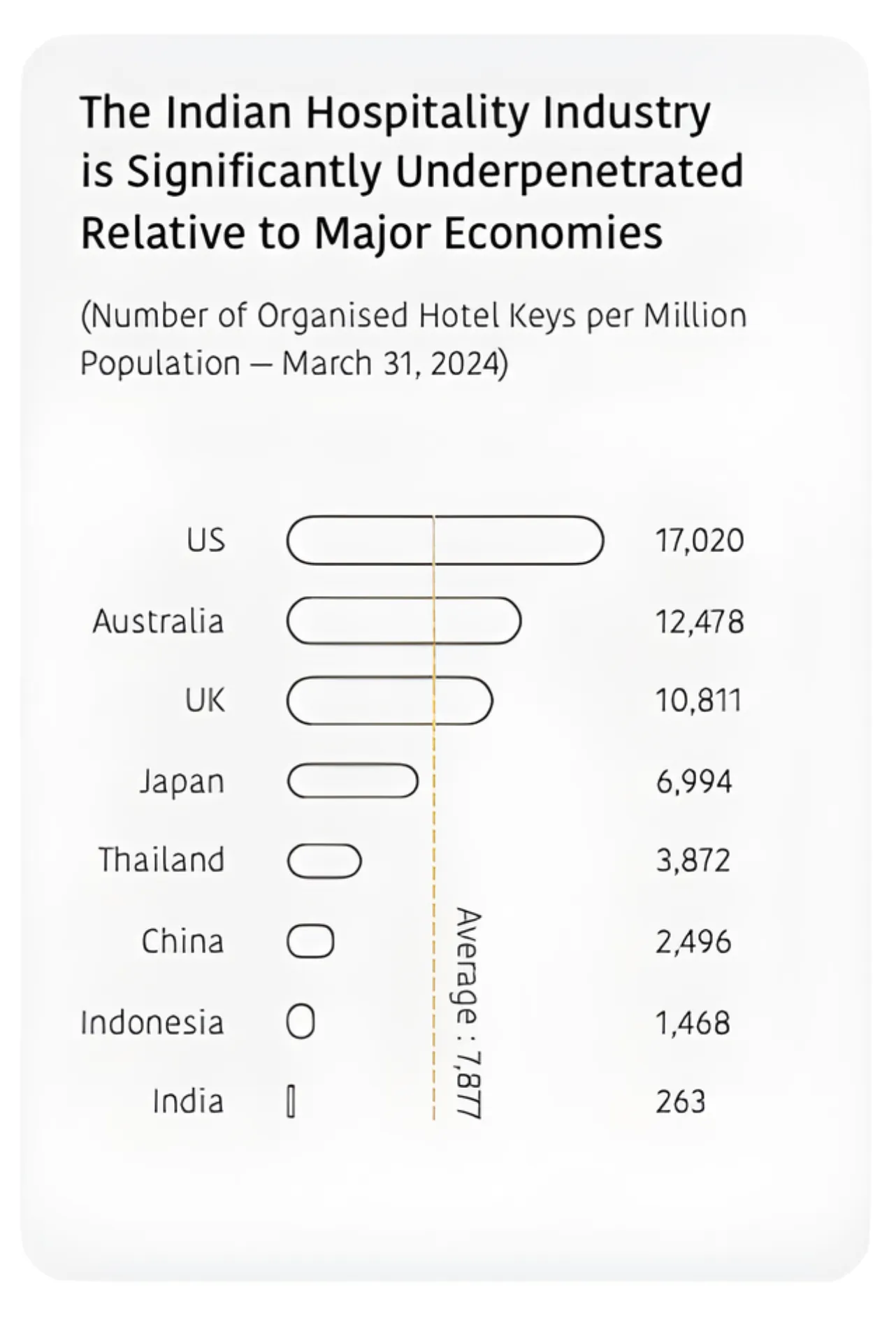

India’s hospitality industry is in the middle of a major growth phase, setting new records in FY25. Strong domestic travel, better infrastructure, a growing middle class, and steady government backing are driving the momentum. In 2024, the sector added ₹20.9 trillion to the country’s GDP 19.9% from 2019 and supported about 46.3 million jobs, roughly 9.1% of total employment. Yet, with only 263 organized hotel rooms per million people versus a global average of 7,877, India is still far behind, leaving huge room for expansion.

Global Economic Context

The global economy expanded by 3.3% in 2024, marking a slower pace than in previous years. As per the IMF’s April 2025 World Economic Outlook, growth is expected to ease further to 2.8% in 2025 before picking up slightly to 3.0% in 2026. Advanced economies grew by 1.8% in 2024, while emerging and developing markets delivered stronger growth at 4.3%. India and China remained the key engines of global growth, posting 6.5% and 5.0% respectively. Even with these challenges, the world economy has held up relatively well. Inflation has cooled sharply (from 4.6% in 2023 to 2.6% in 2024) providing some relief. Still, persistent trade tensions and growing protectionist policies continue to cloud the outlook.

Indian Economy: Strong Fundamentals

India continues to stand out as the world’s fastest-growing major economy, expanding by 6.5% in FY25 despite a challenging global backdrop. The Reserve Bank of India expects similar growth in FY26, while the IMF projects India’s per capita nominal GDP to rise at a healthy 9.2% CAGR over the next five years.

This momentum rests on solid fundamentals. Private consumption, which makes up nearly 57% of GDP, grew 7.6% during the year, showing a strong rebound. Capital investment also remained firm—Gross Fixed Capital Formation rose 6.1% to 33.4% of GDP—thanks to higher government spending and a steady pickup in private investment. The services sector continues to be India’s growth engine, expanding 7.2% in FY25, led by financial services, healthcare, hospitality, and public administration. The job market also strengthened, with unemployment easing to 4.9% in FY24, while foreign exchange reserves climbed to $645 billion by March 2025.

A broader structural shift is underway as India’s middle class expands rapidly, expected to represent 50–70% of the population by 2030. The FY26 Union Budget accelerated this trend with major tax reforms, raising the basic exemption limit to ₹4 lakh and exempting incomes up to ₹12 lakh under the new regime. The move is set to lift disposable incomes and further fuel consumption-led growth.

Global Hospitality and Tourism Industry

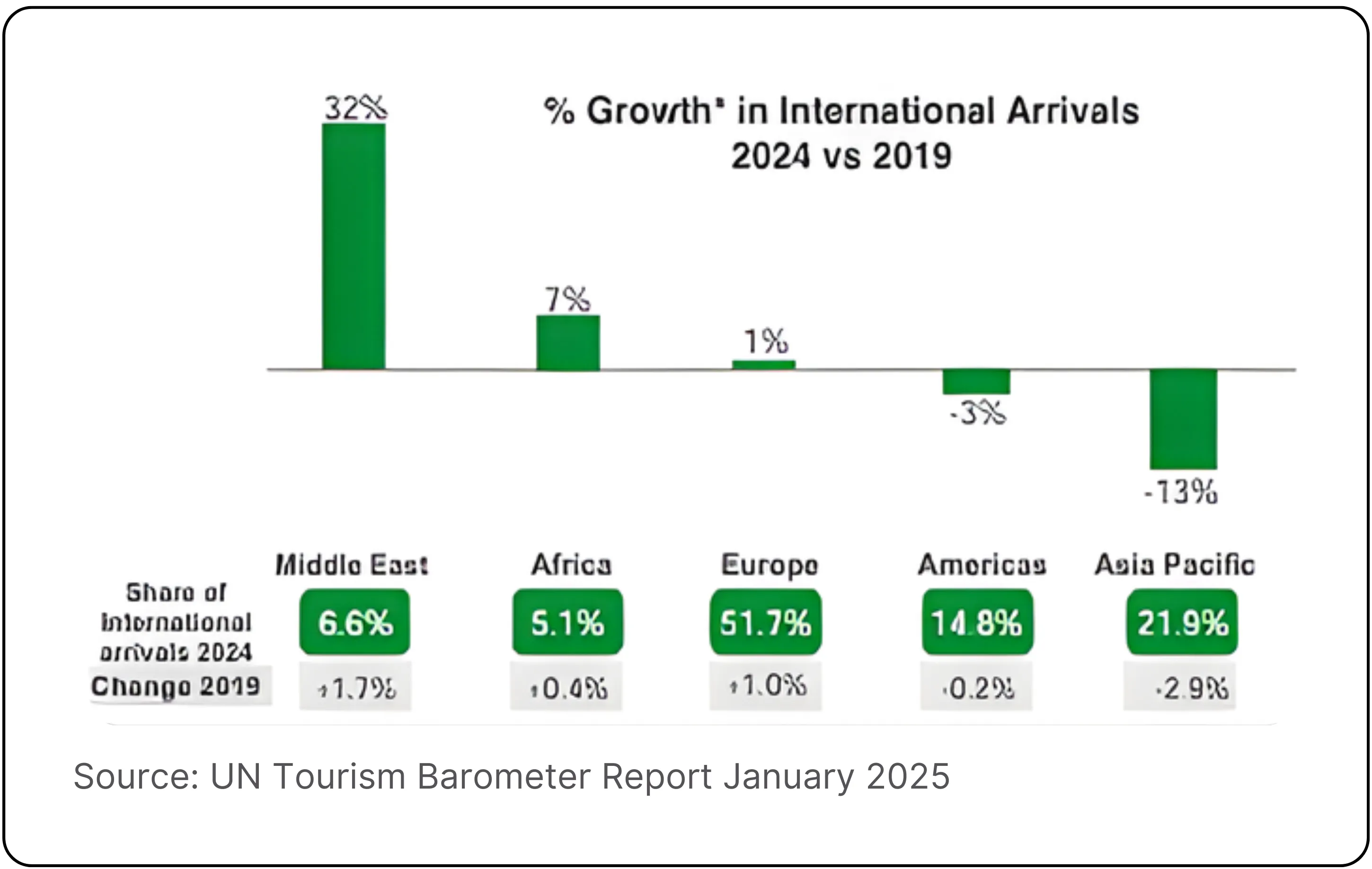

The global hospitality and tourism industry made a strong comeback in 2024, nearly reaching pre-pandemic levels. International tourist arrivals climbed to 1.4 billion (an 11% rise from 2023) recovering 99% of 2019 volumes. Europe remained the top destination, drawing 747 million visitors, which accounted for 52% of global arrivals. That’s a 5% year-on-year increase and slightly above its 2019 benchmark.

The Asia-Pacific region also rebounded sharply, welcoming 316 million international visitors in 2024. Its global share rose to 22% from 18% a year earlier, making it the fastest-growing region with 33% annual growth, though still at 87% of pre-pandemic levels.

Tourism export revenues, including passenger transport, hit a record $1.9 trillion, up 3% from 2023 and 4% higher than 2019 in real terms. The World Travel & Tourism Council (WTTC) reported that the sector contributed 10% ($10.9 trillion) to global GDP and supported 356.6 million jobs, about 10.6% of total employment worldwide.

The outlook for 2025 remains upbeat. The UN World Tourism Organisation expects international arrivals to grow another 3–5%, while 64% of industry professionals anticipate stronger performance ahead. The WTTC projects the sector’s economic output to reach $11.7 trillion in 2025, supporting roughly 371 million jobs across the world.

Indian Hospitality Industry Overview

India’s hospitality industry covers a wide and varied landscape; from luxury resorts and branded hotels to budget stays, midscale properties, serviced apartments, and new-age lodging options like homestays and boutique stays. It’s also closely tied to complementary segments such as restaurants, event spaces, wellness services, and branded residences, all of which add depth and value to the broader ecosystem.

Interested in another sector with equally strong consumption tailwinds? Explore our detailed report on Unlocking Growth in India’s $90 Billion Jewellery Industry to see how premiumisation and export demand are shaping the next wave of opportunities.

Market Performance

In 2024, India’s hospitality industry strengthened its position as a key driver of economic activity. Hotel transactions totaled $348 million during the year, reflecting strong investor confidence and upbeat market sentiment. The sector maintained healthy occupancy levels of around 63–65%, supported by steady demand across segments. Average room rates hovered between ₹7,800 and ₹8,000, while revenue per available room (RevPAR) stood at ₹5,000–₹5,200 among Premium Hotels, showing a well-balanced mix of occupancy and pricing strength.

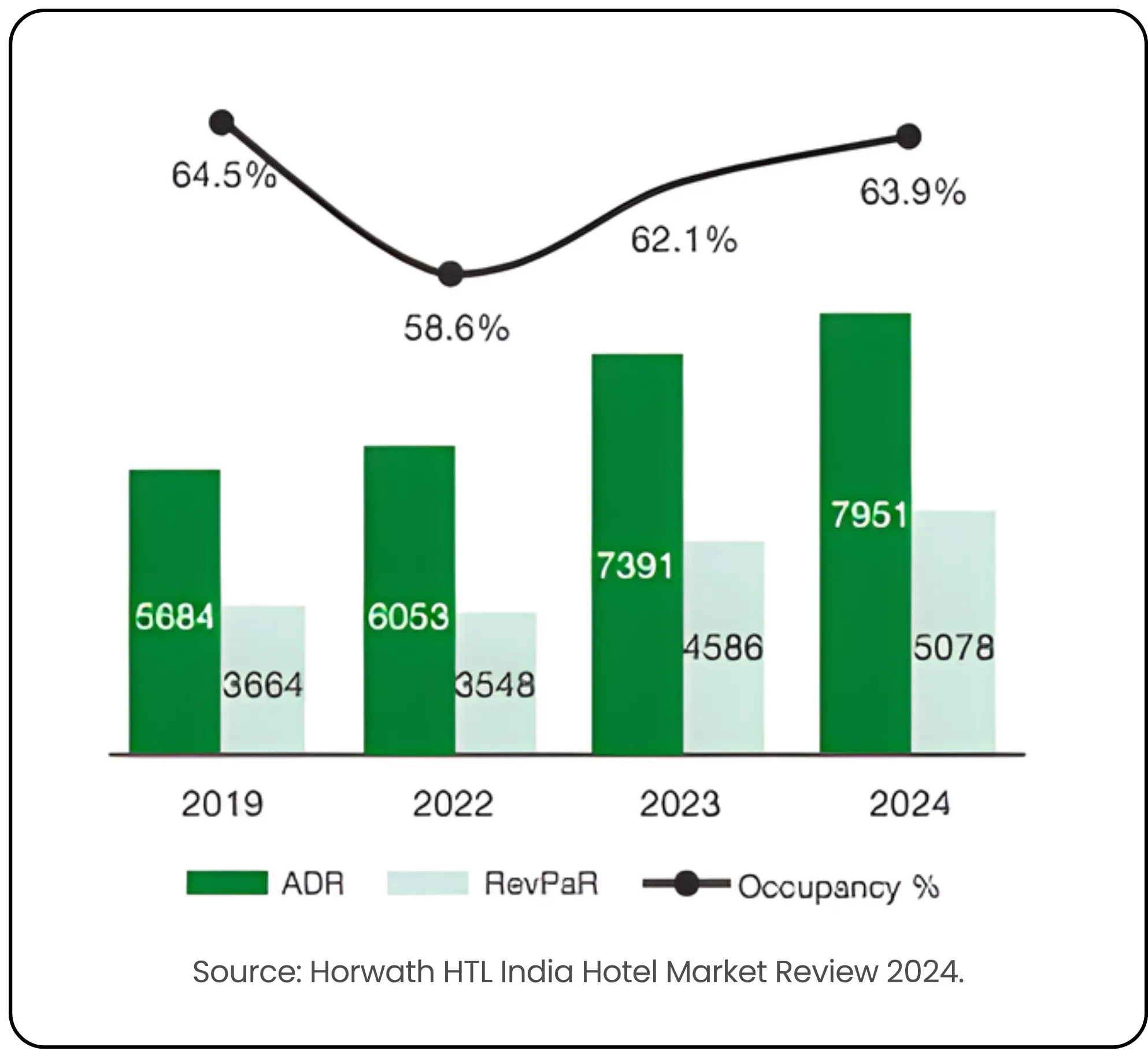

As per the India Hotel Market Review 2024, national occupancy reached 63.9%, slightly up from 62.1% in 2023, and only a touch below the 2019 level of 64.5%. What stands out, however, is the sharp rise in revenue—daily revenue per room was 82% higher than 2019, signaling strong growth in both market capacity and value. The average daily rate (ADR) climbed 7.5% year-on-year to ₹7,951, while RevPAR rose 10.7% to ₹5,078.

Among cities, Udaipur posted the highest ADR, followed by Mumbai, Goa, and New Delhi, underlining sustained demand for premium leisure and business destinations. Around 14,400 new rooms were added across 169 hotels in 2024, pushing India’s total branded hotel inventory to roughly 200,000 keys. Interestingly, more than two-thirds of new additions came from emerging locations beyond the top 10 markets; evidence of the sector’s expanding footprint and growing diversification.

Growth Drivers

Domestic Tourism Boom

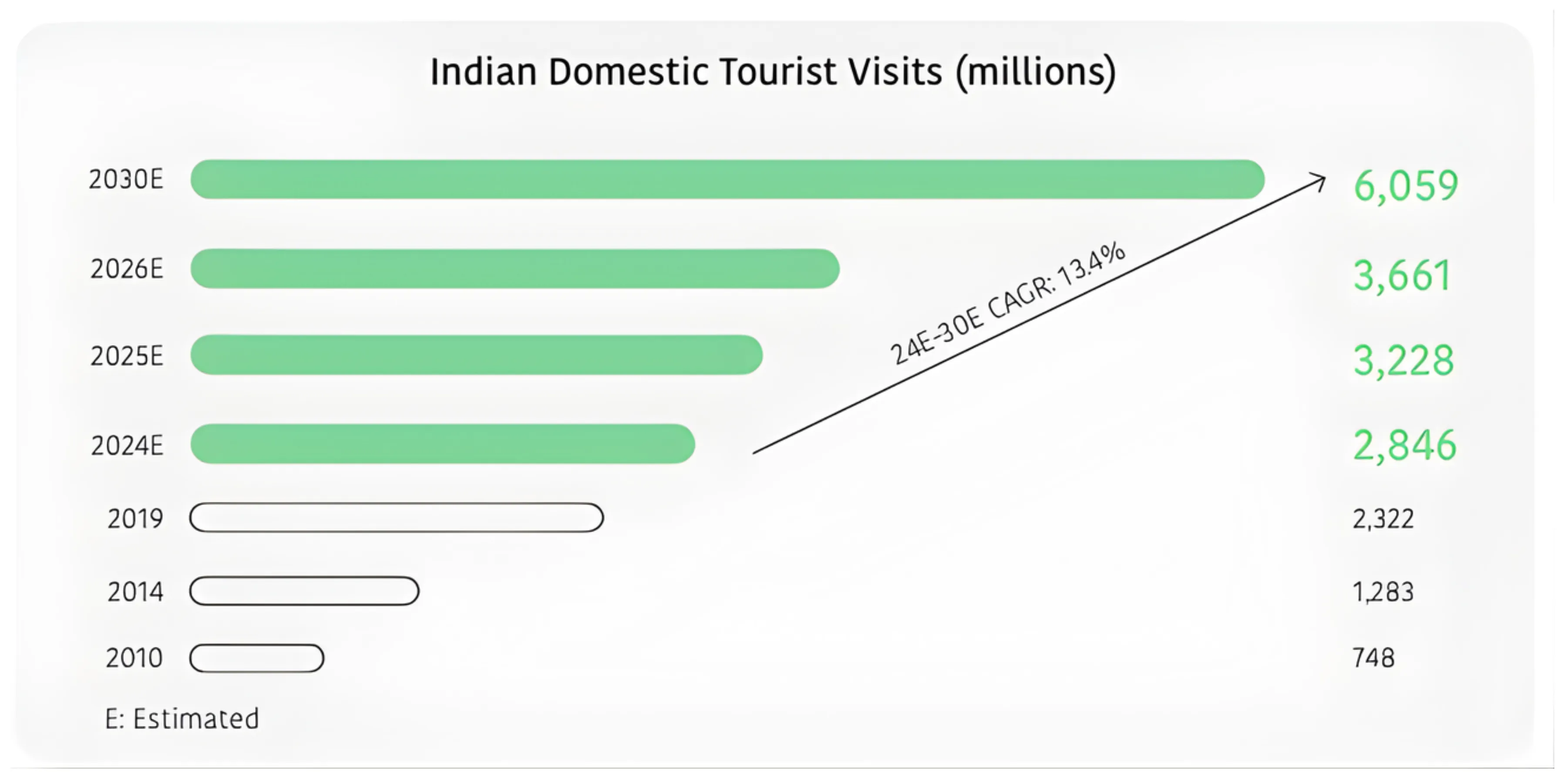

Domestic travel remains the strongest pillar of India’s hospitality growth story. Tourist visits within the country are set to more than double (from 2.8 billion in 2024 to over 6 billion by 2030) translating to a CAGR of 13.4%. Air travel, a key indicator of tourism health, has already surpassed pre-pandemic levels, with domestic passenger traffic up 12% in FY25 compared to 2019.

International Tourism Recovery

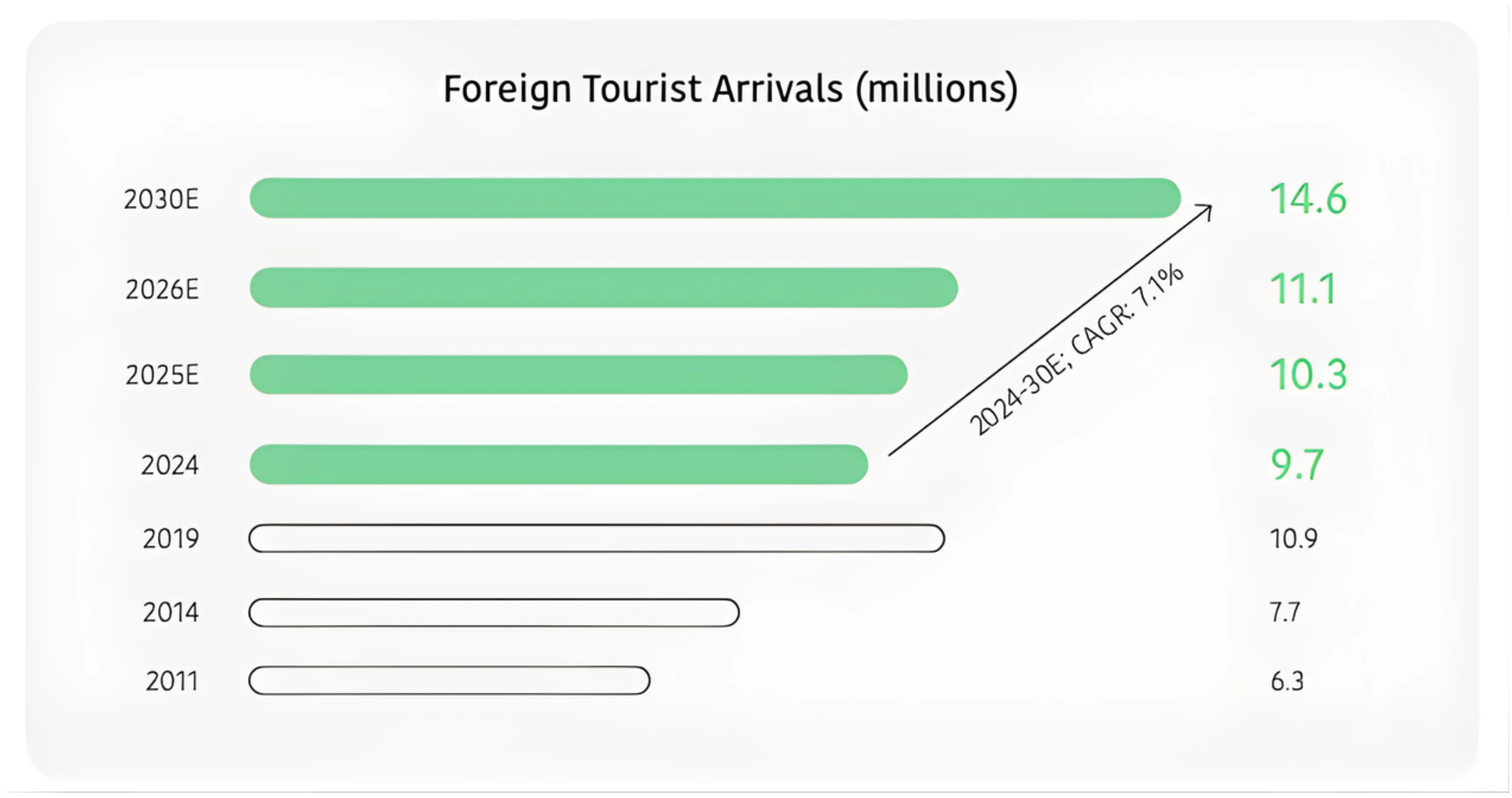

India’s global tourism appeal has bounced back sharply, powered by its cultural diversity, better connectivity, and improved infrastructure. Foreign tourist arrivals touched 9.7 million in 2024, up from 9.23 million a year earlier, recovering 88% of pre-COVID levels. Initiatives such as new tourism circuits, the PRASHAD scheme, and easier visa rules have strengthened India’s global image. Going forward, foreign arrivals are expected to climb to 14.6 million by 2030—a 7.1% CAGR—while outbound travel continues to surge, with 30.2 million Indians traveling abroad in 2024, 12% above 2019 levels.

Infrastructure Push

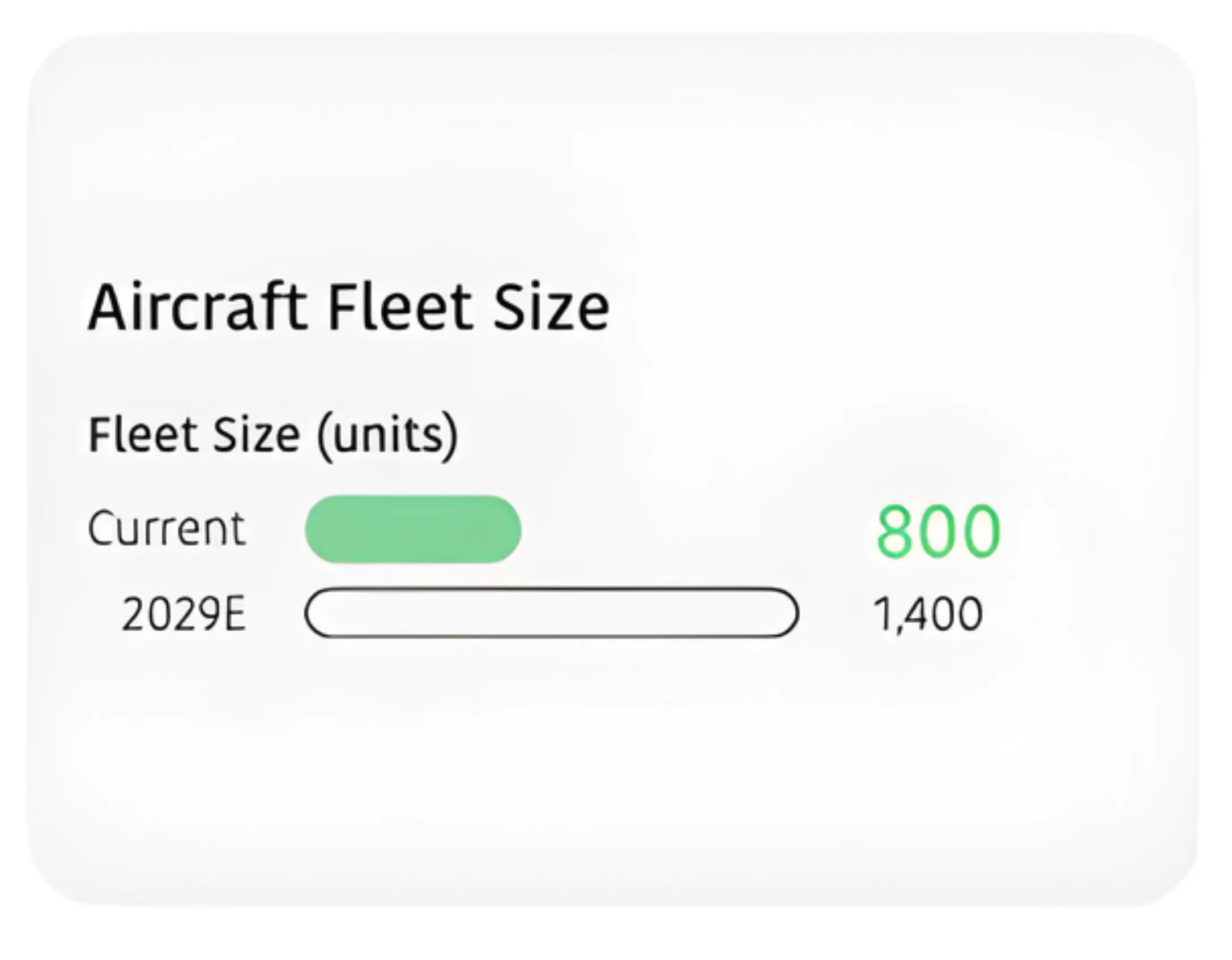

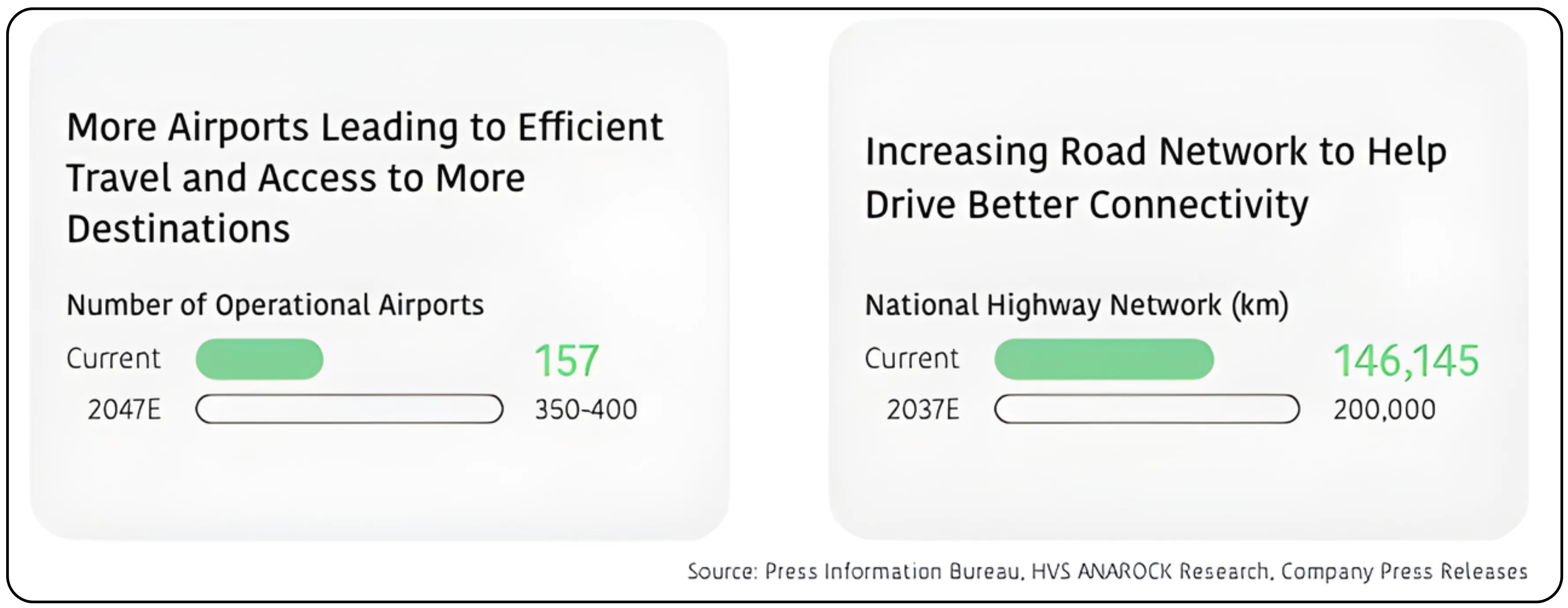

The FY26 Union Budget earmarked ₹1,121 billion for infrastructure, aimed at enhancing air, road, and rail connectivity. The country plans to expand its operational airports from 157 in 2024 to 350–400 by 2047, while airline fleets are projected to grow from 800 to 1,400 aircraft by 2029.

The national highway network is also set to expand from 1.46 lakh km to 2 lakh km by 2037, cutting travel time and improving accessibility. In FY25 alone, 10 new greenfield airports became operational, bringing the total to 159, while large projects in Noida (Jewar) and Navi Mumbai near completion for launch in 2025.

Policy Support and Incentives

Tourism has emerged as a national growth priority. The Union Budget 2025–26 allocated ₹25 billion to the Ministry of Tourism, with most of it directed toward Central Schemes and development projects. India now offers e-visas to citizens of 167 countries under nine categories, simplifying travel entry. Campaigns like Dekho Apna Desh and Incredible India continue to boost visibility, while the government urges states to grant tourism “industry status,” unlocking benefits like tax incentives, land concessions, and GST relief. Programs such as Swadesh Darshan, PRASHAD, UDAN, and Dekho Apna Desh are driving large-scale infrastructure and heritage development, with 27 new sites across 18 states and UTs added under PRASHAD in 2024.

Diversified Revenue Streams

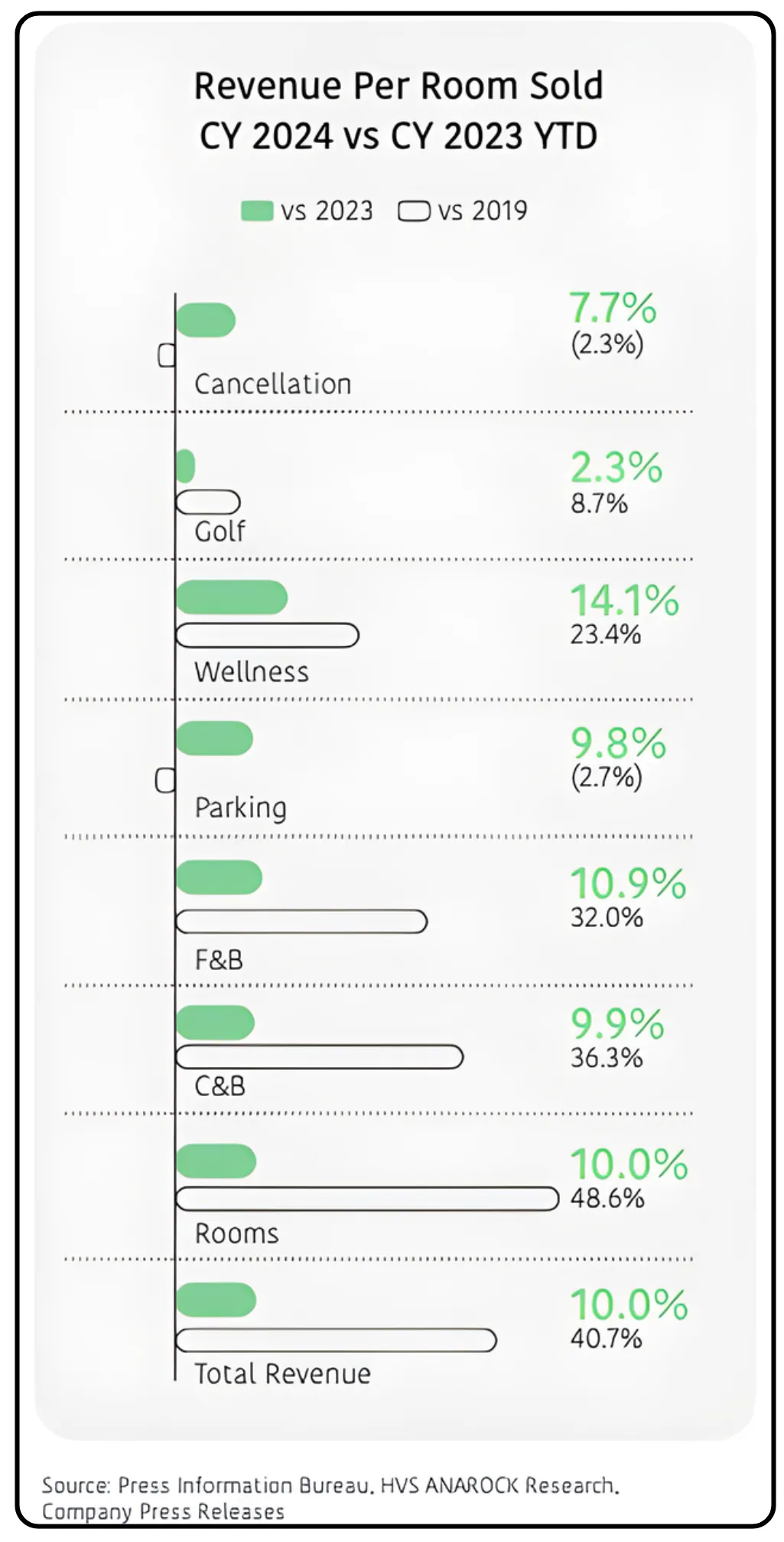

The hospitality industry is shifting from room-led income to a broader, experience-driven model. In 2024, total hotel revenue per room sold rose 10% year-on-year, driven by strong growth in wellness (14.1%), food and beverage (10.9%), and conferences and banquets (9.9%). Compared to 2019, room revenue is up 48.6%, F&B up 32%, and event revenue up 36.3%. This shift reflects a more balanced and profitable ecosystem built on experiences, wellness, and high-value guest engagement.

For a deeper look into another critical pillar of India’s services economy, check out our detailed report — A Comprehensive Industry Analysis of India’s Hospital Sector, covering growth trends, policy support, and profitability outlook.

Luxury Hospitality Segment Analysis

Severe Supply Gap in Luxury Hotels

India’s luxury hospitality market is still vastly underdeveloped compared to global standards. As of March 2024, the country had just 23 luxury hotel keys per million people—far below Australia (973), Thailand (690), and China (177). Even across the broader organized hotel segment, India has only 263 keys per million population, versus a global average of 7,877.

Developed economies show much higher hotel density. The U.S. has over 17,000 keys per million people, Australia about 12,500, and the U.K. over 10,800. Within Asia-Pacific, Japan stands at 6,994, and Indonesia at 1,468. India, by comparison, has just 0.27 hotel keys per thousand people, versus the global average of 2.2—highlighting massive room for expansion. With only 0.1 branded room inventory per 1,000 people, the opportunity for large-scale penetration remains wide open. The disparity in luxury hotel keys per million in India vs global markets underscores the country’s untapped potential. India’s luxury segment remains under-supplied compared to Asia-Pacific peers, leaving room for strong pricing power and premium positioning.

Demand-Supply Imbalance

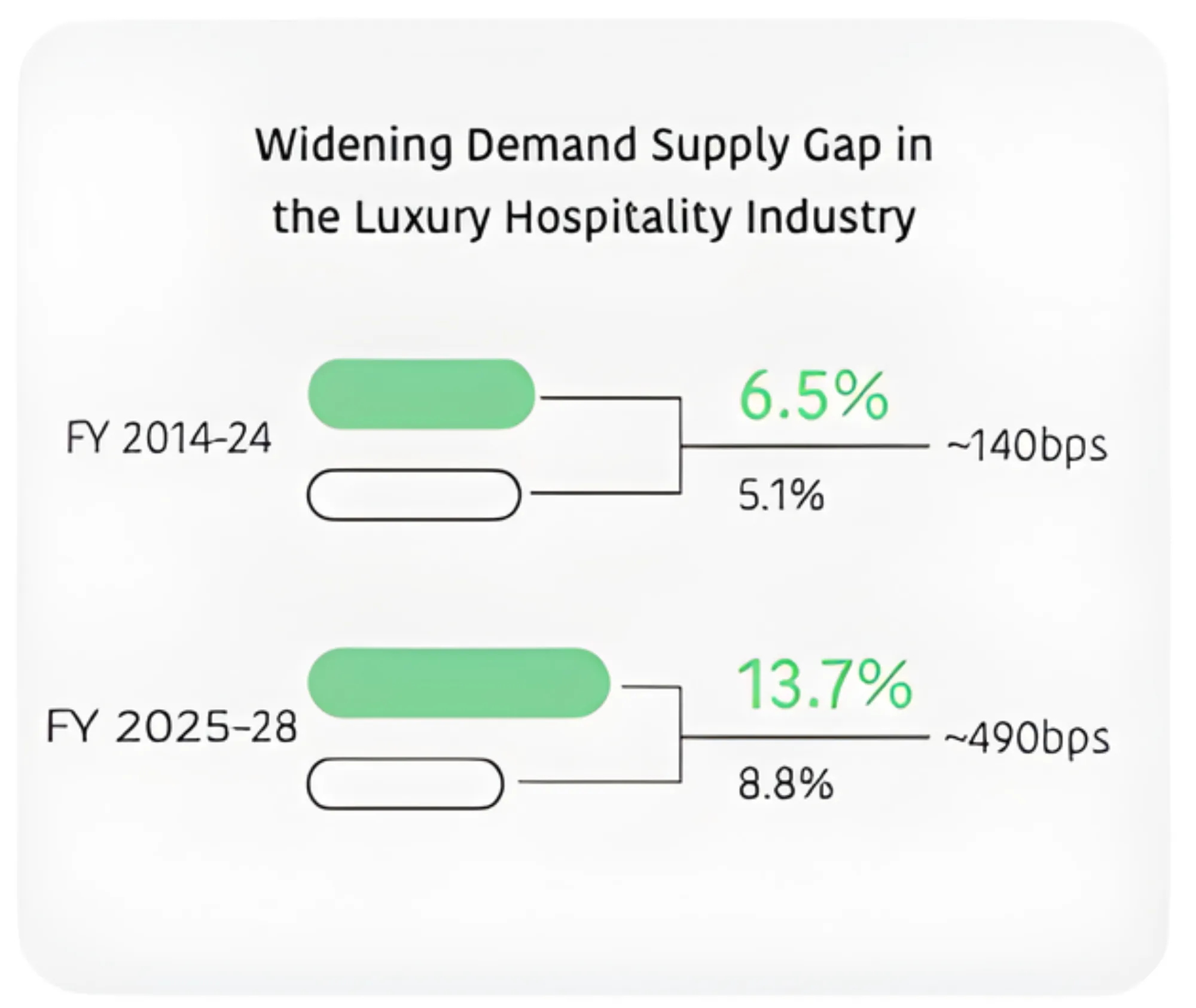

Over the past decade, luxury hotel demand in India has consistently grown faster than supply. Between FY14 and FY24, demand expanded at a CAGR of 6.5%, while supply lagged behind at 5.1%, creating a 140-basis point gap. This imbalance is projected to widen further to nearly 490 basis points by FY28, as demand accelerates to 13.7% CAGR against 8.8% in supply.

Rising disposable incomes, growing appetite for premium experiences, and the shift toward high-end leisure travel are fueling this demand surge. On the supply side, hurdles like high land costs, lengthy approvals, and heavy capital requirements continue to restrict growth—setting the stage for sustained Average Room Rate (ARR) gains and favorable market conditions for upscale expansion.

Strong ARR Growth Potential

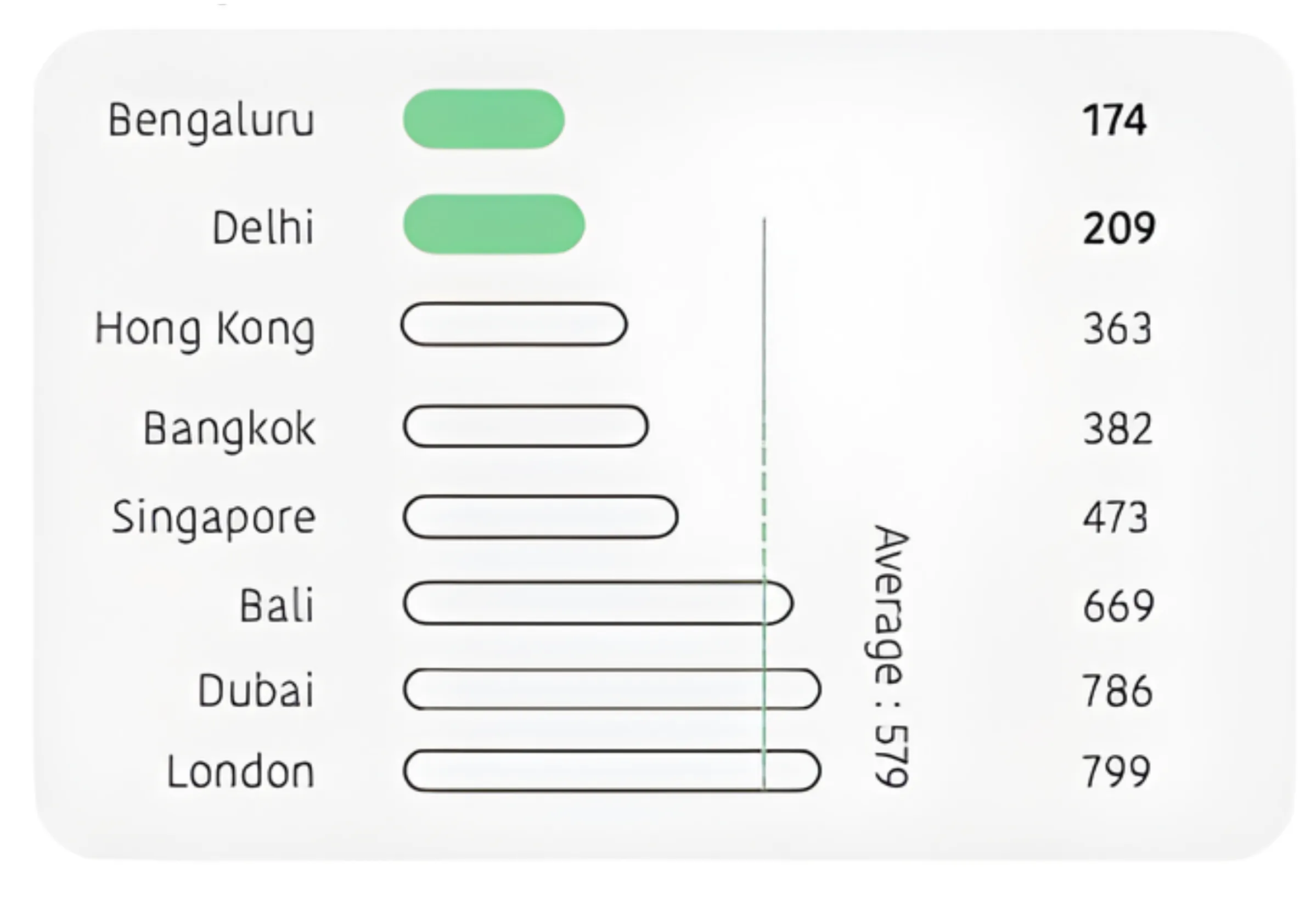

Average room rates in India’s luxury segment remain far below international averages, offering significant headroom for growth. In FY25, Bengaluru’s luxury hotels averaged $174 per night and Delhi’s $209, compared to the global average of $579. Other key markets like Hong Kong ($363), Bangkok ($382), and Singapore ($473) command higher rates, while destinations such as Bali, Dubai, and London exceed $669.

This wide gap signals long-term pricing power for Indian operators, especially as service quality, global visibility, and experiential offerings continue to improve.

Rise of Experiential Luxury Travel

Luxury travel in India is evolving from traditional stays to immersive experiences. Guests are increasingly seeking cultural, wellness, and nature-based experiences, ranging from heritage trails and wildlife lodges to spiritual and wellness retreats. Millennials, in particular, are driving this change, favoring authentic and personalized journeys over standard luxury formats. This shift is reshaping the segment toward deeper engagement, higher margins, and distinct value propositions centered on experience-driven hospitality.

Market Outlook and Future Projections

Strong Growth Trajectory Ahead (2025–2027)

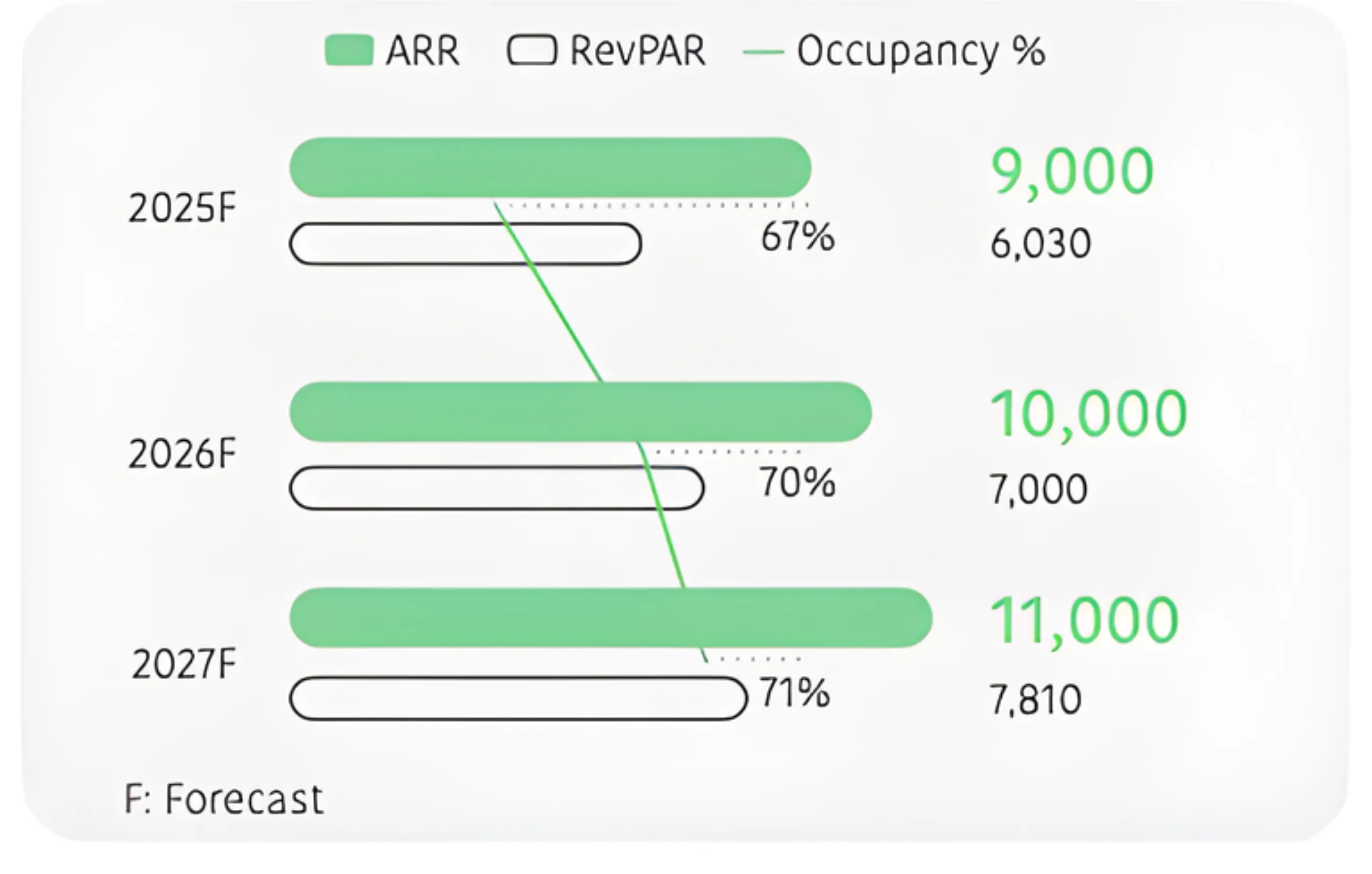

India’s hotel industry enters 2025 with solid momentum and a clear growth runway. Average room rates (ARRs) are projected to rise to around ₹9,000 in 2025 with occupancy averaging 67%, translating to a RevPAR of ₹6,030. The uptrend is expected to continue through 2026, with ARRs touching ₹10,000 and occupancy improving to 70%, pushing RevPAR to ₹7,000. By 2027, ARRs are forecast to reach ₹11,000, while occupancy climbs to 71%, resulting in a RevPAR of ₹7,810—marking steady improvement in both pricing and utilization. Consistent RevPAR and ARR growth in Indian hospitality reflect a strong demand cycle, aided by improving infrastructure, business travel, and tourism recovery. Room rates are expected to rise steadily through FY27 as supply trails demand.

Expanding Supply Pipeline

Industry data from Horwath HTL indicates a robust pipeline of about 105,000 branded hotel rooms expected by 2029, though minor delays are possible. The growth is being driven by rising tourism, corporate travel, and continued infrastructure upgrades. In 2024, branded hotel inventory grew by 8% year-on-year—adding nearly 14,400 new rooms—and by 32% compared to 2019, adding roughly 50,000 rooms. Demand growth kept pace, up 11% over the previous year (equivalent to 11,000 additional rooms sold daily) and 30% higher than 2019 levels (about 29,000 more rooms sold daily).

Tier-2 and Tier-3 Cities Driving the Next Phase

A major shift is underway as hotel development spreads beyond the metros. Over two-thirds of new supply in 2024 came from tier-2 and tier-3 cities, driven by better air connectivity, state tourism initiatives, and hybrid work trends. India’s urbanization push is creating new consumption hubs—urban residents now make up 35–37% of the population, still well below the global average of 57%, leaving vast headroom for growth. The number of Indian cities with populations above one million has jumped from 52 in 2011 to around 75 in 2024, expanding the addressable market for hospitality operators.

Business Travel and MICE Revival

Business travel is rebounding strongly alongside India’s growing corporate and startup ecosystem. The expansion of Global Capability Centers (GCCs), IT/ITeS hubs, and commercial real estate has fueled demand for hotels catering to meetings, incentives, conferences, and exhibitions (MICE). Alongside this, India’s booming wedding industry and the rise of spiritual tourism continue to support year-round occupancy. The addition of world-class convention centers across major cities is further cementing India’s position as a key business and event destination in Asia.

Growth Strategy: Asset-Light Model

Leading Indian hotel chains are adopting an asset-light model to expand efficiently while maintaining profitability. This strategy enables faster scaling and higher returns on capital in a market witnessing strong post-pandemic growth. This approach focuses on expanding room inventory via management contracts and franchise agreements rather than owning properties, enabling faster market penetration with lower capital requirements.

ITC Hotels exemplifies this shift, targeting a portfolio of over 220 operational hotels with 20,000+ keys by 2030, of which nearly 70% will be under management or franchise models. Over the past two years, the company launched 30 hotels across its brand portfolio—29 of which operate under management or franchise agreements in India and Nepal. During the same period, ITC Hotels signed 54 new contracts, including 30 in the most recent fiscal year, reflecting its strong execution pipeline and growing brand appeal among hotel owners.

The ongoing domestic tourism boom in India and the rise of MICE and experiential luxury travel are reshaping demand patterns. Travelers are increasingly seeking authentic experiences—ranging from wellness retreats to destination weddings—creating opportunities across emerging cities.

Curious to see how the asset-light model plays out in practice? Check out our fundamental analysis on Praveg Ltd., a hospitality player driving strong margins and long-term growth.

Major Players in the Industry

| S.No. | Name | Sales Rs.Cr. | Med Sales Growth 5Yrs % | OPM % | P/E | CF Operations Rs.Cr. | Public Hold % | DII Hold % | CMP Rs. | Book Value | Debt Rs.Cr. |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Indian Hotels Co | 8825.39 | 23.13 | 32.81 | 61.84 | 2194.37 | 16.2 | 19.4 | 746 | 78 | 3084.27 |

| 2 | ITC Hotels | 3731.04 | 60.03 | 34.4 | 61.15 | 803.45 | 14.43 | 20.21 | 216.69 | 53 | 80.23 |

| 3 | EIH | 2790.19 | 24.39 | 37.34 | 31.44 | 825.08 | 47.04 | 14.17 | 395.1 | 73.36 | 265.06 |

| 4 | Chalet Hotels | 2251.36 | 25.59 | 42.33 | 73.9 | 950.39 | 3.53 | 23.4 | 964.9 | 139 | 2604.04 |

| 5 | Leela Palaces Hotels | 1300.57 | 11.02 | 45.75 | 83.66 | 552.88 | 4.51 | 11.08 | 435.95 | 183 | 2743.71 |

| 6 | Lemon Tree Hotel | 1333.84 | 22.42 | 49.37 | 61.79 | 541.58 | 36.51 | 19.71 | 168.25 | 14.6 | 1712.65 |

Key Challenges and Risks

Despite strong growth momentum, the hospitality sector continues to navigate multiple headwinds. Global trade tensions, geopolitical uncertainty, and inflationary pressures can impact travel sentiment and discretionary spending. During such periods, travelers tend to favor value-oriented and regional destinations, which may moderate demand growth for premium hotels. On the supply side, land availability, regulatory complexities, high construction costs, and extended project timelines remain key bottlenecks, particularly in the upscale and luxury categories. Additionally, climate-related risks such as extreme weather events pose increasing challenges for a sector heavily reliant on tourism and travel mobility. Addressing sustainability and resilience in operations is becoming essential for long-term competitiveness.

The Road Ahead

India’s hospitality industry is at an inflection point, backed by solid fundamentals, rising tourism demand, improved infrastructure, and supportive government policies. Its growth is fueled by a larger middle class, higher disposable incomes, and a clear shift toward experience-led travel.

With only 263 organized hotel keys per million people compared to the global average of 7,877, the sector remains vastly under-penetrated—highlighting its long runway for expansion. Demand for branded rooms is expected to consistently outpace supply, which continues to grow at a measured pace.

The industry’s evolution beyond accommodation—into wellness, dining, and MICE-led experiences—underscores its growing resilience and economic relevance. As India moves toward its vision of becoming a developed nation by 2047, the hospitality sector will remain central to that progress through job creation, investment generation, and the strengthening of global connectivity.

Turn research into action — trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.