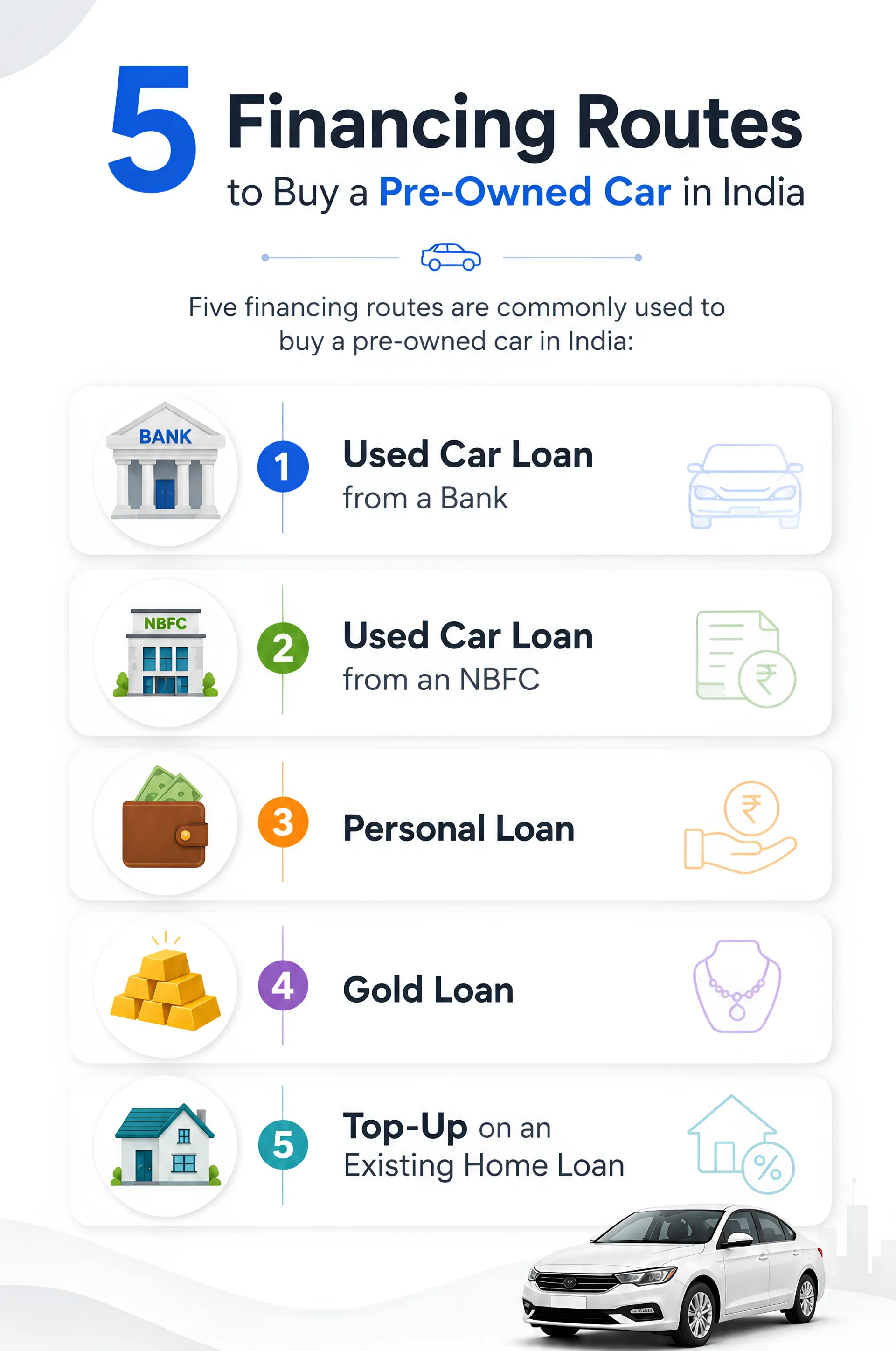

A used car loan looks simple on the surface: pick a lender, check the interest rate, sign. In practice, the rate you see advertised is rarely the number that decides how much you actually pay. Processing fees, valuation charges, the loan tenure, and even how old the car is by the time you finish repaying can shift the real cost by a wide margin. Five financing routes are commonly used to buy a pre-owned car in India: a dedicated used car loan from a bank, one from an NBFC, a personal loan, a gold loan, or a top-up on an existing home loan. Each behaves differently once you look past the number on the brochure.

Comparing Your Financing Options

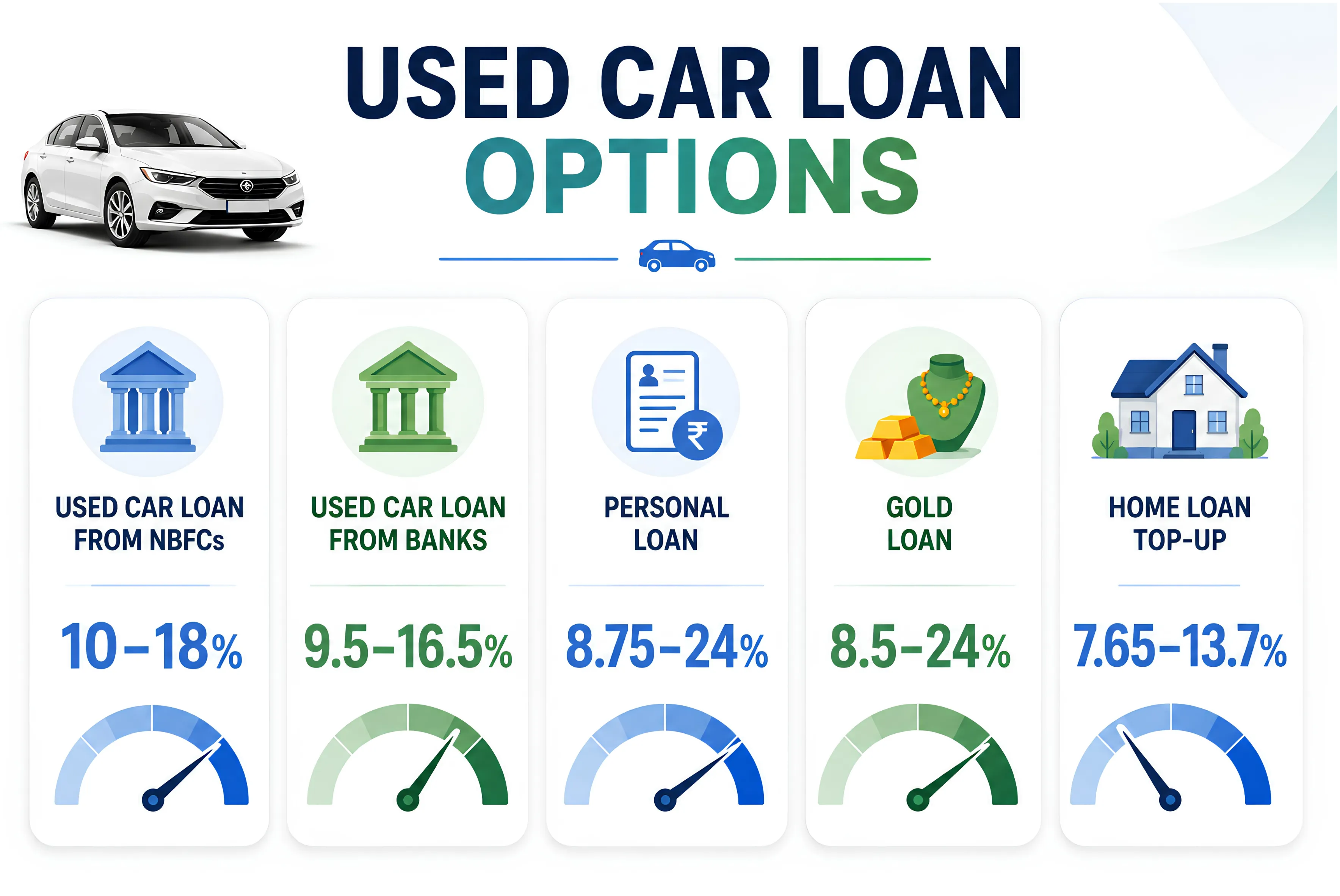

Used car loan from NBFCs: 10–18%. NBFCs tend to approve faster and are more willing to finance older vehicles and thinner credit files than banks typically accept. That flexibility carries a cost: processing fees usually run 1–2% of the loan amount, and the rate itself sits at the higher end of the market. For a buyer who wouldn't clear a bank's eligibility checks, this is often the only door open, but it's rarely the cheapest one.

Used car loan from Banks: 9.5–16.5%. Banks generally price lower than NBFCs, but the loan comes with its own list of add-ons: vehicle valuation charges, mandatory GPS tracking device fees, and documentation costs that don't show up in the advertised rate. There's also a quieter issue worth knowing about. Dealers frequently earn a commission for steering buyers toward a specific lender, so the bank recommended at the showroom counter isn't automatically the best deal available in the market.

Personal loan: 8.75–24% Since a personal loan is unsecured, it skips the vehicle-as-collateral structure entirely, which some buyers prefer. The tradeoff is a shorter repayment window than a dedicated car loan, which pushes the EMI higher, and not every personal loan amount will stretch far enough to cover a premium used car. The rate band here is also unusually wide, so the actual cost depends heavily on individual credit history.

Gold loan: 8.5–24%. For a buyer who has gold to pledge, this can work out cheaper than a used car loan at the lower end of its range. Two risks come with it. Tenures tend to be short, so EMIs run high, and if gold prices fall sharply while the loan is running, the lender can demand additional collateral or early repayment through a margin call.

Home loan top-up: 7.65–13.7%. This is the least expensive option on paper because it's secured against property. That's also where the risk lies: a home, an appreciating and essential asset, is pledged to fund a car, a depreciating one. Not every lender offers a top-up facility, and the ones that do generally favour borrowers who are well into their existing home loan tenure rather than those who took the loan recently.

Why the Rate on the Brochure Rarely Tells the Full Story

A lower advertised rate doesn't automatically mean a cheaper loan once processing fees, valuation charges, GPS costs, and documentation fees are added in. Two loans quoting similar rates can end up costing very different amounts once these charges and the repayment tenure are factored in. The only reliable comparison is the total cost of borrowing: principal, interest, and every fee combined, not the rate in isolation.

Consider a simple illustration. On a loan of ₹5 lakh over five years, a lender charging 10% interest but adding a 2% processing fee and modest valuation and documentation charges could end up costing more in year one than a lender charging 10.5% with a flat, low processing fee and no add-ons. The gap only shows up when both are laid out as total repayment, not when the rates are compared side by side.

Tenure, and the car's age, also change the maths

Most banks and NBFCs cap used car loan tenures somewhere between three and seven years, and many tie this to the vehicle's age rather than a fixed number. A common industry practice is to cap the loan's maturity at around seven to eight years from the car's original registration date, not from the date of purchase by the second owner. A five-year-old car, in other words, may only qualify for a two or three-year loan, regardless of what tenure the lender advertises. A shorter tenure means a higher EMI but lower total interest paid, while a longer one eases the monthly burden but adds to the overall cost. It's worth asking the lender directly what tenure your specific car qualifies for before comparing rates.

Fixed versus floating

Used car loans are, more often than not, offered at a fixed rate, which means the EMI stays constant through the tenure. Home loan top-ups, by contrast, are usually floating and move with the lender's benchmark rate. This matters most for the top-up route: a low rate today doesn't guarantee the same rate two or three years into the loan.

Foreclosure charges

If there's a real chance of paying off the loan early, this is worth checking before signing rather than after. Foreclosure or prepayment charges on used car loans commonly range from 2% to 5% of the outstanding amount, though several lenders waive this after a minimum number of EMIs have been paid, and some banks don't charge it at all when the closure is funded from the borrower's own money. A loan that looks cheapest today can turn expensive if it penalises early closure and the borrower's plans change.

Also Read: India’s Most Expensive Cities in 2026

A Borrower's Checklist Before You Sign

Compare lenders, not just dealer offers. A commission-linked recommendation at the showroom is not the same as the best rate in the market.

Evaluate total repayment, not just the interest rate. Add up every fee that applies across the life of the loan before deciding.

Maintain a good credit score. It remains one of the strongest levers for negotiating a better rate across every option listed above.

Keep your FOIR within lender limits. FOIR, or Fixed Obligation to Income Ratio, measures how much of monthly income is already committed to existing EMIs and rent. Most lenders in India look for this to stay under 40 to 50%, though the exact ceiling varies by income band and lender policy. As an example, someone earning ₹80,000 a month with ₹25,000 already going toward EMIs and rent has a FOIR of roughly 31%, which leaves reasonable room for a new EMI. The same person with ₹45,000 already committed would be close to the ceiling most lenders apply, and a new car loan could get declined or offered on tighter terms.

Ask about the car's age at loan maturity, since this can silently shrink the tenure a lender is willing to offer, regardless of the advertised range.

Check the foreclosure clause, particularly if there's any possibility of repaying early.

Consider cheaper alternatives before signing, especially where gold or home equity is available, as long as the risks specific to that route are acceptable.

Which Route Suits Whom

A salaried, first-time borrower with a clean credit history and no existing loans is usually best served by comparing two or three banks directly, since this segment typically gets the most competitive rates. Someone with an older vehicle or a thinner credit file may find NBFCs are the only lenders willing to finance the purchase at all, in which case the priority shifts to minimising fees rather than chasing the lowest headline rate. A borrower who already owns gold and needs funds quickly, and is confident about repaying within a short window, may find a gold loan works out cheaper than either. And someone deep into repaying a home loan, with substantial equity built up and a stable income, is often the one buyer for whom a top-up genuinely is the cheapest route, provided they're comfortable with a family home standing as security for a car.

The Bottom Line

There is no universally "best" way to finance a used car. The right choice depends on what can be pledged, how quickly funds are needed, and how much risk is acceptable. What matters is resisting the pull of the headline rate and instead working out the full cost of each option, checked against personal repayment capacity, before signing anything.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.