Thyrocare Technologies Limited is one of India’s first IT-enabled, fully automated diagnostic lab chains, focused on preventive healthcare. Founded in 2000 and headquartered in Navi Mumbai, the company has played a major role in making diagnostics affordable and accessible across the country. Thyrocare Technologies business model combines automation, centralized processing, and technology integration to deliver large-scale efficiency.

It began with just thyroid testing in 1996 and has now expanded to offer more than 920 tests — covering thyroid health, diabetes, cardiac risk, cancer markers, infectious diseases, and full preventive health check-ups. All its labs are fully automated and run on strong IT systems, ensuring high accuracy and quick reporting.

Thyrocare operates on a centralized hub-and-spoke model, which allows it to process large volumes efficiently. On average, it takes just 3.43 hours from receiving a sample to releasing the report — a key advantage in the diagnostics space. Its ability to maintain low costs with high speed and accuracy has made it a trusted diagnostics brand across India.

In FY 2024-25, the company achieved full Thyrocare NABL accreditation across all 29 owned labs — a landmark feat considering only about 2% of labs in India have this certification.

Thyrocare Business Model and Revenue Verticals

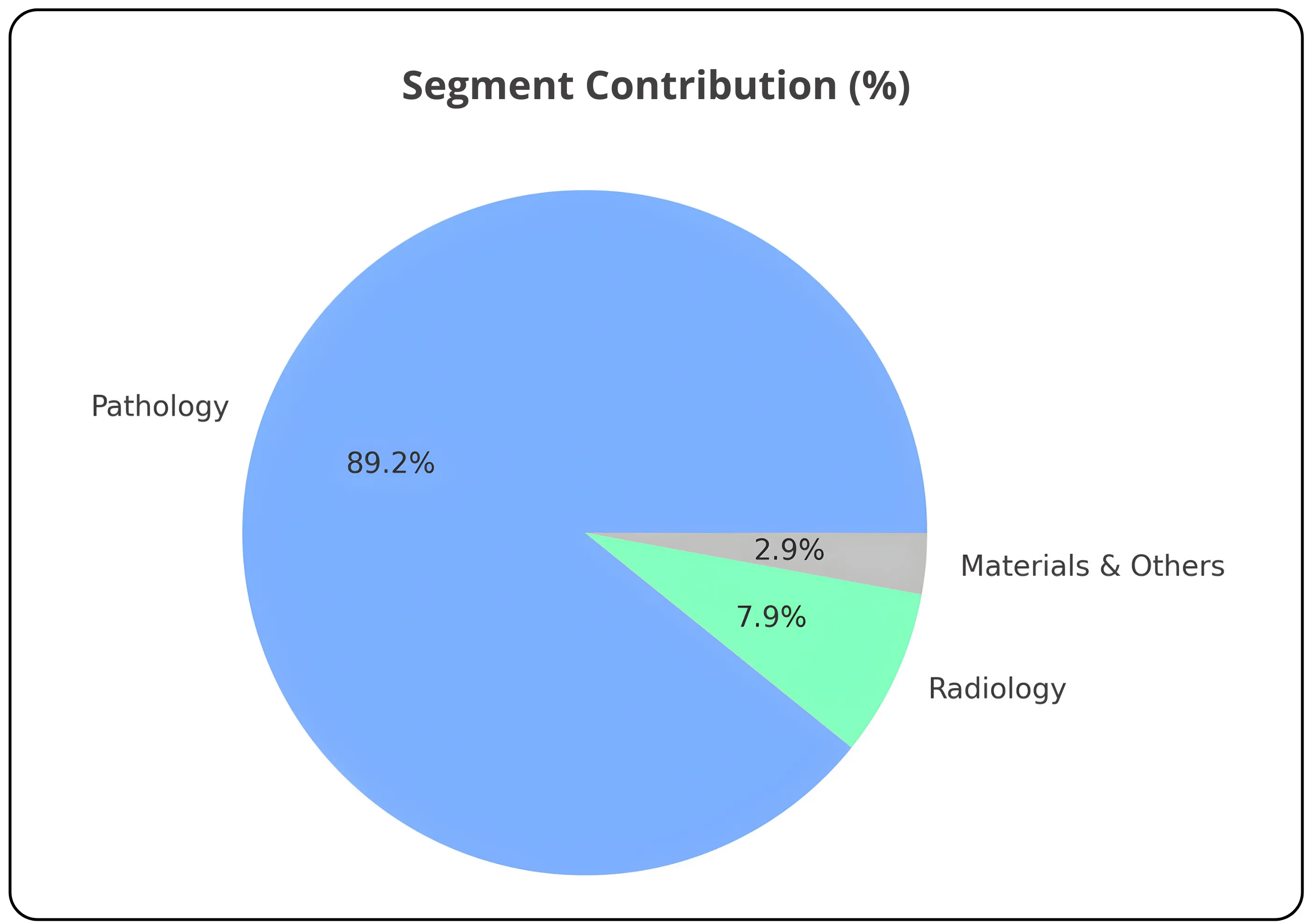

| Segment | Revenue (₹ Cr) | % of Total | YoY Growth |

|---|---|---|---|

| Pathology (study of diseases ) | 613.22 | 89.22% | 20.71% |

| Radiology (X-rays, CT scans, MRIs to diagnose) | 54.29 | 7.90% | 14.03% |

| Materials & Others | 19.84 | 2.89% | 22.02% |

| Total | 687.35 | 100% | 20.19% |

Thyrocare Technologies business model is primarily B2B-driven, with revenue coming from three verticals — pathology, radiology, and materials/others. In FY 2024-25, pathology contributed ₹613 crore, accounting for 89% of total revenue and growing 20.7% year-on-year. Radiology brought in ₹54 crore (8% of revenue), while materials and other income contributed ₹19.8 crore. Overall revenue stood at ₹687 crore, growing 20.2% YoY.

Franchise Network (around 62% of pathology revenue)

Thyrocare franchise network scale is the company’s core growth engine, supported by over 10,100 active partners as of Q2 FY26. This includes around 1,000 branded Thyrocare collection centers that alone contribute 40% of revenue, along with unbranded partners such as hospitals, nursing homes, and standalone labs. Two years ago, the company introduced a slab-based pay-for-performance pricing model. This incentivizes franchisees to scale volumes by offering better pricing in higher business slabs — helping rejuvenate the network and retain loyalty.

Partnerships Business (around 32% of pathology revenue)

This is one of Thyrocare’s fastest-growing verticals, expanding at 35% YoY in Q2 FY26. It includes partnerships with HealthTech platforms like PharmEasy and other diagnostic aggregators, corporate wellness clients for employee health programs, insurance companies for pre-policy medical screenings (supported by a dedicated phlebotomy fleet of 1,900 personnel), and government-led TB testing projects in Gujarat and Maharashtra. These projects currently contribute around 1% of total revenue. Unlike peers, Thyrocare manages its own phlebotomist network rather than depending only on franchisees.

Direct-to-Consumer (D2C) Business

Through its app and website, the company allows customers to directly book tests. While this contributes only around 6% of pathology revenue today, it serves the strategic purpose of maintaining market-level price transparency and brand visibility.

Radiology Services

Under its subsidiary Nueclear Healthcare, Thyrocare provides advanced diagnostic imaging services including PET-CT, MRI, CT, and ultrasound. In FY 2024-25, it completed over 28,500 PET-CT scans and also manufactures its own FDG radiopharmaceutical used for these scans — a competitive advantage in cost and availability.

Product Portfolio

The Aarogyam preventive health check-up packages contribute 36% of pathology revenue and recorded 16% YoY growth. Jaanch, a set of doctor-curated test packages focused on lifestyle disorders, grew 31% YoY. Her-Check caters to women’s reproductive health needs.

Geographic Reach

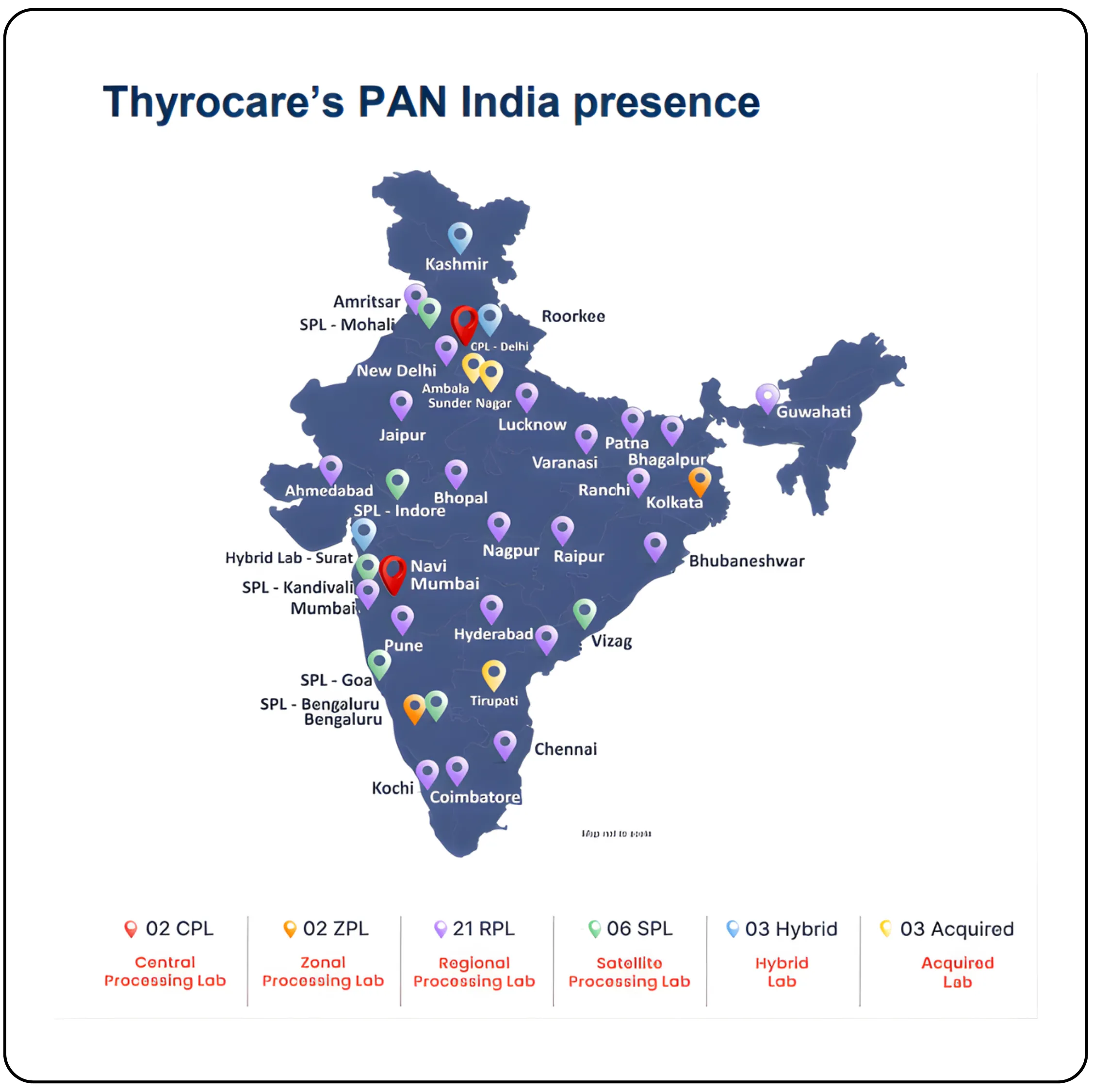

Thyrocare operates 37 laboratories across India and one lab in Tanzania. Its lab network includes 2 central processing labs (Navi Mumbai and Delhi), 2 zonal labs, 21 regional labs, 6 satellite labs, 3 hybrid labs, and 3 acquired labs from Polo and Vimta. Its services are currently accessible across more than 4,600 pin codes in India.

Thyrocare Financial Performance FY25 FY26 and Trend Analysis

Five-Year Financial Trajectory

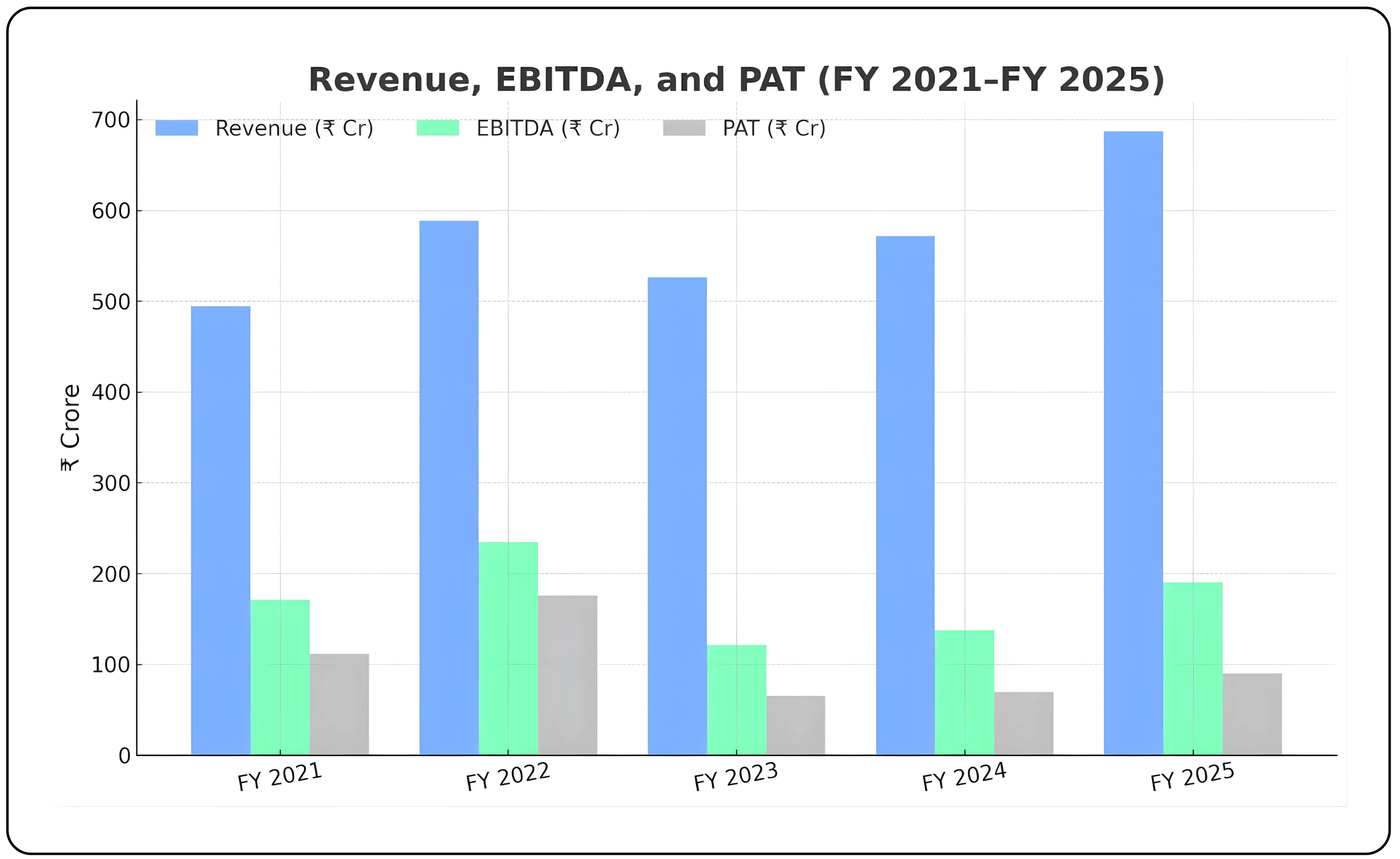

| Metric | FY 2021 | FY 2022 | FY 2023 | FY 2024 | FY 2025 |

|---|---|---|---|---|---|

| Revenue (₹ Cr) | 494.62 | 588.86 | 526.67 | 571.88 | 687.35 |

| EBITDA (₹ Cr) | 171.19 | 234.71 | 121.23 | 137.81 | 190.36 |

| PAT (₹ Cr) | 111.76 | 176.06 | 65.89 | 69.78 | 89.98 |

| EBITDA Margin (%) | 34.61% | 39.86% | 23.02% | 24.10% | 27.69% |

| PAT Margin (%) | 22.60% | 29.90% | 12.51% | 12.20% | 13.09% |

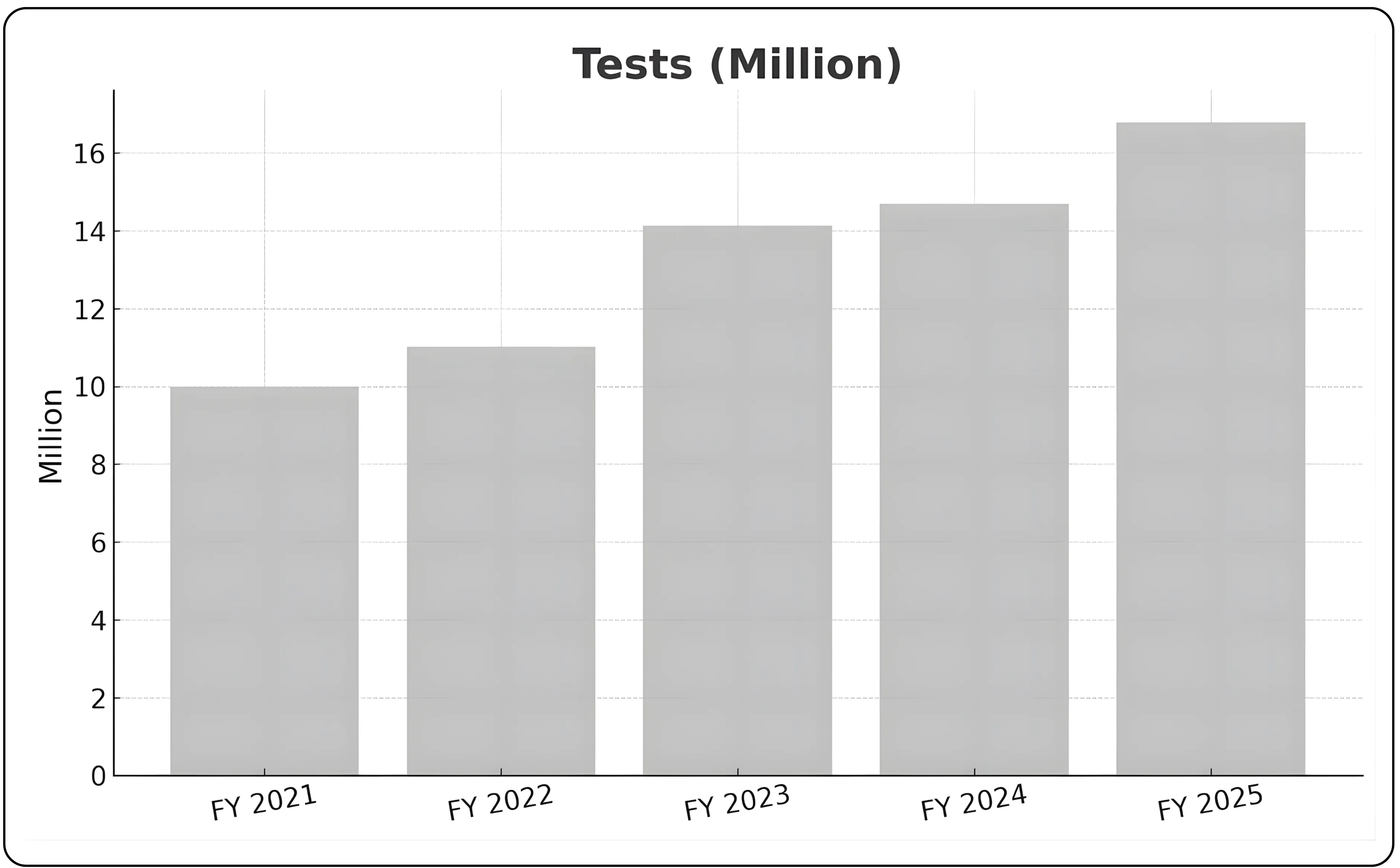

| Tests (Million) | 9.99 | 11.03 | 14.14 | 14.70 | 16.79 |

Key Observations:

Thyrocare’s financial performance reflects a full COVID-cycle normalization followed by a healthy structural recovery. Revenue grew from ₹495 crore in FY21 to ₹687 crore in FY25 (8.6% CAGR), but growth momentum has been much stronger in the non-COVID core portfolio, which has compounded at 19% annually over the last four years. FY22 marked a one-off peak due to COVID testing tailwinds, followed by a sharp reset in FY23. From FY24 onward, the business has been on a clear recovery path, culminating in its highest-ever annual revenue in FY25.

Margins have normalized from COVID-era highs but have steadily improved over the past two years — with EBITDA margin recovering from 23% in FY23 to 28% in FY25, and PAT margin stabilizing around 13%. Test volumes have grown faster than revenue (from 10 million in FY21 to 17 million in FY25), indicating strong operating leverage and network utilization efficiencies.

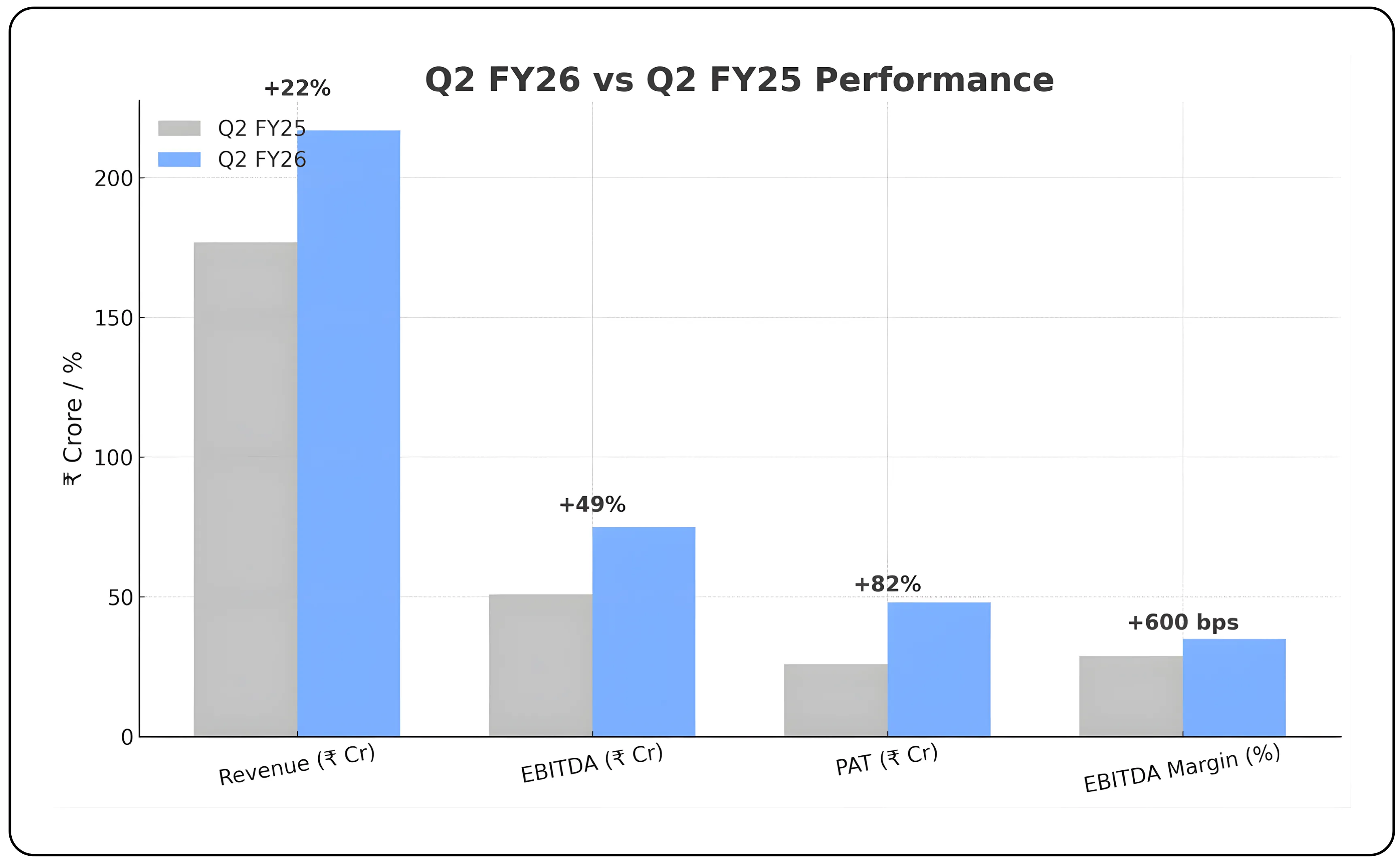

Q2 FY26 Quarterly Results Analysis

The Q2 FY26 results (July-September 2025) represent outstanding operational and financial performance:

| Metric | Q2 FY26 | Q2 FY25 | YoY Growth |

|---|---|---|---|

| Consolidated Revenue | ₹217 Cr | ₹177 Cr | +22% |

| EBITDA | ₹75 Cr | ₹51 Cr | +49% |

| EBITDA Margin | 35% | 29% | +600 bps |

| PAT | ₹48 Cr | ₹26 Cr | +82% |

Thyrocare financial performance FY25 FY26 highlights a strong rebound in both topline and margins, reflecting the success of its franchise and partnership model.

Operational Metrics

- Tests Conducted: 53.3 million (+21% YoY)

- Patients Served: 5.0 million (+12% YoY)

- Tests per Patient: 10.7 (up from 9.9), driven by comprehensive health packages

- Active Franchisees: 10,100 (+20% YoY from 8,446)

- Revenue per Patient: ₹406 (up from ₹368 YoY)

Segment Performance

- Pathology Revenue Growth: +24% YoY

- Franchise Business: +20% YoY

- Partnership Business: +35% YoY (API PharmEasy +46% YoY)

- Radiology (Active Centers): +3% YoY (improved profitability focus)

Quality Metrics

- Complaints per Million Tests: 3.8 (down 67% YoY from 11.8), approaching Six Sigma standards (target: <3.4 per million)

- NABL-processed samples: 96%

Cash Flow Strength

- Operating Cash Flow (H1 FY26): ₹127 crores (+43% YoY)

- Net Cash & Equivalents: ₹190+ crores (debt-free balance sheet)

With Thyrocare strengthening its position in diagnostics through scale and efficiency, it’s worth looking at other niche players transforming healthcare delivery in their own segments.

Also read: Could Laxmi Dental Be the Hidden Gem in Healthcare?

Company-Specific Growth Drivers

Franchise Network Expansion

Thyrocare’s revamped franchise strategy is delivering strong results. Its on-ground field force now consists of 100 members — 40 in-field and 60 at the call center. The company has been consistently adding 100 to 150 net new franchise partners every month over the last 12–18 months. A major focus remains on high-volume “diamond to silver” category franchisees, who are driving most of the incremental business. Expansion is particularly strong across Tier 2 and Tier 3+ cities, where growth is outpacing metro markets. Thyrocare’s revamped franchise strategy and expanding franchise network scale have been central to its 20%+ volume growth.

Acceleration in Partnerships Business

Partnership-led revenue — especially from HealthTech aggregators — is growing at over 35% yearly as digital diagnostic platforms scale rapidly. The insurance segment is a large opportunity, supported by SyncHealth’s ECG-at-home capabilities for pre-policy medical exams and annual checkups. Corporate wellness programs are also seeing rising demand. A key differentiator for Thyrocare is its proprietary phlebotomy fleet.

A phlebotomy fleet refers to a group of trained phlebotomists or mobile units equipped to collect blood samples from multiple locations, such as homes, clinics, or health camps. which ensures service consistency across markets.

Test Menu Expansion and Technology Upgrades

The company has been actively expanding its test portfolio to improve its competitive strength. It has added histopathology capabilities at its Gurgaon and Navi Mumbai labs and introduced the BioFire PCR platform for rapid infectious disease detection. Coagulation tests including PT INR and APTT are now available across all regional labs. Thyrocare has also deployed advanced HPLC systems for high-throughput testing and has migrated from manual ELISA to fully automated platforms to improve accuracy and efficiency.

Strategic Acquisitions

In July 2024, Thyrocare acquired Polo Labs for ₹4.26 crore, strengthening its network in Punjab, Haryana, and Himachal Pradesh. The integration is complete and already contributing to regional scale benefits. In October 2024, it acquired Vimta Clinical Diagnostics for ₹7 crore to deepen its presence in Telangana and Andhra Pradesh. This integration is expected to conclude by Q1 FY26. Both deals follow a disciplined acquisition strategy, capped between ₹12-20 crore and aligned to deliver returns on invested capital within 12 months.

International Expansion – Tanzania

Thyrocare marked its international entry with operations in Tanzania, where it processed its first sample in April 2024. It has already partnered with over 150 healthcare facilities in Dar es Salaam. Revenue is growing at 30% quarter-on-quarter, with the business targeting breakeven within 18–24 months. While current contribution is minimal, the long-term potential is significant.

Preventive Healthcare Brands

Aarogyam continues to lead with 36% contribution to pathology sales, growing at 16% YoY. The introduction of the new Plus and Pro series, along with 24x7 non-fasting package variants, is driving higher adoption. The Jaanch brand is growing even faster at 31% YoY and is emerging as a key platform for lifestyle-oriented diagnostics.

GLP-1 Weight Loss Opportunity

Management has identified the GLP-1 weight loss therapy market — led by drugs like Ozempic and Wegovy — as a major growth opportunity. These drugs require continuous diagnostic monitoring, and Thyrocare is developing specialized test packages for pre-therapy, active therapy, and post-therapy stages to capture this demand.

Logistics and Cold Chain Investments

Thyrocare has fully integrated smart cold chain logistics by equipping every sample transport box with data loggers for live temperature monitoring. It is the first diagnostic chain in India to implement this nationwide. This has reduced sample cancellations, improved accuracy, and significantly enhanced service reliability. The company has also brought down its average pan-India sample turnaround time from over 40 hours to under 18 hours.

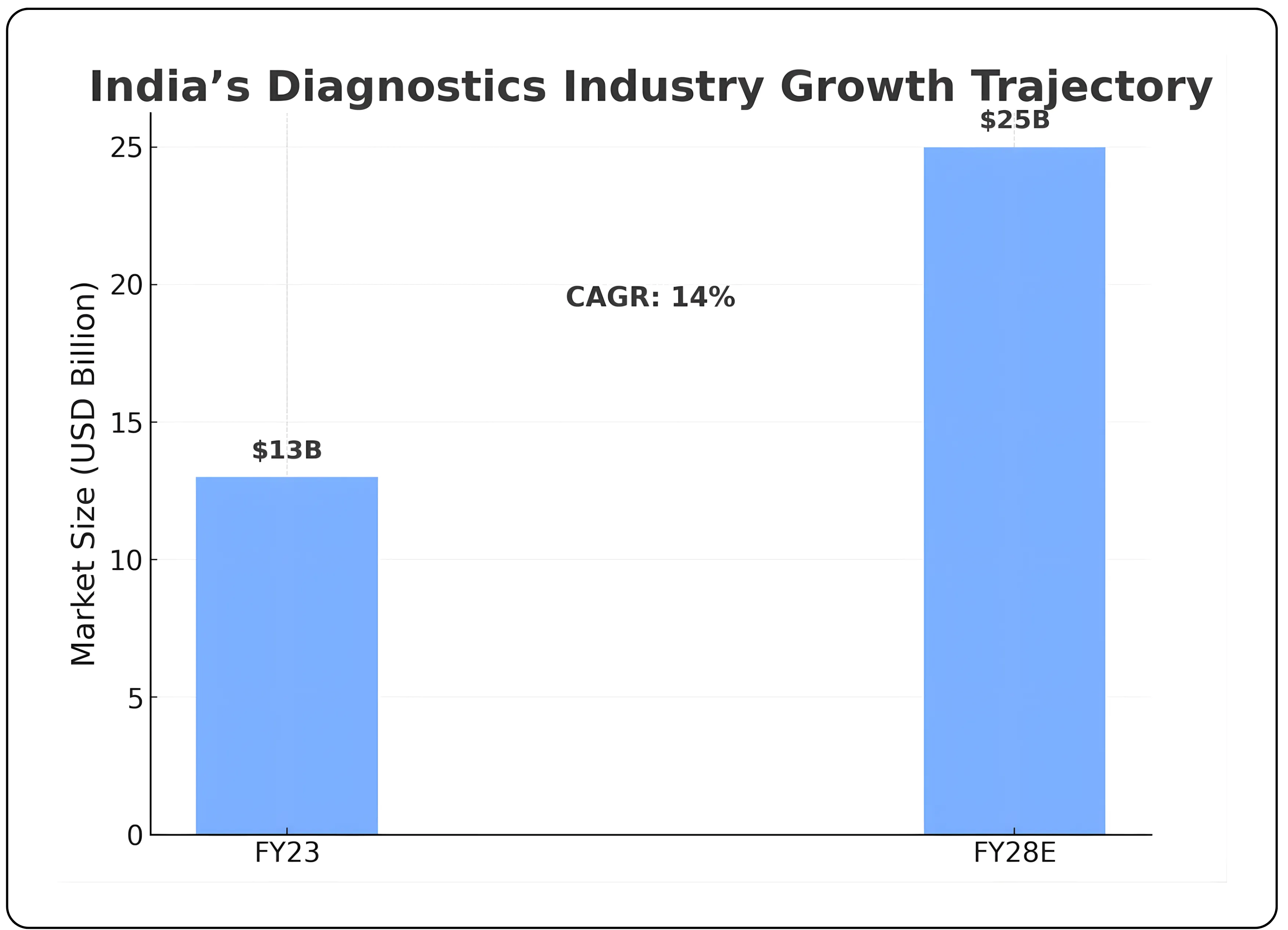

Diagnostics Industry Outlook India and Macro Tailwinds

The Diagnostics industry outlook India remains strong, with the market projected to grow from USD 13 billion in FY23 to USD 25 billion by FY28, reflecting a CAGR of 14%.

Market Size and Growth Potential

India’s diagnostics industry is on a strong growth trajectory, expanding from a USD 13 billion market in FY23 to an expected USD 25 billion by FY28 — a CAGR of 14%.

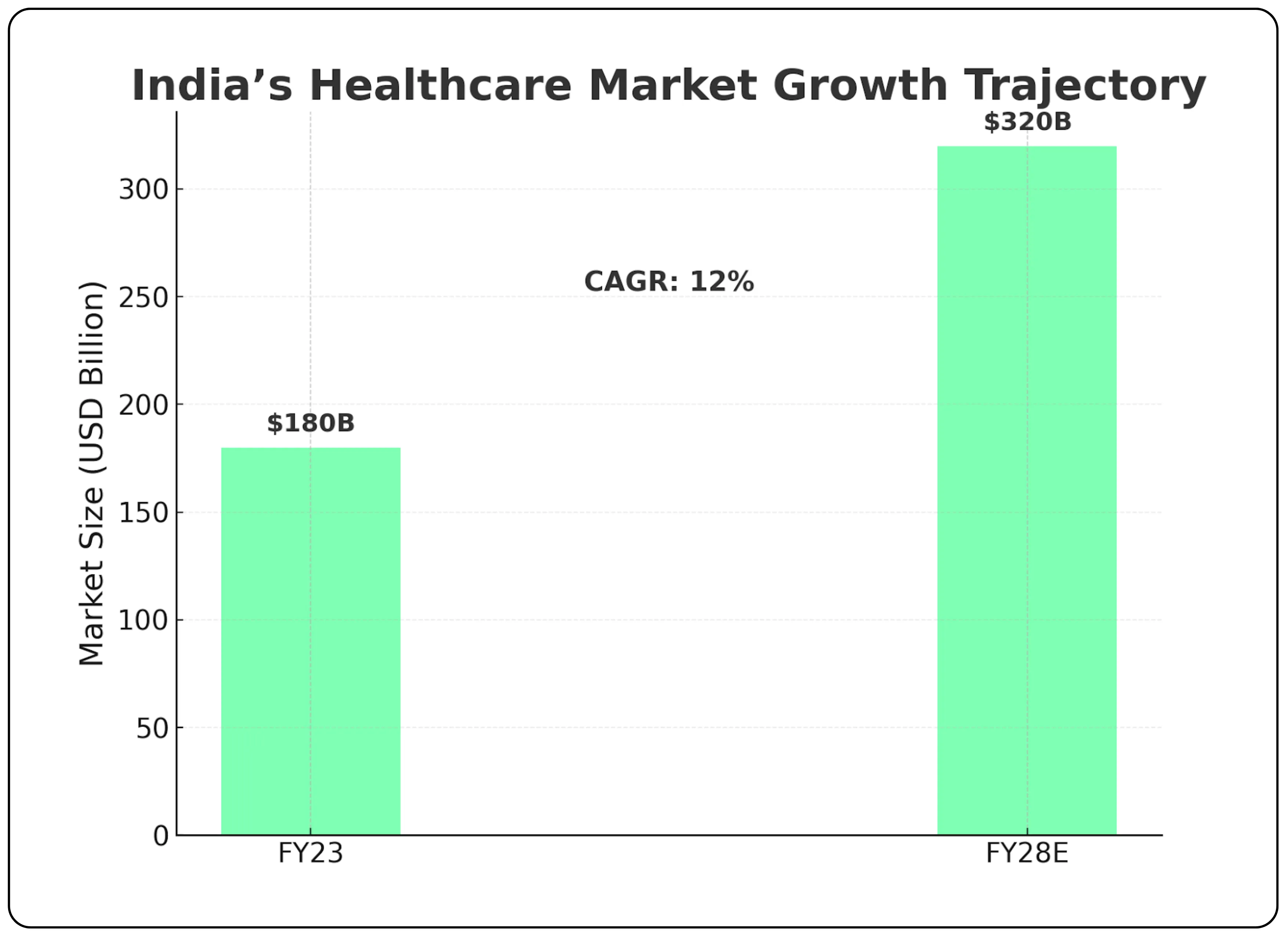

The broader Indian healthcare market is also projected to grow from USD 180 billion to USD 320 billion over the same period, at a CAGR of around 12%, indicating strong support for long-term structural growth.

Demographic and Health Trends

India’s ageing population is a major demand catalyst — the share of people aged 60 and above is projected to rise from 8.4% in 2011 to nearly 15% by 2036. The burden of chronic diseases is accelerating rapidly. In Thyrocare’s own HbA1c study covering 20 lakh samples, almost 50% of individuals tested showed abnormal blood glucose levels. Rising cases of diabetes, hypertension, and cardiovascular disorders are leading to a shift from reactive to preventive healthcare, with consumers increasingly opting for periodic wellness checkups and proactive screenings.

Government Support

Government initiatives are actively strengthening the diagnostic ecosystem. The PMJAY scheme is expanding insurance coverage, widening access to diagnostic services. The Ayushman Bharat Digital Mission is enabling deeper digitization through national health registries, electronic health records, and the United Health Interface (UHI), improving accessibility. Public healthcare spending has risen at a 15.8% CAGR to reach 1.9% of GDP in FY24, further supporting infrastructure expansion.

Tier 2 and Tier 3 Market Penetration

Demand growth is accelerating beyond metro cities as urban migration pushes population density into Tier 2, Tier 3, and Tier 4 regions. While online diagnostic platforms are still underpenetrated in these regions, Thyrocare’s franchise-led offline model is seeing its strongest growth here. Meanwhile, partnerships continue to drive growth in metro markets, creating a well-balanced channel mix.

Technology Adoption

AI and machine learning are increasingly being used to improve diagnostic accuracy and efficiency. Wearable and real-time health monitoring devices are gaining acceptance. Automation and data-driven systems are helping reduce costs and streamline operations.

Insurance-Led Demand

Health insurance penetration is rising steadily, leading to higher volumes of pre-policy and annual health checkups. Corporate wellness programs are becoming a key recurring revenue driver, especially from large enterprises and IT/financial firms. Preventive screenings are evolving from one-time purchase behavior to subscription-like recurrence.

As India’s healthcare ecosystem expands beyond diagnostics into pharma manufacturing, CDMOs are emerging as key growth drivers.

Also read: Senores Pharma Capitalizing on CDMO Tailwinds for Global Ascent.

Thyrocare Competitive Advantages and Moat

Despite operational and industry challenges, Thyrocare competitive advantages remain anchored in scale, automation, and compliance leadership.

Dual Channel Model

The company benefits from both offline and online demand. Franchise-led growth is strongest in Tier 2+ regions, while digital partnerships drive metro consumption. Unlike peers, Thyrocare operates its own phlebotomy fleet — ensuring superior service consistency in partnership channels.

Asset-Light Expansion

Its franchise-based expansion strategy allows rapid geographical scale with minimal capital deployment, while centralized processing keeps testing costs low. The hub-and-spoke logistics model further optimizes cost per sample.

Data and Research-Driven Edge

With one of the largest diagnostic databases in the country, Thyrocare regularly publishes research studies (e.g. 20 lakh sample HbA1c report), reinforcing its thought leadership while using data intelligence to drive strategic lab expansion — such as its Bhagalpur lab informed by demand visibility from its Patna facility.

Financial Strength

The company remains debt-free with over ₹190 crore in net cash and generated ₹127 crore in operating cash flow during H1 FY26 — giving it strong flexibility for strategic acquisitions and organic growth investments.

Structural Advantages

- Scale-led cost advantage — largest fully NABL-accredited chain with centralized testing enables industry-low cost per test

- Network effect moat — 10,100+ franchisees create self-reinforcing growth with low incremental cost of expansion

- High entry barriers in quality — 100% NABL + CAP accreditation vs. industry’s ~2% average makes replication extremely difficult

- Technology-first infrastructure — 24/7 automated labs, data-logged cold chain, <4 hr TAT at national scale remains unmatched

- High doctor trust — 25+ year track record with 9/10 doctor endorsement entrenches credibility

Operational Advantages

- Hub-and-spoke logistics efficiency — centralized processing improves utilization and preserves margins

- Dual-channel model — franchise-led Tier 2/3 expansion with parallel HealthTech/platform-led growth in metros

- Company-owned phlebotomy fleet — operational control edge over aggregator-driven competitors

- Asset-light scaling — franchise model enabling capital-efficient expansion versus peers’ owned center strategy

Strategic Advantages

- Embedded HealthTech access via API Holdings (PharmEasy) without losing independence

- Data-driven insights — large sample pool enabling disease trend analysis and product innovation

- Early automation adoption — deep tech muscle memory and switching cost advantage

- Financial strength — debt-free, ₹190+ crore net cash buffer for acquisitions and strategic expansion

Embedded HealthTech access via API Holdings PharmEasy Thyrocare acquisition provides strategic synergies in digital diagnostics while maintaining brand independence.

Future Outlook and Strategic Roadmap

Network & Menu Expansion Expansion

The company is expanding its franchise network across Tier 2–4 cities, focusing on high-throughput partners, insurance-led diagnostics, and SyncHealth ECG-at-home services. Internationally, it aims to consolidate operations in Tanzania before scaling further in Africa.

Thyrocare is adding high-value tests in histopathology, molecular diagnostics, and genetics, along with new packages for GLP-1 therapy and lifestyle disease monitoring.

Near-Term Strategic Initiatives

| Focus Area | Key Highlights |

|---|---|

| Franchise Acceleration | Adding 100–150 net franchise partners per month, prioritizing high-volume partners and deeper penetration in non-metro markets. |

| Partnership Business Scaling | Scaling ECG-at-home services via SyncHealth nationally; expanding insurance-led pre-policy testing, annual health checkups, and integrations with HealthTech platforms and corporate wellness programs. |

| Path to Radiology Profitability | Nueclear Healthcare shifting from volume-led to profitability-led growth; focus on optimizing center-level economics before expansion. |

| Acquisition Integration | Vimta integration to conclude by Q1 FY26; Polo Labs fully integrated. Pursuing ROIC-driven M&A, capped at ₹12–20 crore per deal. |

| International Expansion – Tanzania | Targeting to double revenues in FY26 and achieve operating breakeven in 18–24 months; foundation for broader African expansion. |

| Technology and Digital Investments | Investing in automation, digital patient platforms (microsites, live tracking, cross-sell), and enhancing partner experience via Privilege Club and ThyroNXT. |

| Quality Excellence | Aiming for Six Sigma efficiency (<3.4 complaints per million tests), 100% NABL accreditation, and compliance with CAP and EQAS standards. |

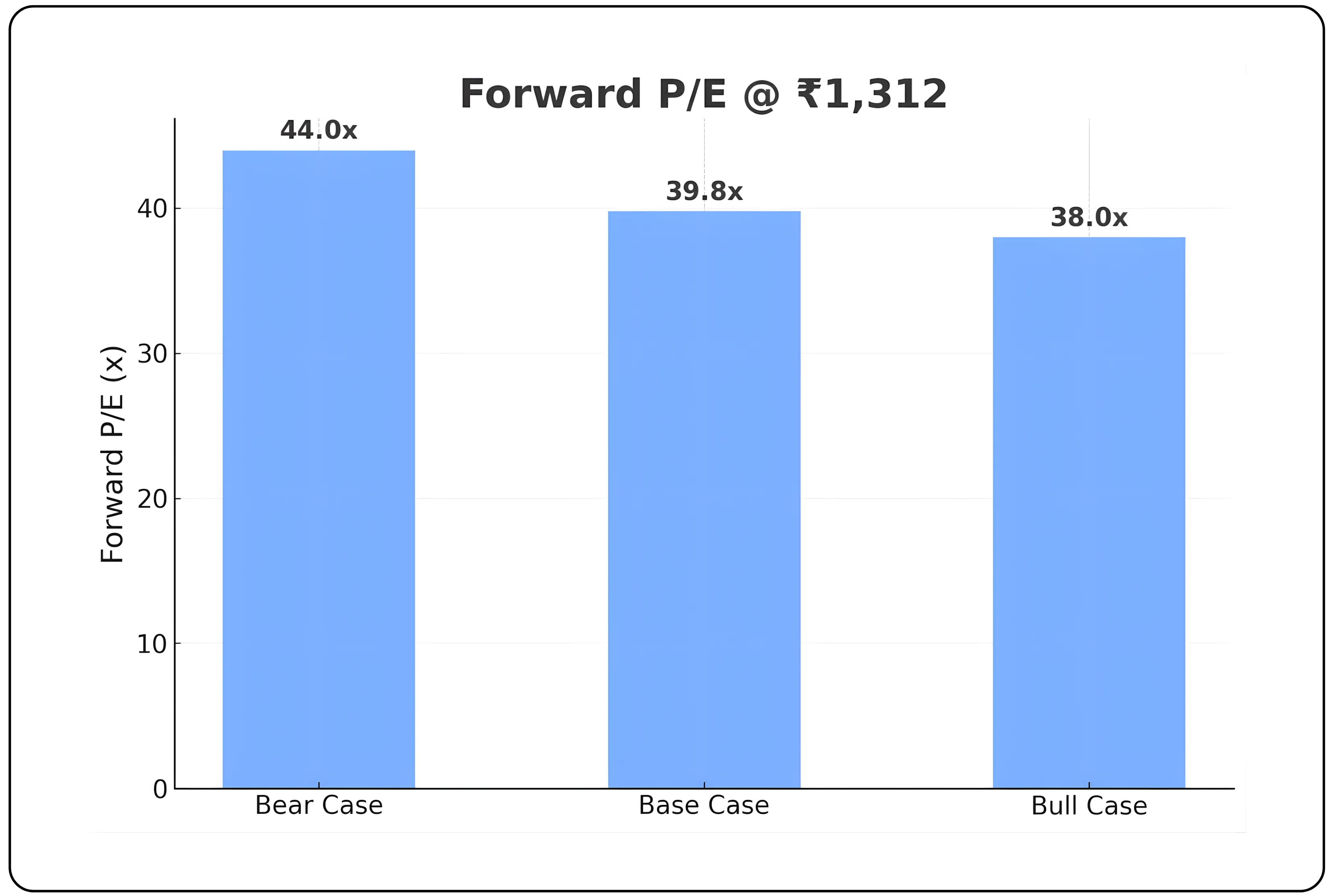

Valuation Analysis

Forward P/E Valuation Scenarios

| Scenario | FY26E PAT (₹ Cr) | FY26E EPS (₹) | Forward P/E @ ₹1,312 | Premium vs Industry (36x) | Growth over FY25 |

|---|---|---|---|---|---|

| Bear Case | 158 | 29.81 | 44.0x | +22% | 76% |

| Base Case | 175 | 32.98 | 39.8x | +11% | 94% |

| Bull Case | 183 | 34.52 | 38.0x | +6% | 103% |

Bear Case (44.0x Forward P/E)

PAT estimated at ₹158 Cr ( +76% YoY growth over FY25 ). This assumes H2 underperforms — deeper Q3 seasonal weakness, softer Q4 recovery, and mild margin compression. Despite this being the risk case, Thyrocare still trades at a 22% premium to industry P/E (36x) — supported by its compliance moat, debt-free balance sheet, and negative working capital model.

Base Case — Most Aligned with Management (39.8x Forward P/E)

PAT estimated at ₹175 Cr (+94% YoY growth). This reflects management’s guidance — Q3 dip but compensated fully by Q4 momentum, with margins holding steady. A 11% premium to industry P/E is reasonable given Thyrocare’s execution visibility, bonus + dividend confidence signals, and capital-efficient growth model. This is the “fair value zone”.

Bull Case (38.0x Forward P/E)

PAT rises to ₹183 Cr (+103% YoY). This assumes stronger-than-expected execution — accelerated partner channel scaling, early GLP-1 adoption, and faster Tanzania ramp-up. Forward valuation compresses to just +6% above industry P/E despite superior growth — making this scenario genuinely attractive if execution beats expectations.

Valuation Interpretation

Current trailing P/E of 54.5x normalizes to 38–44x forward as earnings double in FY26. Even under a conservative lens, Thyrocare continues to justify a premium given:

• 100% NABL/CAP compliance leadership

• Asset-light franchise-led scalability

• Strong cash generation with zero debt

• Multiple simultaneous growth levers (partnerships, GLP-1, Africa, expansion)

Base Case = Fairly Valued

Bull Case = Attractive Risk-Reward

Bear Case = Downside protected by quality & balance sheet

India’s CDMO sector is rapidly evolving into a global growth story, driven by strong demand and innovation in pharma outsourcing. Also read: India’s CDMO Boom A Rising Global Powerhouse.

Risks & Challenges

1. Operational Execution Risks

Thyrocare’s hub-and-spoke model relies heavily on cold-chain logistics and uninterrupted transportation. Any disruption in sample movement, fuel price spikes, or cold-chain failure can impact service delivery and turnaround times. With 10,100+ franchise partners, consistent execution quality across regions remains a challenge — particularly in Tier 2/3 cities where infrastructure is less reliable.

Laboratory operations are centralized, creating single-point dependency at high-volume processing centers. Equipment downtime, reagent supply issues, or staffing gaps could directly impact testing volumes. As scale rises, maintaining operational discipline and partner engagement becomes critical.

2. Business & Industry Risks

The diagnostics sector remains highly fragmented with low entry barriers, leading to price-based competition from both regional labs and large chains like Dr. Lal PathLabs and Metropolis.

Seasonality is intrinsic to the business — Q2 typically strong, Q3 softer due to lower fever-related testing volumes. A shift in patient preference toward at-home collections and digital-first platforms could disrupt walk-in franchise economics if Thyrocare is not consistently ahead in convenience.

Additionally, revenue concentration risk exists with API Holdings (PharmEasy), which is both majority shareholder and major B2B partner. Increasing share of partnership-led volumes raises dependence on external platforms.

3. Regulatory & Compliance Risks

Thyrocare’s competitive edge rests on its 100% NABL accreditation, which requires continuous audit compliance across all laboratories. Newly acquired entities (e.g., Vimta) still need full integration into this standard.

Regulatory intervention remains a structural risk — including pricing caps via CGHS/government schemes and potential GST revisions.

With growing digitalization under ABDM, data privacy, cybersecurity, and EHR compliance will increasingly come under scrutiny, exposing the company to legal and reputational risks in case of breach.

4. Financial & Strategic Risks

Working capital management is critical, with rising receivables from franchise and partnership clients. Acquisition-led expansion (Vimta, Polo) carries integration and goodwill impairment risk if synergy realization is delayed.

The radiology subsidiary (Nueclear Healthcare), though improving, has historically been margin dilutive. International expansion into Tanzania adds FX exposure and execution complexity, with breakeven still 18–24 months away.

Macro risks such as healthcare consumption slowdown, wage inflation in skilled manpower, or pandemic-like disruptions can affect testing volumes and capex planning.

Revenue concentration with API Holdings PharmEasy Thyrocare acquisition remains a structural dependency, as the partnership drives a major portion of platform-led volumes.

Final Thoughts

Thyrocare is transitioning from a COVID-era beneficiary to a structurally resilient, multi-growth-lever diagnostics leader, demonstrated by its strong Q2 FY26 performance (22% revenue growth, 82% PAT growth, 35% EBITDA margin). The company’s franchise-led scale, multi-channel strategy, automation-led cost advantage, and debt-free balance sheet support its positioning as a quality-focused player in India’s evolving preventive and wellness-oriented healthcare market. Near-term execution will hinge on sustaining 20%+ growth, maintaining 33–35% EBITDA margins, timely breakeven in Tanzania, successful GLP-1 package rollout, and smooth post-acquisition integration of Vimta and Polo Labs. At the current valuation range of 55x P/E, the stock reflects premium pricing aligned to quality, scalability, and capital efficiency rather than deep value. Key risks to monitor include margin compression below 30%, franchise slowdown, rising partnership dependency, or any disruption to quality credentials.

Turn research into action and explore smarter investing opportunities with CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.