The Indian automotive component sector has steadily emerged as an alternative global supply hub, with the sector now recognized as a critical node in the global auto supply chain, particularly as companies pursue 'China plus one' sourcing strategies. The sector’s revenue growth has now outpaced vehicle production for the second consecutive year, signalling a structural shift toward higher value addition per vehicle. This change is being driven by increasing content from electronics, EV-compatible systems, and precision engineering components.

Demand and Global Realignments

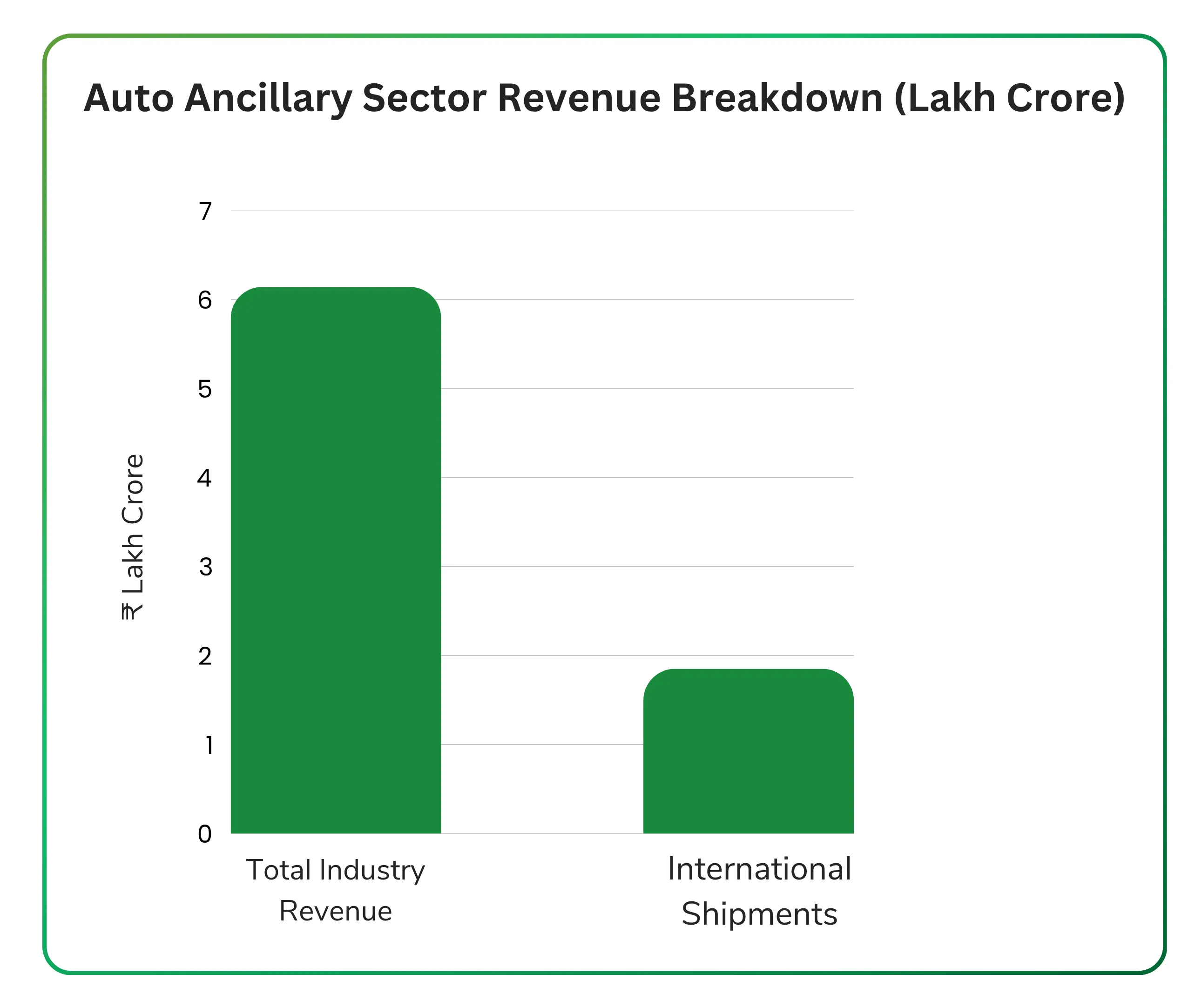

The Indian automotive component sector has steadily emerged as an alternative global supply hub within the global auto supply chain, as international OEMs pursue diversification strategies beyond single-country dependencies. India's auto component revenue reached ₹6.14 lakh crore in FY2025, with exports of ₹1.85 lakh crore, representing the sector's capacity to serve global original equipment manufacturers across North America, Europe, and emerging markets. As global OEMs focus on supply chain diversification, Indian manufacturers have expanded capacity and strengthened global linkages. The sector has demonstrated consistent growth since FY2016, with an expected revenue CAGR between 8–10% through FY2026, positioning India as a critical player in automotive mission plan 2047 targets. This growth is supported by a 9.1% rise in domestic vehicle production and increasing EV adoption. While electric vehicles reduce mechanical part requirements, leading suppliers are gradually shifting toward higher-value components such as electronics and thermal systems.

Sector Constituents and Financial Metrics

Within this complex operational ecosystem, distinct strategic niches determine the financial health of individual corporations. By focusing intently on heavy engineering, Cummins India is a leading supplier through the production of high-displacement diesel and hydrogen internal combustion engines.

Cummins India

Known for its proprietary ride control solutions, Gabriel India retains exceptional market share by manufacturing millions of specialized shock absorbers and front telescopic struts annually.

Gabriel India

For passenger car climate control, Subros holds a significant presence supplying integrated heating, ventilation, and air conditioning compressors.

Subros Ltd.

Following a massive generational technological shift, Pricol has pivoted effectively from mechanical dials to producing advanced thin-film transistor instrument clusters and linked telematics modules.

Pricol Ltd.

On the heavy commercial side, Automotive Axles directly supports the trucking industry by forging specific rear drive axles and foundational drum brakes. To capture premium domestic upgrade trends, Steel Strips Wheels has steadily shifted its massive pressing capacity toward the production of high-margin alloy and passenger steel wheel rims.

Steel Strips Wheels

These leading auto component companies span multiple vehicle segments—two wheeler auto components, passenger vehicle platforms, commercial vehicle suppliers, and tractor component systems—each navigating the ice to ev shift with distinct technological advantages.

| Entity | Core Business Focus | Trailing Sales (₹ Cr) | Operating Margin (%) | Market Capitalization (₹ Cr) | Price-to-Earnings Ratio |

|---|---|---|---|---|---|

| Cummins India | Commercial Vehicle Engines | 8,800 | 18% | 1,10,000 | 55x |

| Gabriel India | Ride Control & Shocks | 3,200 | 8% | 5,500 | 30x |

| Pricol | Digital Driver Displays | 2,300 | 12% | 5,800 | 38x |

| Subros | Thermal Management | 3,000 | 8% | 4,200 | 45x |

| Automotive Axles | Drivetrain & Axles | 2,300 | 11% | 3,500 | 20x |

| Steel Strips Wheels | Alloy & Steel Wheels | 4,200 | 10% | 4,000 | 18x |

| Lumax Industries | Automotive Lighting | 2,600 | 11% | 2,800 | 22x |

| Rico Auto | Aluminum Die Castings | 2,400 | 9% | 1,800 | 25x |

| Rane Madras | Steering & Suspension | 2,300 | 7% | 1,500 | 35x |

| Automotive Stampings | Sheet Metal Stampings | 850 | 5% | 1,200 | 40x |

| Munjal Showa | Suspension Systems | 1,400 | 4% | 650 | 15x |

| Autoline Industries | Welding & Assemblies | 700 | 6% | 600 | 25x |

This peer group demonstrates the valuation diversity across the auto component sector. While leaders like Cummins command premium valuations reflecting their engine expertise, smaller component specialists like Automotive Axles and Steel Strips Wheels maintain competitive price-to-earnings multiples, offering entry points for investors evaluating auto component valuation india and long-term component pe ratio india positioning.

Smaller constituents like Munjal Showa and Autoline are increasingly focusing on welding automation and specialized suspension sets to maintain margins amidst the ICE-to-EV shift.

The EV Transition: Auto Component Disruption and Opportunity

The transition to electric vehicles presents simultaneous disruption and opportunity, with the EV transition auto components India representing perhaps the sector's most material structural shift in three decades. For suppliers, the ICE to EV transition fundamentally reshapes the auto component fundamental analysis framework. An ICE vehicle comprises over 2,000 moving parts; an equivalent EV drivetrain requires fewer than 20. The components eliminated include cylinder blocks, pistons, fuel delivery systems, exhaust assemblies, and alternators, categories that account for a significant share of the domestic supplier base's current revenue. This mechanical simplification directly challenges suppliers concentrated in engine parts, transmissions, and exhaust systems; categories where roughly 50% of the domestic auto component industry remains positioned.

"Nearly 50% of the domestic auto component players are either making engine parts or the transmission drive, which will have no place in an electric car." — Munjal Showa MD&A, FY2025

A new supply-side risk emerged in 2025: China's export restrictions on rare earth magnets (which it controls to over 80% globally) caused magnet export volumes to drop 75% year-on-year, driving a 15–25% cost increase for magnet-dependent components across EV motors, power steering, actuators, and sensor assemblies. Pricol's Management Discussion explicitly flags rare earth magnet availability as a material input cost risk affecting product roadmaps.

EV component localization in India currently stands at 30–40%; battery cells remain almost entirely imported. The ACC Battery Storage Program (₹18,100 crore) and PLI scheme for advanced automotive technology are the primary policy instruments targeted at closing this gap. Companies that qualify on EV-platform programs while continuing to serve the 30+ million ICE vehicles produced annually are best positioned to manage the transition without revenue disruption.

For deeper insight into how capital-intensive sectors navigate structural transitions, Samhi Hotels Limited - A Fundamental Analysis of the Turnaround Case demonstrates the same analytical framework applied to turnaround scenarios.

Vehicle Segment Performance

Production trends diverge significantly across India's auto component market segments, with auto component two wheeler india and auto component passenger vehicle india outperforming the auto component commercial vehicle india segment.

| Segment | Production Growth (FY25) | Volume | Driver / Risk |

|---|---|---|---|

| Two-Wheelers | +11.3% | 19.6 mn units | Rural demand recovery; scooter-led |

| Passenger Vehicles | +3.3% overall; EVs +13.6% | 4.3 mn units (all-time high) | EV premium mix driving component value |

| Commercial Vehicles | −3.3% | 9.6 lakh units | MHCV flat; LCV −5.2% |

| Three-Wheelers | +5.4% | 7.4 lakh units (all-time high) | Urban fleet growth |

| Tractors | +7–8% retail | — | Kharif/Rabi harvest driven |

These segment-level dynamics reflect underlying demand drivers: rural consumption supporting two wheelers, urban fleet upgrades in three wheelers, and persistent pressure on heavy commercial vehicle operations. The composition of this vehicle production base directly determines the demand profile for component suppliers across the auto component tractor india and auto component semiconductor india verticals.

The EV-led premium shift has elevated per-vehicle component value in HVAC, instrumentation, and ride control. Suppliers concentrated in MHCV supply faced direct volumetric pressure, partially offset by aftermarket revenue from the existing installed fleet.

The 9.1% headline production figure masks diverging segment-level trends. Growth was concentrated in two-wheelers and utility vehicles, while commercial vehicles contracted.

Operational Metrics, Capital Expenditure, and Auto Component PLI Scheme Impact

Moving beyond generalized industry tailwinds, precise capacity expansions, distinct geographic revenue splits, and targeted technological investments dictate the immediate execution risks for these manufacturers. Within the domestic supply chain, significant capital expenditure is being aggressively deployed toward specific original equipment vehicle programs. Geared explicitly toward the Tata Sierra and next-generation commercial vehicle platforms, firms like Autoline Industries have commissioned dozens of advanced robotic welding nodes. Growing beyond pure passenger mobility applications, Subros is actively expanding its thermal engineering capacity from 15 lakh to 20 lakh units to capture emerging home and railway air conditioning demand.

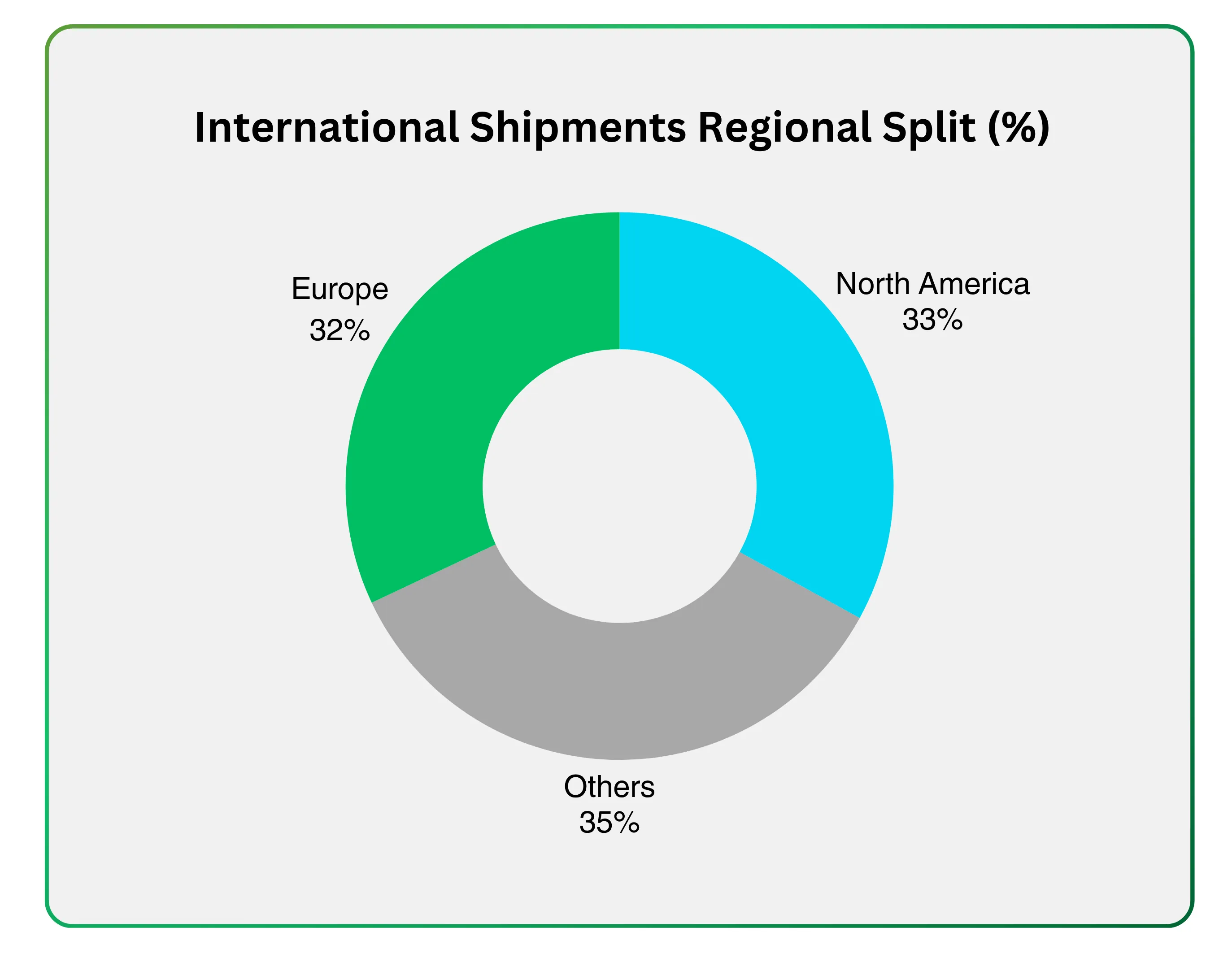

Beneath the aggregate ₹1.85 lakh crore in international shipments, distinct geographic dependencies dictate export profitability. Growing at a steady pace of 5% annually, the North American market absorbs approximately 33% of total outbound component volume. Expanding at a much faster rate of 12%, European original equipment manufacturers account for an almost identical volumetric share of 32%.

Anticipating the obsolescence of legacy internal combustion platforms, niche market leaders are funding highly specialized technological pivots. Shifting away from mechanical instrumentation, Pricol is investing aggressively in connected vehicle telematics and thin-film-transistor displays to secure future revenue streams. Hedging against pure battery-electric commercial vehicle dominance, Cummins India has intentionally diverted engineering capital toward hydrogen internal combustion engine architectures.

Sustained Policy Intervention: Auto Component PLI Scheme, PM E-DRIVE, and Mission 2047

Beneath surface-level demand recovery, the auto component pli scheme india and complementary policy instruments continue to dictate capital allocation across the sector. The combined framework of production-linked incentives, pm e drive scheme support, and automotive mission plan 2047 commitments creates structural support for component manufacturers pursuing ev auto components india and advanced automotive technology qualification. Under the extensive Production Linked Incentive scheme, federal authorities have committed nearly ₹26,000 crore to catalyze local manufacturing of advanced automotive technologies. To qualify for these fiscal benefits, component manufacturers have dramatically increased their research and development outlays. Alongside this direct financial support, the national vehicle scrappage policy has begun to generate a steady replacement cycle for aging commercial fleets. Across the entire value chain, such policy levers have effectively forced global tier-one suppliers to deepen their domestic joint ventures rather than relying merely on imported assemblies, though such localization does little to insulate them from broader economic fluctuations.

Policy Framework: The following government initiatives are directly material to the sector's FY2026 and medium-term growth trajectory:

PLI Automobiles & Auto Components (₹2,818 crore, FY26; extended to March 2028): Targets Advanced Automotive Technology products EV drivetrains, traction motors, battery management systems. Union Budget 2025 increased PLI allocations for the combined auto and battery category by 713%. Catalyzed ₹4,850 crore in committed investment against a ₹7.8 billion program target. (Source: Lumax, Gabriel MDs FY2025)

PM E-DRIVE (₹10,900 crore, effective till March 2026): Supports 25 lakh electric two-wheelers, 3.2 lakh three-wheelers, and 14,000 electric buses. Allocation was increased by 114% in Union Budget 2025. (Source: Gabriel India MD FY2025)

FAME II (+₹1,500 crore) and EMPS 2024 (₹500 crore): Maintained EV demand continuity across the FY24–25 policy transition window.

Customs duty exemption on 35 battery capital goods (Budget 2025): Reduces investment cost for domestic battery cell manufacturing, the sector's most critical localization gap.

100% FDI under Automatic Route: Sector attracted $37.21 billion in cumulative FDI equity (April 2000 – September 2024). FDI inflows across India reached USD 81.04 billion in FY24–25 (+14% YoY). (Source: Rico Auto MD FY2025)

PM Gati Shakti / Dedicated Freight Corridors / Maritime Development Fund (₹25,000 crore): Reducing logistics costs and improving export transit times versus competing geographies Mexico, Germany, Thailand. (Source: Cummins India MD FY2025)

Automotive Mission Plan 2047: Targets auto sector's GDP contribution to exceed 12% (from ~7.1% currently); projects 65 million incremental direct and indirect jobs.

The commodity exposure and export dynamics examined here parallel the supply-chain pressures in Strategic Outlook of The Indian Tea and Coffee Sector, where raw material volatility and global demand shifts reshape sector fundamentals.

Key Risks and Headwinds

US Tariff Exposure: The auto component US tariff regime, effective April 2025, directly impacts the 33% of Indian component exports destined for North America. For companies with concentrated north america auto component exports revenue, tariff escalation carries material margin risk and forces strategic supply-chain reconfiguration. JTEKT India's US-bound export share declined from 4% to 2.4% of revenues in FY2025, with a disclosed 56 basis-point margin impact. Tariff escalation risk remains elevated for companies with concentrated North American revenue.

Customer Concentration: Tier-1 suppliers typically derive 60–80% of OEM revenue from two to three customers. Long-cycle platform commitments structurally limit diversification, making annual revenue sensitive to volume forecast changes at individual OEMs.

Raw Material Volatility: Steel, aluminium, and specialty plastics represent 55–65% of bill-of-materials costs. FY2025 margin stability (11–12% operating margins) depended on benign commodity pricing. Long-cycle OEM pricing contracts create a 2–4 quarter lag between input cost escalation and pricing relief.

Part-Count Reduction Risk (ICE to EV): As described above, roughly half the domestic supplier base is concentrated in ICE-specific components. The timeline of EV penetration will determine whether this shift creates gradual reallocation or abrupt revenue displacement for companies that have not begun transitioning their product mix.

Semiconductor Dependency: ADAS modules, digital instrument clusters, infotainment systems, and telematics units depend on chipsets with concentrated manufacturing geographies and long procurement lead times. Any recurrence of 2021–22-style supply tightening would directly affect OEM production schedules and Tier-1 delivery performance. (Source: Lumax MD FY2025)

Maritime Route Disruption: The Red Sea crisis elevated auto component logistics india costs and extended transit times on european auto component exports routes. Suppliers with material Europe-bound revenue retain structural exposure to further maritime disruptions. JTEKT India cited increased inward freight costs as a disclosed margin impact. Suppliers with material Europe-bound export revenue retain structural exposure.

Cyclicality and Input Pricing Pressures: The sector remains bound to OEM production cycles, with two-wheeler and tractor volumes particularly sensitive to agricultural yields and credit availability. During demand downturns, specialized suppliers absorb the financial strain of underutilized capacity. Beyond volume risk, margins are consistently tested by international commodity pricing, primarily steel, aluminum, and copper. To mitigate inflationary shocks, leading players have increasingly formalized raw material pass-through clauses in long-term supply agreements.

Strategic Outlook

The Indian automotive component sector is expected to grow at 8–10% revenue CAGR through FY2026, supported by domestic demand, export expansion to North America and Europe, and sustained auto component pli scheme support. However, this outlook depends on several factors: stable demand, no escalation in the auto component us tariff regime, easing of auto component rare earth magnet supply constraints, and a gradual ice to ev transition that allows suppliers time to adapt. The growth trajectory carries four conditions: domestic demand must hold, the US tariff situation must not escalate to India-specific barriers, the rare earth magnet supply disruption requires partial resolution within 18–24 months, and EV penetration must continue at a pace that allows suppliers time to transition their product mix. Each of these is tracked as a disclosed risk across the management filings reviewed.

India's share in the global auto component market currently stands at approximately 3%. The sector's ambitious automotive mission plan 2047 targets an 8% global market share by 2030, positioning the Indian auto component sector as a critical node within the global auto supply chain, exceeding $1.6 trillion. The companies reviewed in this report, through their R&D investment, patent filing activity, EV-platform qualifications, and export market expansion are the early evidence of whether that target is realistic.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.