India's external balance sheet quietly made a comeback in the March quarter of FY25. According to Crisil's latest ‘BoP First Cut’ report, India posted a current account surplus of $13.5 billion, or 1.3% of GDP, in the fourth quarter of FY25. That’s a sharp turnaround from the $11.3 billion deficit in the previous quarter and also an improvement over the $4.6 billion surplus in the same period last year.

So, what's behind this shift, and what should investors make of it?

What is a current account surplus?

A country records a Current Account Surplus when the money it earns from the rest of the world exceeds what it spends abroad. In simple terms, the world owes more to the country than the country owes others.

The current account balance is calculated as:

Current Account Balance = (Exports of Goods + Exports of Services + Primary Income Receipts + Secondary Income Receipts) - (Imports of Goods + Imports of Services + Primary Income Payments + Secondary Income Payments)

Primary investment income (e.g., interest, dividends, reinvested earnings) and compensation of employees (e.g., wages earned by Indian workers abroad).

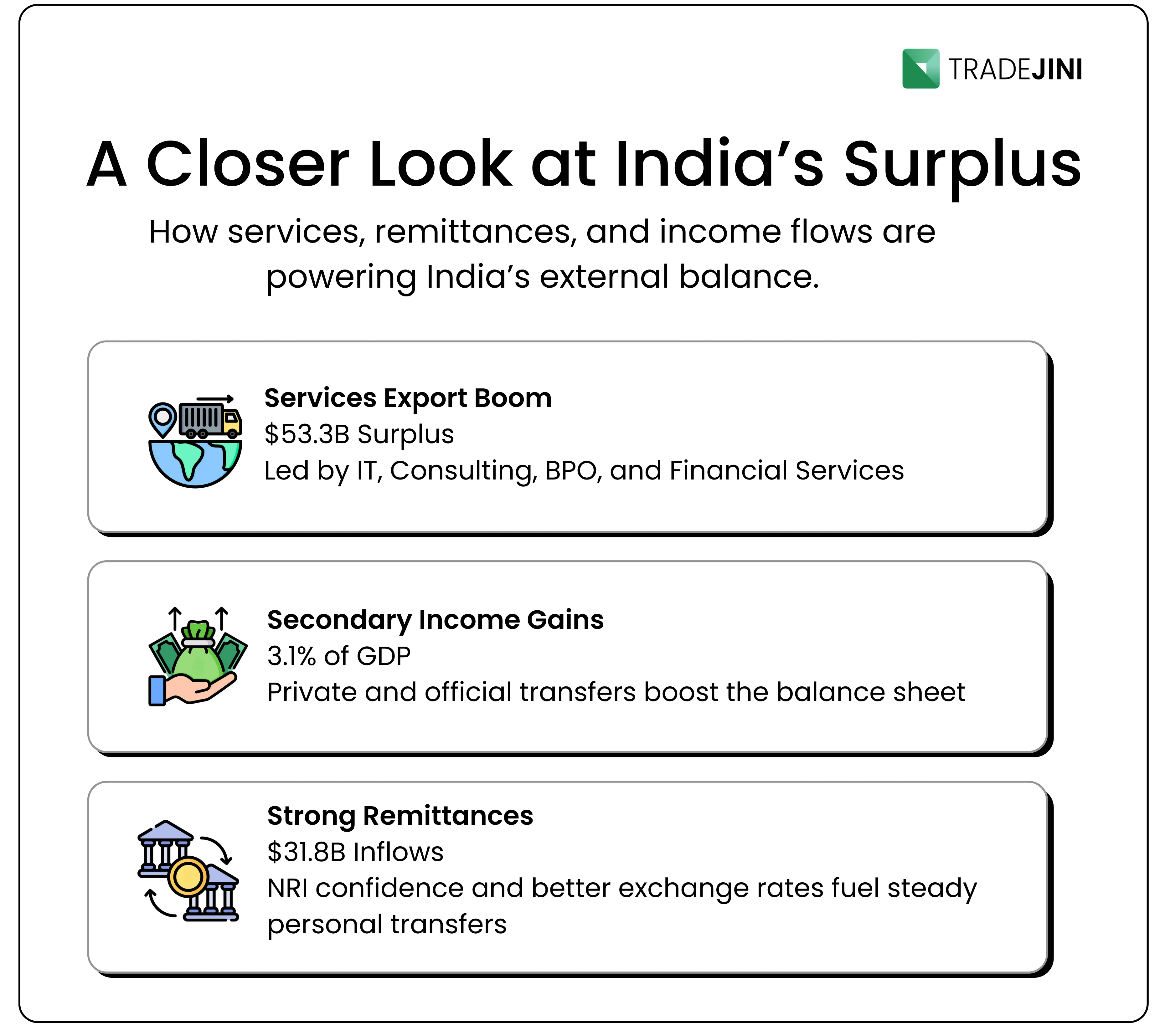

Secondary income includes private transfers (e.g., remittances from Indian workers abroad, a major inflow for India) and official transfers (e.g., grants from foreign governments).

The goods trade deficit widened to $59.5 billion, which put pressure on the balance, but it was more than offset by strong services and remittances.

But capital flows are drying up

The flip side to this optimistic current account story is the capital account, which witnessed some drag.

Foreign portfolio investors (FPIs) pulled out a net $5.9 billion in the March quarter, especially from equity and fund segments. With global risk appetite wavering, higher U.S. yields, and uncertainty around India's general elections during that period, this outflow isn’t entirely surprising.

FDI slowed down, with net inflows dropping to just $0.4 billion, versus $2.3 billion in the same quarter last year. Inflows dipped, and outflows edged up slightly.

NRI deposits and trade credit also saw moderation, while external commercial borrowings (ECBs) picked up slightly, possibly indicating that Indian corporates are still confident about raising debt abroad despite a stronger dollar.

Full-Year View

For the full fiscal year, India recorded a current account deficit (CAD) of $23.3 billion, or 0.6% of GDP, slightly narrower than FY24’s $26 billion (0.7% of GDP). This was achieved despite:

A higher goods trade deficit (7.3% of GDP vs. 6.7% last year)

Offset by a higher services trade surplus (4.8% of GDP vs. 4.5%)

Read More: How Global Economic Environment is Rapidly Changing

Outlook for FY26

Looking ahead, Crisil expects the CAD to widen to 1.3% of GDP in FY26. A few pressure points to watch:

Tariff-related volatility from the U.S. could hit India’s merchandise exports.

Middle East tensions could impact remittance flows and oil prices.

That said, India’s structural strengths, like a strong services sector and a steady stream of worker remittances, could cushion some of these shocks. The resilience of India's economy, strengthened by a strong services sector and steady remittances, contributed significantly to the current account surplus in the March quarter of FY25.

What does this mean for retail investors?

Here’s how this macro backdrop matters from an investor’s point of view:

Rupee stability could persist

A current account surplus usually supports the rupee. Even as capital flows weaken, the RBI's reserve buffer and a narrowing CAD could prevent major depreciation pressure.

For traders, this may reduce currency volatility but don’t discount global triggers.

Debt markets could stay attractive

Lower CAD and stable reserves help keep India's sovereign ratings in check. With foreign debt inflows still positive (albeit slower), Indian debt could remain appealing to foreign investors.

If you invest in debt mutual funds or G-Secs, these flows matter.

FPI sentiment remains key

Despite the surplus, FPIs were net sellers in equities in Q4. That trend has reversed somewhat post-election in Q1 FY26, but investors should remain cautious about global signals, especially U.S. Fed actions and commodity price movements.

Watch sector-wise FPI flows, especially in financials, tech, and FMCG.

Bottom line

India’s return to a current account surplus is a sign of resilience, especially in a world facing multiple headwinds. While the headline figure brings cheer, the decline in FDI and FPI flows reminds us that external sentiment can shift quickly.

For now, investors should stay diversified, watch the global cues, and focus on long-term allocation strategies rather than reacting to short-term macro data.

At Tradejini, we believe that keeping track of these macro trends enables our retail investors to make smarter, more grounded decisions.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.