India’s maritime story is expanding far beyond ports and cargo movement. An important transformation is taking place offshore, where exploration projects, supply runs, port operations and emergency support depend on specialised vessels that can operate in demanding environments. That’s the space ABS Marine Services Ltd, a specialised offshore vessel management and marine services company operating across India’s ports and offshore sector, has made its own.

For over three decades, the company has built a reputation in vessel management, offshore services and port operations. But it’s the recent pivot towards owning high-spec (Dynamic Positioning Class 2 vessels) DP2 offshore vessels (backed by multi-year contracts with ONGC, Schlumberger and port authorities) that has pushed ABS Marine into a stronger, more visible position within India’s marine ecosystem.

ABS Marine is not a typical asset-heavy shipping business, but a contract-driven offshore services model built around specialised vessels, long-term charters, and predictable earnings visibility. The company is stitching together a revenue model built on stable, contract-backed earnings, modern vessels and technical compliance. And those pieces are starting to show up clearly in the numbers.

A Closer Look at the Business

Business Verticals and Revenue Mix

ABS Marine operates through four distinct business verticals, each serving a different part of the offshore and port services value chain. Importantly, revenue contribution is increasingly skewed toward asset-backed, contract-driven segments.

1. Ship Management Services

This is the company’s legacy business and includes total ship management, providing crew management services, technical and commercial management, regulatory compliance, and operational oversight of third-party vessels. While margins are relatively stable, this vertical is lower on capital intensity and returns. Ship management contributes a steady but declining share of overall revenue as asset ownership scales. This marks the phase where ABS Marine commenced ship owning activities, transitioning from a pure management model to a contract-backed offshore support vessel ownership strategy centred on DP2 offshore vessels.

2. Vessel Ownership and Chartering

Vessel ownership has emerged as the key growth driver, anchored around DP2-class platform supply vessels operating under medium- to long-term contracts. This segment commands higher margins and stronger cash flow visibility. Its revenue share has expanded materially following recent vessel acquisitions and deployments.

3. Marine Services

Marine services include offshore logistics support, towing, anchor handling, and allied offshore activities. Revenue from this vertical is more cyclical and linked to offshore activity levels but benefits from strong client relationships with ONGC and global service providers.

4. Port Services

Port services comprise harbour operations, pilotage support, and port-side marine activities, often executed in coordination with port authorities and public sector undertakings across the Indian ports sector. This segment provides diversification and relatively predictable utilisation, though it remains a smaller contributor to consolidated revenue.

Overall, ABS Marine’s revenue mix is gradually shifting away from pure management services toward owned vessels and long-term charter contracts. This transition improves earnings quality, margin sustainability, and return visibility, while also increasing balance sheet intensity.

Revenue Split

Revenue Split by Customer Type

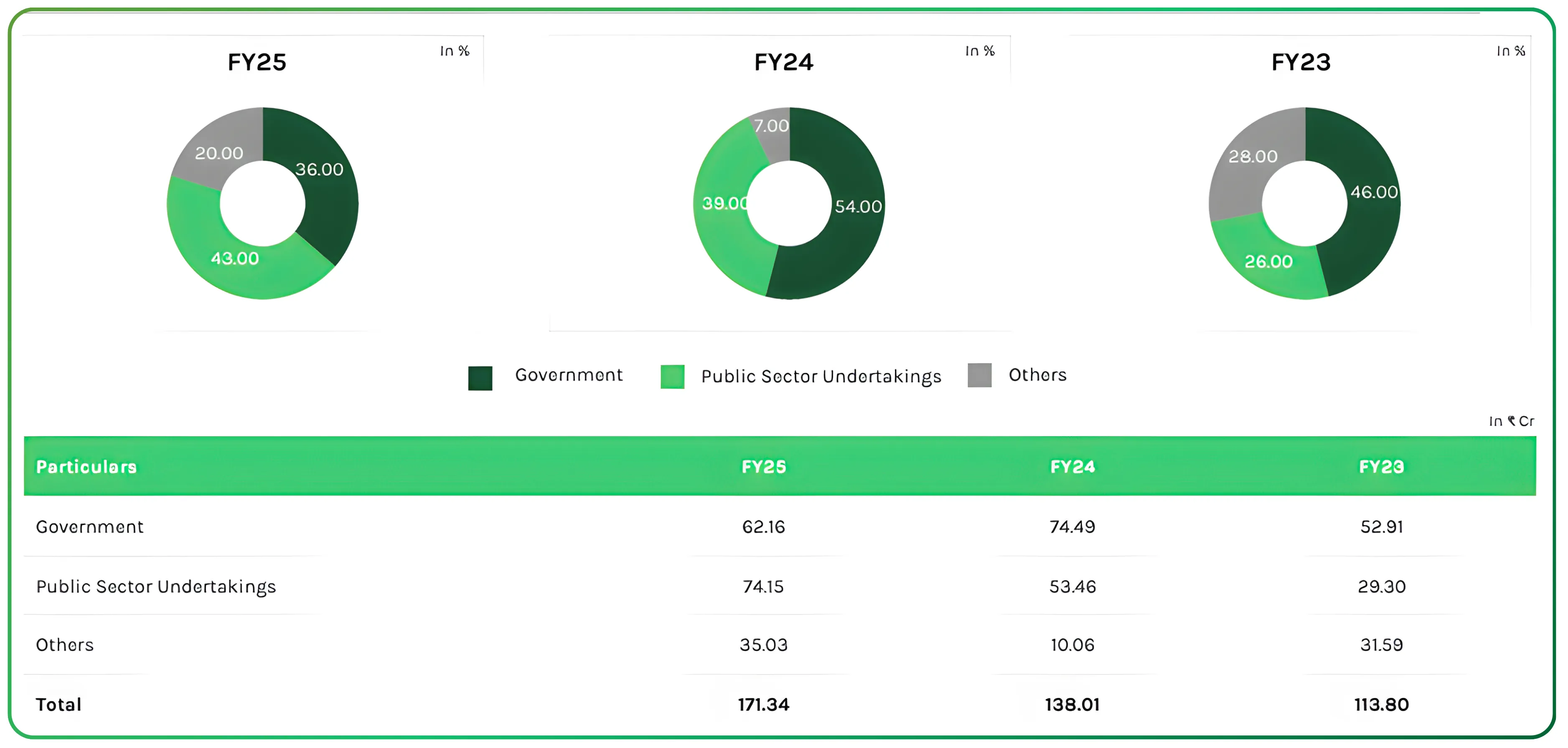

ABS Marine’s revenue profile remains largely anchored to government-linked entities, though the mix has evolved meaningfully over the last three years.

Revenue concentration remains tilted toward government and PSU clients, offering contract stability and payment security. FY25 also reflects a broader diversification, with a higher contribution from non-government customers compared to FY24.

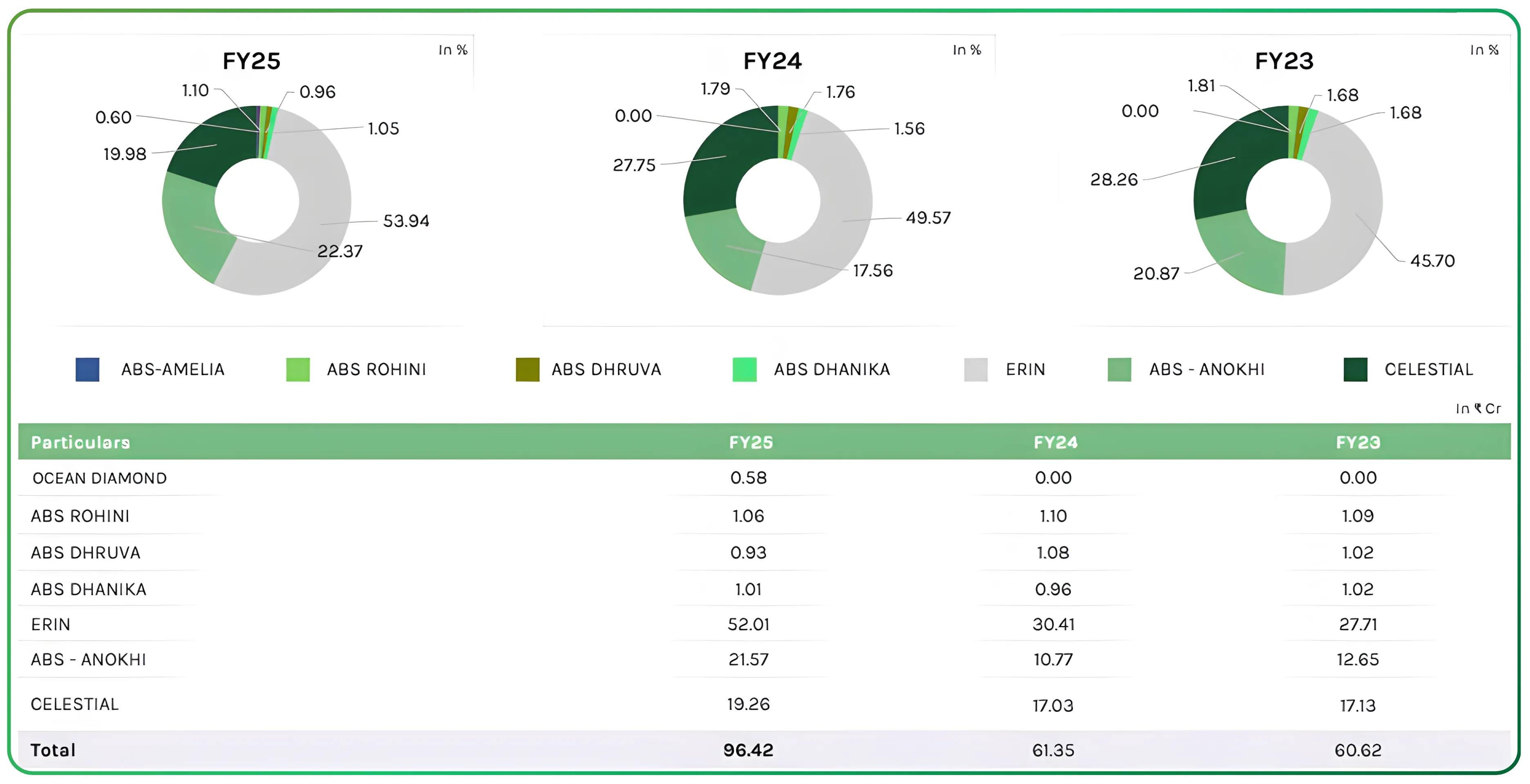

Revenue Split from Owned and Existing Vessels (FY25)

Revenue from owned vessels is increasingly concentrated in a few high-utilisation assets operating under long-term contracts.

ERIN has consistently remained the single largest revenue contributor, while ABS Anokhi has scaled sharply post-deployment. The company is increasingly reliant on fewer, higher-quality vessels rather than a fragmented fleet.

For readers tracking the sector closely, the complete marine industry breakdown is split across Part 1, Part 2, and Part 3 — each covering a different layer of India’s maritime economy.

Why ABS Matters in the Marine Economy

India’s offshore segment is entering a multi-year expansion cycle. Offshore accounts for nearly 30% of global oil and gas production, and 2024 alone saw more than $110 billion worth of new offshore project sanctions globally. At home, India’s port modernisation pipeline exceeds ₹40,000 crore under PPP arrangements.

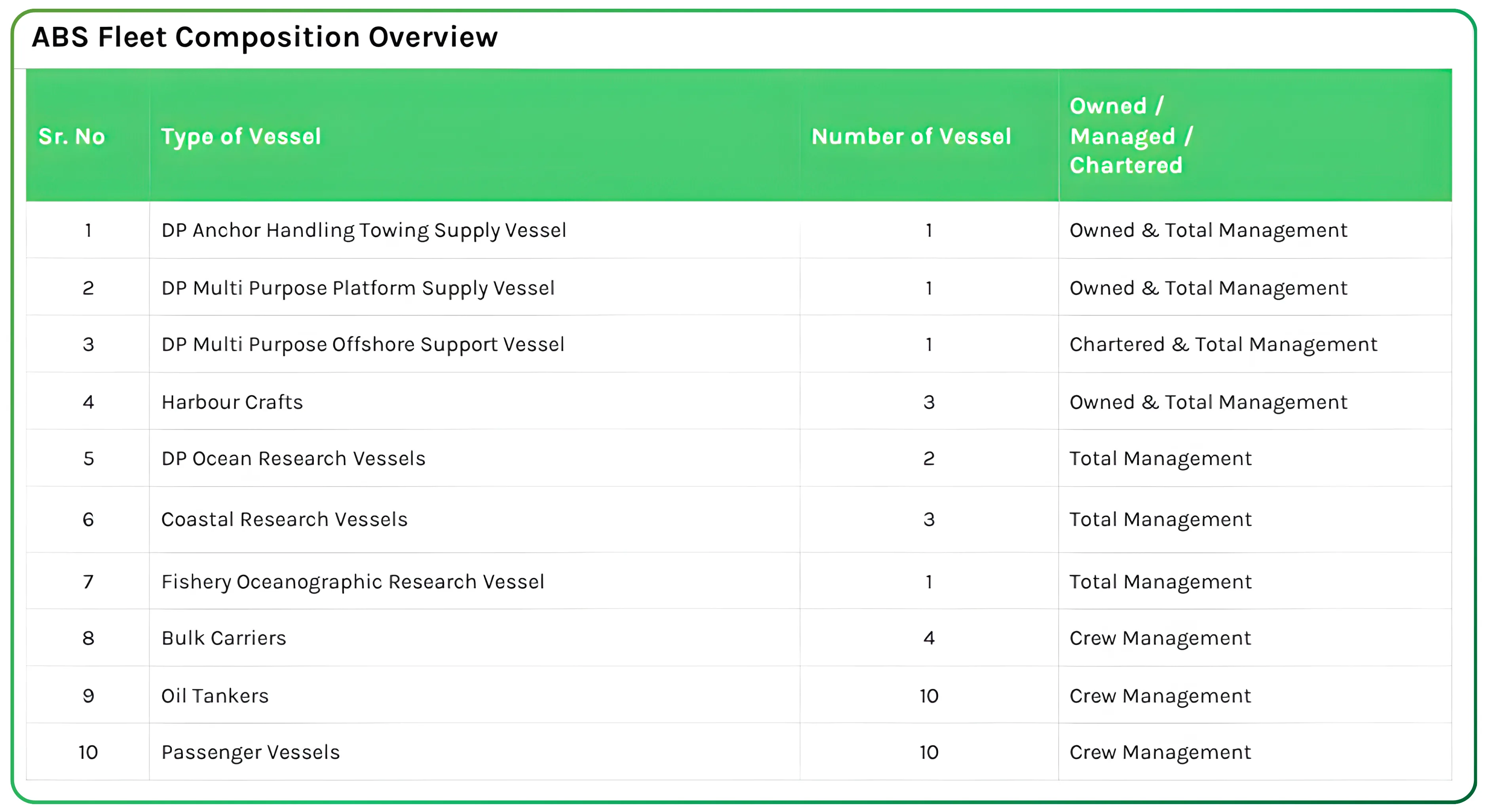

All of this needs workhorses: DP2 platform supply vessels, well-stimulation vessels, patrol boats and specialised craft that can support deepwater operations, emergency response and coastal activities. The issue is that the global OSV (Offshore Support Vessel) fleet is ageing (average age above 20 years) and newbuild supply remains tight.

While segments like oil tankers, gas tankers, and bulk carriers dominate the broader shipping industry, ABS Marine operates in a specialised offshore niche aligned with the gas sector and offshore energy services.

ABS Marine has used this moment wisely. It now owns a young offshore fleet with an average age of 12.4 years, significantly below the global OSV average, and has committed to acquiring only DP2 vessels going forward. In a market starved of compliant, modern capacity, this creates real bargaining power, and the company is already seeing it through stronger contract wins.

Segment Deep Dive

Offshore Vessel Operations (the growth engine)

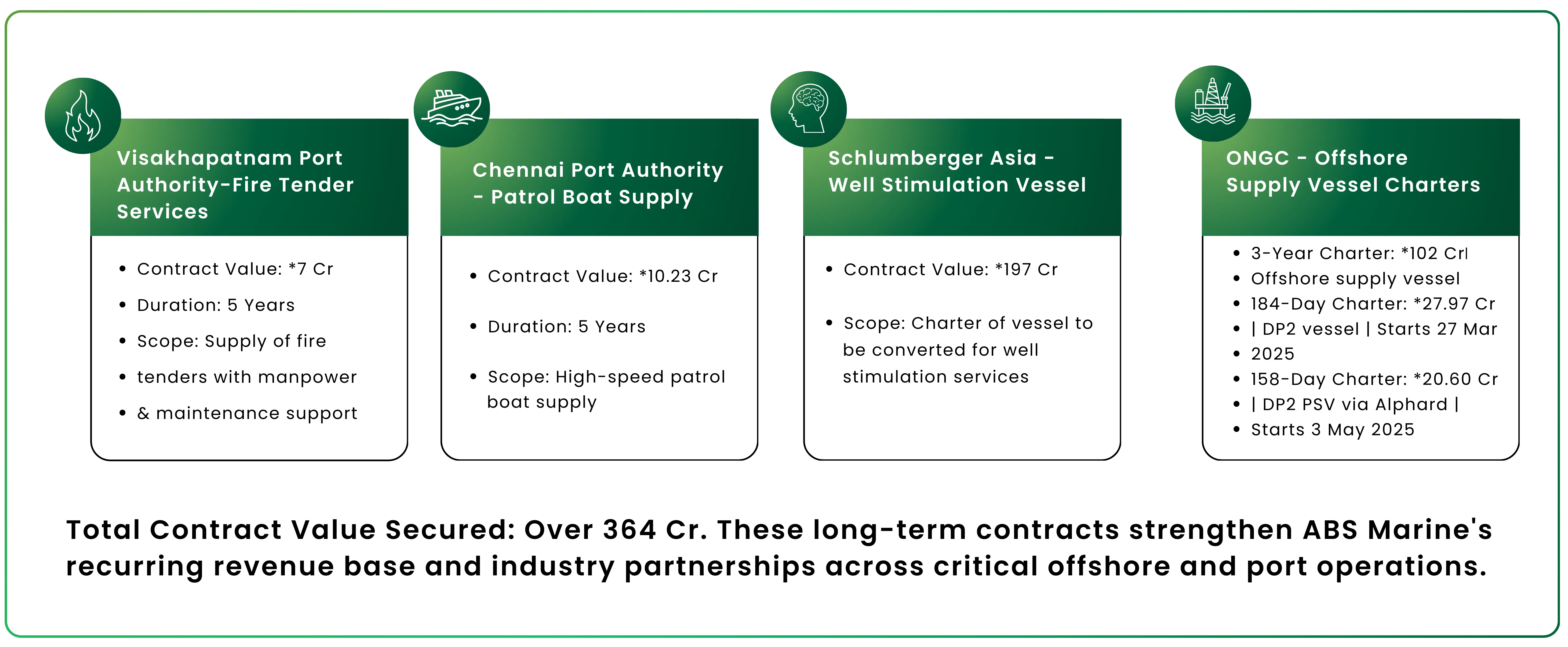

This is now the core of ABS Marine’s earnings. FY25 was a turning point: the company acquired two DP2 PSVs (Ocean Diamond and Emerald) both with contracts already tied in. The third DP2 PSV arrives in FY26 and management expects this vessel to be larger and more capable.

Two major vessels underwent contract upgrades that materially changed the company’s P&L trajectory:

- ABS Anokhi resumed service under a revised ONGC contract after a DP1→DP2 upgrade.

- Celestial shifted from an ONGC contract into a much higher-paying three-year agreement with Schlumberger.

These two vessels alone lifted H2 FY25 earnings sharply, and they anchor the business for the next few years.

The vessels were sourced from established global yards, including the Xiamen Shipbuilding Industry, and acquisitions such as the M.V. Celestial vessel were executed through structured transactions involving Epsom Shipping India Pvt Ltd, a long-standing entity in offshore support vessel operations

While ABS Marine reports a single consolidated maritime segment, management commentary provides clear directional insights on margin profiles. Offshore ship-owning operations, particularly DP2 vessels under long-term charters, are the highest-margin vertical, with management guiding vessel-level EBITDA margins of 60–65%. Port services and ship management are more service-oriented and manpower-driven, offering steadier but lower margins. As the revenue mix shifts toward owned offshore vessels, consolidated margins have expanded, reflected in the sharp improvement seen in H1 FY26.

The company does not disclose segment-wise financials; margin commentary is based on management guidance and revenue mix trends.

Ship Management

This remains a steady, recurring revenue stream contributing around 40–45% of business. The company manages 2,000+ seafarers and has a strong reputation among government institutions and PSUs.

Port & Marine Services

From patrol boats for Chennai Port to firefighting services for Visakhapatnam Port, ABS Marine operates within specialised niches where relationships matter as much as capability. These contracts don’t swing earnings dramatically, but they add stability.

Where the Revenue Mix Is Heading

Management expects the share of earnings from vessel ownership to rise to 55–60%, making the business structurally more profitable. This shift alone is the reason for EBITDA margin expansion.

Financial Story

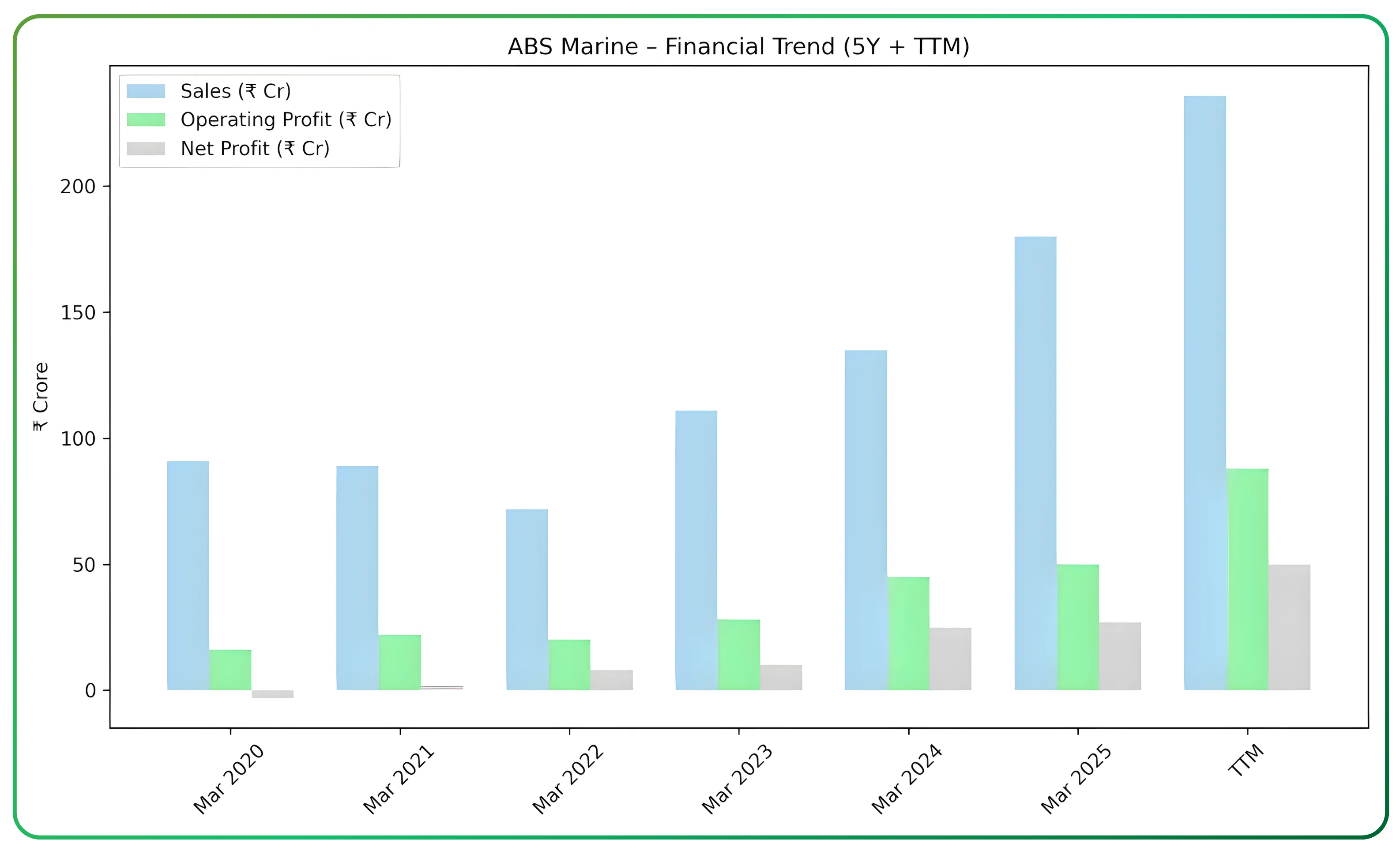

ABS Marine’s numbers over the past five years reflects how the company has steadily evolved, with a gradual improvement in scale and profitability over time. At a market capitalization of around ₹505 crore (market cap of ABS Marine), the company reflects improving earnings growth.

| Financials | Mar 2020 | Mar 2021 | Mar 2022 | Mar 2023 | Mar 2024 | Mar 2025 | TTM |

|---|---|---|---|---|---|---|---|

| Sales (₹ crore) | 91 | 89 | 72 | 111 | 135 | 180 | 236 |

| Operating Profit (₹ crore) | 16 | 22 | 20 | 28 | 45 | 50 | 88 |

| Operating Margin (%) | 17% | 25% | 28% | 25% | 33% | 28% | 37% |

| Net Profit (₹ crore) | -3 | 2 | 8 | 10 | 25 | 27 | 50 |

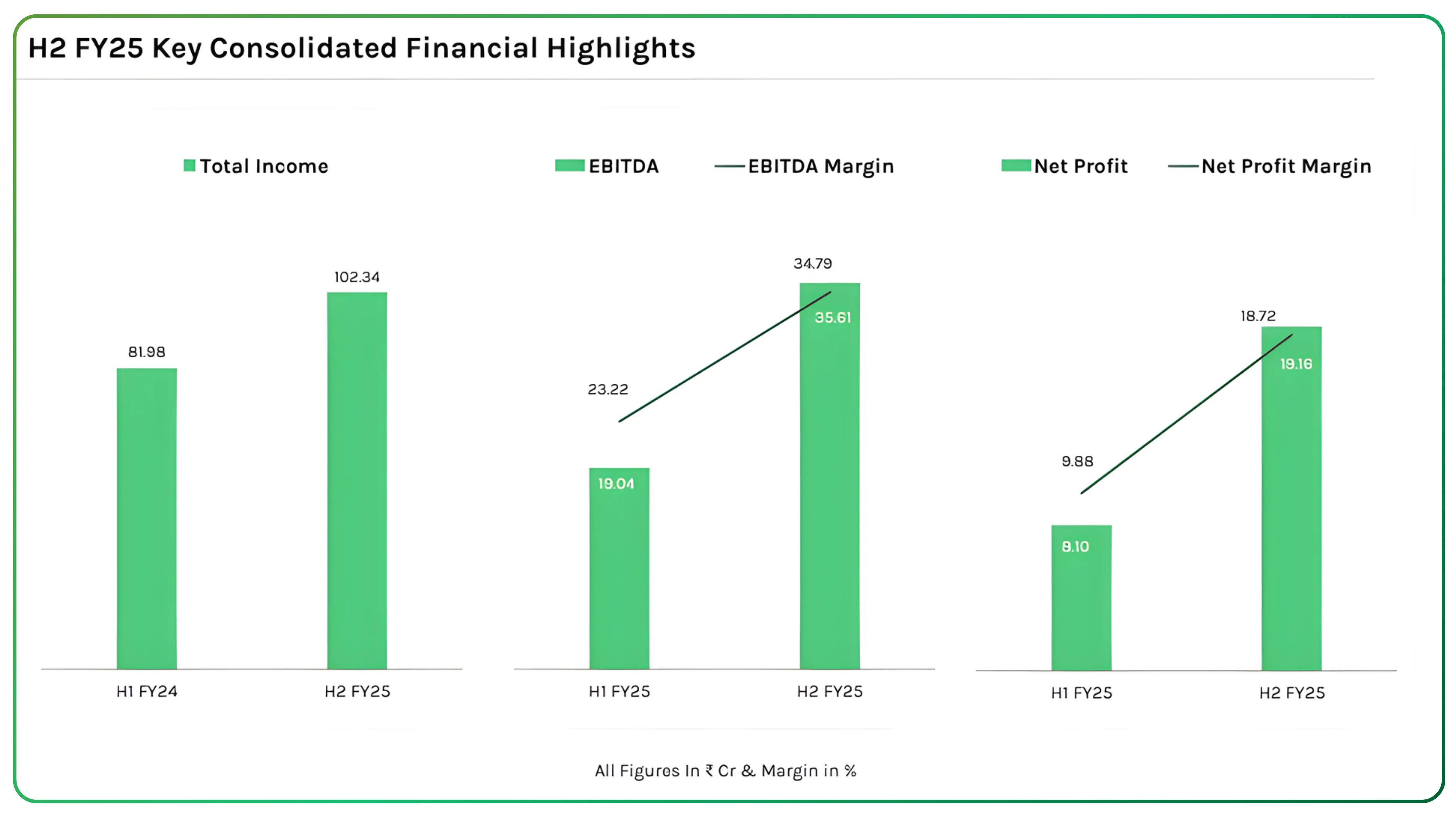

ABS Marine moved from a low-margin management-heavy model into a more asset-backed, higher-yielding structure. Margins expanded as modern DP2 vessels entered the fleet and older contracts rolled into new terms. FY25 H2 was especially strong (revenue grew 25%, EBITDA jumped 87% and PAT more than doubled) driven entirely by the improved charter profile of key vessels.

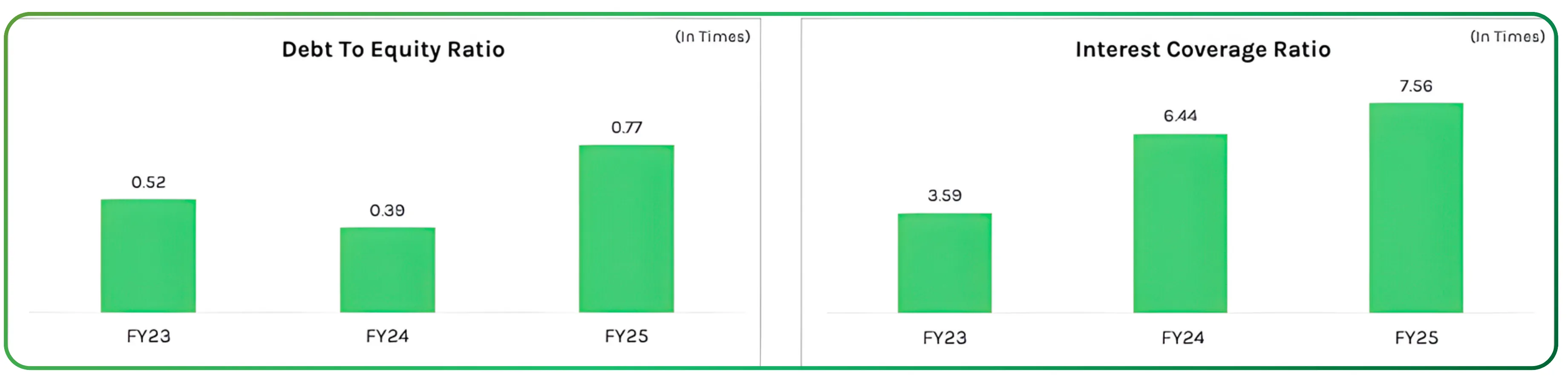

Borrowings increased in FY25 as ABS Marine entered a deliberate fleet-expansion phase, funding new DP2 offshore vessel acquisitions through its standard 70–75% debt and 25–30% equity financing model. The rise in debt primarily reflects term loans taken for contract-backed vessels such as Ocean Diamond, Emerald, and the recently delivered DP2 well-stimulation vessel, all tied to long-term charters with ONGC, Schlumberger, and other clients. Management has clarified that the increase is asset-backed and strategic, not driven by refinancing or financial stress, with average borrowing costs at around 9.5%.

A rising debtor cycle (113 days) and a heavier working capital load are worth watching. But the profitability curve is clearly moving upward and management is guiding consolidated EBITDA margins of 40–45% going forward.

If ABS Marine sticks to that band, the business model looks much more like a predictable offshore asset operator than a cyclical shipping outfit.

Strategic Positioning

ABS Marine is positioning itself well: younger DP2 vessels, longer contracts, more private oilfield clients and a stronger footprint across port services.

The real differentiators include:

A modern fleet at a time when global OSV (Offshore Support Vessel) supply is ageing

Recurring, multi-year contracts reducing volatility

Strong relationships with NOCs like ONGC and global oilfield companies like Schlumberger

Technical expertise and compliance that reduce customer risk

Increasing shift toward higher-margin owned assets

Most operators struggle because volatility in day rates makes earnings unpredictable. ABS Marine has solved this by locking in contracts typically without exposure to fuel and water fluctuations (charterers bear those costs) making earnings primarily a function of utilisation and operational discipline.

Moat: What Sets ABS Marine Apart

ABS Marine’s moat isn’t about size, it’s about positioning, compliance and timing.

1. Technical & Compliance Advantage

Operating DP2 vessels requires certification, training and systems that not every regional operator can match. This makes ABS a preferred partner for contracts that emphasise safety and reliability.

2. Long-Term Contract Visibility

Three- and five-year agreements with ONGC and Schlumberger provide predictable cash flows, shielding the business from oil price swings.

3. Younger Fleet in a Tight Market

With an average fleet age of 12.4 years, ABS stands out in a world where OSVs commonly exceed 20 years. This will matter a lot as offshore demand increases.

4. Sticky Client Relationships

ABS has decades-long ties with government and PSU clients. On the private side, Schlumberger (SLB) is emerging as a major partner. This blend makes the revenue book more resilient.

5. Revenue Mix Tilted Toward Ownership

Owned vessels deliver significantly higher margins than management contracts. The more ABS Marine shifts in this direction, the stronger its moat becomes.

Looking beyond this sector? We’ve published performance reviews on Gravita India, VA Tech Wabag, and Deep Industries as well.

Valuation: Where ABS Marine Stands

At a market cap around ₹505 crore and a P/E of 10, ABS Marine trades at a noticeable discount to the broader marine services industry (P/E of 12–13). That discount exists even as TTM sales reached ₹236 crore and net profit crossed ₹50 crore.

EV/EBITDA at 8.9 places the company in a zone where the market is acknowledging profitability, but not fully crediting future cash flows from new DP2 deployments. Debt-to-equity of 1.34 reflects an expansion phase rather than stress.

If margins stick in the guided 40–45% zone, that valuation could shift meaningfully. But here’s where a scenario analysis helps.

Base / Bull / Bear: A Scenario View Anchored to Management Commentary

Base Case: The Guided Path

If ABS Marine delivers on what management outlined (₹135–140 crore revenue potential in H1 FY26, deployment of the third PSV, and EBITDA margins in the 40–45% range) then the current valuation likely holds or moves slightly higher. The company becomes a predictable offshore operator with steady multi-year cash flows, but with elevated debt during the expansion phase.

Valuation in this case stays tethered to current multiples unless cash flows accelerate faster than debt.

Bull Case: When Everything Management Hinted Actually Plays Out

This isn’t imaginary upside — it comes directly from disclosed commentary:

Offshore charter rates increasing due to global supply shortages

Three DP2 vessels running at high utilisation

Two PSVs rolling into long-term contracts in Sep–Oct 2025 at higher rates

SLB contract potentially exceeding the ₹197 crore quoted value

EBITDA doubling from the earlier base (management’s own words)

Industry cycle remaining tight for “a few years”

In such a setup, ABS Marine could command better valuation multiples, moving toward the 10–12x EV/EBITDA band typical of offshore operators in favourable cycles. PAT margins would likely stabilise at the upper end of the mid-teens.

This bull case is entirely built on the company’s own commentary, not external assumptions.

Bear Case: If the Known Risks Surface

Everything here comes from disclosed risks:

Contract rollover delays for two DP2 PSVs expiring in FY26

Debtors rising further from 113 days

Debt rising to ~₹300 crore without matching EBITDA lift

Short-term contracts failing to convert into long-term ones

Working-capital tightening delaying vessel deployment

In this case, margins could slip back toward the historical 28–32% range and interest costs weigh on profits. Valuation may remain compressed, closer to single-digit P/E until debt normalises.

Risks & Monitorables

Key risks to monitor are largely operational rather than existential, but they have direct implications for cash flow visibility and execution quality. These include maintaining working capital discipline amid rising debtor days, timely deployment of the third PSV, and renewal outcomes for contracts due in September–October 2025. In addition, the interest cost trajectory as debt approaches ₹300 crore, execution pace of newly acquired vessels, stability of long-term engagements with ONGC and SLB, and prevailing pricing trends in the OSV market will be important variables to track over the medium term.

Final Perspective

ABS Marine is methodically building a modern, technically compliant fleet at a time when both global and domestic offshore activity is accelerating and incremental capacity remains limited. By anchoring growth around long-term contracts and prioritising DP2-class vessels, ABS Marine is positioning itself for more stable utilisation and structurally higher margins.

The financial profile reflects a transition into a new phase, where profitability is increasingly driven by asset quality and contract visibility rather than pure management fees. The next 12–18 months, as newly inducted vessels stabilise under long-term charters, will be critical in shaping the market’s assessment of earnings durability and return metrics.

At this stage, ABS Marine stands out as one of the few listed players offering a relatively clean, contract-led exposure to India’s offshore services cycle.

Turn research into action — trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.