Rohan still remembers the first month he earned above ₹1 lakh.

He was 27, working in Bengaluru, and had just received a promotion at a consulting firm. The salary message arrived on a Thursday evening. By Friday night, he had already started browsing for a bigger apartment closer to work. Within three months, his old bike was replaced with a car on EMI. Weekend dinners became normal instead of occasional. His old phone suddenly felt outdated. His annual Goa trip quietly became an international holiday.

None of it felt reckless.

After all, he could afford it now.

Two years later, Rohan was earning almost double what he made at 27. But every month still ended the same way. Salary credited. Expenses deducted. Credit card bill due. Investments postponed “for now”.

Somehow, more money had not created more breathing room.

That silent shift is called lifestyle inflation.

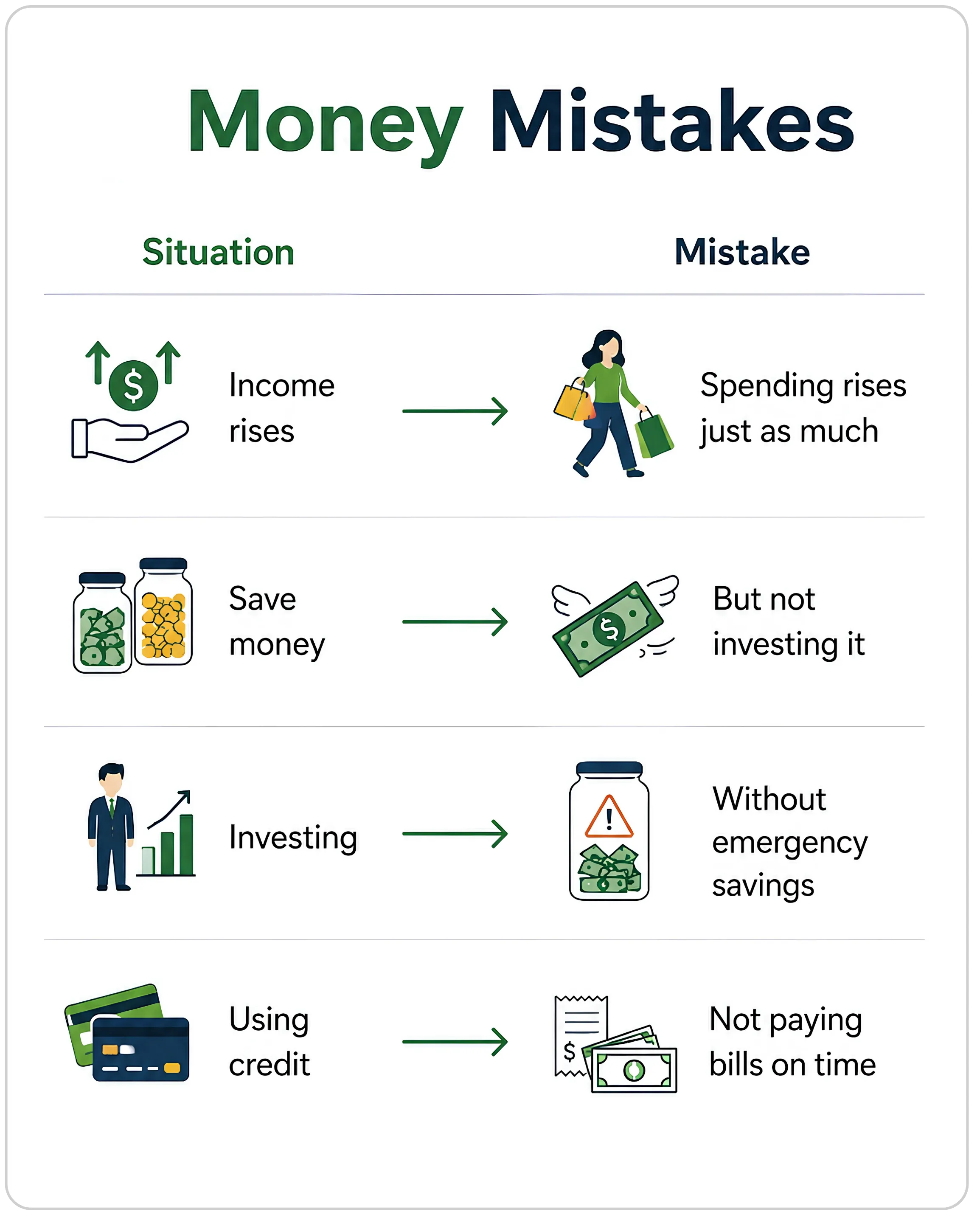

Lifestyle inflation happens when your spending rises every time your income rises. The extra money that could have built savings, investments, or financial freedom slowly gets absorbed into a more expensive version of everyday life. This pattern of lifestyle inflation personal finance experts discuss has become increasingly common among young professionals in urban India.

The tricky part is that lifestyle inflation rarely feels irresponsible. Most of the upgrades look reasonable on their own. A slightly better apartment. A newer phone every few years. More frequent vacations. Food delivery instead of cooking after work. None of these decisions look dramatic individually. But together, they slowly change your baseline. Over time, this gradual shift becomes a classic example of lifestyle creep India is witnessing across rising income groups.

And once a higher lifestyle becomes normal, going backwards feels uncomfortable even when financially necessary.

The Upgrades That Quietly Become Permanent

Take Neha, a 31-year-old marketing manager in Mumbai. When she started working, her monthly expenses were around ₹35,000 and she managed to save nearly ₹20,000 every month. Five years later, her salary had nearly tripled. But her savings had not. Her rent had doubled because she moved into a premium apartment. Her gym membership upgraded into an expensive fitness club. She now took cabs daily instead of using the metro. Her online shopping habits also changed quietly. Spending ₹8,000 on skincare or ₹15,000 during a sale no longer felt “too much.” On paper, she was successful. But she still depended entirely on her next salary credit. The higher income never translated into long-term wealth. This kind of lifestyle inflation often creates the illusion of financial success without actually improving long-term wealth creation.

Or consider Arvind from Hyderabad. During the pandemic, he started investing seriously through SIPs of ₹25,000 per month. By 2025, his salary had increased significantly. But instead of increasing investments, he upgraded his lifestyle. A larger SUV came with a ₹28,000 monthly EMI. Weekend brunches became routine. International travel entered the yearly budget. Slowly, his SIPs stayed frozen while his expenses expanded around them. The opportunity cost was invisible. That same additional ₹40,000 spent monthly could have compounded into crores over the next two decades. But lifestyle inflation rarely shows you the future version of the money you spend today.

The hidden opportunity cost lifestyle upgrades create is rarely visible immediately, but over decades, it can significantly impact wealth creation and financial freedom Indian investors aim for.

Why Lifestyle Inflation Feels So Normal

Lifestyle inflation becomes dangerous because human beings adapt quickly.

The first time you fly business class, it feels luxurious. The fifth time, it feels normal. The first expensive apartment feels exciting. A year later, it simply becomes “home”. What once felt special slowly becomes the minimum acceptable standard.

Behavioural finance researchers call this hedonic adaptation. It means people quickly return to a stable level of satisfaction even after positive lifestyle changes. The excitement fades, but the higher monthly expense stays. This idea of hedonic adaptation which researchers discuss explains why lifestyle upgrades stop feeling exciting surprisingly fast.

Social comparison also quietly fuels lifestyle inflation in urban India today.

You see friends upgrading phones, buying homes, travelling abroad, or dining at expensive places. LinkedIn celebrates promotions. Instagram celebrates lifestyles. Suddenly, spending starts feeling connected to progress. Holding back can even feel like falling behind. Social comparison spending in India has intensified because social media constantly exposes people to curated lifestyles and visible consumption.

But wealth and lifestyle are not the same thing.

Lifestyle is visible. Wealth usually is not.

The person driving a luxury car may still be worried about EMIs. The person quietly investing every month may look ordinary today but create far more financial freedom over time. This gap between lifestyle vs wealth Indian households experience often becomes visible only during financial emergencies or job uncertainty.

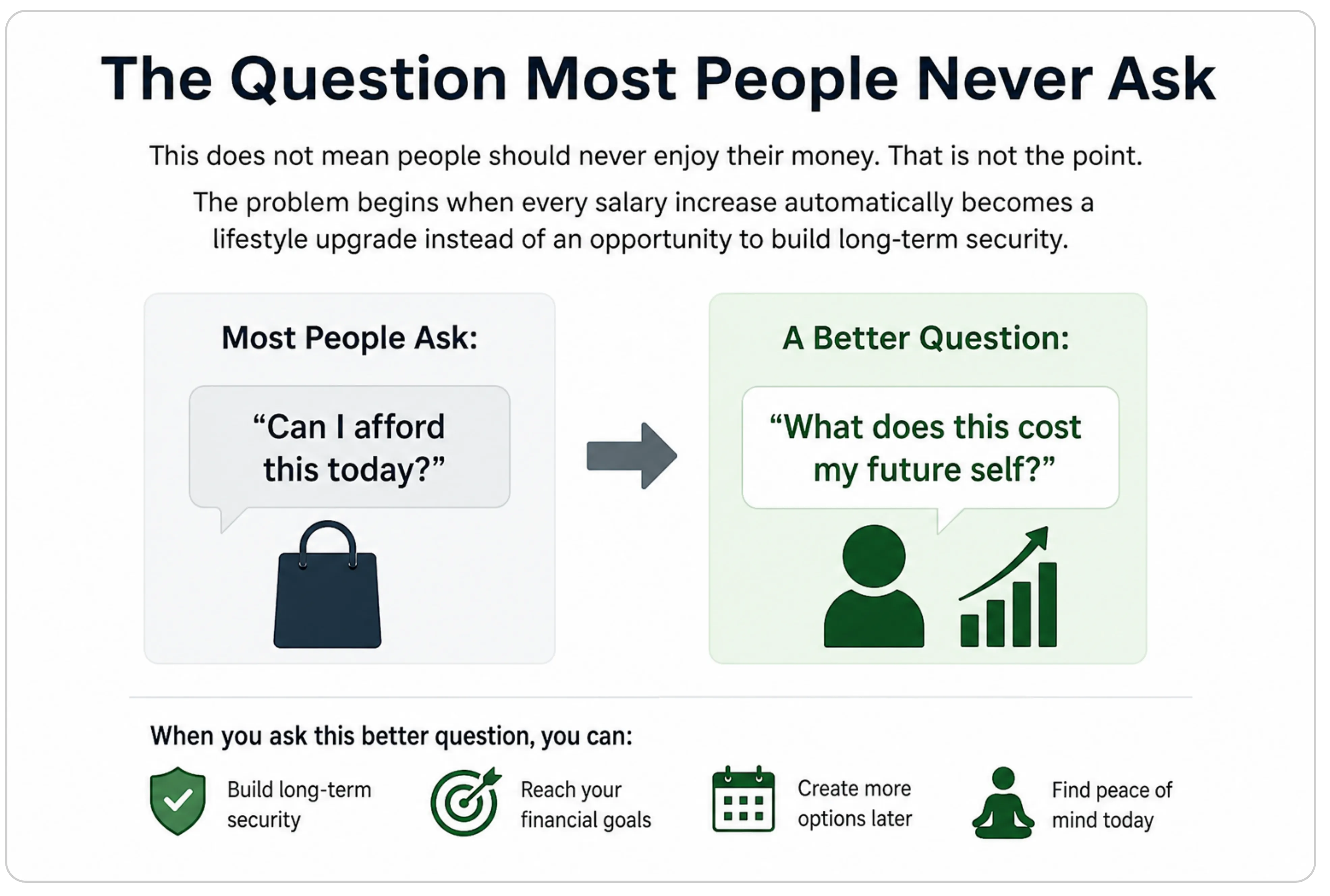

The Question Most People Never Ask

This does not mean people should never enjoy their money. That is not the point. The problem begins when every salary increase automatically becomes a lifestyle upgrade instead of an opportunity to build long-term security.

A useful question is not “Can I afford this today?”

It is “What does this cost my future self?”

That extra ₹20,000 spent every month may not feel life-changing today. But over 20 years, invested consistently, it can become the difference between working by choice and working because you have no option.

Before dismissing lifestyle inflation as someone else’s problem, it helps to pause and ask a few uncomfortable questions.

When your income increased last time, did your investments increase first or your expenses?

Do you feel richer today than you did three years ago despite earning more?

If your salary stopped for six months, how much of your current lifestyle could you realistically maintain?

If even one of these questions makes you uncomfortable, lifestyle inflation may already be shaping your financial decisions quietly.

More Income Should Create Freedom, Not Pressure

Lifestyle inflation does not usually arrive as one bad financial decision. It arrives as small upgrades that slowly become permanent expectations. The danger is not that people earn more and spend more. The danger is when higher income stops creating freedom and only creates a more expensive routine to maintain.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.