What if we told you that a metal once cursed by medieval miners now holds the key to a $7 trillion energy revolution? While everyone obsesses over gold and silver, nickel is trading at $15,300 per tonne, quietly sitting at the epicentre of the biggest industrial transformation. This metal comes from deep inside the Earth and is now turning up in the batteries of electric cars.

Nickel has a surprisingly colourful backstory. Back in medieval Europe, miners kept coming across an ore that looked like copper but refused to yield any usable metal. Frustrated, they nicknamed it “kupfernickel” - literally “Devil’s Copper” - believing mischievous spirits were to blame. It wasn’t until 1751 that Swedish chemist Axel Fredrik Cronstedt finally isolated nickel and revealed it to be something entirely new.

So, what makes nickel so special? It is a combination of strength, hardness, and resistance to corrosion. These qualities turned it into a quiet workhorse of the industrial age: an essential ingredient in stainless steel, superalloys for jet engines, coins, plating, and countless everyday products.

Today, nickel’s story is entering a new chapter. Its ability to store and release energy efficiently makes it a key material in the high-performance batteries used in electric vehicles and grid storage. In other words, the metal once cursed by miners has become a cornerstone of modern industry - and a potential driver of the global clean-energy transition.

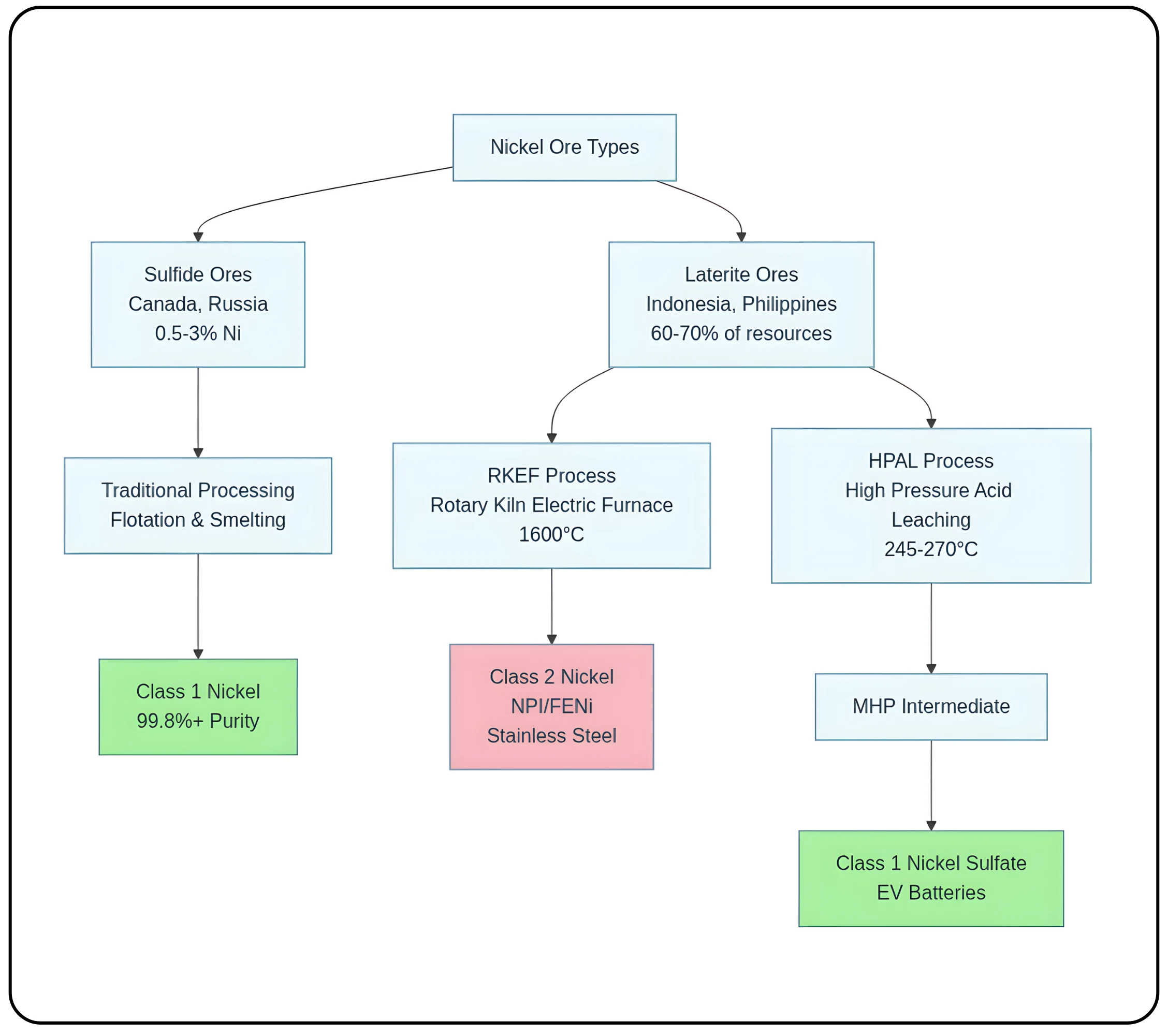

The entire nickel industry is shaped by a fundamental geological bifurcation between two ore types:

PUT BRANCH CHART

Magmatic Sulfide deposits:

These deposits are formed from cooling magma and are primarily found in regions like Canada and Russia. Known for their typically higher grade (0.5%-3% Ni), they have historically been one of the main sources of nickel. They are relatively easy to process via conventional methods such as concentration and smelting.

Lateritic deposits:

Formed through intense weathering of rocks in tropical climates, such as those in Indonesia and the Philippines, these deposits constitute 60-70% of the world’s nickel resources. They are mined via low-cost open-pit methods but are metallurgically complex, requiring the entire ore to be processed through energy-intensive methods.

The depletion of high-grade sulfide deposits has forced a global shift towards the more abundant laterite sources, fundamentally altering the industry’s geography and technology. This pivot from traditional producers to new power centers like Indonesia is a shift of geological necessity, bringing new logistical, geopolitical, and environmental risks.

The global supply landscape

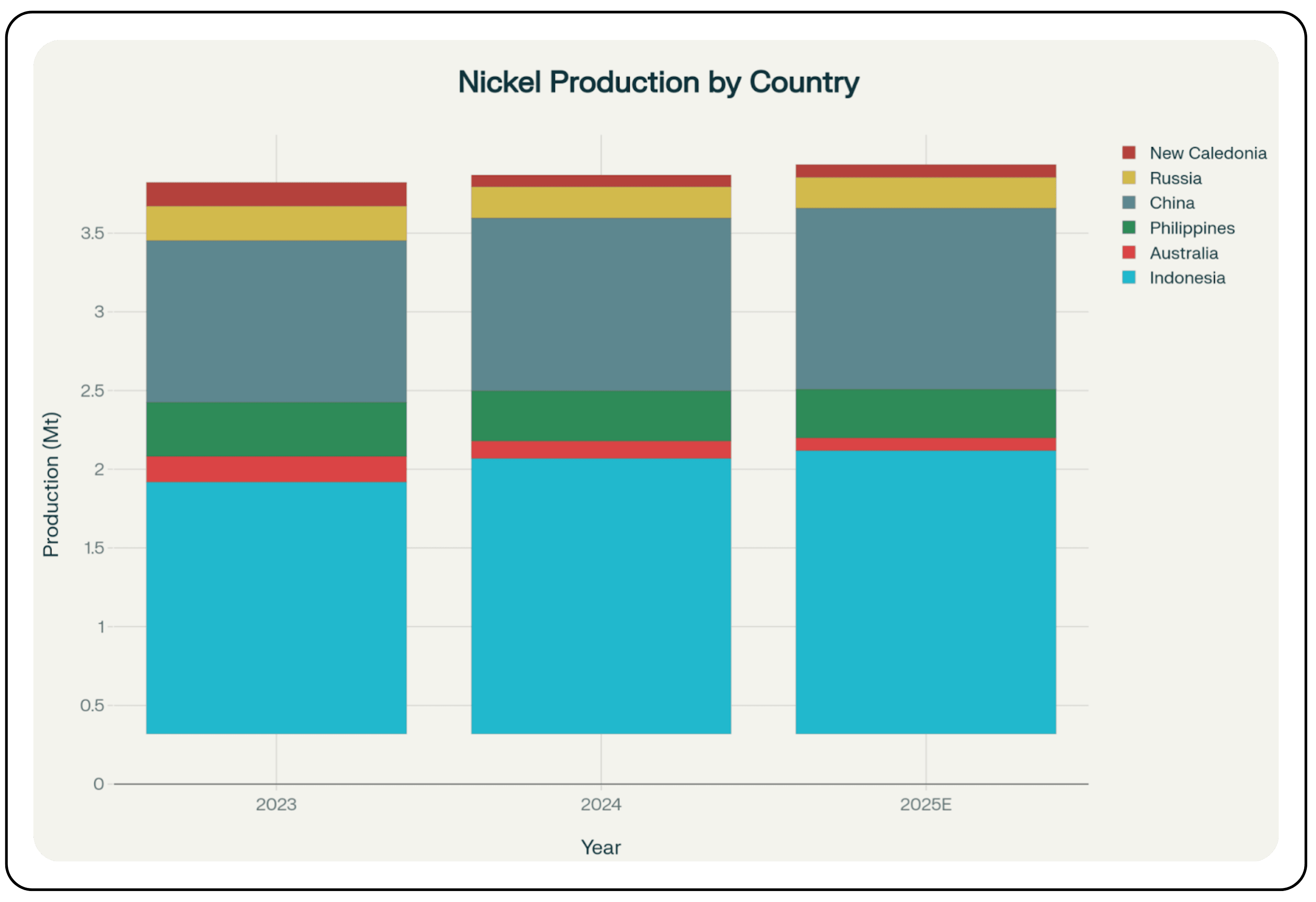

The global nickel supply chain has changed dramatically. What was once a diversified network of producing countries is now increasingly concentrated in a single corridor dominated by China and Indonesia.

Indonesia’s dominance and China’s role:

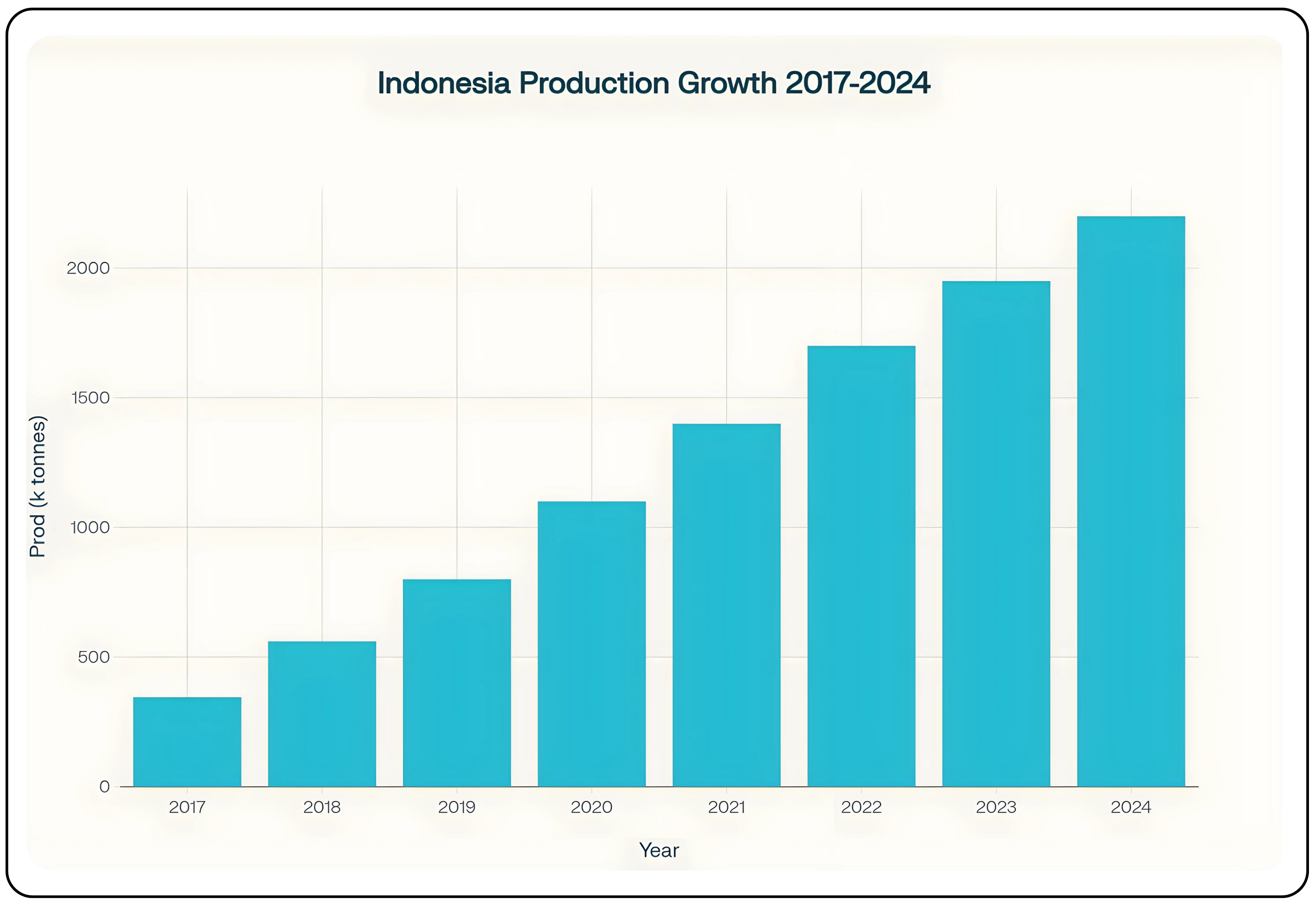

Indonesia has single-handedly reshaped the global nickel market. Its production skyrocketed 538% in seven years, from 345,000 tonnes in 2017 to an estimated 2.2 million tonnes in 2024, giving it control of over 50% of global mine production. This was catalyzed by a 2020 ban on raw ore exports, forcing downstream investment. This transformation was enabled by over $30 billion in Chinese investment, which recognized the need to secure nickel for its stainless steel and electric vehicle (EV) industry.

The emerging China-Indonesian axis now controls an estimated 75% of the world’s finished nickel production, a level of market concentration that surpasses OPEC’s historical share of oil. This dominance has created an existential challenge for higher-cost producers in Australia and New Caledonia, who are struggling to remain competitive. Having established this market control, Indonesia is now signaling a move toward active market management, with plans to cut its 2025 mining quota by 40%. Such a reduction could remove a volume of ore equivalent to over one-third of global demand, introducing significant political and supply risks for dependent consumers.

Global nickel market dynamics

The nickel market is undergoing a structural shift, marked by a growing disconnect between supply and demand. This imbalance stems from a fundamental reshaping of the global supply base.

Price Analysis and Imbalance

Nickel: A tale of two markets

As of the third quarter of 2025, nickel prices on the London Metal Exchange (LME) are languishing near multi-year lows at about $15,200–$15,400 per metric tonne. On paper, the market looks flooded, with a projected surplus of 198,000 tonnes for the year. Indonesian mines alone now supply more than 63 percent of the world’s nickel, and this surge has pushed combined LME and Shanghai Futures Exchange inventories to a multi-year high of 230,600 tonnes by April 2025 - a major factor keeping prices under pressure.

But the headline “glut” hides a crucial detail. Almost all of the oversupply is in Class 2 nickel - lower-purity products such as nickel pig iron (NPI) and ferronickel that feed the stainless-steel industry. The story is very different for Class 1 nickel (99.8% + purity), which is the grade needed for electric-vehicle batteries. Supplies of Class 1 nickel are far tighter, and converting Class 2 into Class 1 is expensive, energy-hungry, and environmentally damaging.

In other words, today’s oversupply does little to relieve the bottleneck for battery-grade nickel. This split market creates a long-term investment angle: while headline prices may stay depressed by the flood of Class 2 material, the constrained Class 1 value chain could hold far greater value as EV and energy-storage demand accelerates.

Demand architecture - stainless steel and batteries

Nickel demand rests on two pillars: its traditional role in stainless steel and its rapidly growing use in EV batteries.

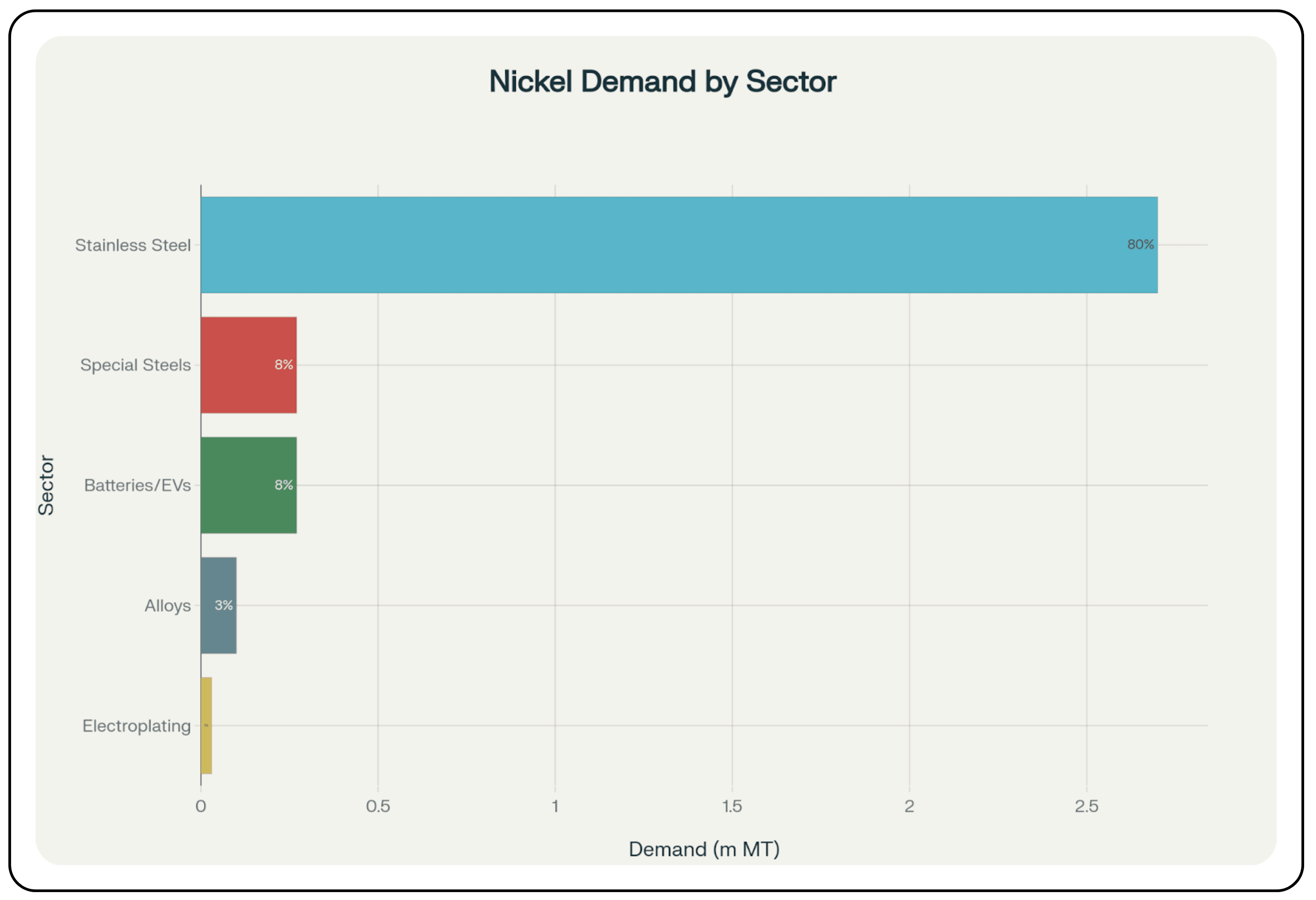

- The stainless steel bedrock: The stainless steel sector remains the primary consumer, accounting for 67-70% of total demand. Nickel imparts essential properties of corrosion resistance and strength in the most common grades of stainless steel. This sector provides a solid, foundational demand base, with production growing at 4-5% annually.

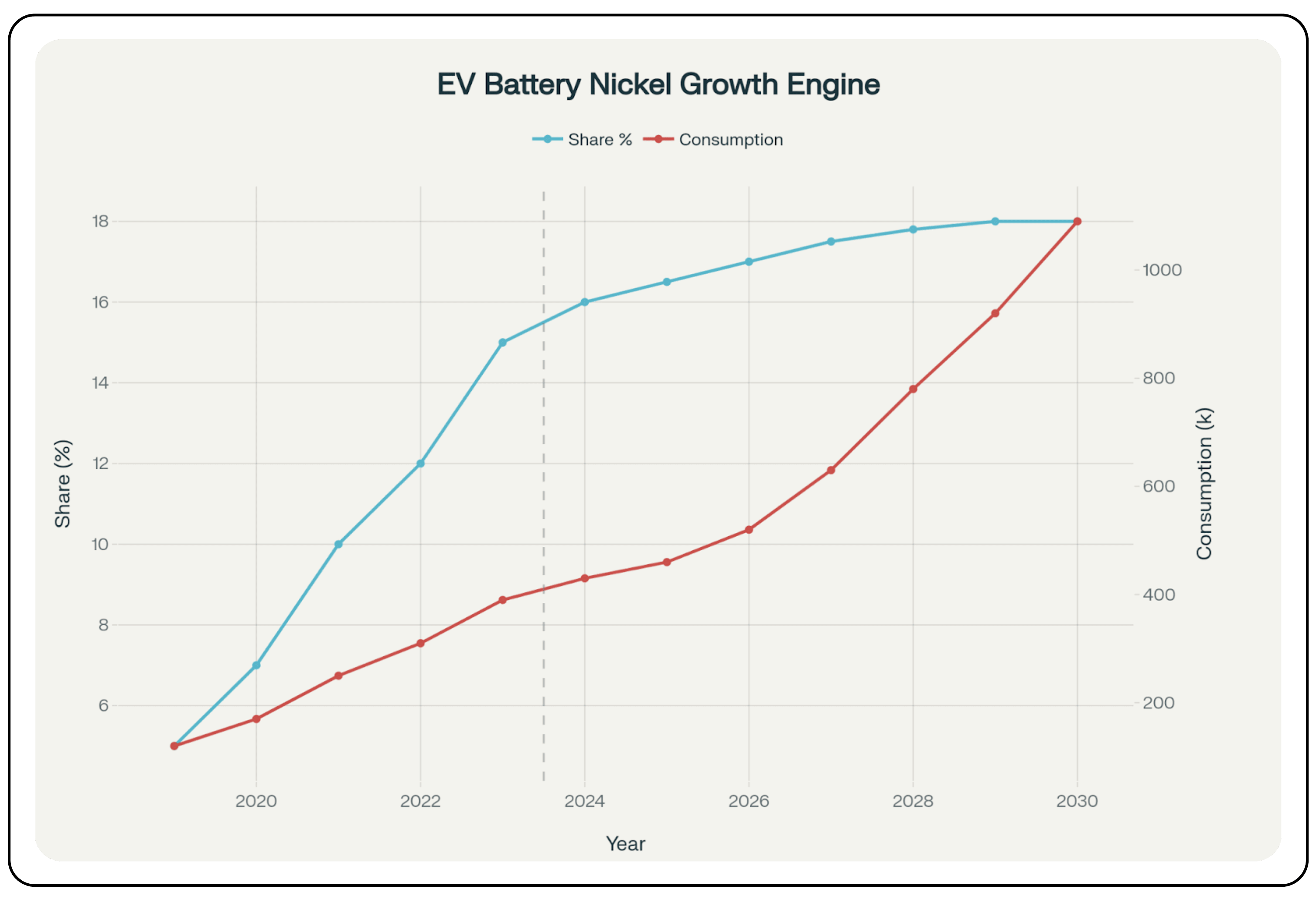

- The EV battery growth engine: The EV battery sector is the most dynamic growth driver of future nickel demand. Its share of battery-related consumption surged from 5% in 2019 to 15% in 2023. This is projected to rise to 18% by 2030, requiring up to 1.09 million tonnes of annual demand. High-nickel cathodes (NMC, NCA) are favoured for their superior energy density, which translates to longer driving ranges for EVs.

- Other critical applications: Beyond stainless steel and EV batteries, nickel is irreplaceable in high-performance superalloys used in aerospace and defense, corrosion-resistant alloys for the marine and chemical processing industries, and various other specialty applications.

The concurrent growth from these sectors is creating a structural ‘quality squeeze.’ As massive EV demand for Class 1 nickel competes with incumbent high-spec industries, the market will be forced to produce more Class 1 material from laterites via the expensive and environmentally challenging HPAL process. This will likely lead to a sustained ‘purity premium’ for Class 1 nickel over Class 2 NPI.

From mine to metal - production pathways

The geological split between sulfide and laterite ores dictates two radically different production value chains.

Sulfide vs. Laterite Ores

Sulfide ores are higher-grade, can be physically concentrated, and are processed via a traditional pathway of mining, crushing, flotation, smelting, and refining to produce Class 1 nickel. In contrast, laterite ores are generally lower-grade and cannot be concentrated. Instead, the entire ore must be chemically treated.

Laterite processing: RKEF vs. HPAL

The processing of laterites is split into two main routes:

- Pyromettallurgy (RKEF): The Rotary Kiln-Electric Furnace process treats saprolite ore at extreme temperatures (up to 1,600°C) to produce Class 2 ferronickel (FENi) or Nickel Pig Iron (NPI) for the stainless steel industry. It is extremely energy-intensive.

- Hydrometallurgy (HPAL): This High-Pressure Acid Leaching is used to process limonite ore with sulfuric acid under high pressure and temperature (245-270°C) in large autoclaves. It produces an intermediate product (MHP) that is refined into Class 1 nickel sulfate for batteries.

Economics and environment

Costs: HPAL plants are notoriously expensive, with an average capital intensity of $49,000 per tonne of annual capacity, significantly higher than RKEF plants. While capital costs differ greatly, operational costs are more comparable, driven by electricity for RKEF and chemical reagents for HPAL.

Environment: Laterite processing is far more energy- and carbon-intensive than sulfide processing. The RKEF process has carbon emissions more than double those of HPAL. However, HPAL is still more carbon-intensive than sulfide processing and generates enormous volumes of toxic, acidic tailings that require perpetual management.

Trading and Logistics

The global nickel market is underpinned by a sophisticated infrastructure for price discovery and physical logistics, anchored by the London Metal Exchange (LME) and, increasingly, the Shanghai Future Exchange (SHFE).

The LME provides the global reference price through its physically-deliverable contract. Key specifications for the LME contract are for Class 1 nickel: a lot size of 6 metric tonnes and a minimum purity of 99.80%. The LME’s flexible prompt date structure allows for precise hedging out to 63 months.

Physical delivery is facilitated by a global network of over 450 LME-approved warehouses across 34 locations. Settlement is conducted using the LME warrant, a document of title for a specific lot of metal stored in a warehouse, with transfers handled electronically via the LMEsword system. The movement of stocks within this network provides a real-time barometer of physical demand and global trade flows.

The Multi Commodity Exchange of India (MCX) serves as the principal hub of nickel futures trading in the country. The MCX provides the domestic reference price through this physically-deliverable, INR-denominated contract. This allows Indian market participants to hedge not only against global price volatility but also against currency fluctuations.

| Contract Feature | Specification (Effective Sept 2025 Expiry) |

|---|---|

| Trading Unit | 250 kilograms per contract |

| Delivery Unit | 1,500 kilograms (i.e., 6 contracts) |

| Last Trading Day | Third Wednesday of the expiry month |

| Settlement Type | Compulsory physical delivery |

| Delivery Mechanism | Centralised warehousing system |

| Primary Delivery Centre | Thane, Maharashtra |

| Additional Warehouses | Exchange-accredited, third-party operated within a 100 km radius of Thane |

| Delivery Period | Staggered three-day period at the end of the contract month |

| Delivery Intentions | Sellers with open positions submit their intention to deliver via the exchange; allocations are made randomly to buyers |

| Acceptable Material | Only LME-approved brands of primary nickel cathodes with a minimum 99.80% purity |

Market Outlook and Strategic Analysis

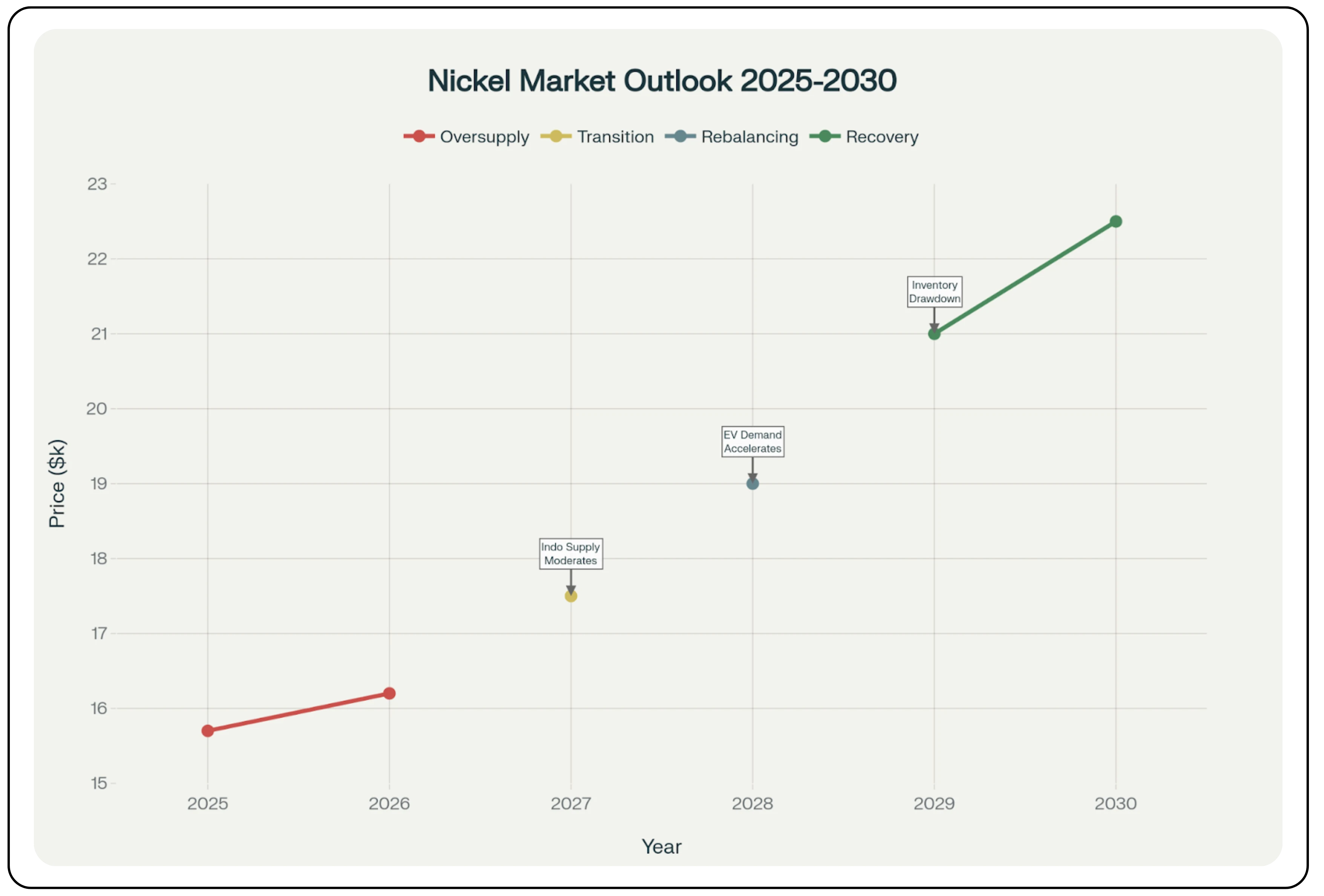

The nickel market’s short-term outlook is dominated by oversupply, while long-term fundamentals are shaped by the energy transition.

The consensus view for the short term (2025-27) is bearish to neutral, with an Indonesian-driven surplus expected to keep prices anchored. Major forecasts for 2025 put the average price at around $15,700 per metric tonne.

A market rebalancing is expected between 2028 and 2030 as Indonesian supply growth moderates and EV-driven demand for Class 1 nickel accelerates. This is forecast to erode the surplus, with prices projected to recover towards and beyond $20,000 per metric tonne by 2030.

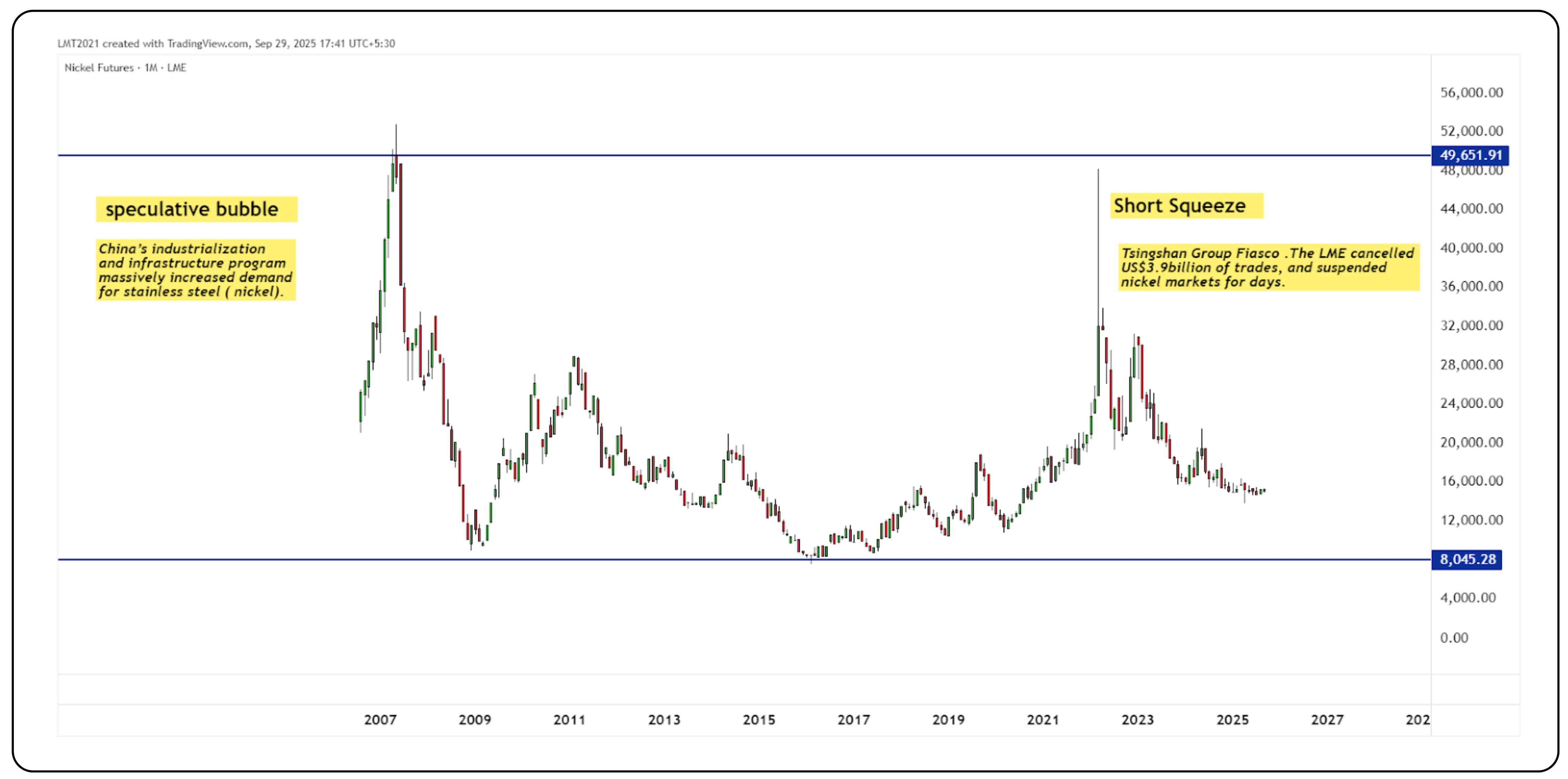

However, this fundamentals-driven forecast must be viewed against the backdrop of nickel’s inherent volatility. A look at the market’s history reveals its susceptibility to extreme price shocks that can temporarily override supply-and-demand dynamics.

Two key events illustrate this risk:

- The 2007 Speculative Bubble: Driven by China’s unprecedented industrialization and massive demand for stainless steel, nickel prices surged to record highs in a classic commodity super-cycle bubble.

- The 2022 Short Squeeze: More recently, the market was thrown into chaos by a historic short squeeze centered around producer Tsingshan Group. The event triggered a price spike so severe that the London Metal Exchange (LME) was forced to suspend trading and cancel transactions, a move that highlighted extreme financial risk within the market structure.

While the 2025-30 outlook projects a more orderly price recovery based on moderating supply and rising EV demand, these historical events serve as a crucial reminder. They underscore the potential for macroeconomic shifts or financial market dislocations to cause rapid and dramatic deviations from the forecasted path.

Key risks and strategic recommendations

The path forward contains significant risks, including potential sanctions on Russian supply (which accounts for 11% of the global total), further Indonesian resource nationalism, and a faster-than-expected shift by automakers to nickel-free LFP batteries.

For investors: Differentiate between the oversupplied Class 2 market and the structurally tighter Class 1 market. Focus on Class 1 producers and monitor signals for market rebalancing around 2027-28.

For Industrial Users: Use the current low-price environment to secure long-term Class 1 supply investment upstream investment and diversify away from the concentrated Sino-Indonesian supply axis.

For policymakers: Foster domestic supply chains through industrial policy, consider strategic stockpiling of Class 1 nickel, and implement strong ESG standards to level the playing field for more sustainable producers.

Conclusion

The global nickel market is navigating a defining transition. While today’s story is one of oversupply, the reality is more nuanced: a bifurcated market where an oversupply of Class 2 nickel coexists with a structurally constrained outlook for Class 1, the material essential for the energy transition. The depletion of traditional sulfide deposits is forcing the industry down more expensive and environmentally challenging pathways to meet EV demand, which will likely entrench a “purity premium” for battery-grade nickel. Success in this new era will belong to those who can manage the profound geopolitical risks for a concentrated supply chain and the technological risks of evolving battery chemistries. From being a cursed ore to a critical enabler of a decarbonized economy, nickel’s most consequential chapter has just begun.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.