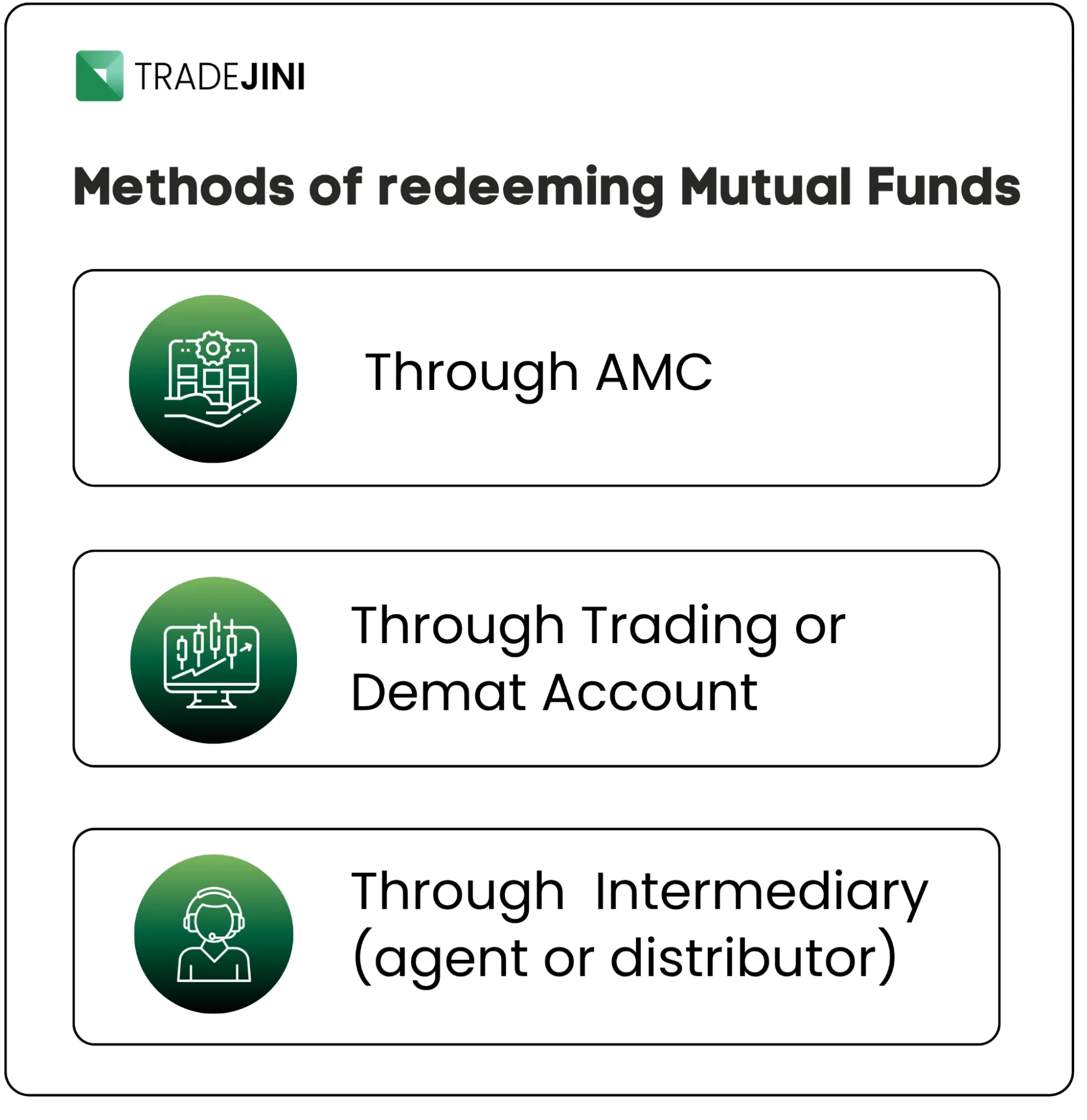

You can redeem open-ended mutual funds shortly after investing, and the amount is usually credited to your registered bank account within three business days. But the ease and timing of redemption also depend on the type of mutual fund and the process you use, whether through your demat or trading account, the AMC’s website, the mutual fund house, or the Registrar and Transfer Agent (RTA) like CAMS or KFintech. Transfer agents (such as CAMS or KFintech) facilitate the mutual fund redemption process, especially for online and offline submission.

If you are holding mutual funds in a demat account through CubePlus, you can log in to the platform, go to the mutual fund section, select the scheme, and place a sell order to redeem mutual fund units. The redemption proceeds will be credited to the bank account linked to your demat or trading account. If you hold units directly with the AMC or through an RTA, you can redeem by logging into their website or mobile app, or even by submitting a physical redemption form at their service centres.

You can choose either option, Online redemption or offline redemption

Offline mutual fund redemption

Collect a Redemption request form from your mutual fund house (AMC) or its service center.

Fill in the required details such as your name, folio number, scheme name, and the number of units you wish to redeem.

Sign the form and submit it at the Registrar’s office (like CAMS or KFintech), the AMC branch, or any authorized collection centre.

Once processed, the redemption amount will be credited to your registered bank account.

Online mutual fund redemption

Visit the official website of the AMC, MFCentral, RTA’s (CAMS/KFIN) Broker in case you hold demat holdings of mutual funds or use a third-party mutual fund platform.

Access your investments using your PAN or login credentials, whichever is applicable.

Select the mutual fund folio and scheme, and choose the number of units or amount to redeem.

Review and confirm the transaction. The redemption proceeds will be credited to your linked bank account after processing.

So, how liquid is your investment?

If you are investing in an open-ended mutual fund, it is pretty liquid. Once you place a redemption request, the money usually gets credited to your bank account within three business days. That is fairly quick compared to most other investments.

Some liquid funds also offer instant redemption, allowing investors to access their money the next day (T+1) during a financial emergency. This feature can be especially useful in situations like job loss or unexpected expenses, where quick access to cash is crucial.

However, some funds, like retirement funds, come with longer lock-ins. These may be locked for five years or until you reach retirement age, whichever is earlier.

Not all mutual funds are the same when it comes to withdrawals

Different mutual funds have different rules about how and when you can take your money out. For example, ELSS (Equity Linked Savings Scheme) funds have a three-year lock-in, which means you cannot withdraw your investment for three years from the date you invested.

On the other hand, open-ended mutual funds offer much more flexibility. You can redeem your investment whenever you need to. But, and this is important that you might have to pay an exit load if you pull out your money too early.

Debt funds have their own redemption rules and exit load structures, which may differ from those of equity or mid-cap funds.

Every AMC (Asset Management Company) sets its exit load structure for each mutual fund scheme. If you redeem your investment early, usually within the first year, exit loads can typically range from 0.25% to 2% depending on the scheme. However, most funds reduce or completely waive the exit load after a specified holding period, often after one year.

What is an exit load, and why does it matter?

An exit load is a small fee the mutual fund charges if you redeem your units before a specific period, usually a few months to a year. It is not meant to penalise you; it is just a way for fund managers to discourage short-term trading in long-term funds.

Say a scheme has a 1% exit load if you redeem within one year. You invested on April 1, 2024, and decided to withdraw on February 1, 2025, when the NAV (Net Asset Value) is ₹200. In this case, you would get ₹198 per unit after a ₹2 deduction.

Also Read: Mutual fund: Myths-Money and Making Smart Moves

Capital Gain Tax

In addition to exit loads, applicable taxes such as capital gains tax may apply when redeeming mutual fund units. Long-term capital gains are taxed differently from short-term gains, and the tax treatment varies for equity and debt funds. It is important to consider your investment horizon before redeeming, as holding investments for the long term can help reduce the impact of both taxes and exit loads.

These charges are mentioned in the fund’s official documents, like the fact sheet or key information memorandum, and so it is always a good idea to go through them.

Long-Term Capital Gains (LTCG)

Definition: Gains from the sale of equity shares or equity-oriented mutual funds held for more than 12 months.

Exemption limit: ₹1.25 lakhs per financial year (as per the new rule from Budget 2024).

Tax rate: 12.5% on LTCG above ₹1.25 lakhs, without indexation benefit.

Short-Term Capital Gains (STCG)

Definition: Gains from the sale of equity shares or equity-oriented mutual funds held for 12 months or less.

Tax rate: 20% flat rate on all short-term capital gains (no exemption limit).

STCG is applicable even on a ₹1 gain, with no threshold benefit.

What happens to your fund units when you redeem?

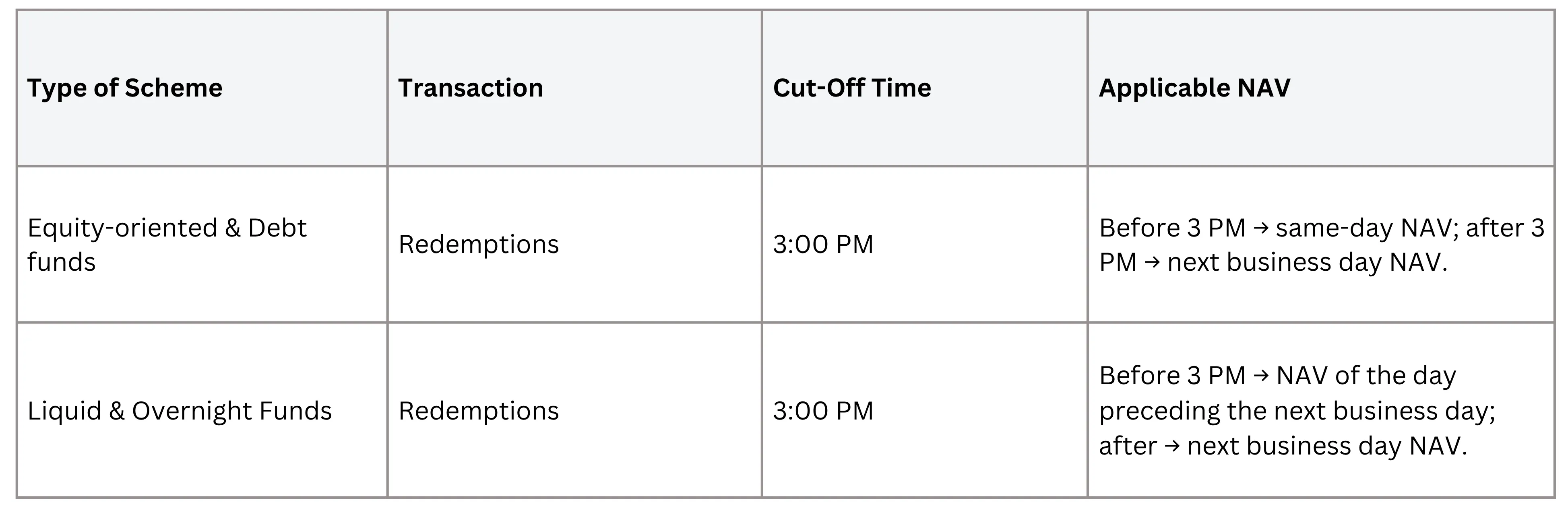

Units are debited from your scheme As soon as you place a redemption request, the equivalent number of mutual fund units is deducted from your scheme. This is based on the NAV applicable as per the cut-off time.

NAV is used to calculate the redemption amount

The Net Asset Value (NAV) applicable, whether same-day, previous-day, or next-day, depending on the time and fund type, is used to calculate your redemption value.

Redemption amount = Number of units x the applicable NAV.

Funds are transferred to your bank account

After processing, the money (redemption proceeds) is credited to your registered bank account, usually within:

T+1 working day for Overnight and Liquid funds

T+2 working days for equity, debt and hybrid funds

Now, when you want to redeem your investment, you have the flexibility to redeem all units or only a part of your holdings.

If you want to redeem the entire investment, you simply choose the ‘redeem all units’ option.

If you want to redeem partially, you can enter the number of units you want to sell (unit-based redemption) or specify the amount in rupees you wish to withdraw (amount-based redemption). In unit-based redemption, you specify the number of units redeemed, and the redemption amount is calculated using the applicable NAV. In amount-based redemption, you specify the amount, and the platform calculates the number of units redeemed based on the applicable NAV.

For example, if you have 1,000 units of a fund and the NAV is ₹100, your total investment is ₹1,00,000. You can choose to redeem ₹20,000 worth (amount-based redemption) or just 200 units (unit-based redemption), whichever method is easier for you. The number of units redeemed is calculated using the prevailing NAV, and the redemption amount is based on the current net asset value. The platform or AMC will calculate and process the redemption application.

When life throws a curveball: Redeeming in financial emergencies

Life does not always go according to plan. An unexpected hospital bill, sudden job loss or urgent home repairs can create financial pressure without warning. In such situations, your mutual fund investments can act as a financial cushion. But before you hit redeem, it is important to understand how it works and what you need to keep in mind. As explained in the earlier paragraph, knowing the turnaround time for different types of mutual fund schemes becomes crucial during emergencies. It helps you plan better and access funds more efficiently when every day matters.

Why investor returns might differ from scheme to scheme.

When you check mutual fund ads, they often show great returns. But as an investor, your actual return might be slightly lower. Why? Because charges exit loads, and taxes can reduce your take-home amount.

Open-ended funds = more liquidity, quick access to money

Exit loads = small fee if you redeem too early

Lock-ins = ELSS (3 years), retirement funds (5 years or till retirement)

Returns = actual investor returns may be slightly lower due to charges (expense ratio) and taxes

Investors should also consider redeeming their mutual fund units if the fund shows consistent underperformance, below-par performance, or negative alpha compared to benchmarks like the Sensex or Nifty50. Switching to a better-performing fund can help achieve financial goal completion and improve long-term returns.

Plan your investments with your timeline in mind

Before you invest, ask yourself, when will I need this money? You should align your mutual fund redemptions with your investment objectives and financial objectives to ensure your investment decisions support your overall financial plan. Planning redemptions around your investment horizon helps ensure you meet your financial goals efficiently. If it is in the short term, choose funds with no or low exit loads. If you are investing for the long term and do not mind a lock-in, options like ELSS could work well, especially if you are under the old tax regime.

Withdrawing smartly matters as much as investing wisely

Mutual funds offer easy access to your money, but smart withdrawals need planning. Check for lock-in periods, exit loads, and tax impact before redeeming. Open-ended funds offer flexibility, while ELSS and retirement funds require a longer commitment. Align your withdrawals with your financial goals to get the best out of your investment. If the fund's strategy no longer aligns with your objectives or risk profile, it may be time to redeem your units. Ensure that redemptions are processed through the same account used for the original investment to avoid any issues. Many platforms also provide other services, such as customer support and digital tools, to assist you with mutual fund redemptions.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.