In June 2025, retail inflation in India touched a six-year low of 2.1%. On the surface, that’s welcome news. But even in times when prices in the wider economy look stable, another form of inflation can quietly eat away at your finances: lifestyle inflation.

What is lifestyle inflation?

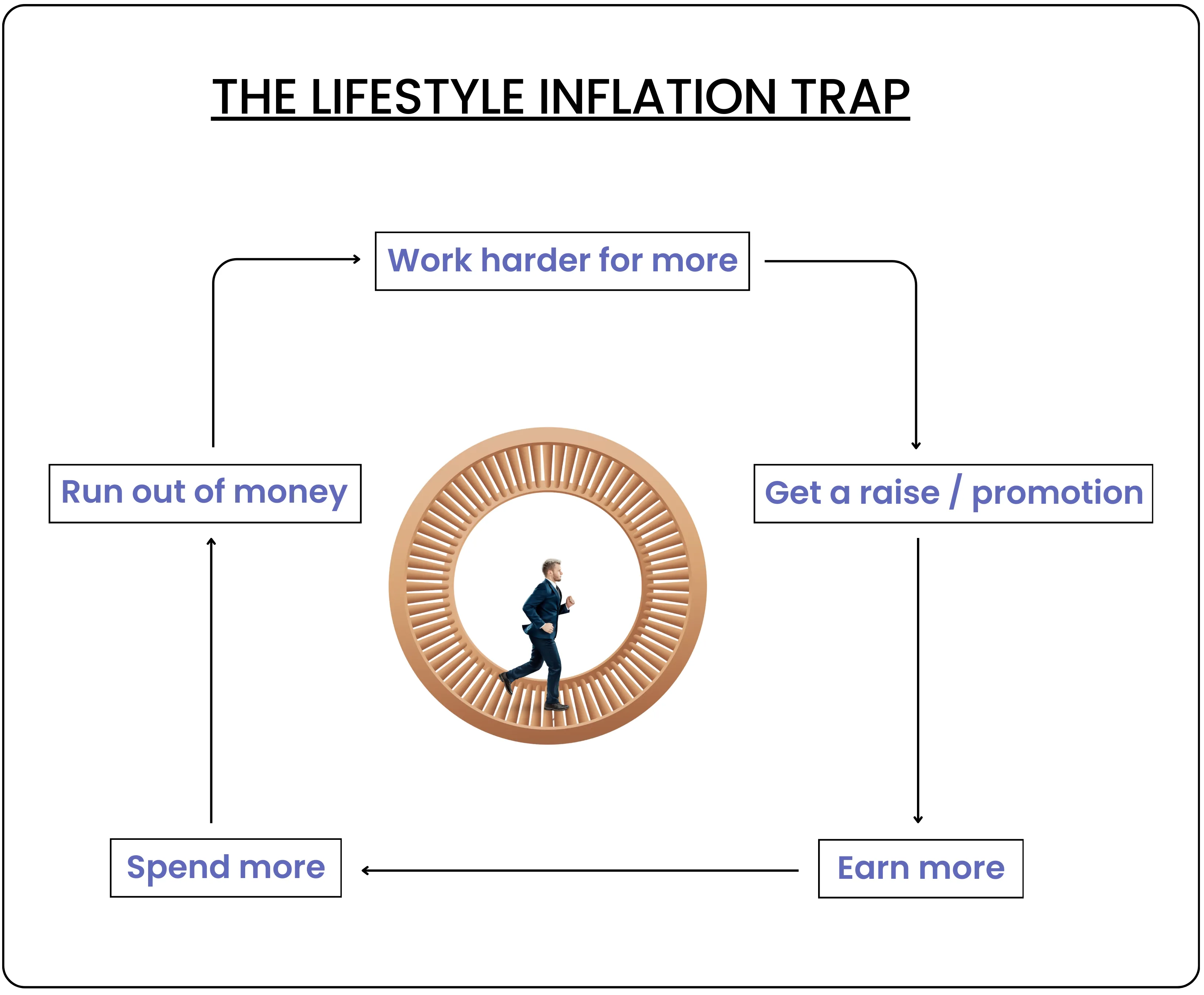

Lifestyle inflation occurs when your spending steadily rises in line with your income. It’s subtle, almost deceptive. You get a salary hike, or perhaps a bonus, and instead of channeling that money into savings or investments, you upgrade your life, maybe it’s a bigger apartment, a better car, or a fancier vacation. The new standard quickly becomes the baseline, and before long, the extra income that once felt like freedom vanishes into routine expenses.

Consider this example. If your monthly salary jumps from ₹1 lakh to ₹1.1 lakh, the additional ₹10,000 could strengthen your savings, chip away at loans, or boost your retirement fund. But if you decide to finance a bigger house, take a lavish holiday, or buy gadgets on EMI, you will likely end up spending far more than the extra income. The gain turns into a liability.

The danger lies in how quietly this shift unfolds. Over time, higher expenses can expose you to a debt trap. Many people rely on credit cards or personal loans to bridge the gap between aspirations and actual earnings. What starts as ‘just one swipe’ can snowball into a cycle of revolving debt, where the minimum due never seems to end. Others fall into what’s often called the ‘Keeping up with the Joneses’ syndrome, upgrades motivated less by need and more by comparison with peers, friends, or colleagues.

A useful way to check if you are sliding into lifestyle inflation is to look at your debt-to-income ratio. Ideally, your monthly debt obligations should not exceed 40–50% of your income. Beyond this point, financial stress is almost inevitable.

Also Read: Cost Inflation Index Simplified for Smarter Tax Saving

Here’s a simple comparison:

| Scenario | Outcome |

|---|---|

| Salary increases by ₹10,000, expenses remain unchanged |

Extra savings or investment |

| Salary increases by ₹10,000, lifestyle upgrades by ₹15,000 |

Debt burden, reduced savings |

The real cost of lifestyle inflation is not just the strain on monthly budgets but the long-term setback it causes. Funds that could have grown into a retirement corpus or secured a child’s education get diverted toward discretionary spending. Over years, this compounds into a shortfall that forces people to either delay goals or make difficult compromises.

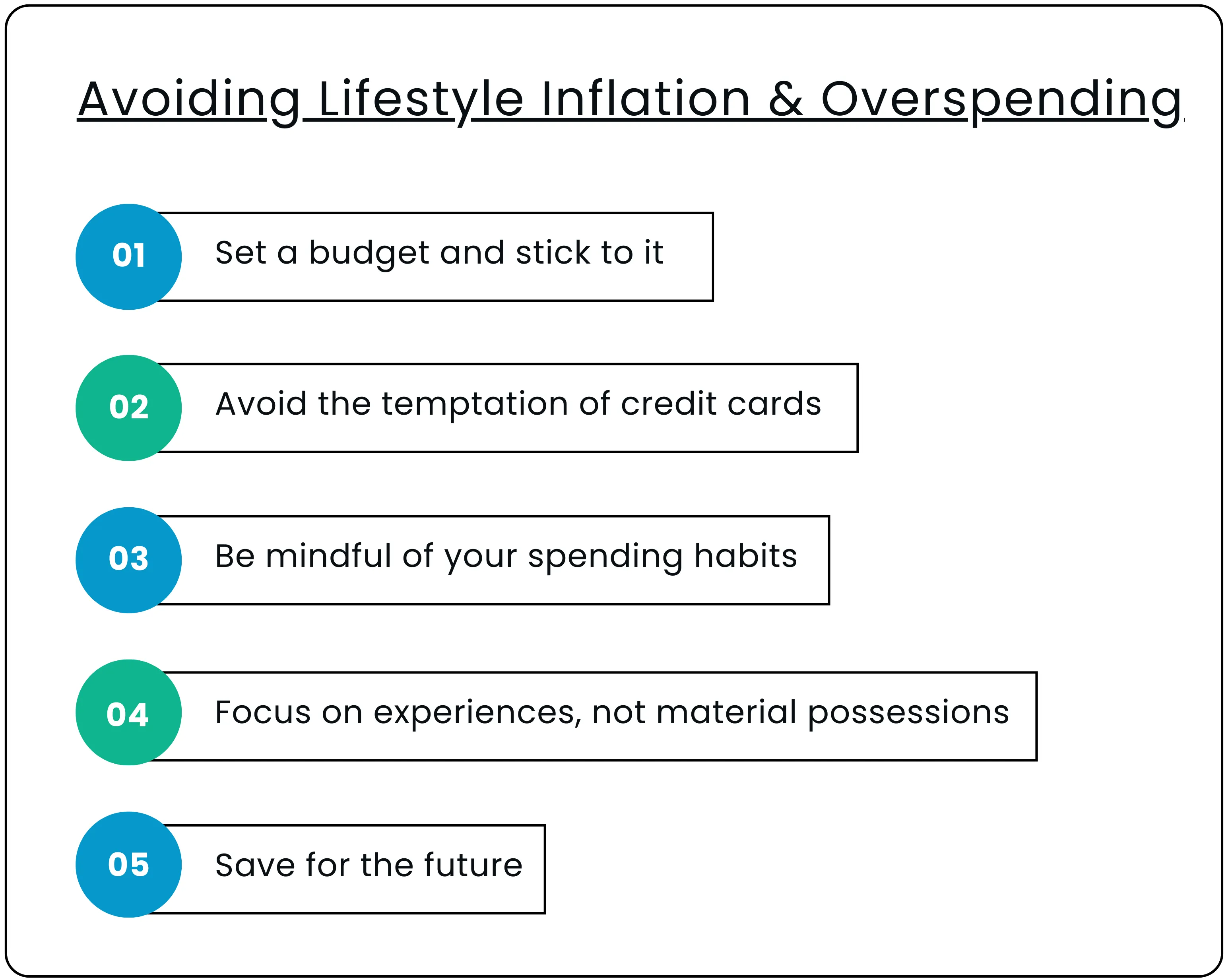

This doesn’t mean you shouldn’t enjoy the fruits of your hard work. The occasional upgrade or indulgence is natural and even healthy. The key is balance. Channeling a portion of every income increase into savings before adjusting your lifestyle can help preserve financial stability. For instance, if your pay rises by 10%, earmark at least half of that increment for investments. The remaining half can comfortably fund lifestyle upgrades without derailing your financial plan.

Lifestyle inflation isn’t a headline-grabbing economic statistic like CPI or WPI. It’s far more personal, creeping into daily choices and habits. But for that very reason, it demands attention. Recognizing its signs early, rising credit card balances, constant EMIs, or a savings account that never grows despite higher pay, can help you pull back before it’s too late.

Because at the end of the day, true financial progress isn’t just about earning more. It’s about keeping more and using it wisely. The best way to begin is by putting your money to work through disciplined investing. Start with mutual funds and learn how to do it step by step in our user guide linked below.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.