Managing personal finance isn’t just about earning and saving, it is also about borrowing wisely. While loans can help you achieve goals like buying a home or funding education, they can also drag you into a debt trap if misused. In a recent discussion with industry veterans, some key insights emerged on how Indians manage debt, financial mistakes in India, and what every investor should know about financial planning.

Why do people go wrong with loans?

One of the most common mistakes people make is borrowing without a clear need or repayment plan. Easy access to personal loans and 0% EMI schemes often tempts consumers to upgrade lifestyles rather than assets. While these loans look harmless, they eat into your future cash flow, leaving little room for savings and investments.

Rule of thumb! Never let your EMIs exceed 28–30% of your monthly income. If you are earning ₹1,00,000 per month, the combined EMIs for all your loans should not exceed ₹30,000.

These are classic examples of bad borrowing habits that slowly push people into long-term debt.

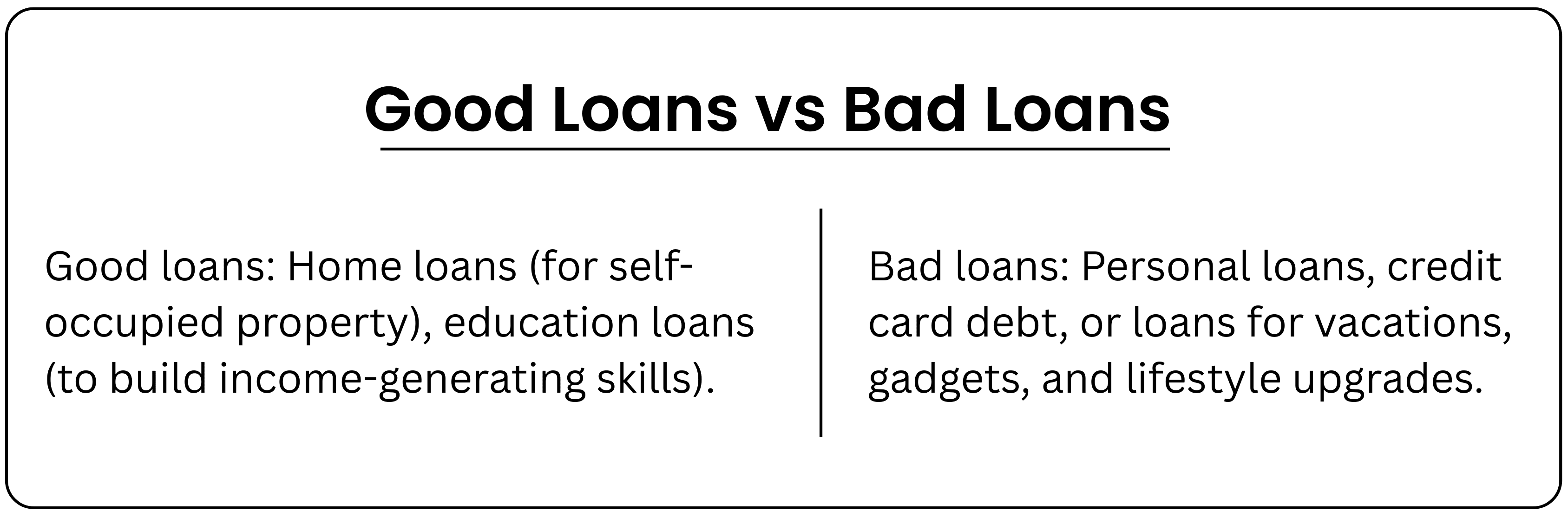

Good loans vs bad loans

Even with good loans, timing is critical. Buying a house right out of college is rarely a wise move. Many analysts suggest that you wait until you are financially stable (typically 35–40 years old), settled in a city, and have at least one-third of the property value as a down payment.

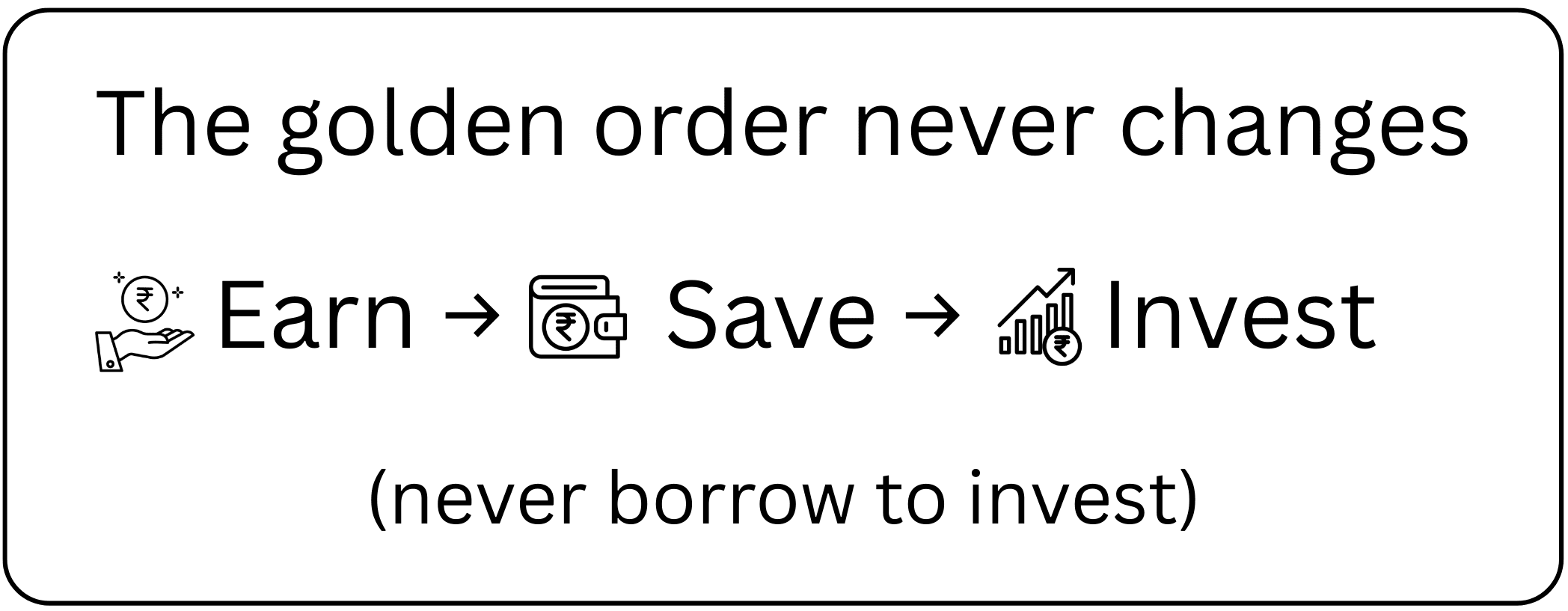

Why borrowing to invest is a recipe for disaster

One big mistake people make is that they borrow money to invest in stocks or real estate. This is risky because markets fluctuate, but EMIs don’t. A prolonged downturn can wipe out your capital while the loan liability remains.

The EMI trap

An amazing EMI option may seem tempting, but it can lead you to purchase things you don’t need. The same goes for credit cards. The biggest danger is the credit card debt trap, especially the minimum due credit card India option, where you pay only 5% and roll over the rest. This can cost you 36–40% annually in interest, turning a ₹20,000 expense into ₹24,000 in just a few months.

Easy EMIs often tempt people to upgrade phones, cars, or vacations they don’t really need. This is classic lifestyle inflation, the silent creep where your spending grows with your income, but savings don’t. Want to know more about lifestyle inflation? Click here

Be Smart: Buy only what you can afford in full and pay your credit card dues completely every month.

Mistakes that hurt wealth creation

- Keeping large sums idle in savings accounts (earning just 3–4% post-tax, which is below inflation).

- Putting all surplus into real estate locks liquidity and earns low returns (often below inflation).

- Trying to time the market instead of staying invested for the long term.

Loan myths

| Loan myths | The Facts |

|---|---|

| A 0% EMI scheme means free borrowing. | Most 0% EMIs come with hidden charges like processing fees or inflated product prices. It often leads to unnecessary spending. |

| Paying the minimum due on credit cards keeps you debt-free. | Minimum payments only postpone the liability. The remaining balance attracts 36–40% annual interest. |

| Home loans are always good debt. | They are productive only if taken at the right stage of life, with stable income and a sufficient down payment. |

| Borrowing to invest in stocks will multiply wealth faster. | Risky move. Market returns are uncertain, but EMI payments are fixed. A downturn can trap you in debt. |

| Personal loans are harmless since they are unsecured. | Personal loan mistakes often arise when they are used for lifestyle expenses. Unsecured loans carry high interest rates and can quickly spiral into a debt trap if used for lifestyle spending. |

| Having multiple credit cards improves financial flexibility. | Multiple cards often tempt overspending. A high credit utilization ratio can also hurt your credit score. |

How to stay out of loan & credit traps

Borrow with purpose, not emotion

Ask yourself: Is this loan helping me build an asset or just funding a lifestyle choice? If it’s the latter, avoid it.

Stick to the 30% rule

Never let your EMIs go beyond 28–30% of your monthly income. This ensures you always have room for savings, investments, and emergencies.

Build an emergency fund first

Before taking any loan, make sure you have at least 6 months of expenses saved up. This acts as a cushion if income slows down.

Pay credit cards in full

Minimum due payments are a trap. Always clear the full bill every month to avoid interest charges.

Think long-term before committing

A loan is not just money today, it’s a slice of your future income. Don’t sign up unless you are confident about repaying comfortably.

Avoid falling into the trap

Managing credit responsibly is the foundation of learning how to manage debt wisely. Loans can help you achieve financial milestones, but misuse can derail your financial journey. Plan your goals, maintain an emergency fund, invest systematically (SIPs), and avoid unnecessary debt. If you are unsure, consult a financial advisor, just like you consult a doctor for your health.

To begin, start your smart investing on CubePlus and take control of your financial goals.

👉 Click here to sign up

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.