.webp%3Falt%3Dmedia%26token%3D19cd6f9e-16e5-455c-9cf0-a0f7c4ae9d4a&w=3840&q=85)

The Public Provident Fund (PPF) has long been a foundational savings and fixed income instrument for Indian households, often serving as a tool for financial planning and asset allocation. Households invest in the Public Provident Fund seeking safety, tax efficiency, and long-term capital protection. Backed by the Government of India, it occupies a unique position among fixed-income options by combining sovereign security with favourable tax treatment and a clearly defined investment framework.

For individual investors, the PPF fund is not merely a savings account but a statutory, long-duration instrument governed by specific legal, tax, and liquidity rules that distinguish it from bank fixed deposits. Understanding the benefits of PPF account ownership is essential to appreciate the differences between it and other small-savings schemes.

Sovereign Guarantee and Public Provident Fund Interest Rate

The defining characteristic of the Public Provident Fund is its sovereign guarantee. Unlike bank deposits, which are insured only up to ₹5 lakh under the Deposit Insurance and Credit Guarantee Corporation framework, PPF balances are backed by the Government of India, making them effectively free from default risk.

The Ministry of Finance, Government of India, announces the Public Provident Fund Interest Rate every quarter, often influenced by prevailing Monetary Policies. Interest on Public Provident Fund is compounded annually and is paid in March every year.

Also read: Why Disciplined Investing Has Limits in Creating Big Wealth

The Fifth Day Rule

The Fifth Day Rule. A critical technical detail often overlooked is the Public Provident Fund calculation. The interest is compounded annually but calculated monthly. However, the calculation of PPF account interest is based on the lowest balance in the account between the close of the fifth day and the end of the month.

This means that a deposit made on the 6th of a month will earn zero interest for that specific month. To earn interest for the full month, funds must be credited to the account on or before the 5th. This nuance plays a significant role in the compounding effect over the 15-year tenure.

Taxation Structure in the 2026 Regime

The PPF continues to fall under the Exempt-Exempt-Exempt or EEE classification. This status is relevant for investors analyzing their post-tax returns.

- Contribution Phase: For individuals filing under the Old Tax Regime, contributions up to ₹1.5 Lakhs per financial year are deductible under Section 80C. For those under the New Tax Regime, this deduction is not available.

- Accumulation Phase: The interest added to the account every year is fully exempt from income tax. This is a key differentiator from Fixed Deposits, where accrued interest is taxed annually.

- Withdrawal Phase: The entire maturity corpus, comprising both the principal and the accumulated interest, is free from tax.

Eligibility and the Clubbing Provision

The scheme is open to all Resident Indians. However, there are specific restrictions that define who can hold an account.

Individual Ownership: A PPF account can only be opened in the name of one individual. (It is not a personal provident fund account) Joint accounts are not permitted.

Minors and Guardians: A guardian can open an account on behalf of a minor. However, the law applies a rule to the investment limit. The combined deposit in the guardian's own account and the minor's account cannot exceed the cumulative limit of ₹1.5 Lakhs per financial year.

HUF Restrictions: Since May 2005, Hindu Undivided Families or HUFs have been barred from opening new PPF accounts. Any HUF accounts opened before this date may continue until maturity, but cannot be extended further.

Also read: The Strategic Importance of an Emergency Fund in the Economic Landscape of 2026

Premature Closure Provisions

The scheme allows for the account to be closed before the 15-year maturity, but only under specific, documented circumstances. This is permitted only after the account has completed five full financial years.

The valid grounds for premature closure include:

Medical Treatment: For life-threatening ailments affecting the account holder, spouse, dependent children, or parents.

Higher Education: For the account holder or dependent children, on production of admission documents.

Residency Change: On a change in residential status to Non-Resident Indian (NRI), premature closure of the account is permitted. However, the account may also be continued until maturity without making further contributions.

The Penalty Clause

Premature closure attracts a penalty in the form of an interest rate reduction. The interest for the entire tenure of the account is recalculated at a rate that is 1% lower than the rate actually credited. This retrospective deduction is adjusted from the final payout.

Maturity and Extension Mechanics

Upon completion of 15 financial years, the PPF account matures. At this stage, the subscriber has three options:

Closure: The entire balance can be withdrawn, and the account closed.

Extension without contribution: If no application is submitted, the account is automatically extended. The existing balance continues to earn the prevailing interest rate, and the subscriber may withdraw any amount once in each financial year.

Extension with contribution: The account may be extended in blocks of five years with fresh deposits by submitting the prescribed request form within one year of maturity. During each five-year extension block, withdrawals are limited to 60 percent of the balance at the beginning of the extension period.

Transferability

A PPF account can be transferred seamlessly across India, whether from the Post Office Public Provident Fund scheme to a bank or between banks. The transfer process preserves the original account opening date, balance, and maturity schedule, ensuring continuity of the investment.

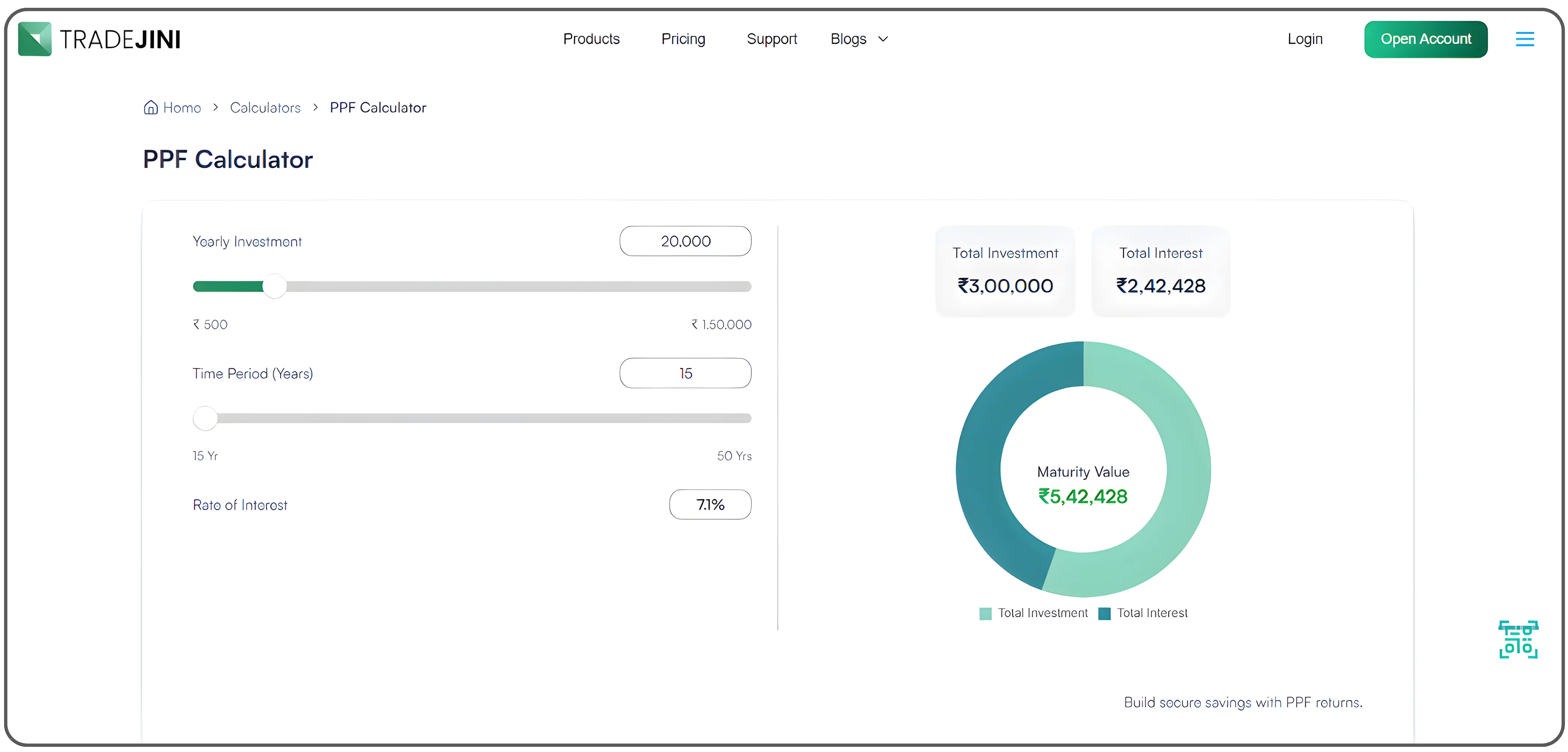

Use Tradejini’s PPF calculator to estimate your maturity value and understand how regular contributions compound over time.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.