India’s alcohol industry sits at a unique intersection of consumer demand, state regulation, fiscal dependence, and brand-led economics, making the Indian alcohol market one of the most complex segments within the alcoholic beverage industry. Unlike most consumer sectors, alcohol is not governed by a uniform national framework. Each state controls pricing, distribution, retail formats, and excise duties, making this an industry where profitability is shaped as much by policy as by consumer preference. Despite these complexities, the alcohol sector has demonstrated steady growth, improving margins, and a visible shift toward premiumisation across categories, reflecting favourable market dynamics.

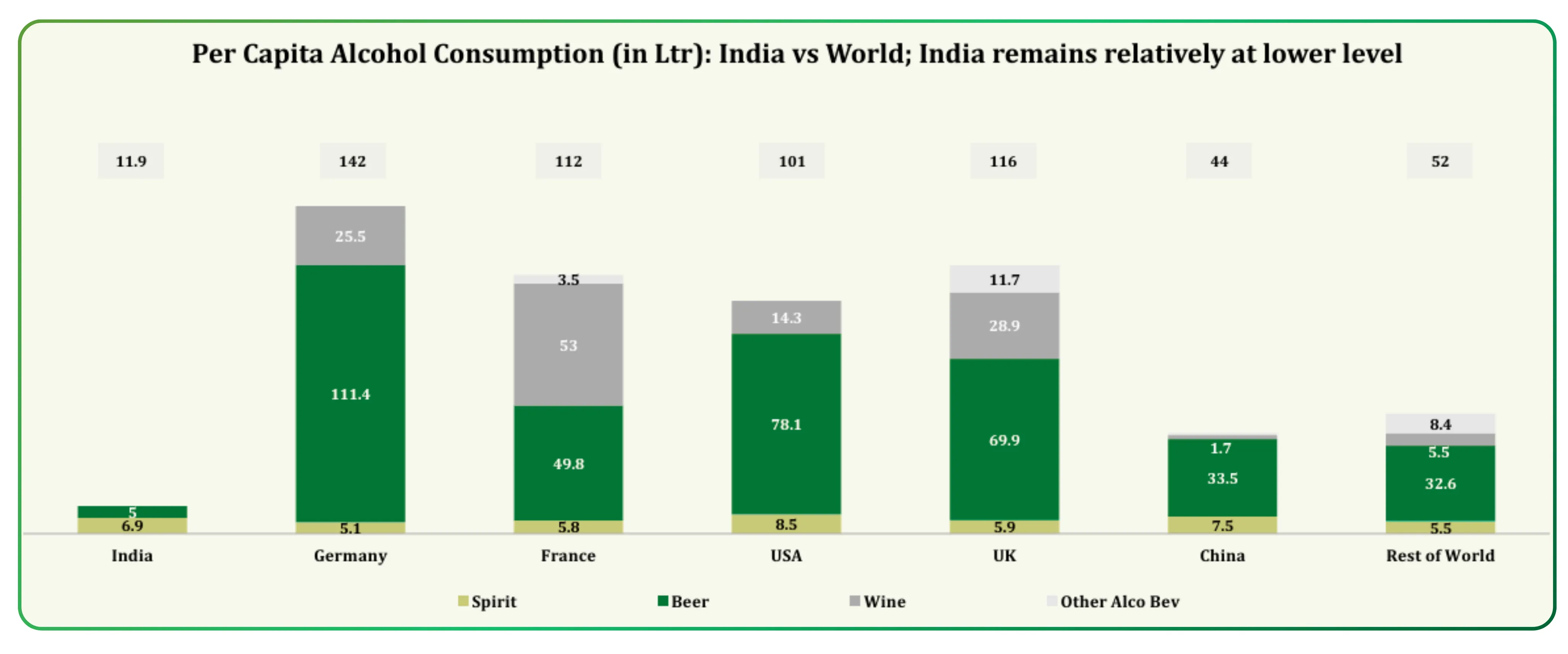

Alcohol consumption in India remains structurally underpenetrated on a per-capita basis, even though the country is already among the largest global markets by volume. This gap between absolute scale and per-capita consumption continues to create long-term headroom, particularly as incomes rise, urbanisation deepens, and social attitudes evolve.

Macro and consumption backdrop

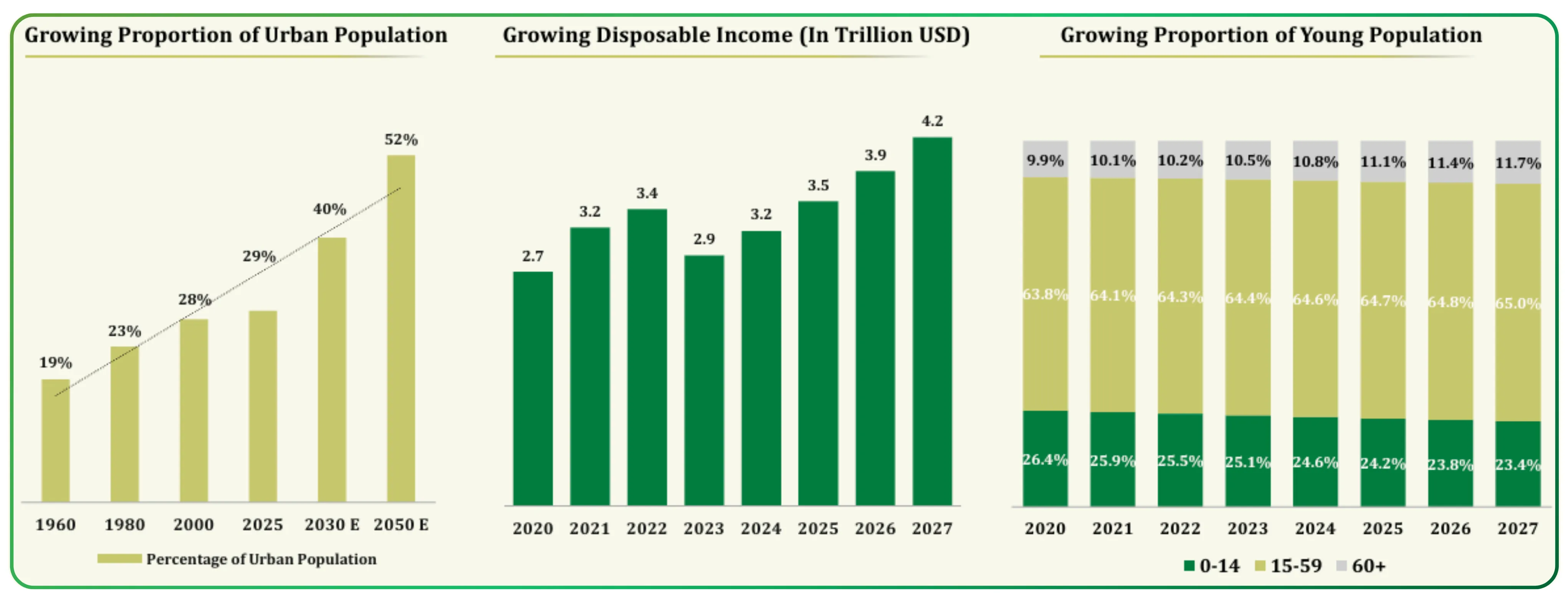

India’s macroeconomic environment has remained supportive for discretionary consumption, aided by sustained economic growth and improving income visibility. GDP growth of around 6.5% in FY25, moderate inflation near 4.6%, and steady government spending have supported consumer demand across various categories. Private consumption now accounts for more than half of India’s GDP, with discretionary spending growing faster than essentials. As per capita income crosses the US$2,000 mark, consumption patterns begin to resemble those of other emerging economies, where alcohol shifts from an occasional indulgence to a more regular, socially accepted purchase.

Alcohol companies have also pointed out that India adds roughly 15 to 20 million people to the legal drinking age population every year. This demographic pipeline, combined with rising participation of women and more gender-neutral social drinking environments, is expanding the addressable market beyond traditional consumer cohorts.

Industry structure and category mix

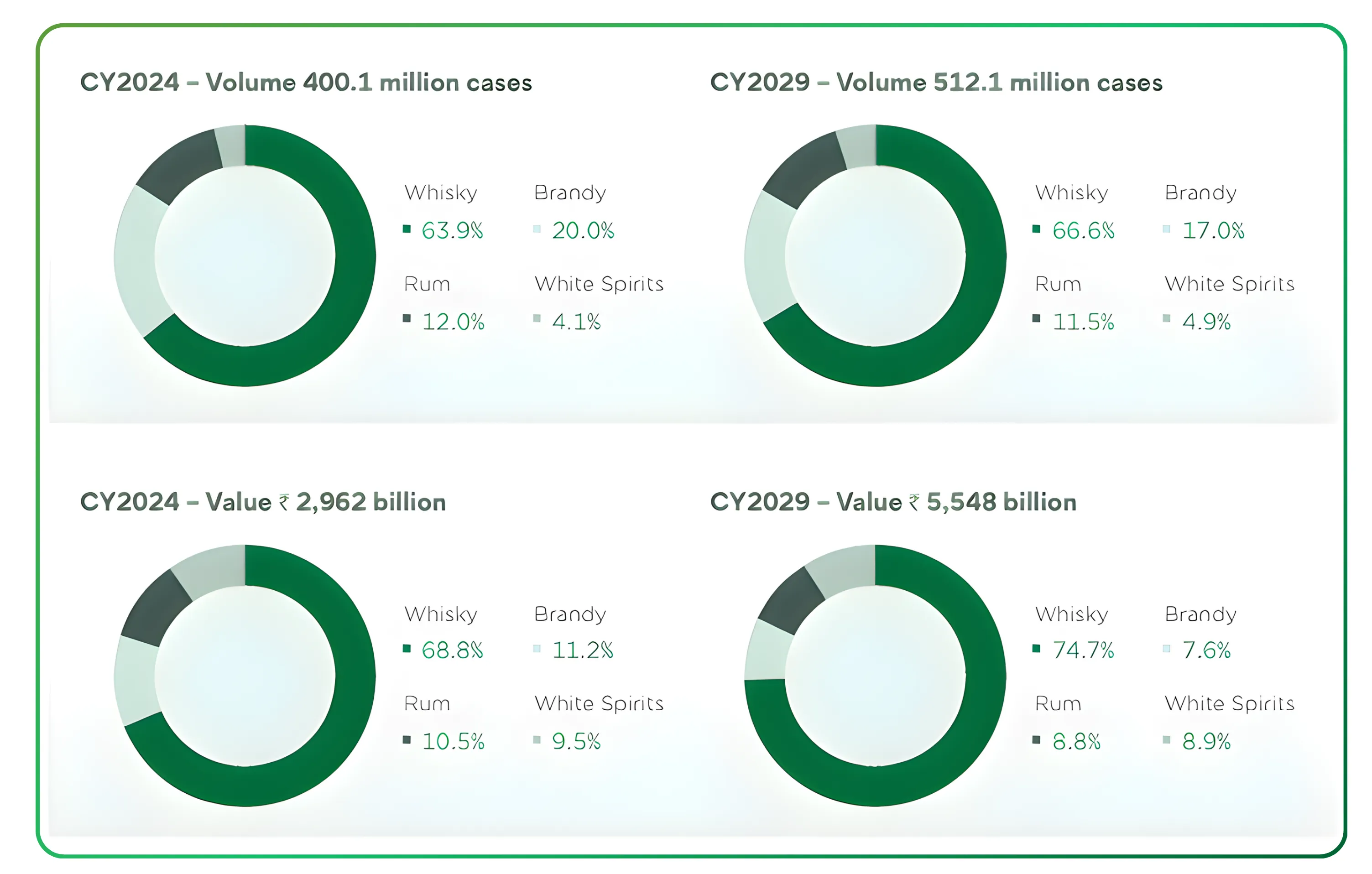

The Indian alcohol market is dominated by spirits, particularly Indian Made Foreign Liquor (IMFL), which accounts for the majority of alcohol production and industry value. Whisky remains the largest category, contributing close to two-thirds of IMFL volumes, followed by brandy, rum, and a smaller but fast-growing white spirits segment that includes vodka and gin.

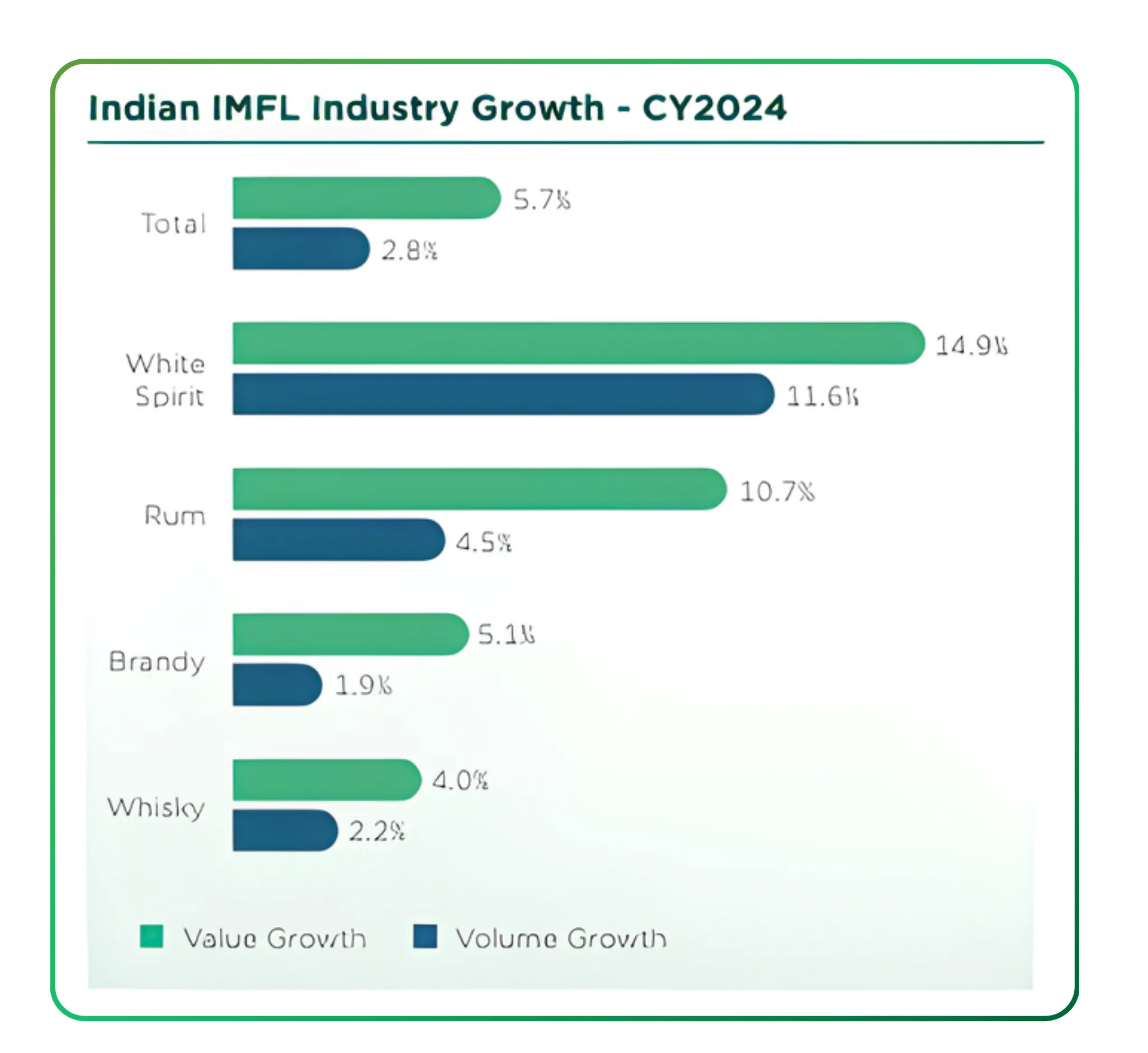

Radico Khaitan’s management highlights that the IMFL industry crossed 400 million 9-liter cases in CY2024, growing 2.8% in volume terms but 5.7% in value terms. This divergence between volume and value growth captures the most important structural trend in the industry: premiumisation. Consumers are not merely drinking more; they are increasingly drinking better.

White spirits are emerging as a standout segment. Although they represent only about 4% of Indian spirits volumes, they recorded double-digit growth in both volume and value. Vodka and gin benefit from cocktail culture, urban bar-led consumption, and growing interest among younger consumers. This is one of the most underpenetrated categories in India.

Wine remains a niche but structurally interesting segment. It accounts for less than 1% of India’s alcohol market, with per-capita consumption below 50 ml annually, compared with a global average of over 5 liters. Despite this, wine is gaining traction and is expected to grow at a much faster pace than spirits, driven by aspirational consumption, urbanisation, food pairing trends, and favourable regulatory treatment in states such as Maharashtra and Karnataka.

Read ABS Marine Anchoring Growth with Long-Term Offshore Contracts for a deep dive into a contract-driven offshore services business.

Regulatory environment and state dynamics

Alcohol remains a state subject, and this continues to be the single biggest risk and differentiator across companies in a highly fragmented market. Excise duties are a major source of revenue for state governments, which creates both dependence and unpredictability. Pricing approvals, license renewals, retail formats, and distribution structures vary sharply across states and can change with political cycles.

FY25 saw several important regulatory developments; Andhra Pradesh liberalised its alcohol policy, allowing premium brand owners to re-enter the state after years of absence. Karnataka simplified pricing and listing frameworks, improving clarity for manufacturers. Uttar Pradesh introduced composite liquor outlets, effectively expanding spirits’ retail reach by allowing beer and spirits to be sold from the same shops. At the national level, the exclusion of extra neutral alcohol (ENA) from GST reduced tax ambiguity and litigation for distillers. Online sales and e-commerce platforms, where permitted by state regulations, are gradually expanding reach to a broader audience, particularly in urban areas.

While these changes are positive, companies remain cautious. Pricing power is not uniform. In many states, price increases require government approval, which can lag cost inflation. This lag directly impacts margins, especially during periods of rising ENA, grain, or packaging costs.

Cost structure and margin drivers

Input costs remain a critical variable. ENA prices depend on grain and molasses availability, which in turn is influenced by monsoons, sugar cycles, and ethanol blending policies. Packaging costs, particularly glass bottles, and logistics expenses also materially affect margins.

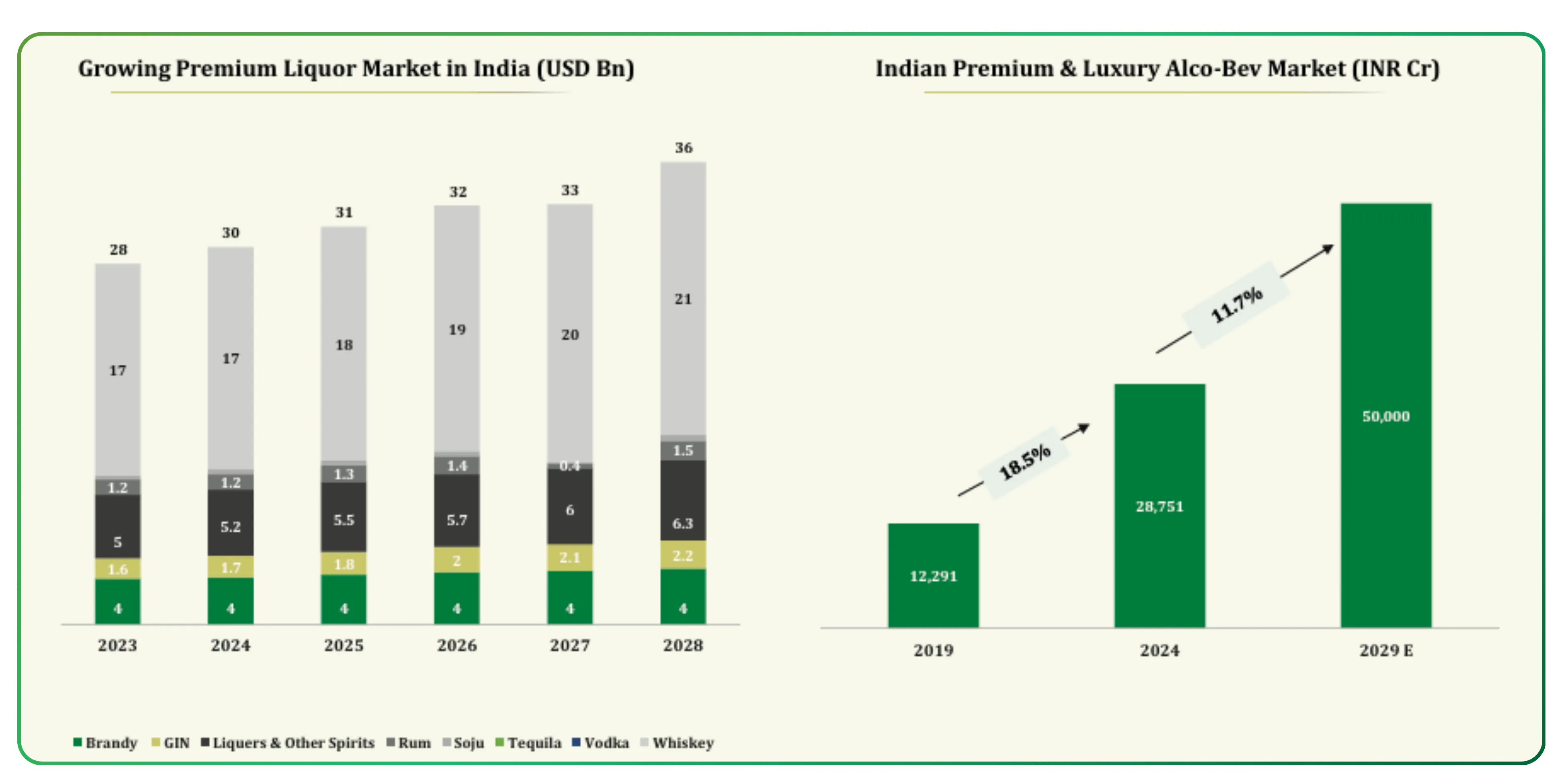

Despite these pressures, operating margins have improved across much of the industry, driven by a richer product mix, cost optimisation, and operating leverage. Premium and Prestige & Above categories deliver significantly higher realisations per case, even though they require higher brand-building expenditure.

This shift is visible in financial outcomes. Tilaknagar Industries expanded its EBITDA margin sharply in FY25 despite inflationary pressures, aided by premiumisation within brandy and cost discipline. Radico Khaitan reported strong growth in Prestige & Above volumes, which now account for nearly half of IMFL volumes and close to 70% of IMFL value. United Spirits continues to generate the bulk of its revenue and profits from its Prestige & Above portfolio, which contributes nearly 90% of net sales value.

Business models across the industry

Although grouped under a single industry, Indian alcohol companies operate very different business models. United Spirits is a scale-driven, distribution-heavy business with unmatched national reach and a diversified premium portfolio. Its strength lies in brand depth, route-to-market control, and steady cash generation.

Radico Khaitan represents a brand-led premiumisation model, where long-term value creation depends on scaling luxury and semi-luxury labels such as single malts and craft gin. This model typically trades margin stability today for higher brand equity tomorrow.

Tilaknagar Industries follows a focused category strategy, with leadership in brandy-dominant southern markets. This concentration has enabled strong margins but increases exposure to state-specific regulatory risks.

Allied Blenders operates at the intersection of scale and mass premium, while Globus Spirits and Associated Alcohols have more diversified exposure across IMFL, bulk alcohol, and ethanol, which introduces higher earnings cyclicality but also asset utilisation benefits.

Sula Vineyards is structurally different. Wine production involves longer working capital cycles, agricultural risks, and brand-led pricing. However, it benefits from favourable regulations and premium positioning that allow higher operating margins despite smaller scale.

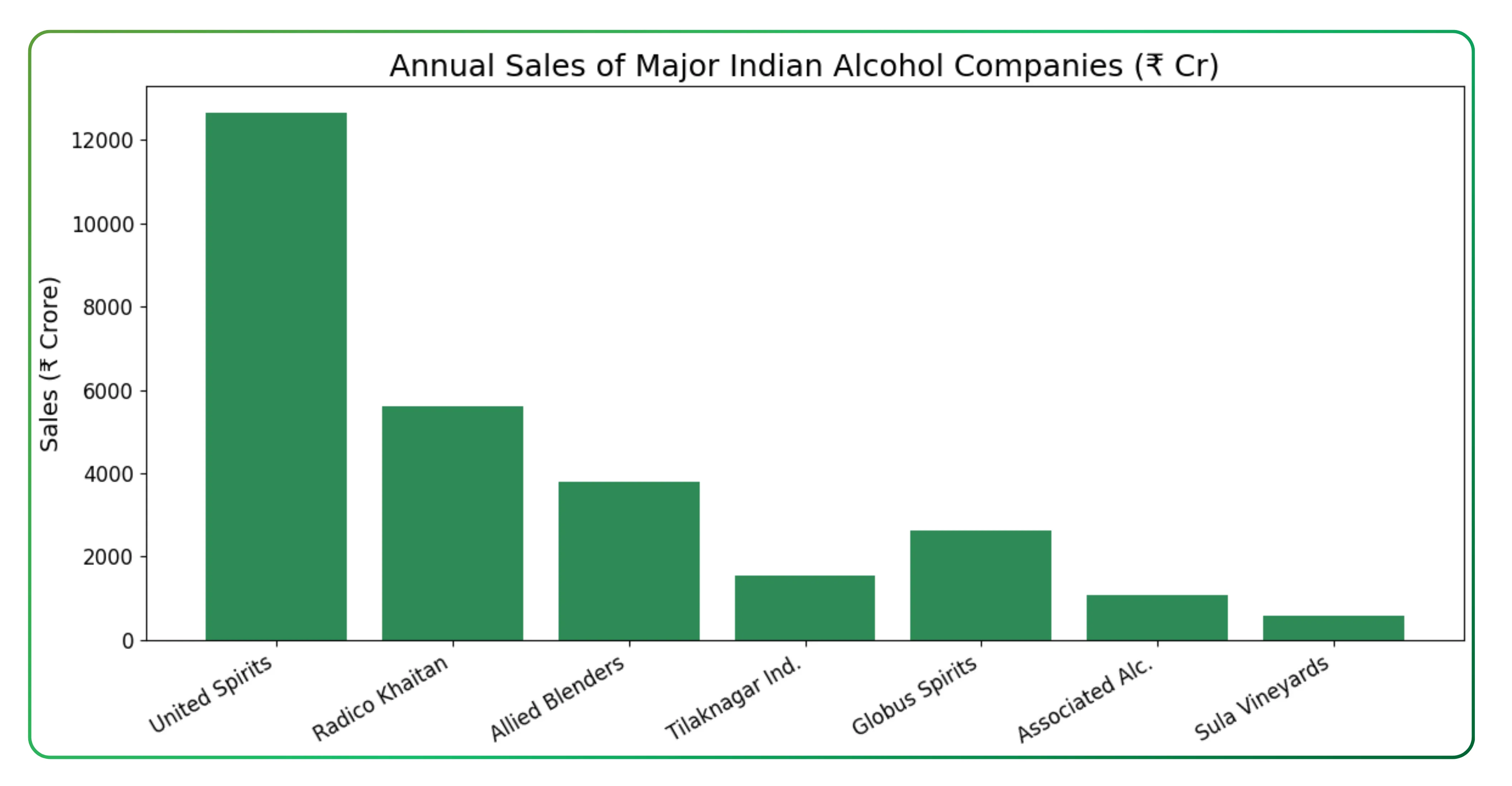

Major listed players Financial snapshot

| Company | Market Cap (₹ Cr) | Sales (₹ Cr) | OPM (%) | P/E (x) |

|---|---|---|---|---|

| United Spirits Ltd | 1,01,815 | 12,658 | 18% | 59.3 |

| Radico Khaitan Ltd | 42,578 | 5,598 | 15% | 91.7 |

| Allied Blenders & Distillers Ltd | 17,230 | 3,808 | 13% | 67.0 |

| Tilaknagar Industries Ltd | 11,176 | 1,554 | 19% | 41.0 |

| Globus Spirits Ltd | 2,809 | 2,616 | 7% | 57.4 |

| Associated Alcohols & Breweries Ltd | 1,786 | 1,090 | 12% | 20.8 |

| Sula Vineyards Ltd | 1,784 | 566 | 22% | 36.4 |

The competitive landscape includes large national players, agile local producers, and foreign brands, each operating under different pricing and distribution constraints.

The differences in business models and scale are clearly reflected in the financial comparison of leading listed players.

United Spirits leads the industry with a market capitalisation of ₹1,01,815 crore and sales of ₹12,658 crore, operating at an 18% margin and trading at a P/E of 59.3x. Radico Khaitan follows with a market capitalisation of ₹42,578 crore, sales of ₹5,598 crore, an operating margin of 15%, and a significantly higher P/E of 91.7x, reflecting expectations around premium growth.

Allied Blenders, with sales of ₹3,808 crore and a 13% operating margin, trades at 67x earnings. Tilaknagar Industries, despite much smaller sales of ₹1,554 crore, delivers a strong 19% operating margin and trades at a lower P/E of 41x. Globus Spirits reports sales of ₹2,616 crore but operates at a thinner 7% margin, while Associated Alcohols, with ₹1,090 crore in sales, maintains a 12% margin and trades at a relatively modest P/E of 20.8x. Sula Vineyards, though the smallest by revenue at ₹566 crore, stands out with the highest operating margin of 22%, reflecting wine’s premium economics.

Read our Q2 FY26 Performance Review of Entero, Senores, Acutaas, Alkem and Laurus for a data-driven look at how key pharma and healthcare companies performed this quarter.

Financial discipline and balance sheets

Balance sheet strength has improved across the sector. Several companies have reduced debt materially, benefiting from better cash flows and disciplined capital allocation. Tilaknagar Industries achieved a net cash position ahead of guidance. United Spirits holds significant cash and liquid investments, giving it flexibility to pursue premium acquisitions and partnerships. Lower leverage has reduced interest costs and improved return ratios, reinforcing profitability even in a regulated pricing environment.

Risks and what to watch

Despite strong structural drivers, risks remain. Regulatory uncertainty continues to be the biggest overhang, particularly in states with frequent policy changes. Input cost volatility, especially in ENA and packaging, can compress margins if price hikes are delayed. Category concentration, such as heavy dependence on brandy or specific states, increases earnings sensitivity to local policy shifts.

At the same time, health consciousness and moderation trends may influence long-term consumption patterns, pushing companies to innovate with lower-alcohol, flavoured, or differentiated offerings. Restrictions on alcohol advertising have pushed brands toward digital engagement, packaging innovation, and experiential marketing.

Long-term outlook

Over the forecast period, the Indian alcohol industry is expected to grow significantly, supported by rising disposable incomes and increasing acceptance of premium products. Euromonitor projections suggest IMFL volumes could reach over 500 million 9-litre cases by CY2029, with value growing much faster than volume due to premiumisation. White spirits and premium whisky are expected to outgrow the broader market, while wine is likely to remain small but fast-growing.

What emerges clearly is that India’s alcohol industry is no longer just a volume story. It is becoming a brand, pricing, and execution story. Companies that manage regulatory complexity well, build premium portfolios patiently, and maintain financial discipline are better positioned to compound value over time. India remains one of the largest alcohol markets globally and continues growing rapidly in value terms, even as consumption shifts toward higher quality products.

Turn research into action, trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.