Options are unlike any other financial instrument because they expire. This single characteristic makes time a trader’s constant companion- and often the biggest source of profit or loss. The metric that captures the effect of time on options is Theta, also called the “time decay” Greek. Theta tells us how much value an option is expected to lose for each passing day, assuming all other variables remain unchanged. While Vega responds to volatility shocks and Delta tracks directional exposure, Theta steadily ticks away in the background, quietly eroding premium values. For sellers, Theta is income: for buyers, it is an unavoidable cost. The challenge lies in managing this decay effectively.

Also Read: The Trader’s Playbook for Using Vega Effectively

Understanding Option Theta

| Concept | Details |

|---|---|

| Definition | Theta measures the change in an option’s price for the passage of one day, with no change in underlying factors. |

| Numerical Example | A Theta of -5 means the option will lose ₹5 of its value each day, all else being equal. |

| Sign Convention | Negative for option buyers (they lose value as time passes). Positive for option sellers (they collect this decay). |

| Simple Rule | Buyers pay Theta. Sellers earn Theta. |

| Decay Pattern | Not uniform across strikes or maturities - Accelerates as expiry approaches - Strongest impact on at-the-money (ATM) options - Interacts dynamically with volatility |

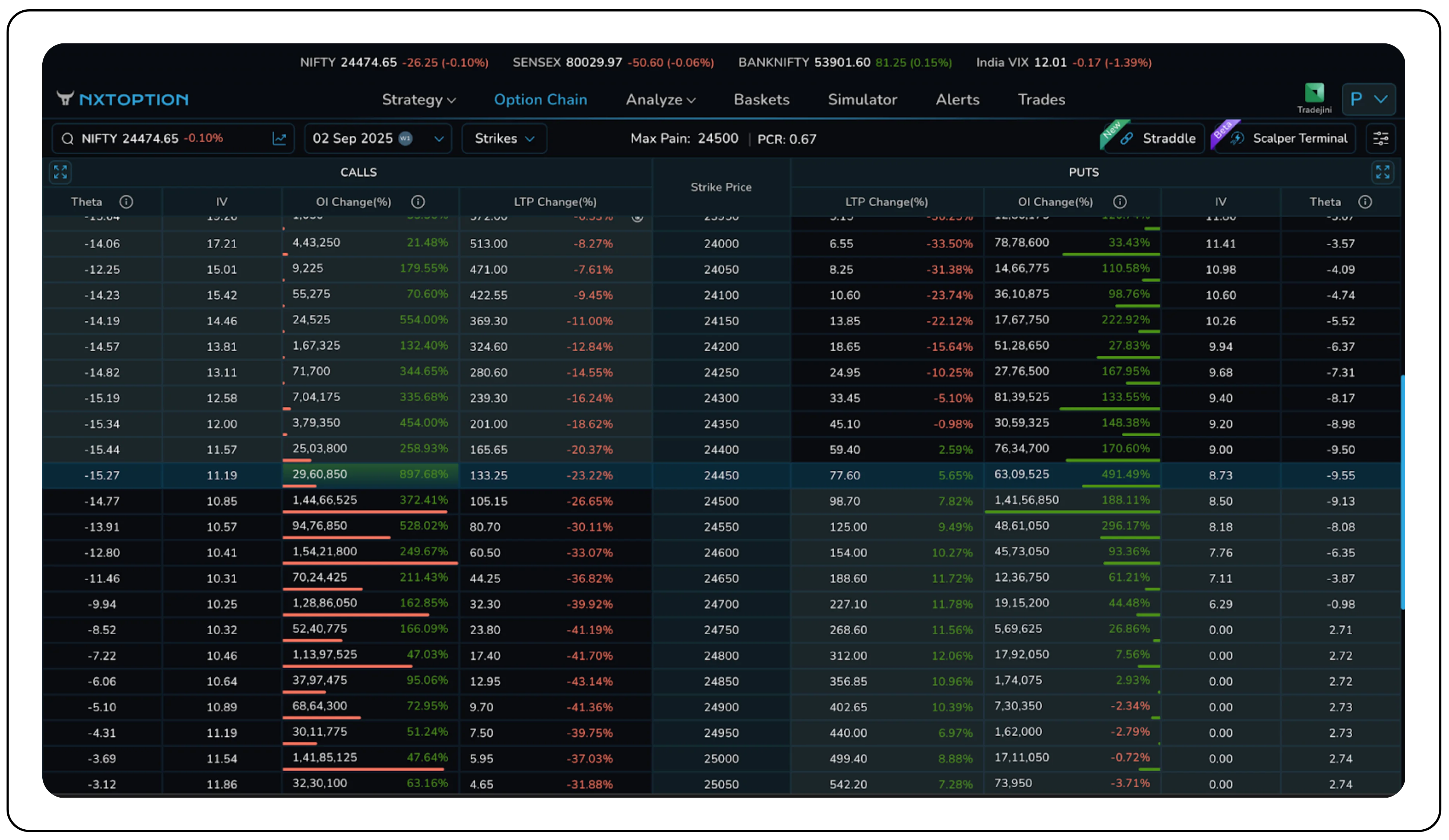

An Example with Live Chain Data

As of 29 August 2025, NIFTY is trading around 24,475. Looking at the option chain for the 02 September 2025 expiry, the following strikes illustrate how Theta plays out in practice:

ATM Call (24,450 CE): * Premium (LTP) = ₹133.25 * Theta = -15.27 OTM Call (25,000 CE): * Premium (LTP) = ₹5.95 * Theta = -3.69 ITM Call (24,000 CE): * Premium (LTP) = ₹513.00 * Theta = -14.06

The ATM option is losing ₹15 per day, assuming the underlying remains flat. That’s more than 10% of its premium vanishing every day. The OTM option is only losing about ₹3.70 per day, but since its premium is less than ₹6, the decay can wipe out its entire value within two days. The ITM option still loses about ₹14 per day; however, since most of its value is intrinsic, the proportional impact is smaller compared to ATM.

Notice that ATM options have the steepest daily decay. Buyers often underestimate how costly this can be when holding positions through expiry week. Sellers, on the other hand, specifically target these high-decay zones to maximize income.

Moneyness and Theta

Theta does not act in isolation; its magnitude is closely linked to moneyness, or the relative position of the option’s strike price compared to the underlying asset’s market price. Traders studying decay patterns often find that the relationship between moneyness and theta resembles a bell curve. At-the-money (ATM) contracts sit at the peak of this curve, while in-the-money (ITM) and out-of-the-money (OTM) contracts taper off on either side.

- At-the-money (ATM): The Fastest Burn ATM options experience the highest rate of time decay. This is because they are made up almost entirely of time value rather than intrinsic value. As expiry approaches, this time value evaporates rapidly. In the option chain, the call option with a strike of 24,450, trading close to spot at 24,475. In expiry week, its premium stands at ₹133.25 with a theta close to -15.27. This means the option loses roughly 11% of its entire value every single day, a steep erosion. This happens because the market is constantly reassessing whether the option will expire ITM or not. With limited time left, the probability window narrows sharply, and thus, the premium has no choice but to collapse.

- Out-of-the-money (OTM): Slow, Then Sudden OTM options carry lower theta compared to ATM, but their decay is a little deceptive. Early in the expiry cycle, OTM premiums appear to hold “value” as traders speculate on potential moves. However, as expiry nears, these premiums can collapse overnight because there is no intrinsic value to cushion them. In the option chain, the call option with a strike of 25,000 with the same spot as before is priced at ₹5.95 but has a theta of -3.69, which means that the option will lose the entirety of its value within two days. For OTM options, the risk is not gradual erosion but the cliff-like fall in the final hours of trade.

- In-the-Money (ITM): Protected but Not Immune ITM options exhibit moderate theta, as a significant portion of their premium comes from intrinsic value, which is not subject to time decay. Still, the time value component present in ITM contracts steadily erodes, though less dramatically than ATM options. In the chain, the call option with a strike of 24,000 with the spot at the same price has a premium of ₹513.00 and holds a theta of -14.06. Out of this premium, ₹475 is the intrinsic value, and only ₹38 is the time value. With its theta, it might only lose ₹14.06 daily, but most of its worth remains stable due to the intrinsic value. ITM options are “safer” from rapid decay, but traders should remember that a higher upfront cost ties up more capital

Volatility and Theta

Volatility exerts a powerful influence on Theta. Since Theta measures the daily erosion of an option’s time value, the absolute size of this decay is closely linked to the premium level. Implied volatility (IV), which represents the market’s expectation of future price fluctuations, inflates or deflates premiums accordingly.

1. In High IV Environment

When IV rises, option premiums become more expensive because traders expect bigger swings. This larger “time value cushion” means that the absolute Theta in rupee terms is higher. In practical terms, more money is lost each passing day as decay eats into the bloated premium. On a day when NIFTY’s IV jumped above 18%, the ATM 24,450 CE was priced around ₹133.25 and had a theta of -15.27. This meant every single trading day, the option holder loses over ₹15.27 per lot per unit just to the passage of time - roughly ₹1145.25 per day (since NIFTY contracts come in a bundle of 75 per lot). For a buyer, this is a steep daily cost.

2. In Low IV Environment

Conversely, when IV contracts, premiums shrink. Because there is less “time fluff” in the option’s price, the absolute Theta is smaller and the daily erosion, while still present, is gentler. When IV dips near 9%, the same ATM 24,450 CE trades closer to ₹70, with Theta around -8. This results in a daily loss is about ₹600 per lot, a little more than half the burn observed in a high-IV environment.

This interplay creates important timing considerations. Selling options in high-IV environments not only fetches higher premiums but also accelerates Theta decay in absolute terms. Conversely, buying options when IV is high is doubly risky, as premiums are elevated and decay is faster.

Time and Theta

One of the most defining features of Theta is that it is non-linear with respect to time. Unlike linear depreciation of assets, option time decay behaves like a convex curve - slow at first, then dramatically accelerating as expiry approaches. Traders who ignore this curvature often find themselves surprised at how quickly premiums collapse in the final days.

1. Far from Expiry: Slow Decay

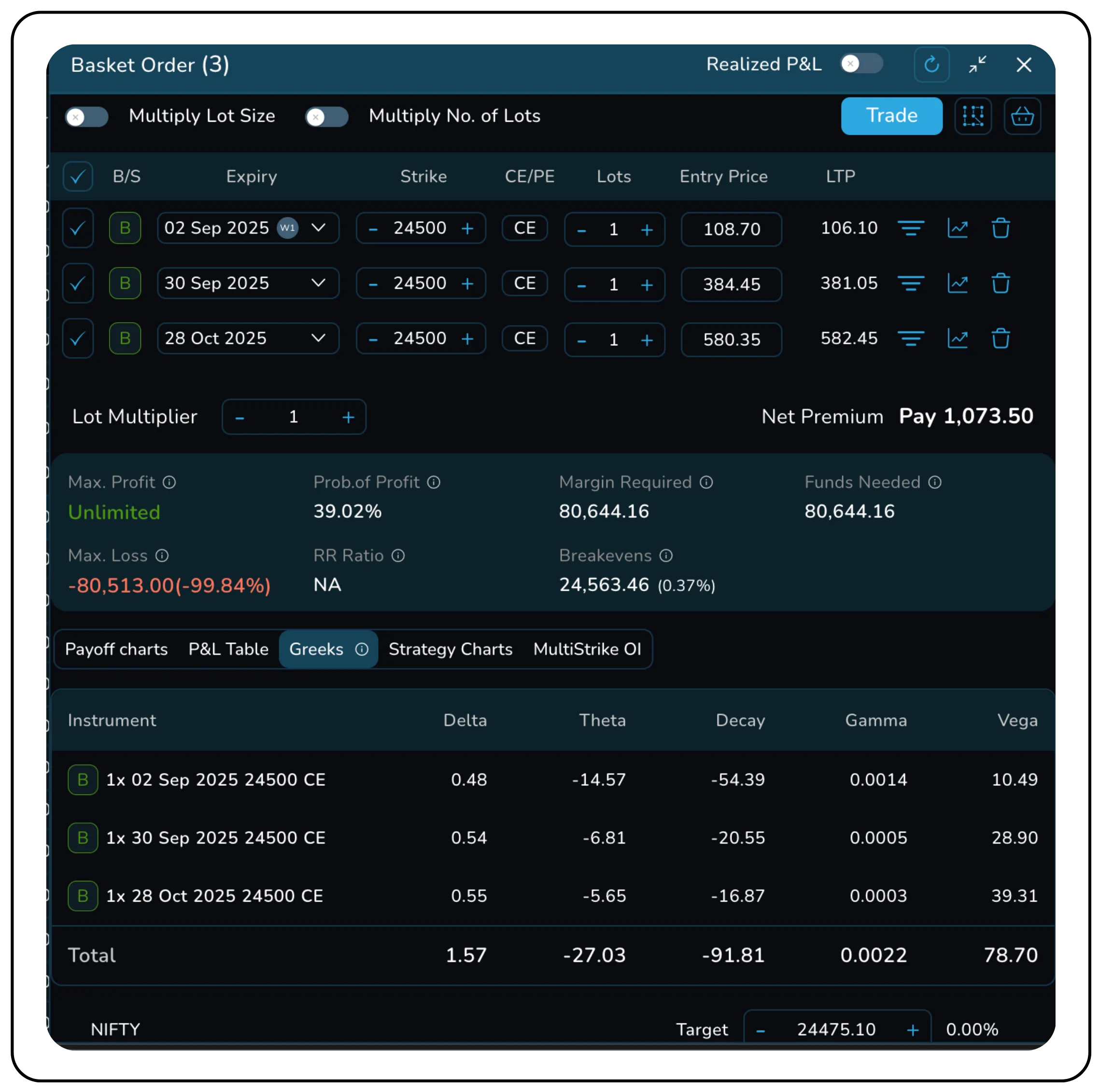

When an option still has several weeks or months left before expiry, its daily Theta is relatively small. Premiums contain significant time value, and the market is still uncertain about where the underlying might end up. As a result, option decay is steady but not alarming. In the image above, we can see that the 28 Oct 2025 24,500 CE is priced at ₹580.35 and has a Theta of -5,65, which means each day the option loses about ₹5.65 purely to time decay. This represents less than 1% of its premium, which is a manageable erosion rate.

2. Closer to Expiry: Accelerating Decay

As the option nears expiry, uncertainty reduces, and premiums begin to lose time value at a faster rate. Theta increases in magnitude, eating away at a larger proportion of the option’s worth each day. The 30 Sept 2025 24,500 CE is priced at ₹384.45 with Theta of -6.81. Despite having a smaller premium than the October option, its Theta is larger in proportion. This means the option loses time value faster - almost ₹6.81 per day. Importantly, this represents nearly 2% daily erosion relative to premium, a sharper decay curve compared to the October expiry.

Final Days: Collapse of Premiums

The steepest part of Theta’s curve arrives in the final week, particularly the last trading sessions before expiry. At this point, the option premium is mostly time value, and with no days left, that value will converge to zero or intrinsic value, which is OTM and ITM, respectively. The 2 Sep 2025 24,500 CE is priced at ₹108.7 with Theta of -14.57. Which means that the option is losing ₹14.37 per day or nearly 13% of its entire premium daily. In practical terms, a buyer holding this option would see its price collapse within a matter of sessions unless the underlying makes a strong, favorable move.

Theta in the Trader’s Playbook

Theta is neither inherently good nor inherently bad - it is a function of perspective and position. For one trader, it may represent a daily cost that must be overcome: for another, it is a steady income stream as long as the underlying market remains quiet.

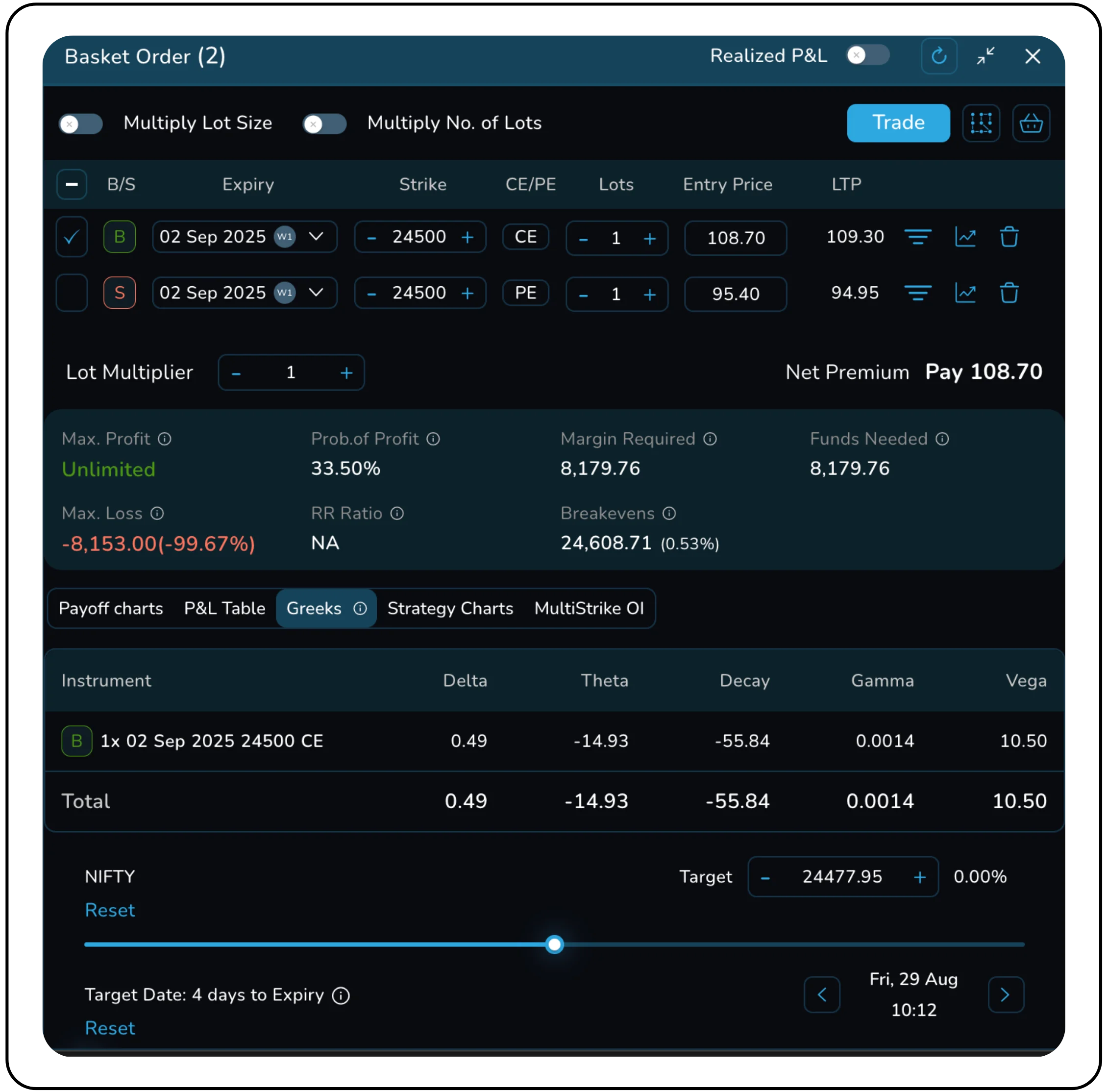

When holding long calls or puts, Theta acts as a relentless adversary. Each day that passes without a decisive move in the underlying erodes part of the premium paid, irrespective of the correctness of the directional view. A trader buys the NIFTY 24,500 CE (weekly expiry, 2 Sep 2025) for ₹108.70. The Theta associated with this position is approximately –14.93. This implies that, if the underlying remains stagnant, the option loses nearly ₹15 in value daily. Over four days, this amounts to almost ₹60 of decay, or more than 50% of the premium.

Implication:

To simply “break even,” the underlying must rise quickly enough to offset both the Theta erosion and the premium already paid. This is why outright buying of short-dated options is extremely speculative in the expiry week. The underlying must not only move in the expected direction but must do so rapidly.

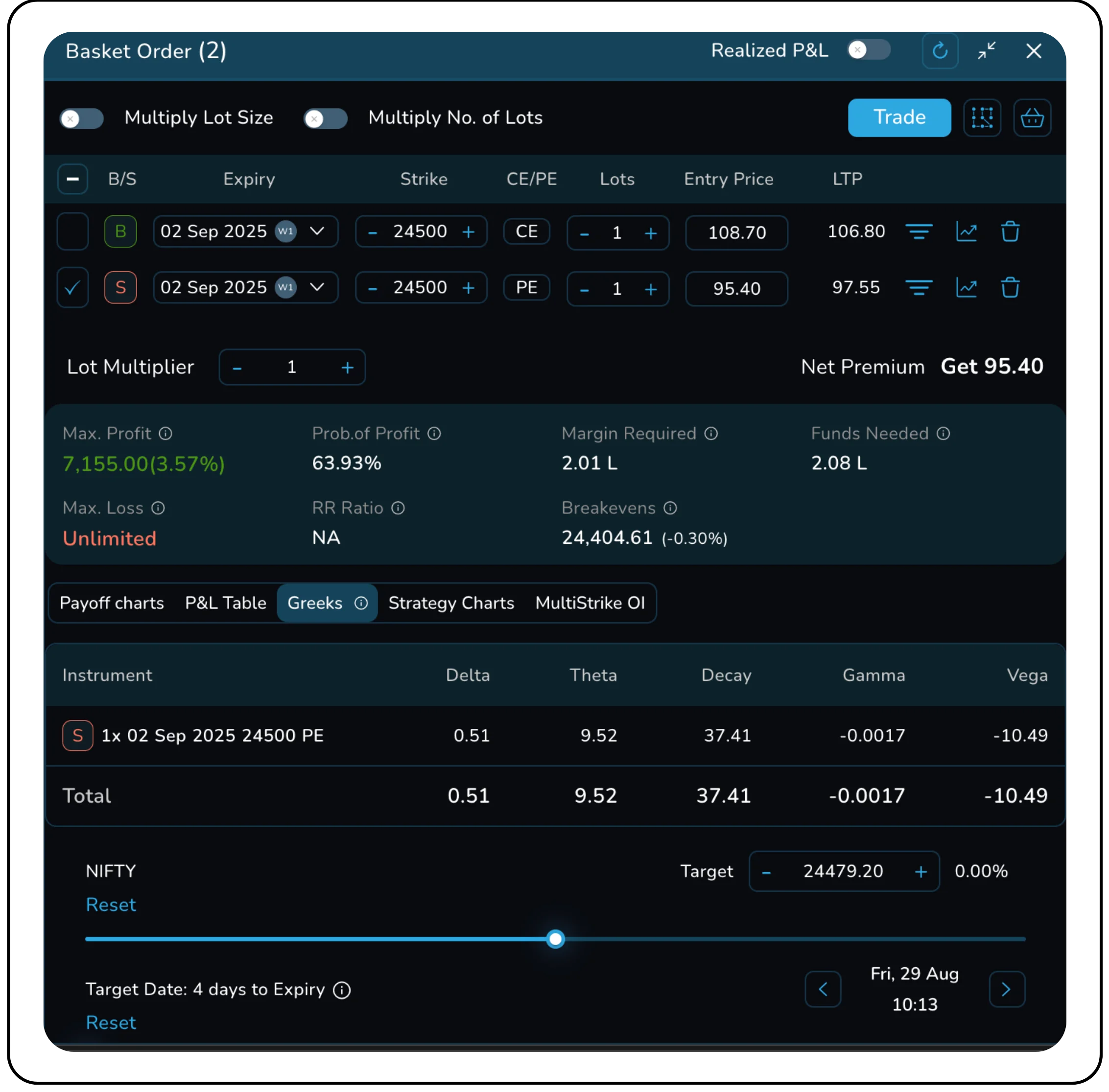

For option sellers, Theta is the equivalent of collecting rent every day the market remains in a narrow range. Every passing day without major movement works in their favor. A trader sells the NIFTY 24,500 PE (weekly expiry, 2 Sep 2025) at ₹95.40. The Theta here is +9.52, meaning the position earns close to ₹10 per day as long as prices hold steady above the strike. In four days, this could translate to nearly ₹38 per lot, adding up to ₹1,900 on a 50-lot contract.

While this steady Theta income is attractive, it is not risk-free. If NIFTY were to drop sharply below 24,500, losses from Delta exposure would quickly overwhelm Theta gains. Hence, the seller benefits most in range-bound, low-volatility markets.

The practical application of theta management lies in aligning strategy with market outlook. When anticipating significant price movement, long positions may be justified despite the theta cost. Conversely, in range-bound markets, short strategies like covered calls, cash-secured puts, or spreads allow traders to harvest theta effectively. Risk management, however, remains critical, since short positions expose traders to adverse price shocks. Thus, prudent traders balance both components: accepting theta as a calculated expense when buying optionality, or harnessing it as a structured income stream when writing options. Ultimately, disciplined theta management transforms time decay from an invisible risk into a deliberate tool for consistent performance.

In conclusion, managing theta effectively requires recoginizing its dual nature: the steady erosion of option premium that works against long positions and simultaneously benefits short positions. Traders must remain mindful that time decay accelerates as expiration approaches, making timing a decisive factor in strategy selection. For long option holders, particularly those speculating on directional moves, theta acts as a silent adversary that steadily reduces value if price movement or volatility shifts do not occur in their favor. In contrast, for short option writers, theta serves as a dependable ally, generating consistent gains as long as the market conditions remain stable.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.