For most Indians, Diwali is not just about diyas and sweets. It’s also the time when online carts overflow, credit cards heat up, and wishlists finally come alive. From gold and gadgets to home decor and gifting, festive spending peaks every year. But amid the celebrations, one area where many go wrong is taxes. Not all expenses that glitter during Diwali can earn you tax relief, and knowing the difference can help you save both money and trouble later.

When Diwali Shopping Doesn’t Count for Tax Benefits

Every year, people try to justify festive spending as an ‘investment.’ A new laptop? ‘It’s for work.’ Gold jewellery? ‘It’s a long-term asset.’ But the truth is, simple personal purchases, no matter how necessary they feel, do not qualify for tax deductions on Diwali shopping.

Under Indian tax rules, only those expenses that have a direct business or professional purpose can be claimed. A new phone bought for personal use or a washing machine for your home doesn’t count.

However, if you run a business and buy hampers for clients or employees, that’s different it may be eligible under Section 37(1) as a legitimate business expense. The catch? You must have proper documentation, bills, payment proofs, and a clear business reason.

For example:

- A small bakery owner who gifts festive hampers to regular customers and staff, maintaining all invoices, can claim these as business expenses.

- But a salaried employee who buys gold coins for relatives and calls it an investment expense will find no such relief during tax filing.

Who Can Actually Claim Deductions

The eligibility depends on your income type and nature of work:

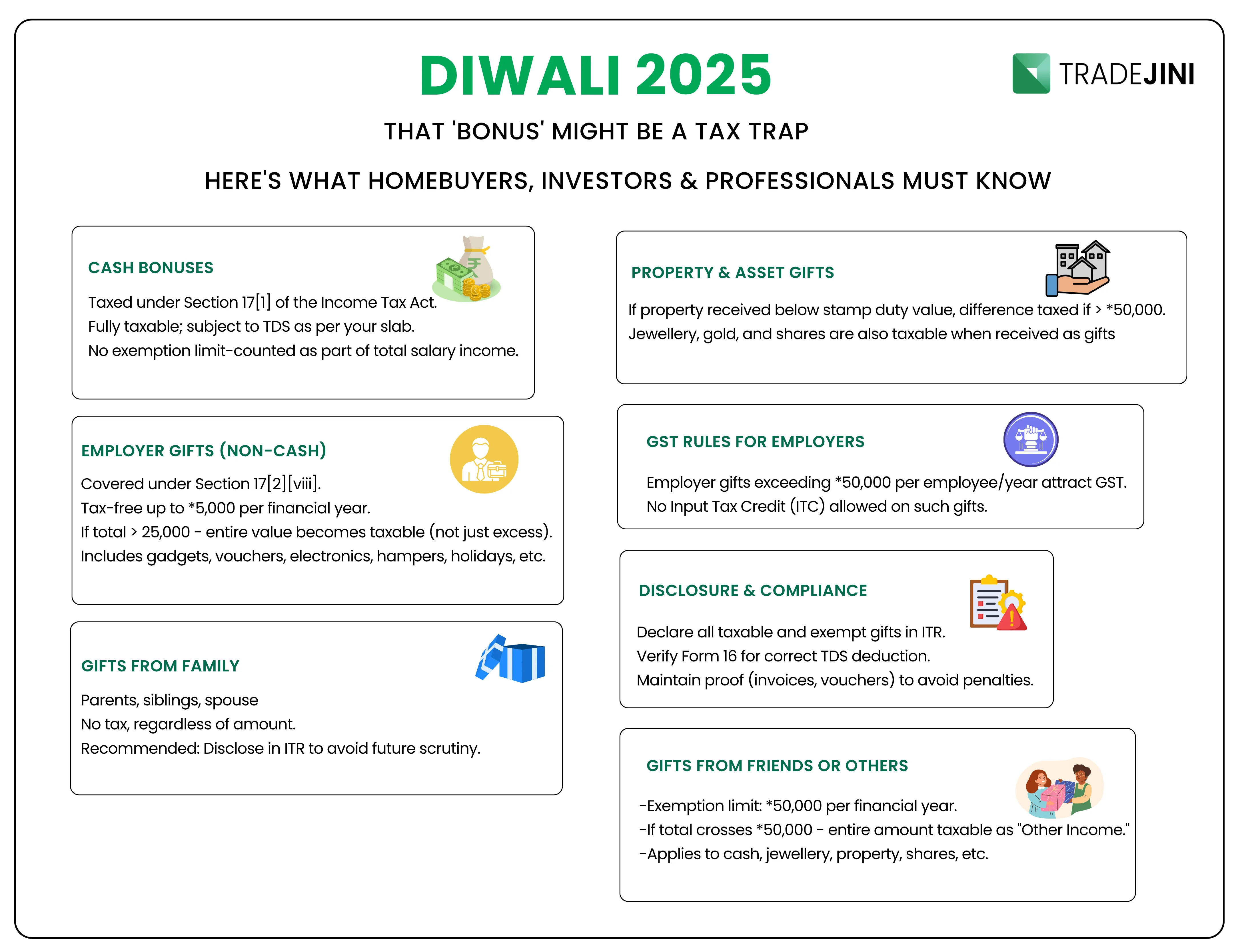

Salaried employees Diwali tax: There’s almost no scope for deductions on festive spending. Employer-given gifts up to ₹5,000 a year are tax-free, anything above that becomes taxable income. (This is the tax-free employee gifts limit you can keep in mind.)

Self-employed professionals: Can claim business-related festive expenses (like client gifts or small events) if they are reasonable and well-documented.

Businesses: Expenses on bonuses, staff celebrations, and client hampers are allowed as business deductions if they are incurred wholly and exclusively for business purposes and proper records are maintained. For employees, such payments or gifts fall under Section 192 (salary and perquisites). However, for clients, dealers, or business partners, if the total value of gifts or benefits exceeds ₹20,000 per recipient in a financial year, TDS at 10% must be deducted under Section 194R.

So, while personal joy is priceless, it’s rarely tax-deductible.

Get ready to trade with luck, because Muhurat Trading 2025 is almost here 👇

Essential Guide to Muhurat Trading 2025: Dates, Timings, and Benefits

When Emotions Take Over Logic

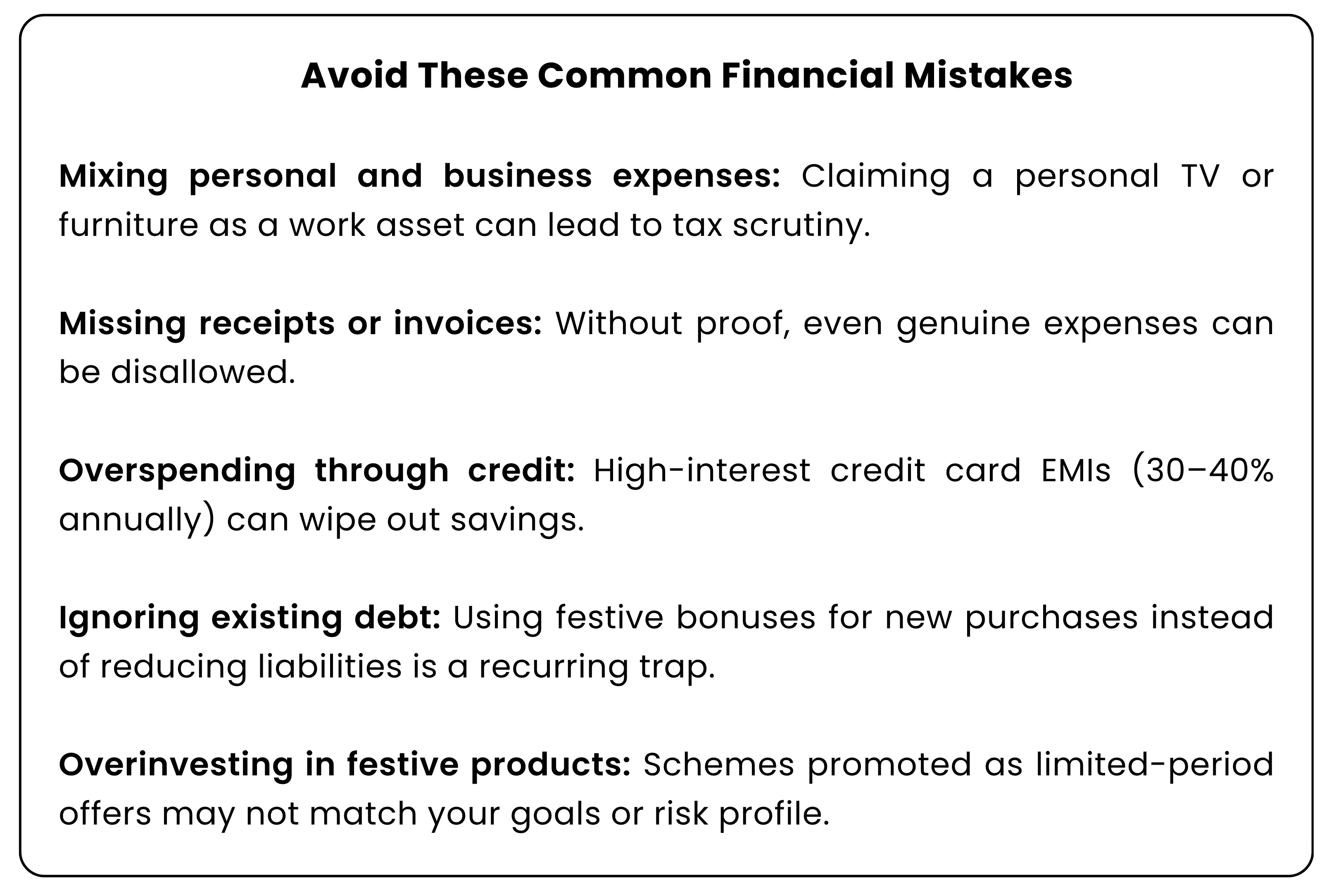

Diwali bonuses, festive offers, and the ‘once-a-year’ mood often led to decisions that strain future finances. Many families treat bonuses as free money, splurging on luxury phones, designer clothes, or impulse online purchases. The realization usually arrives a month later, with a credit card bill and an empty bank account.

Then there’s the lure of ‘zero-cost EMIs’ and cashback schemes, which often come with hidden costs or lock-ins. A refrigerator bought under an EMI plan might cost more in the long run once processing fees, GST, and opportunity costs are added.

The mistake isn’t spending it without a plan.

Consider two households:

- Family A uses part of their Diwali bonus to pay off an old loan and continue their SIPs.

- Family B spends the entire amount on gold, a new TV, and festival shopping.

Six months later, Family A has reduced debt and continued wealth growth. Family B is still paying EMIs for last year’s celebrations.

What to Take and What to Leave?

Banks, brokers, and mutual funds roll out tempting offers during Diwali higher FD rates, processing fee waivers, cashback, or ‘festival-special’ mutual fund NFOs. These look attractive but rarely change the fundamentals.

A 0.25% bump in fixed deposit returns, for instance, isn’t a game changer. It may make sense only if liquidity, tenure, and your cash flow align. Similarly, some credit card deals may offer vouchers or reward points, but only if you pay off dues promptly.

However, real value can sometimes be found in larger financial decisions for instance, homebuyers may benefit from subvention schemes, reduced processing fees, or developer discounts during this period. Such tie-ups can genuinely improve affordability compared to cosmetic offers on short-term products.

The golden rule: read the fine print, not just the festive headlines

The idea isn’t to stop celebrating, it’s to celebrate responsibly.

Plan First, Spend Next

One of the simplest ways to enjoy the festive season guilt-free is to plan ahead. Setting aside ₹5,000–₹6,000 a month from April can build a fund of ₹35,000–₹40,000 by Diwali, enough for shopping, gifting, and small upgrades without touching your long-term savings.

Here’s a simple festive financial planning India template for someone earning ₹70,000 a month and expecting a ₹50,000 bonus:

| Category | Monthly Amount (₹) | % of Income |

|---|---|---|

| Rent & EMIs | 45,000 | 65% |

| Investments (SIP, PF, etc.) | 15,000–20,000 | 25–30% |

| Lifestyle & Utilities | 10,000 | 15% |

| Festive Fund | 5,000 | 7% (set aside each month) |

| Bonus allocation | — | 40% shopping, 40% investments, 20% savings buffer |

By planning this way, celebrations remain bright not burdensome.

The Diwali Mantra, ‘Joy with Judgement’

Festivals should bring happiness, not stress. Whether you’re lighting diyas or planning an IPO application, balance emotion with logic. Keep track of receipts if you’re a business owner, continue your SIPs even during the festive rush, and avoid equating zero-interest with zero cost.

The essence of Diwali lies in the renewal of relationships, energy, and habits.

So, while you illuminate your home, remember to light up your financial discipline too.

Step into the new financial year, Samvat 2082, with smart investments and bright beginnings. Start your journey with CubePlus by Tradejini today and let your portfolio shine as bright as your Diwali diyas!

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.