If you look at a simple biscuit packet, the tiny expiry date printed at the corner barely grabs your attention, yet it represents an entire industry working quietly behind the scenes. ‘Control Print Ltd.’ operates in this almost invisible space, manufacturing machines that print essential information such as expiry dates, batch numbers, QR codes, and barcodes across FMCG, pharma, food, beverages, pipes, cables, steel, plywood and many more categories. From bottles and medicine strips to wire coils and plywood sheets, the printed text you see is almost always produced by a coding and marking machine. In a market long dominated by global giants, Control Print stands out as the only Indian manufacturer, holding an 18–20% domestic market share with an installed base of over 21,500 machines.

Over time, the company has expanded beyond basic coding and marking into three additional areas. The first is Track & Trace technology, which enables product authentication and end-to-end supply-chain visibility using QR codes. The second is packaging, through its V-Shapes acquisition in Italy, which manufactures single-serve sachet machines and laminates. The third is a growing international footprint through Markprint (Netherlands) and Codeology (UK), which add complementary digital printers, end-of-line automation systems, and label application technologies. Together, these create a broader ecosystem: machines, consumables, software, and packaging, allowing the company to participate in multiple parts of the product-identification value chain.

Control Print’s Business Model

The core of the business is simple: industries need reliable, high-speed printing systems to mark their products, and once these machines are installed, they consume ink and solvents every single day. Control Print earns a smaller one-time margin from selling the printers but enjoys high recurring margins from consumables, spare parts, and service contracts. This “razor and blade” model gives the company predictable, sticky cash flows.

The Track & Trace division extends this model by embedding QR-based identification into products. Two of India’s largest pharma companies are currently piloting this system, and if adopted at scale, it could create annuity-like revenue from software, maintenance, and consumables.

In the packaging vertical, V-Shapes focuses on single-dose sachet technology used for products such as honey, shilajit, cosmetics, nutraceuticals and food pastes. The most strategic feature of this business is that V-Shapes machines are electronically locked, meaning users must purchase laminates from Control Print. This creates a second recurring revenue stream similar to the consumables model in coding and marking.

Business Segments and Revenue Contribution

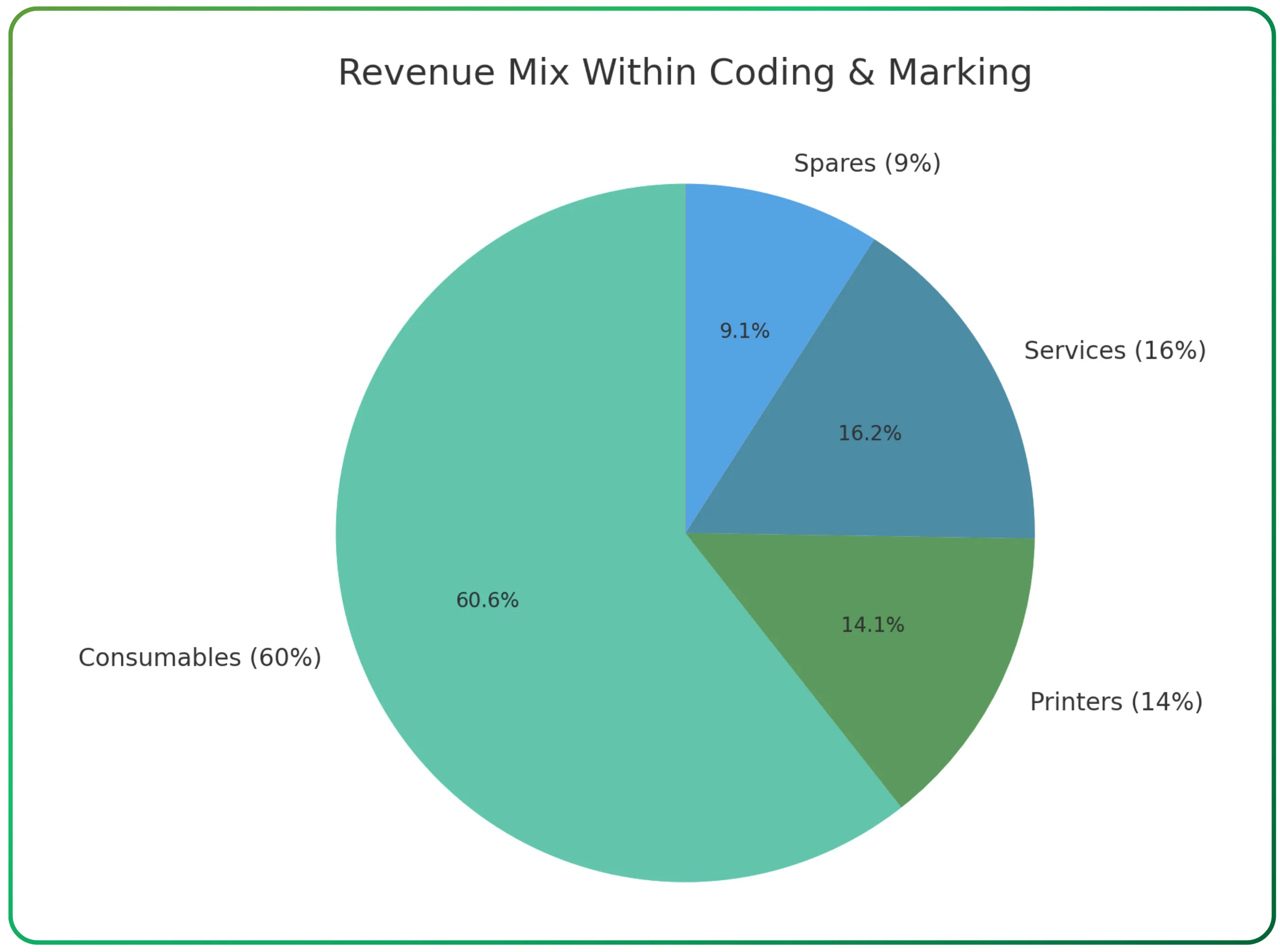

Coding and marking remains the dominant segment and contributes roughly 90–95% of consolidated revenue. Within this segment, consumables account for about 60% of revenue, while printers contribute roughly 14%, services around 16%, and spares close to 9%. This mix highlights that the company maintains strong gross margins of nearly 60%; recurring consumables form the backbone of profitability.

The international subsidiaries, Markprint and Codeology, expand the company’s capabilities in digital printing and end-of-line automation, and both operate profitably at their respective levels. The packaging business, through V-Shapes in Italy and India, is still in an investment phase, with the Italian entity expected to break even in FY27.

The company’s revenue growth over the past five years, along with its steady profitability, has supported a rising market cap and increased institutional interest.

Geographical Presence and Revenue Breakup

The company has built a meaningful international footprint over the last three years. The domestic business is driven through a network that covers more than 1,700 towns and 2,700 pin codes, supported by major manufacturing units in Nalagarh (Himachal Pradesh) and Guwahati (Assam). These two factories manufacture the entire range of coding and marking printers, inks, solvents, and select high-resolution systems for the Indian market.

Image: Markprint in the Netherlands

Beyond India, the company now operates through a set of subsidiaries that broaden its reach across Europe and the Middle East. Markprint in the Netherlands focuses on high-resolution and CMYK digital printers, Codeology in the United Kingdom manages label-print-and-apply systems and end-of-line automation, while CP Italy handles the V-Shapes single-serve packaging business. A new subsidiary in the UAE has been created to target the Middle East and Africa, allowing Control Print to sell both Indian-made products and European-label offerings into these markets. This combination gives the company a presence across India, Europe (Italy, Netherlands, UK), and the Middle East.

Image: Codeology in the UK

When we look at revenue contribution, India continues to account for the vast majority of the business. In H1 FY26, the consolidated revenue stood at ₹223 crore and Overseas operations contributed roughly ₹21 crore during the same period, or about 9–10% of total revenue. Most of the international contribution comes from Markprint and Codeology, as the Italy business is still in a loss-making but transitioning phase.

Control Print is still an India-first company, with domestic operations representing around 90% of the consolidated topline. However, the presence of profitable subsidiaries in the UK and Netherlands, combined with the long-term growth potential in Europe and the Middle East for V-Shapes and Track & Trace solutions, hints that overseas contribution may gradually rise over the next three to five years.

If you're tracking India’s industrial expansion across multiple sectors, we also recommend reading our marine industry report: India’s Maritime Economy — Complete Sector Analysis (Part 1/3).

Financial Performance

Investors tracking Control Print Ltd stock often focus on consolidated numbers, since these best reflect the business drivers behind the Control Print share price and the company’s improving fundamentals.

Consolidated Financials – H1 FY26

| ₹ crore | H1 FY26 | H1 FY25 | YoY (%) |

|---|---|---|---|

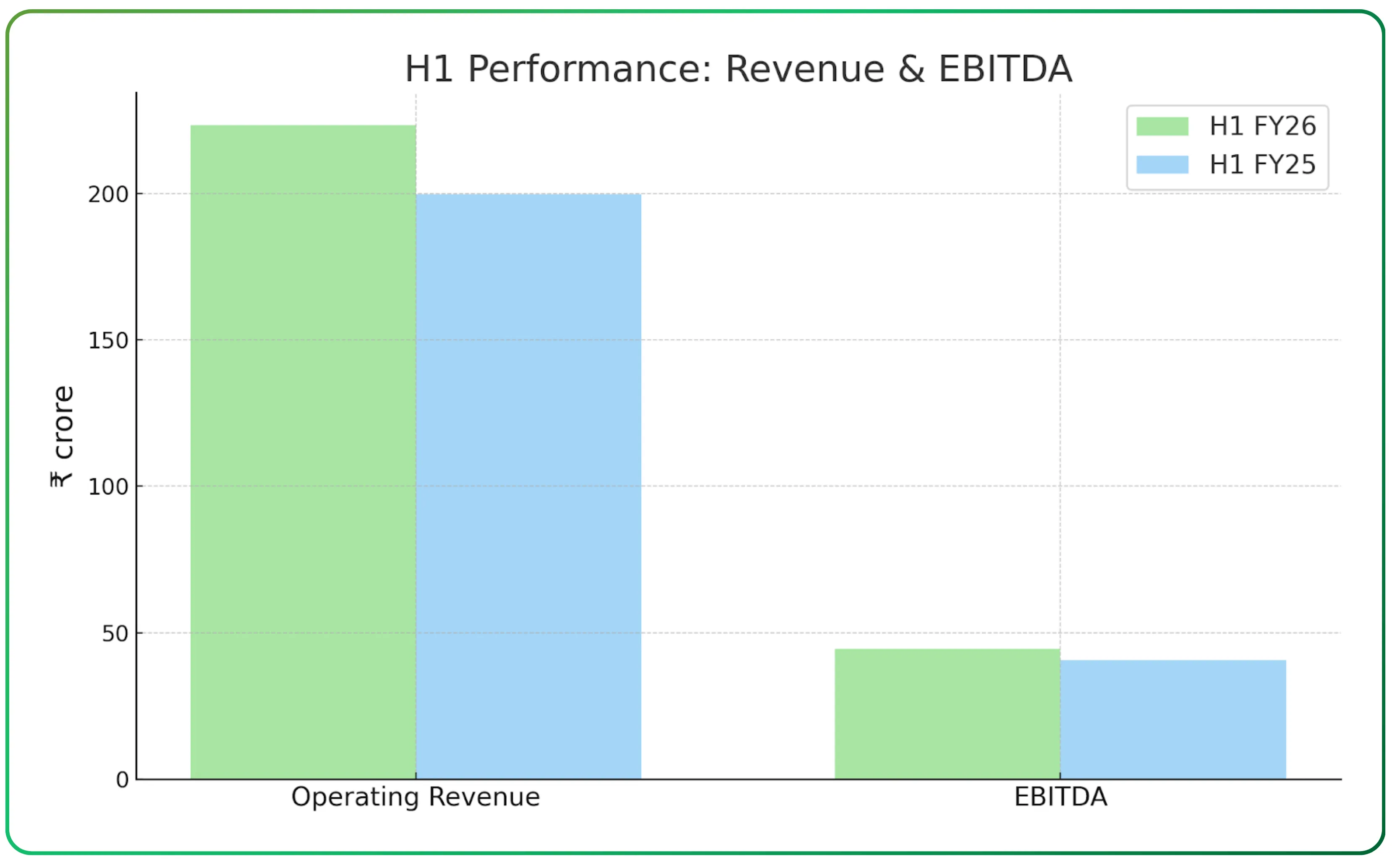

| Operating Revenue | 223.3 | 199.6 | 11.8 |

| Gross Profit | 133.7 | 120.2 | 11.2 |

| EBITDA | 44.5 | 40.7 | 9.4 |

| PAT | 27.2 | 25.1 | 8.0 |

Consolidated results remain subdued due to continuing losses in Italy. However, the profitable performance of Markprint and Codeology offsets part of this drag. Management expects Italy’s losses to moderate in the second half and decline significantly in FY27.

Long-Term Track Record (Consolidated)

| ₹ crore | FY21 | FY22 | FY23 | FY24 | FY25 |

|---|---|---|---|---|---|

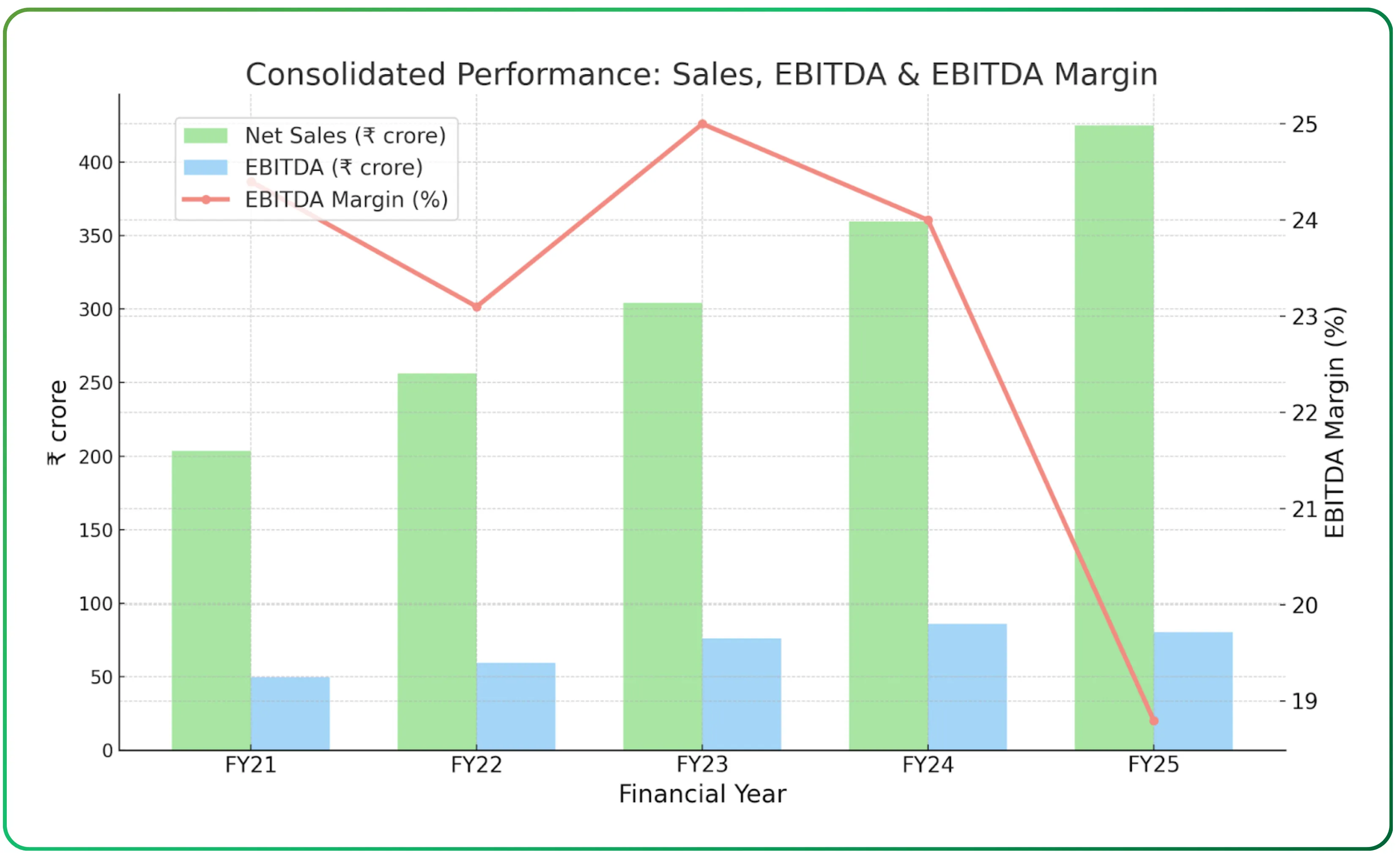

| Net Sales | 203.7 | 256.2 | 304.3 | 359.3 | 425.0 |

| Gross Profit | 125.1 | 153.6 | 183.1 | 212.0 | 246.3 |

| Gross Margin (%) | 61.4 | 59.9 | 60.2 | 59.0 | 58.0 |

| EBITDA | 49.7 | 59.3 | 76.0 | 86.1 | 80.1 |

| EBITDA Margin (%) | 24.4 | 23.1 | 25.0 | 24.0 | 18.8 |

| PAT (excl. exceptional) | 30.8 | 36.9 | 52.7 | 54.2 | 100.1 |

| PAT Margin (%) | 15.1 | 14.4 | 17.3 | 15.1 | 23.5 |

It is worth noting that FY25 PAT was boosted by a one-time exceptional gain and tax credit, leading to an unusually high profit base for that year; underlying operational performance remained stable. FY25 profitability includes significant non-operational gains. The March 2025 quarter reflects a large deferred tax credit, which sharply inflated consolidated PAT and resulted in an unusually high TTM EPS. In FY26, the only major exceptional item is a one-time capital subsidy of approximately ₹4 crore recognised under the CCIIAC scheme for the Himachal Pradesh plant. These items do not reflect ongoing business performance. Other income for the company primarily consists of treasury income from cash and investments, along with occasional foreign-exchange adjustments and minor miscellaneous credits.

On a consolidated basis, revenue grew at roughly 20% CAGR between FY21 and FY25. Gross profit followed a similar trajectory and remained in a tight 58–60% band, reflecting the strength of Control Print’s consumables-heavy business model. EBITDA grew at around 13% CAGR, although the FY25 EBITDA margin compressed due to losses and R&D spending at the Italian subsidiary. PAT expanded sharply, rising at a 34% CAGR, supported by core business strength and one-time exceptional gains in FY25.

The company has scaled consistently, absorbed international acquisitions without destabilising its core profitability, and maintained a fundamentally strong margin profile despite new business investments.

Balance Sheet Strength and Cash Flow Position

Control Print’s balance sheet is one of its greatest strengths. The company carries virtually no debt, with a debt-to-equity ratio of just 0.02 on a standalone basis. Its current ratio of nearly 4 indicates ample short-term liquidity, and both ROCE (18.5%) and ROE (26.9%) remain strong.

Working-capital efficiency has improved materially over the years. Inventory days have reduced from more than 500 days historically to about 224 days, and the cash conversion cycle has fallen to roughly 240 days. The company also holds significant investments and cash equivalents across standalone and consolidated books, giving it flexibility to fund acquisitions, R&D, and the V-Shapes turnaround without external borrowing.

The cash flow record over the past decade shows consistent cash generation from operations. Capex requirements in the core coding and marking segment are modest, and management has confirmed that there is no major capex planned for the next one to two years.

Control Print Ltd shares also attract attention from dividend-seeking investors, as the company maintains a consistent dividend yield supported by strong cash flows and negligible debt.

Industry Landscape

The global coding and marking industry is valued at approximately USD 8.6 billion in 2025 and is expected to reach nearly USD 11.8 billion by 2030, driven by rising packaged food consumption, increasing regulatory mandates, and expanding industrialisation in emerging markets. Asia-Pacific is the fastest-growing region, with strong demand from FMCG, pharmaceuticals, chemicals, construction materials, and automotive.

In India, the coding and marking market is projected to grow at a CAGR of nearly 9% between FY25 and FY30, faster than global growth. The market is dominated by four large players, with Control Print being the only domestic manufacturer. National programmes such as Make in India 2.0, PMKSY, the Automotive Mission Plan, and growing investments in FMCG, food processing, healthcare, building materials, and e-commerce are expected to boost long-term demand.

Competitive Advantages

Control Print benefits from being the only Indian player with full manufacturing capabilities, which allows it to offer faster service, lower cost structures, and stronger customer reach compared to multinational competitors that rely heavily on imports. Its installed base of more than 21,500 printers creates a long-tail stream of consumable sales, which form the most profitable part of the business.

The company’s ecosystem has become broader in recent years. Track & Trace provides a high-value solution layered on top of traditional coding, while V-Shapes offers machine + laminate lock-ins similar to the consumables model. The expansion of Markprint and Codeology adds digital and automation capabilities that strengthen its global relevance. The debt-free balance sheet and steady cash flow generation further reinforce its competitive position.

Key Risks

The biggest execution risk lies in the Italian subsidiary. The business is still loss-making, and delays in certifying recyclable laminates or converting customer trials into full orders could prolong losses. The Track & Trace division, while promising, depends on successful completion of pilots with large pharma companies; meaningful revenue will flow only after wider adoption. The end of the Guwahati GST incentive has removed an annual benefit of around ₹8.5 crore from FY26 onwards, which the company must offset through core growth. Finally, FX fluctuations and the natural growth ceiling of the Indian coding and marking market could limit upside if new initiatives do not scale.

If you’re following India’s manufacturing and capital goods story closely, you may also want to read our analysis of ACE: Is Action Construction Equipment Rising to Become India’s Biggest Equipment Powerhouse?

Valuation

At the current market price of ₹752, the stock trades at roughly 12× trailing earnings. Management expects standalone PBT to comfortably cross ₹100 crore in FY26. However, it’s important to understand that this TTM EPS is temporarily inflated. The March 2025 quarter shows a ₹67 crore net profit, which included exceptional income and a deferred-tax credit that artificially boosted earnings. Because of that one exceptional quarter, the trailing EPS appears higher than what the company earns in a normal twelve-month period.

The best way to value the company, therefore, is to use a normalised earnings base built from the most recent “clean” quarters of FY26. The consolidated quarterly PATs from June 2025 and September 2025 together add up to ₹28 crore. Annualising these two quarters gives a normalised FY26 PAT of approximately ₹56 crore, which reflects the company’s genuine operating performance without the one-time FY25 boost.

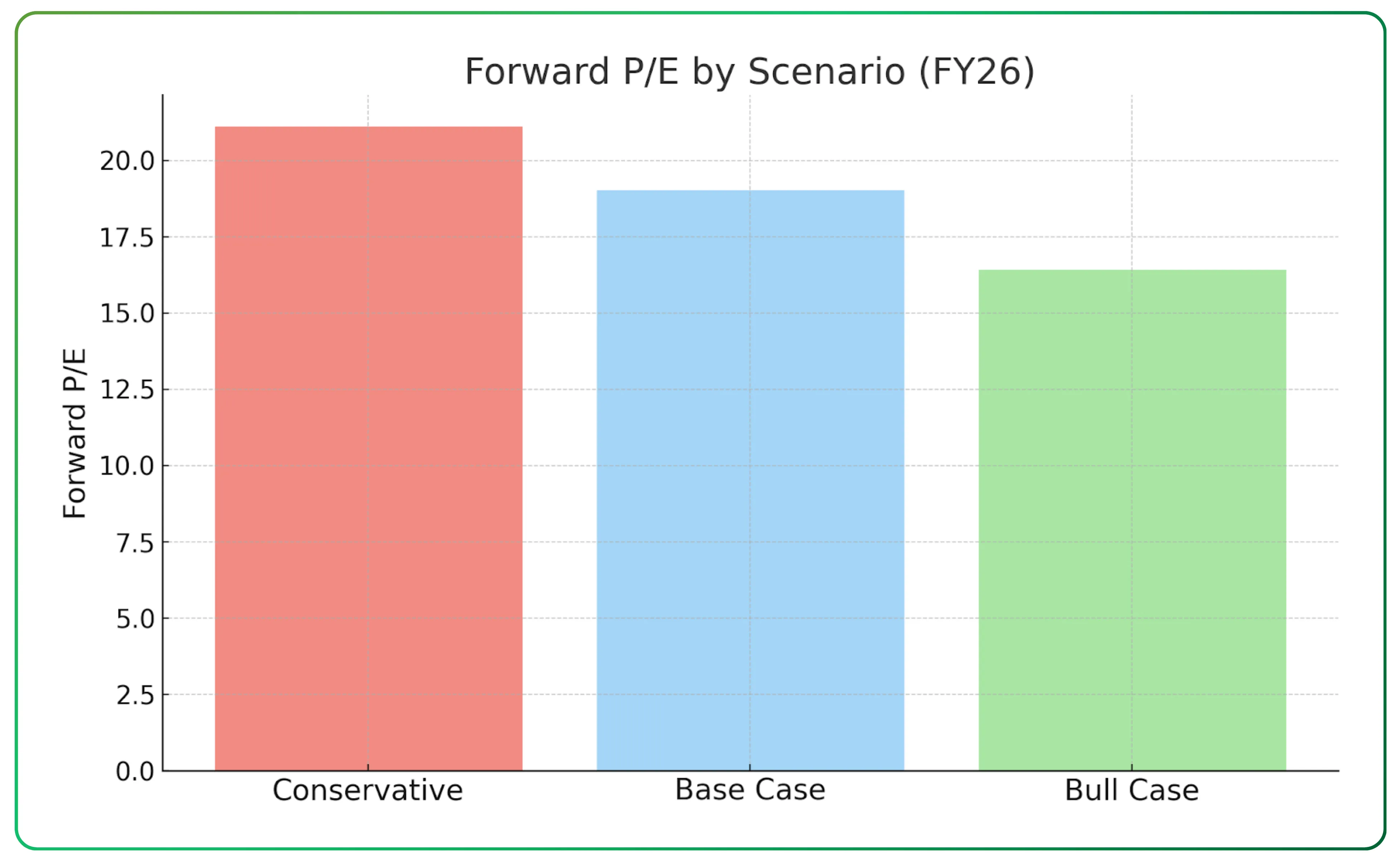

The table below uses this logic and builds three FY26 outcomes (conservative, base, and optimistic).

| Scenario | FY26 PAT (₹ cr) | FY26 EPS (₹) | Forward P/E at ₹752 |

|---|---|---|---|

| Conservative | 56 | 35.6 | 21.1× |

| Base Case | 62 | 39.5 | 19.0× |

| Bull Case | 72 | 45.8 | 16.4× |

At 12× trailing earnings, Control Print appears attractively valued on the surface. But when normalised FY26 earnings are used (which exclude exceptional income) the forward P/E falls in the 16–21× range, depending on the level of improvement in the second half of FY26. This still represents a reasonable valuation for a company with a high-margin consumables engine, a clean balance sheet, and long-term optionality in Track & Trace and single-serve packaging.

These valuation dynamics are central for investors assessing whether to buy Control Print or increase their allocation, especially as mutual funds have gradually increased exposure to the company.

Final Perspective

Control Print is a company that combines a stable, recurring-revenue core with the optionality of new growth engines. The coding and marking business alone is strong enough to support steady growth, thanks to a large installed base, high consumable dependence, and a debt-free balance sheet. On top of this, Track & Trace and the V-Shapes packaging vertical offer meaningful long-term upside if execution remains on track.

The next 12–24 months will hinge on three markers: the success of pharma pilots in Track & Trace, the reduction of Italy losses and approval of recyclable laminates, and the company’s ability to continue expanding its installed base in India. If these unfold as planned, Control Print could transition from a steady industrial player into a broader product-identification ecosystem.

Turn research into action, and trade smarter on CubePlus

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.