India’s marine industry is entering a period of meaningful expansion [India marine industry expansion 2025]. Ports, shipyards, logistics operators, and dredging companies are all benefiting from a clear government push to upgrade maritime infrastructure, deepen channels, modernise fleets, and shift more cargo movement to coastal and inland waterways. Roughly 95% of India’s trade volume moves through the sea [India trade volume maritime], and the country is finally building the capacity required for that scale.

Policy support has been consistent. Sagarmala, Maritime India Vision 2030 [Sagarmala Maritime India Vision 2030], and the longer-term Amrit Kaal agenda have turned ports into integrated logistics hubs, improved shipyard utilisation, and opened up new opportunities in dredging, offshore services, and ship repair. Defence orders continue to anchor the shipbuilding sector, while commercial shipbuilding and inland waterways are emerging as fresh long-term growth avenues.

The goal of this report is simple: present the full picture of India’s marine ecosystem in a way that’s factual, and grounded in data. Each segment is analysed with its key drivers, challenges, financial trends, and the positioning of leading companies.

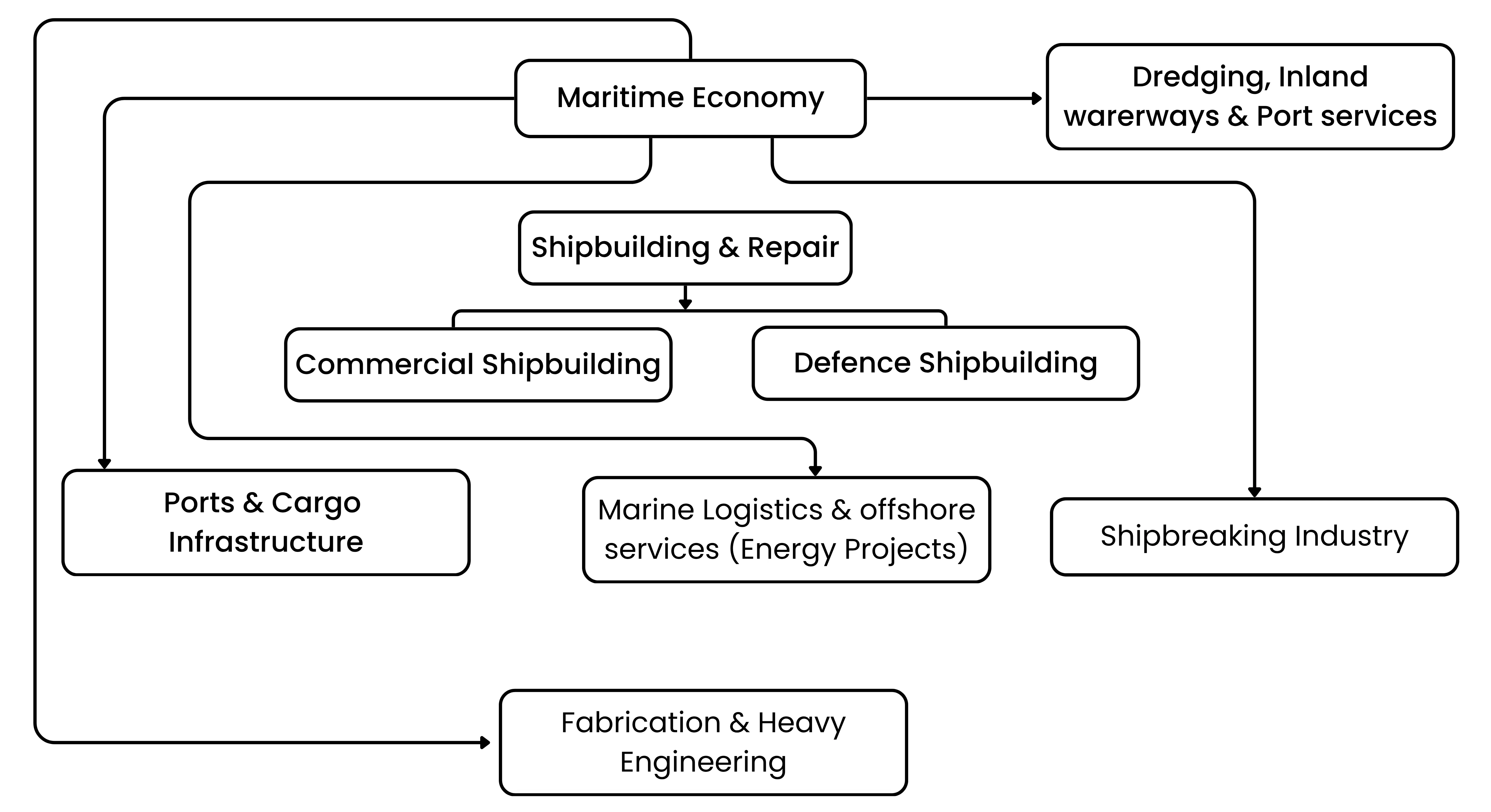

India’s Maritime Landscape

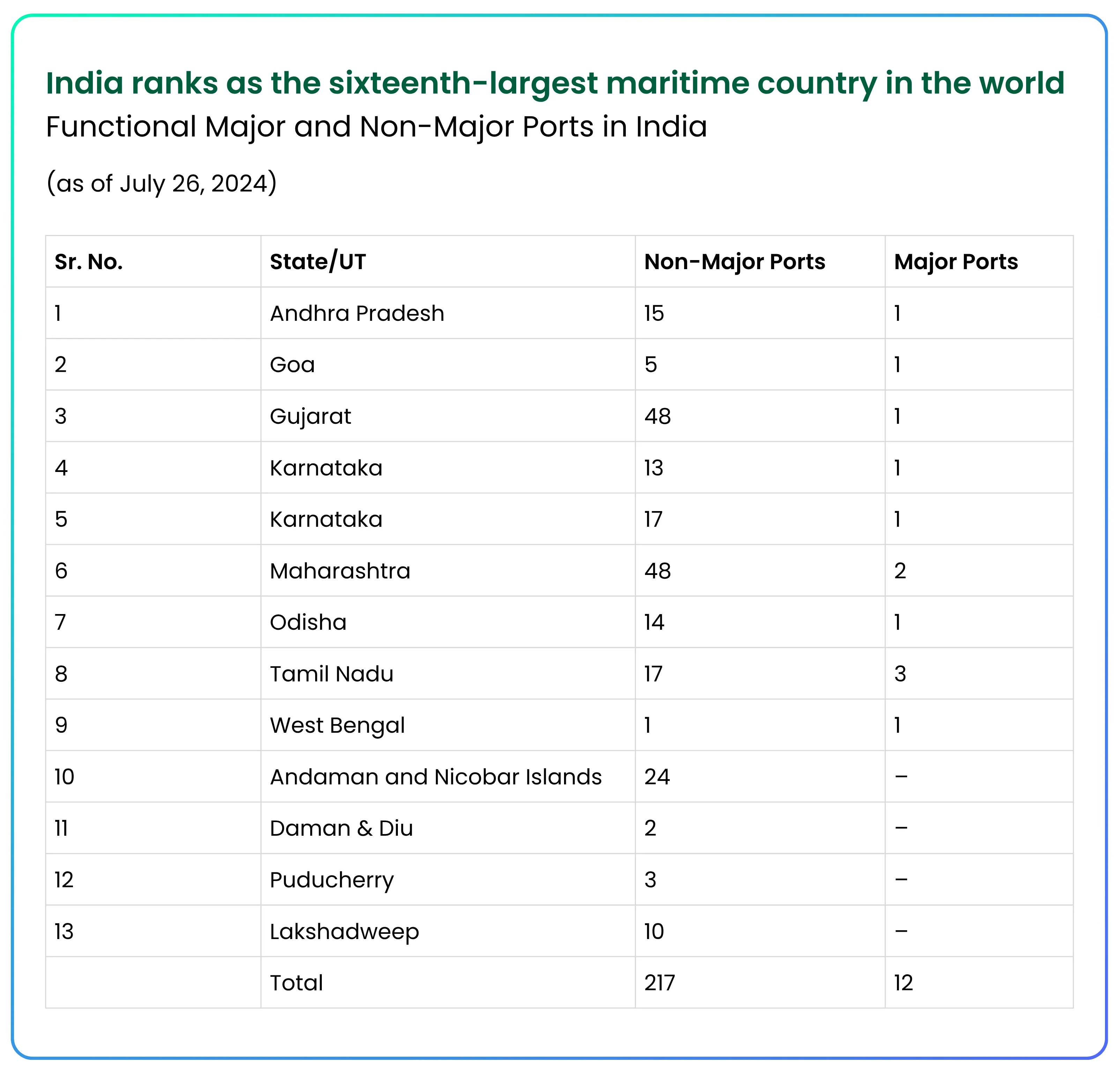

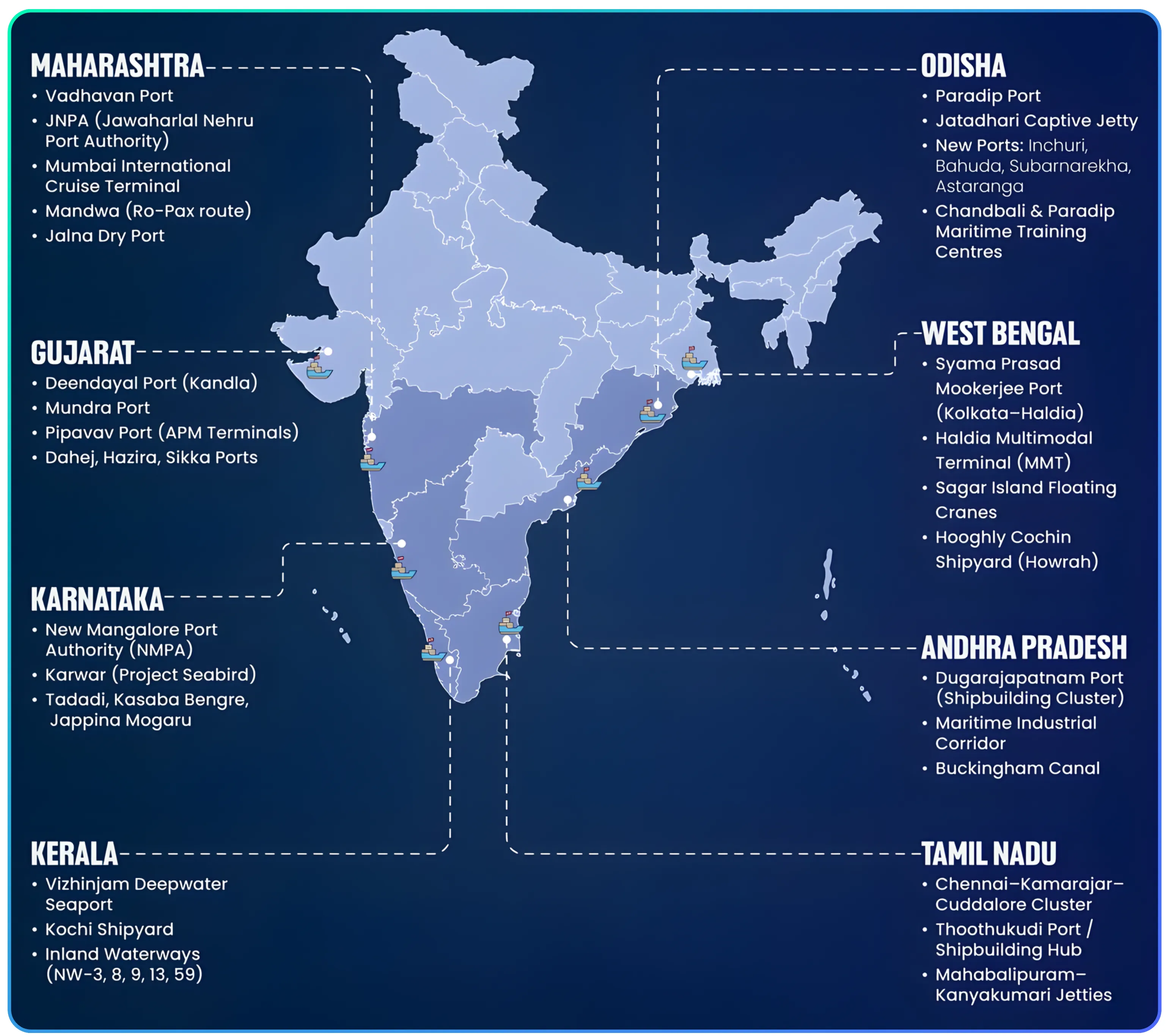

India’s coastline stretches over 7,500 km and sits along one of the world’s busiest maritime corridors. For years, much of this potential was underused. Ports lacked depth, shipyards were mostly focused on defence work, and coastal logistics played a minor role in freight movement.

That pattern is changing. Cargo volumes at both major and non-major ports have risen steadily, private operators have become dominant in containers, and the government has invested heavily in modernising port infrastructure. Inland water transport — once seen as a niche — is gaining traction through large-scale projects on the Ganga, Brahmaputra, and Barak rivers.

The broader direction is clear. India wants cheaper logistics, deeper and more efficient ports, stronger naval capabilities, and a shift toward cleaner, better-connected maritime assets. These efforts are raising demand for dredging, fleet expansion, ship repairs, and ancillary crafts required for day-to-day port operations. At the same time, shipbuilding is widening beyond defence as private yards and public-sector players explore commercial opportunities, offshore vessels, and green-tech platforms.

Taken together, the sector is moving from slow, project-driven growth to a more structural, policy-led expansion. The next sections break down each segment of the industry and the companies shaping it.

Section A: Shipbuilding and Ship Repair Industry

India’s shipbuilding sector has always been tied closely to defence spending. For decades, naval and coast guard orders kept the major public-sector yards busy, while commercial shipbuilding remained a much smaller activity. That balance is beginning to shift. The Navy’s long-term modernization plan still anchors the order books, but shipyards are now preparing for a broader mix of work—offshore vessels, large commercial carriers, green-energy platforms, and long-cycle repair contracts.

At the same time, the government wants India to become a serious commercial shipbuilding and ship-repair hub in Asia. Policy incentives, deeper capacity at major yards, and the interest of private players are gradually pushing the sector in that direction. What this really means is that shipbuilding in India is no longer a single-track defence story. It’s evolving into a more diversified industry supported by multi-year visibility.

With that background in place, let’s look at the major players and how each one is positioned.

Mazagon Dock Shipbuilders Ltd (MDL)

Mazagon Dock is the backbone of India’s defence shipbuilding program. Over the last decade, the yard has delivered destroyers, frigates, and submarines at a pace that has steadily improved its efficiency and profitability. It carries one of the strongest order books in the sector and has demonstrated the ability to execute complex naval platforms consistently ahead of schedule.

MDL’s recent performance also shows a meaningful shift in the company’s ambitions. Along with its traditional warship and submarine programs, the management has signalled interest in commercial shipbuilding, offshore structures, and export opportunities. The upcoming Tuticorin greenfield yard — being developed under the broader Maritime Amrit Kaal vision — is a major part of this shift. If executed well, it will give MDL the scale needed to compete in large commercial vessels, something India has lacked for years.

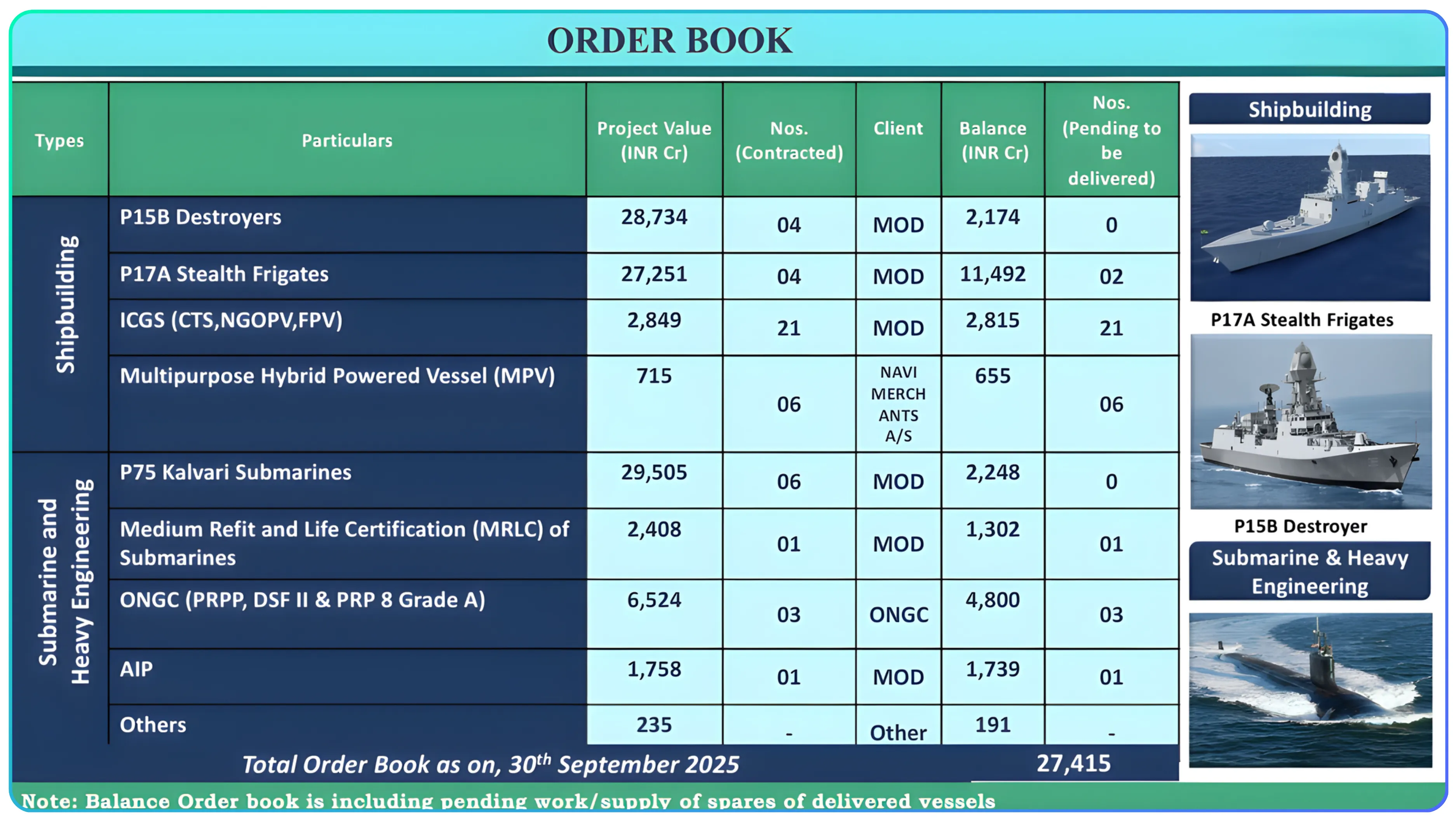

Financially, MDL is in a strong place. Revenue visibility remains high thanks to ongoing P15B destroyers, P17A frigates, and the next wave of submarine programs (P75 additional units and P75I). Margins remain healthy due to design expertise, accumulated learning curves, and a zero-debt balance sheet. The company has consistently highlighted its ability to deliver follow-on projects with better cost control, which explains the sustained improvement in operating profitability.

The next few years will hinge on three things: timely signing of submarine contracts, the evolution of the Landing Platform Dock (LPD) program, and how quickly the commercial shipbuilding initiative takes shape. But as a defence shipyard, MDL’s positioning is as strong as it has ever been. This expansion into commercial vessels and offshore structures marks a clear shift in Mazagon Dock Shipbuilders’ MDL strategy [Mazagon Dock Shipbuilders MDL strategy].

Cochin Shipyard Ltd (CSL)

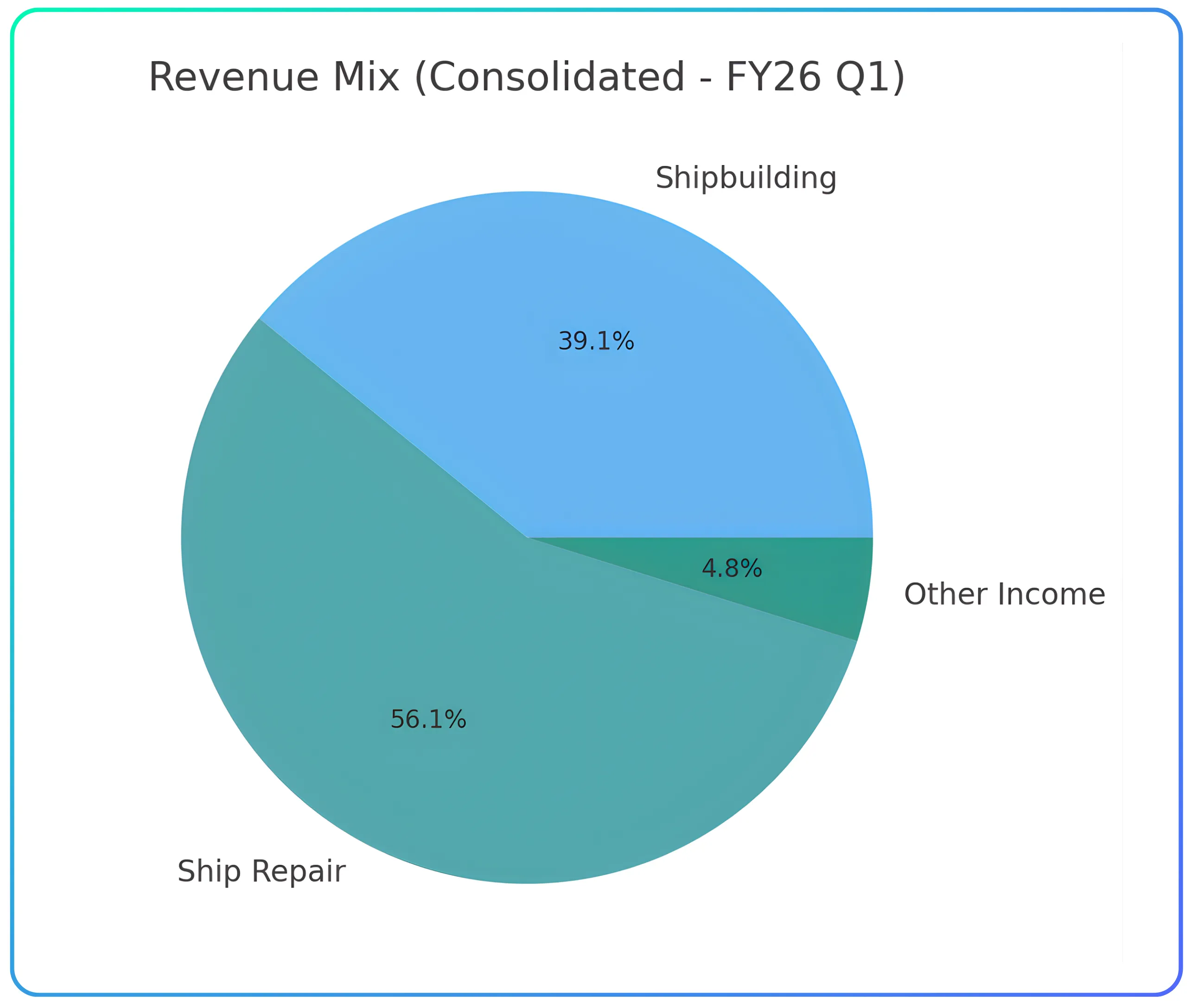

Cochin Shipyard is the most diversified major yard in India. It straddles defence, commercial shipbuilding, offshore structures, tugs, dredgers, and — most importantly — ship repair. Unlike its peers, CSL operates across multiple revenue streams, which gives the company more stability through business cycles.

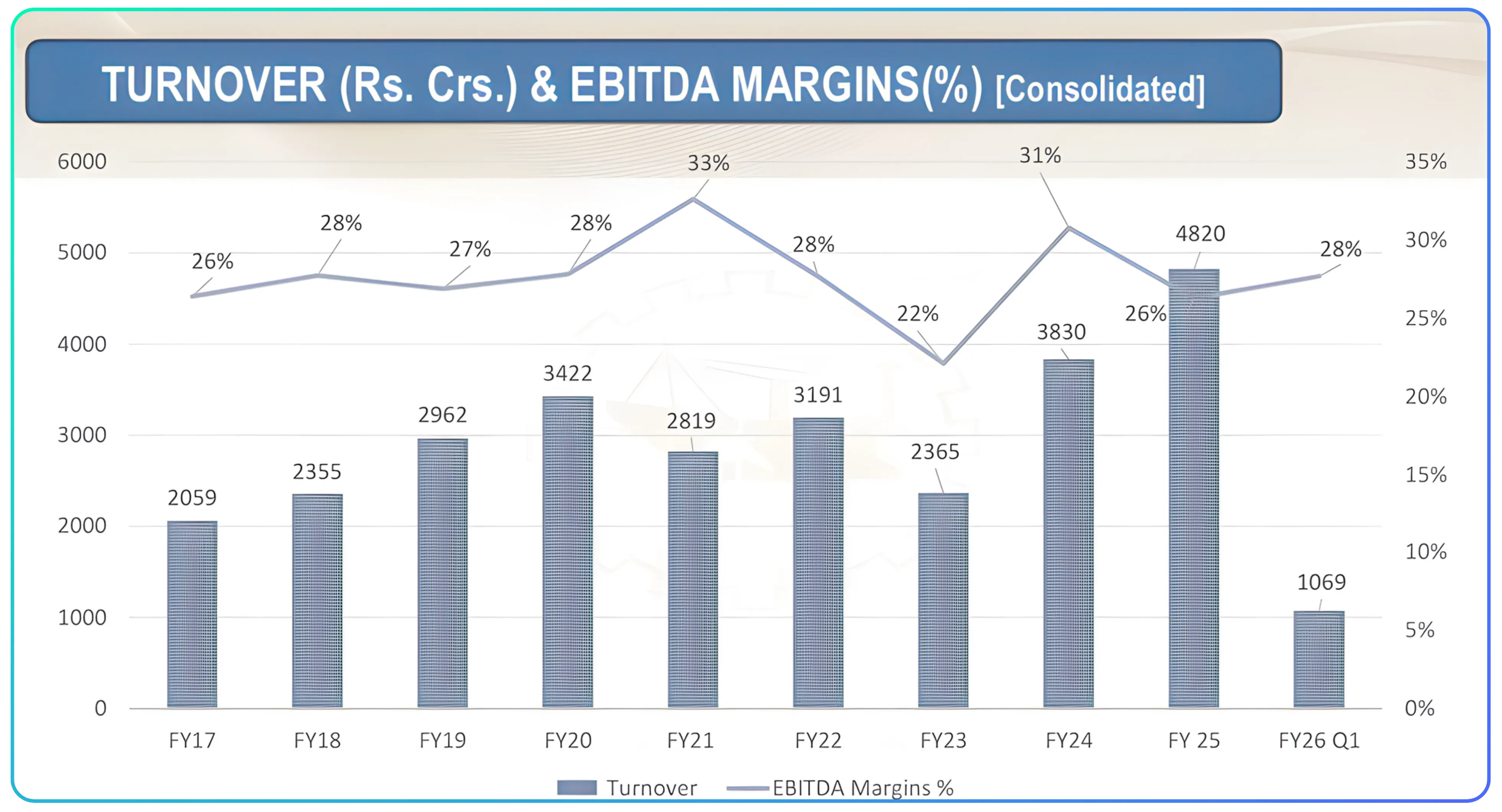

One of CSL’s biggest strengths is infrastructure. The International Ship Repair Facility (ISRF), the new dry dock capable of handling large vessels, and its strong presence in offshore support vessels place it in a unique category. Ship repair, in particular, is a long-term opportunity as global and domestic fleets age and India’s ports demand more frequent maintenance cycles. That business carries higher margins and lower working capital requirements, which supports the company’s financial profile. Ship repair remains one of the strongest pillars of the business [Cochin Shipyard CSL ship repair], supported by the new dry dock and ISRF facility.

CSL is also becoming an important partner in India’s push for green and technologically advanced vessels. Its collaboration with Dredging Corporation and IHC for the construction of large TSHD dredgers is a clear example. The yard is actively exploring opportunities in hydrogen-ready ships, electric ferries, and other alternative-fuel platforms—segments that could become mainstream over the next decade.

The real story with CSL is balance: steady defence work, consistent repair volumes, and a growing contribution from specialised commercial vessels. As the new facilities ramp up, throughput and margins should improve further.

Interested in how other niche players are shaping up? Read our full breakdown of Gravita India, VA Tech Wabag, and Deep Industries here.

Garden Reach Shipbuilders & Engineers (GRSE)

GRSE has carved out its space as a compact, efficient defence yard focused on smaller warships, patrol vessels, and export-ready platforms. It has a strong reputation for delivering ships with high indigenous content, and its engineering capabilities give it an edge in modular construction and auxiliary craft.

GRSE’s financial performance has been stable, supported by a healthy order book and disciplined execution. What differentiates the company is its attempt to broaden its portfolio beyond pure defence shipbuilding. The yard has been investing in ship repair, inland vessels, and pre-engineered steel structures—areas that help smooth earnings.

Among the defence yards, GRSE is often seen as the most operationally flexible. It may not compete directly with MDL or CSL on scale, but it has a reliable pipeline of patrol vessels, frigates, and coast guard platforms that keep utilisation healthy.

Private and Emerging Shipyards

While defence PSUs dominate the shipbuilding landscape, India does have a set of private and semi-private yards that contribute to commercial vessels, offshore structures, repairs, and specialised craft. Their scale is smaller, but their presence matters because they fill gaps that the larger yards don’t always address.

L&T Shipbuilding is the most prominent name in this group. The company once aimed to become a major private shipyard with substantial offshore capabilities, but over the years it has reduced its presence as market conditions tightened and large defence contracts remained concentrated within PSUs. Even so, the facility continues to have strong engineering capability and plays a supporting role in offshore vessels and specialised builds when opportunities arise. It remains strategically relevant but no longer shapes the industry’s capacity in the way it was initially expected to.

The capex (capital expenditure) for L&T Shipbuilding in 2025 is set at approximately ₹1,000 crore. This investment will be directed towards expanding and modernizing the Katupalli shipbuilding facility near Chennai. The project includes new fabrication and assembly shops, paint and blasting shops, warehouses, office and residential buildings, a skill development centre, and greenbelt landscaping—all within the existing 892-acre yard. Boost annual capacity from 15 ship builds and 30 repairs to 25 builds and 60 repairs

Beyond L&T, a cluster of smaller and emerging yards — including private operators in Goa, Gujarat, and Tamil Nadu — handle harbour craft, patrol boats, barges, and repair work. Their role tends to be project-specific rather than structural, but they add flexibility to the ecosystem and help expand India’s ability to serve niche requirements, especially for coastal and inland applications.

Commercial shipbuilding in India is still at an early stage compared to global leaders, but the presence of these yards, combined with renewed policy push, suggests that the next decade could look different from the last. If even a portion of domestic demand shifts from imports to local construction, these players stand to benefit meaningfully.

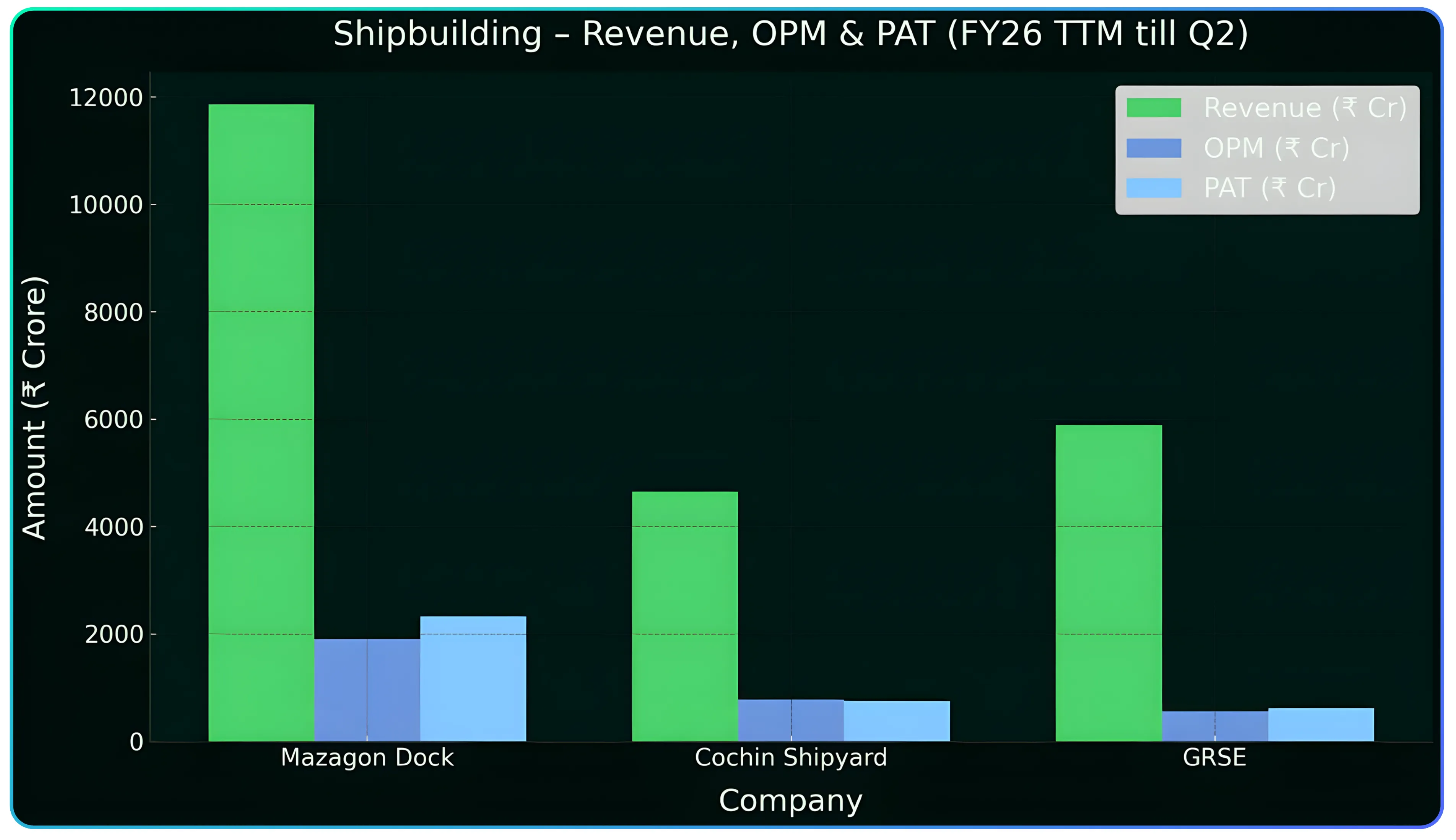

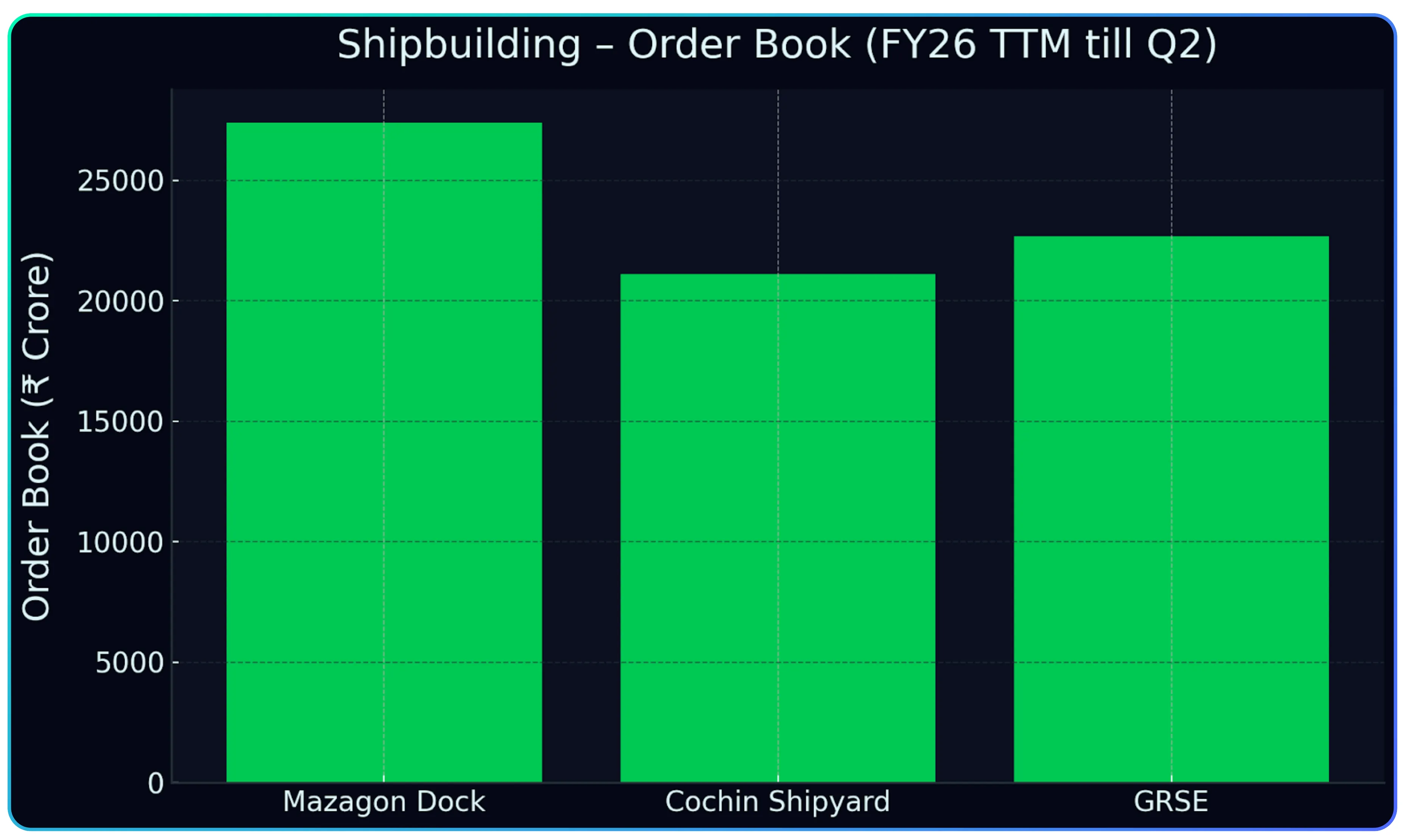

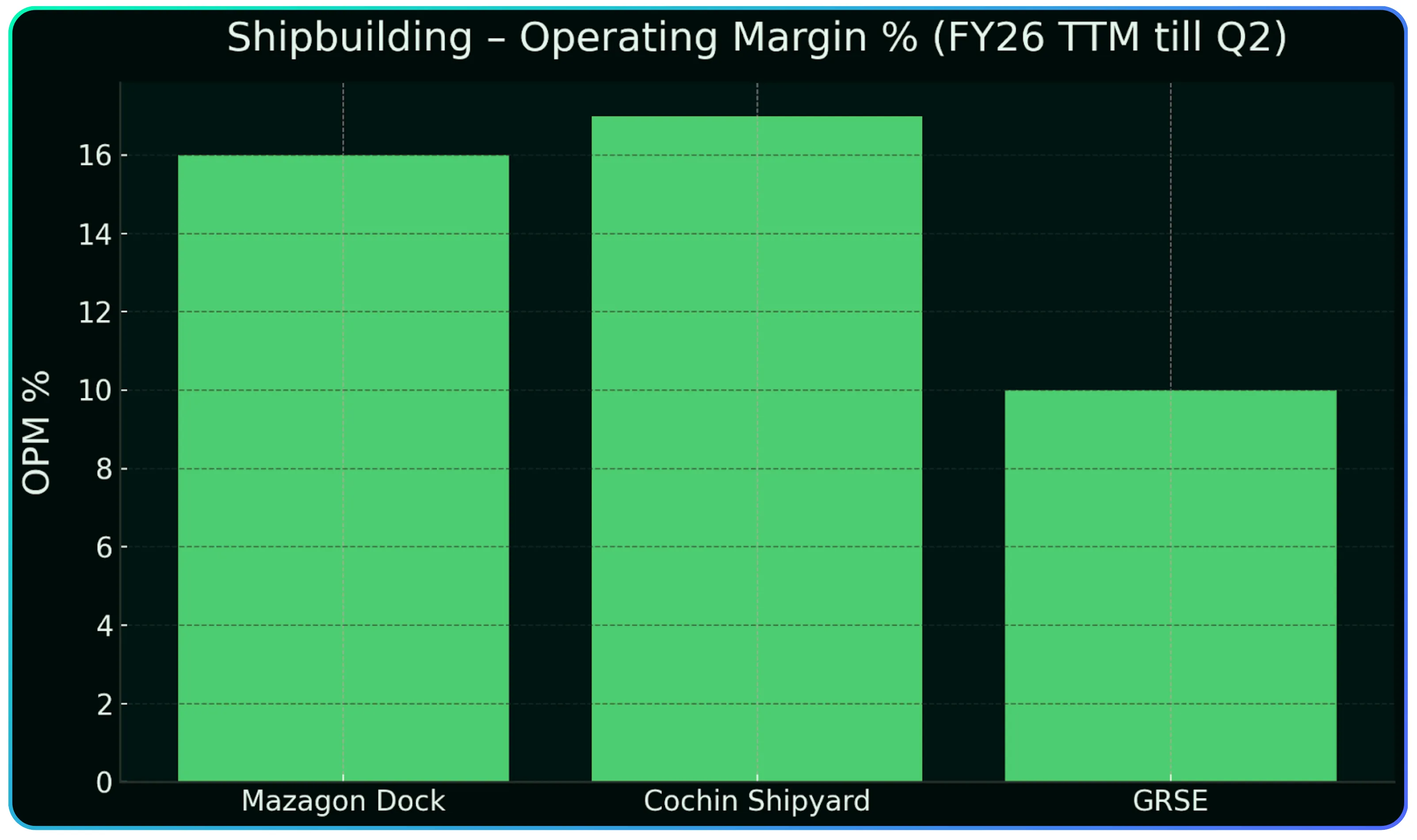

Shipbuilding Companies — Financial Comparison

These numbers also help frame the broader shipbuilding sector order book analysis as we look at execution visibility across the major defence yards.

FY26 ( TTM till Q2)

| Company | Revenue (₹ Crore) (TTM) | OPM (₹ Crore) | OPM % | PAT (₹ Crore) | Order Book (₹ Crore) |

|---|---|---|---|---|---|

| Mazagon Dock Shipbuilders (MDL) | 11,873 | 1,903 | 16% | 2,334 | 27,415 |

| Cochin Shipyard | 4,650 | 785 | 17% | 758 | 21,100 |

| GRSE | 5,900 | 564 | 10% | 616 | 22,680 |

Across the major defence shipyards, the numbers paint a clear picture of scale, stability, and long-cycle visibility. Mazagon Dock leads the pack with revenue of ₹11,873 crore on a TTM basis, supported by operating profit of ₹1,903 crore and a healthy 16% margin. Its profitability is matched by an exceptionally strong order book of ₹27,415 crore, which gives it one of the longest revenue runways in the sector. Cochin Shipyard follows with ₹4,650 crore in revenue and operating profit of ₹785 crore, translating into a solid 17% margin, anchored by a diverse mix of shipbuilding and high-margin repair work. Its order book of ₹21,100 crore provides multi-year execution comfort. GRSE remains a steady performer with ₹5,900 crore in revenue, operating profit of ₹564 crore and a 10% margin, backed by ₹22,680 crore of orders that ensure utilisation across patrol vessels, frigates, and auxiliary platforms. Together, these numbers show a sector driven by defence-led demand, strong execution, and deep order visibility across all three shipyards.

Summary of the Shipbuilding Ecosystem

India’s shipbuilding industry is still led by defence spending, but the overall picture is broadening. Mazagon Dock and Cochin Shipyard anchor the heavy work — frigates, destroyers, submarines, offshore vessels, and large repairs. GRSE supports the fleet with patrol and auxiliary craft. Private yards contribute flexibility, smaller builds, and offshore services. Together they form a supply chain that is gradually becoming more capable, more diverse, and more aligned with the government’s long-term maritime ambitions.

The runway ahead is shaped by three clear forces. Defence modernisation will continue to provide long-term visibility. Commercial shipbuilding, although still small, is getting fresh attention through initiatives like new greenfield yards and coastal economic zones. And ship repair — both military and commercial — is quietly turning into a stable, high-margin business as global and Indian fleets age.

With the shipbuilding chapter complete, we can now move into the next major pillar of the marine value chain.

If you’re exploring broader economic themes, take a look at our analysis on Why India Could Become the World’s Fastest-Growing Hospitality Market.

Section B: Ports and Cargo Infrastructure

India’s ports sit at the center of the country’s maritime economy. They handle almost all international trade by volume, and over the past decade they have evolved from simple cargo-handling locations into integrated logistics hubs with rail links, inland depots, warehousing, and coastal connectivity. The shift has been deliberate. As India’s manufacturing and consumption base expanded, ports had to scale not just capacity but efficiency — deeper drafts, faster turnaround, and multimodal linkages.

The bigger change, though, is structural. Private ports have steadily taken a larger share of container and cargo traffic, driven by better infrastructure, faster evacuation, and customer-focused operations. At the same time, major public ports are undergoing upgrades to remain competitive. The result is an ecosystem where capacity is rising on both sides, competition is greater, and cargo movement is becoming more predictable.

State and central policies have played an important role. Under Sagarmala, port-led development became a national priority. Maritime India Vision 2030 added targets for deeper berths, more mechanisation, transshipment hubs, and higher operational efficiency. Together these initiatives pushed ports to modernise, expand, and integrate with inland logistics corridors such as dedicated freight routes, coastal shipping lanes, and the emerging inland waterway network.

As cargo volumes shift — with coal evolving, containers rising, and liquid cargo staying steady — ports have had to diversify revenue streams and focus more on value-added logistics. This is where private operators, particularly Adani Ports, have moved much faster than their peers.

With that backdrop, let’s move to the leading player.

Adani Ports and Special Economic Zone (APSEZ)

Adani Ports has become synonymous with India’s private port expansion. Over the last decade, the company built and acquired a network of strategically placed ports across the east and west coasts, allowing it to handle a wide range of cargo — containers, dry bulk, liquid, LNG, and coastal movement. What sets APSEZ apart is its integrated model [Adani Ports APSEZ logistics model]: ports are backed by last-mile rail connectivity, inland depots, logistics parks, and warehousing facilities that help customers move cargo more efficiently.

The company highlights consistent cargo growth and a strong pipeline of capacity additions. Volume performance across major ports such as Mundra, Hazira, Kattupalli, Krishnapatnam, and Gangavaram remains healthy, supported by industrial activity, energy imports, container trade, and the company's ability to divert cargo within its network when required. This multi-port strategy reduces volatility and ensures stable utilisation across the system.

APSEZ is also investing heavily in deeper drafts, mechanisation, and multimodal connectivity. The ongoing expansions, including LNG terminals, logistics parks, and dedicated rail infrastructure, improve operating margins and help the company move up the logistics value chain. This aligns well with the broader shift in India’s maritime policy, where ports are expected not just to handle cargo but to support entire supply chains end-to-end.

Financially, APSEZ shows a consistent trend: expanding cargo volumes, improving margins, strong cash flows, and a long-term capex cycle that is funded through a mix of internal accruals and controlled leverage. The company’s ability to integrate acquisitions quickly and drive efficiency improvements remains one of its biggest strengths.

What stands out is the shift from being a large port operator to becoming a logistics ecosystem player. With inland depots, rail services, cold chain facilities, and coastal services, APSEZ is positioning itself as a full-service logistics provider — a model that strengthens customer stickiness and reduces sensitivity to individual cargo cycles.

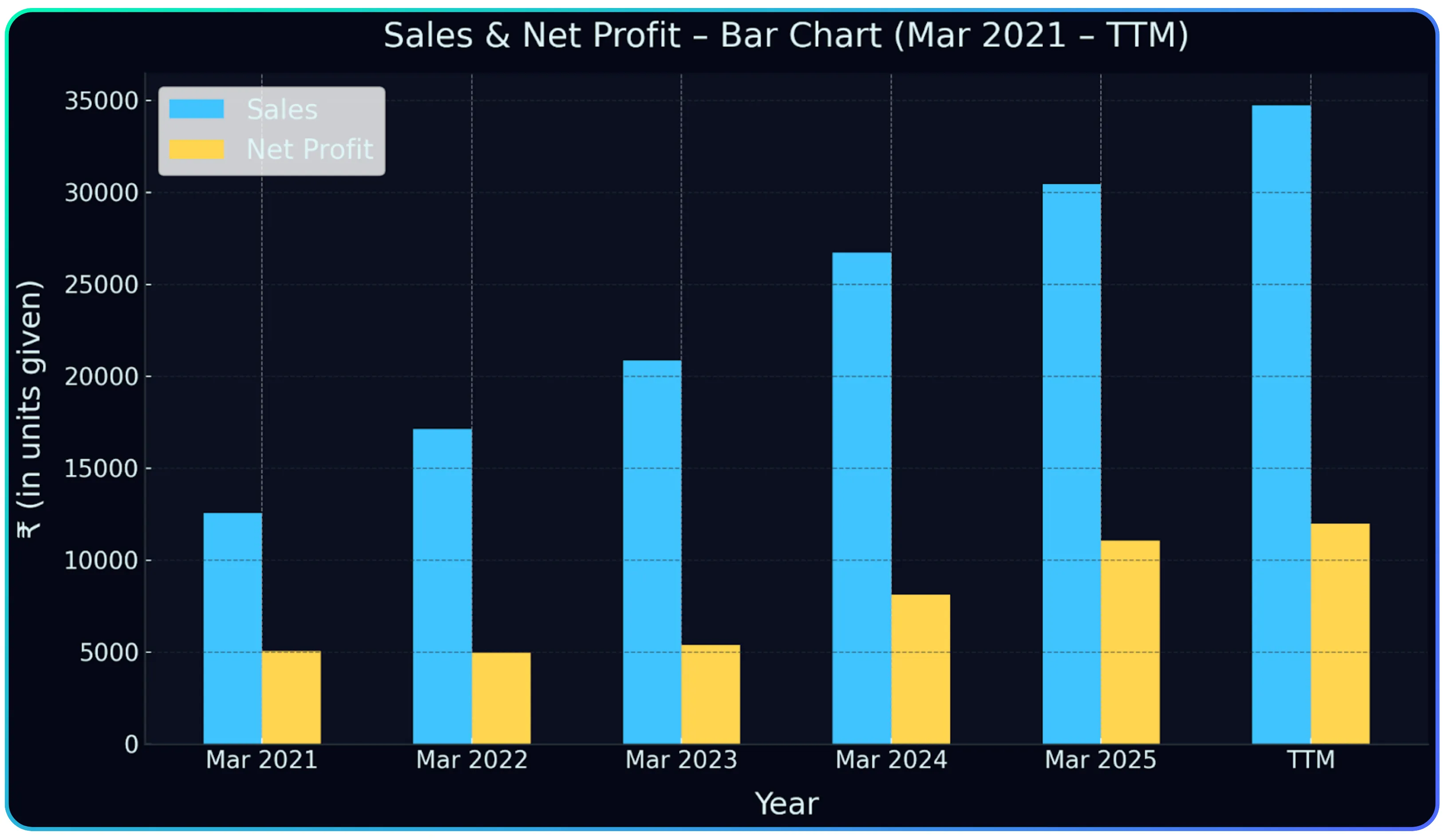

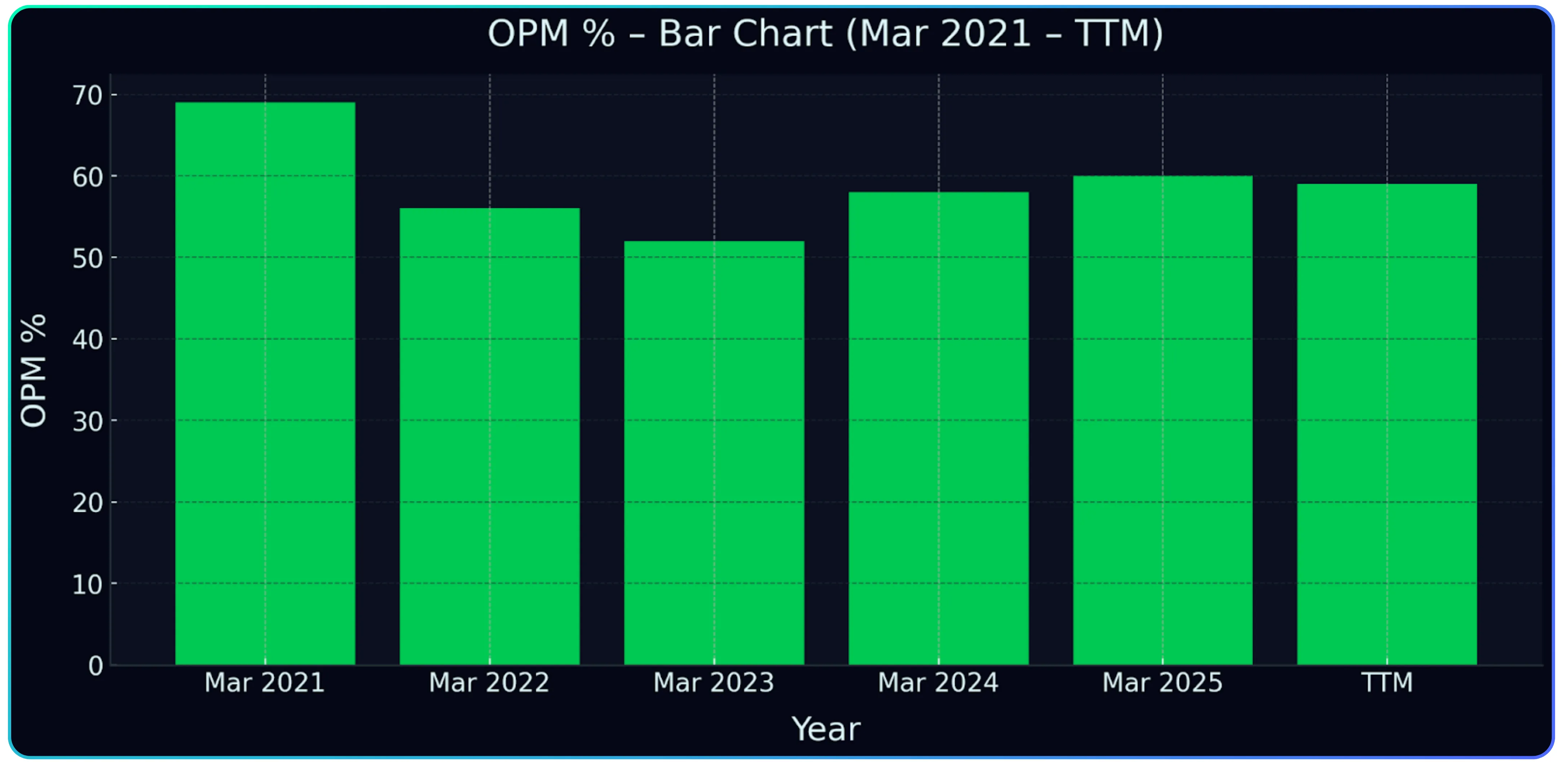

Ports — Financials

Adani Ports (APSEZ) - (Mar 2021 – TTM)

| Year | Sales | OPM % | Net Profit |

|---|---|---|---|

| Mar 2021 | 12,550 | 69% | 5,049 |

| Mar 2022 | 17,119 | 56% | 4,953 |

| Mar 2023 | 20,852 | 52% | 5,391 |

| Mar 2024 | 26,711 | 58% | 8,104 |

| Mar 2025 | 30,475 | 60% | 11,061 |

| TTM | 34,746 | 59% | 11,972 |

Adani Ports has shown a steady and confident expansion in both scale and profitability over the last five years, reflecting the strength of its integrated logistics model. Revenue has climbed from ₹12,550 crore in FY21 to ₹34,746 crore on a TTM basis, driven by rising cargo volumes, deeper port capacity, and the rapid growth of its logistics and marine services verticals. Profitability has remained resilient through market cycles, with operating margins largely holding in the mid-to-high range despite fluctuations in cargo mix; the latest TTM margin stands at 59%. Net profit has more than doubled over the period, rising from ₹5,049 crore in FY21 to ₹11,972 crore, supported by operating leverage, better asset utilisation, and a portfolio of ports that now spans both coasts. The financial trajectory underscores APSEZ’s position as the country’s dominant private port operator with the scale, efficiency, and balance sheet strength to capture long-term growth in India’s maritime and logistics ecosystem.

Bringing It All Together

This brings us to the end of Part 1, where we covered the foundations of India’s maritime ecosystem — the shipyards, defence platforms, commercial builds, ports, and the broader structural shifts in capacity and capability. The story doesn’t end here. Dredging, inland waterways, and marine logistics are equally important pillars shaping India’s maritime future.

To see how these segments connect and where the next wave of growth is emerging, continue reading in Part 2.

Turn research into action — trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.