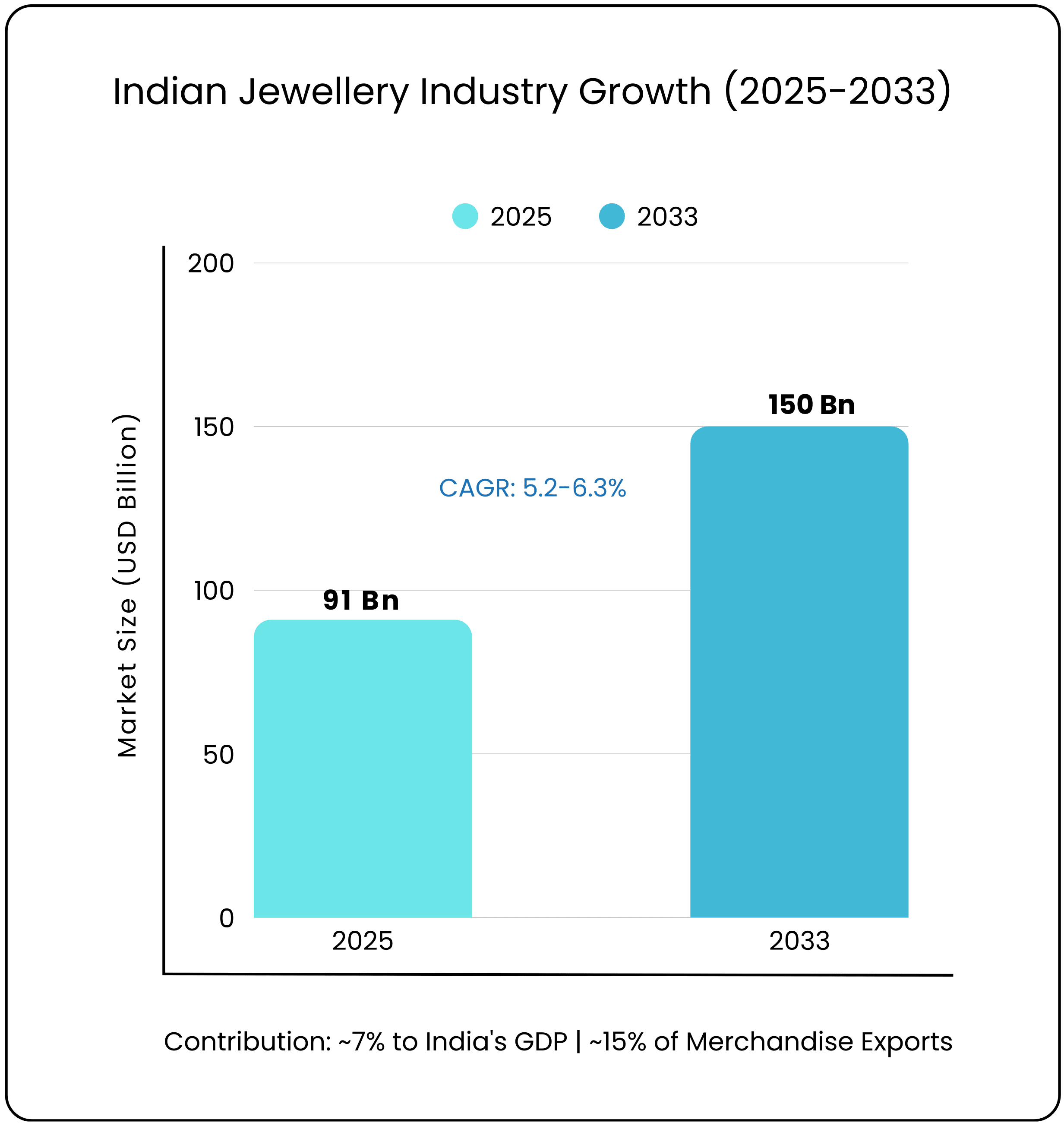

The Indian jewellery industry is one of the most culturally entrenched and economically significant sectors in the country. Valued at USD 90 – 91 billion in 2025, the Indian jewellery market size is projected to reach USD 150 billion by 2033 at a CAGR of 5.2 – 6.3%. The sector contributes 7% to India’s GDP and 15% of total merchandise exports, establishing itself as a critical pillar of the nation’s economic growth.

A major structural shift is underway in the Indian jewellery industry, with organized vs unorganized jewellery market India dynamics changing rapidly. Organized retail is increasing its share to 36–38% in FY25 from just 22% in FY19. This transition, supported by regulatory reforms such as hallmarking and GST impact on jewellery, alongside evolving consumer preferences for branded jewellery, is reshaping the competitive landscape and unlocking investment opportunities in Indian jewellery for well-positioned players.

Industry structure and market dynamics

Market size and growth

India’s domestic jewellery market, valued at over ₹5 trillion, reflects a blend of traditional craftsmanship and modern retail formats.

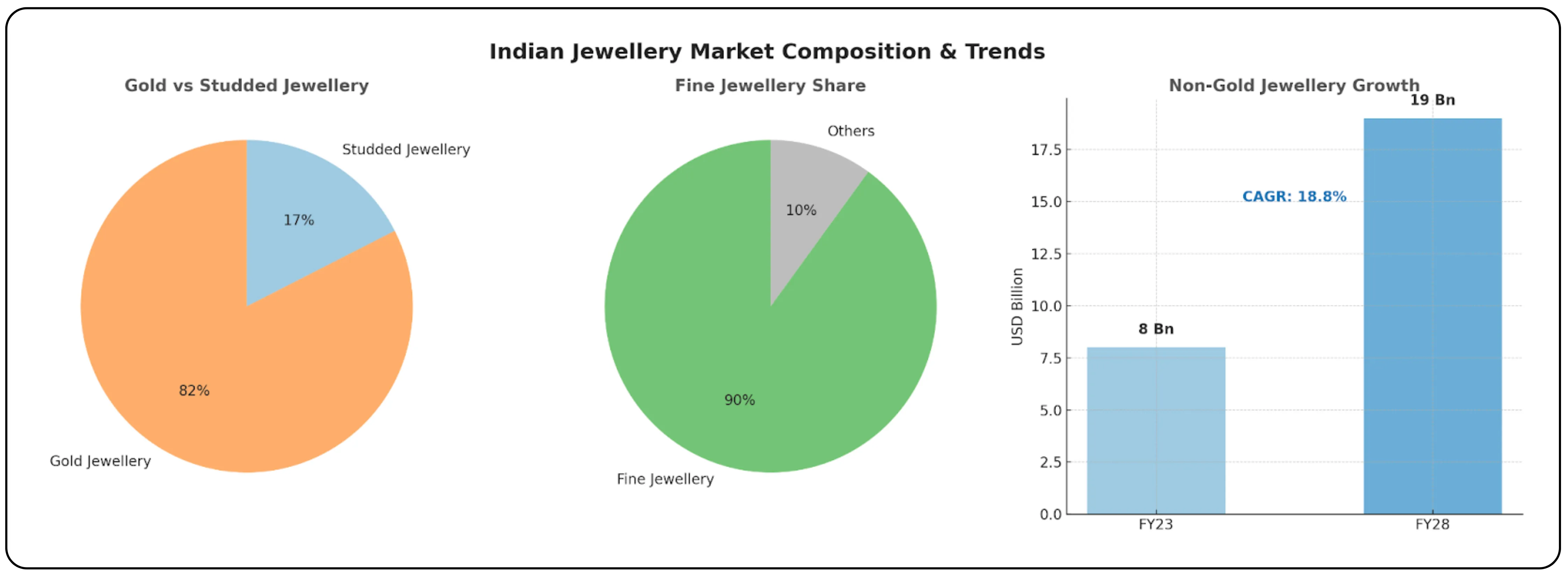

The Gold jewellery market in India dominates the landscape with a commanding 80–85% share, while studded jewellery, including diamonds, accounts for the remaining 15–20%. Fine jewellery represents nearly 90% of the overall market, underscoring its strong cultural and investment relevance. At the same time, non-gold categories are emerging as a key Indian jewellery market trends, with this segment projected to expand at a CAGR of 18.8% between FY23 and FY28, to reach USD 19 billion.

Regional distribution

The Indian jewellery market exhibits strong regional concentration patterns shaped by cultural traditions and economic development.

South India leads with nearly 40% share, with Tamil Nadu standing out as the largest consumer of gold in the country. West India follows with about 25% of the market, largely driven by Maharashtra and Gujarat. North India contributes 21% and East India accounts for the remaining 14%. These regional dynamics play a crucial role in shaping expansion strategies, especially for jewellery companies in India entering new territories.

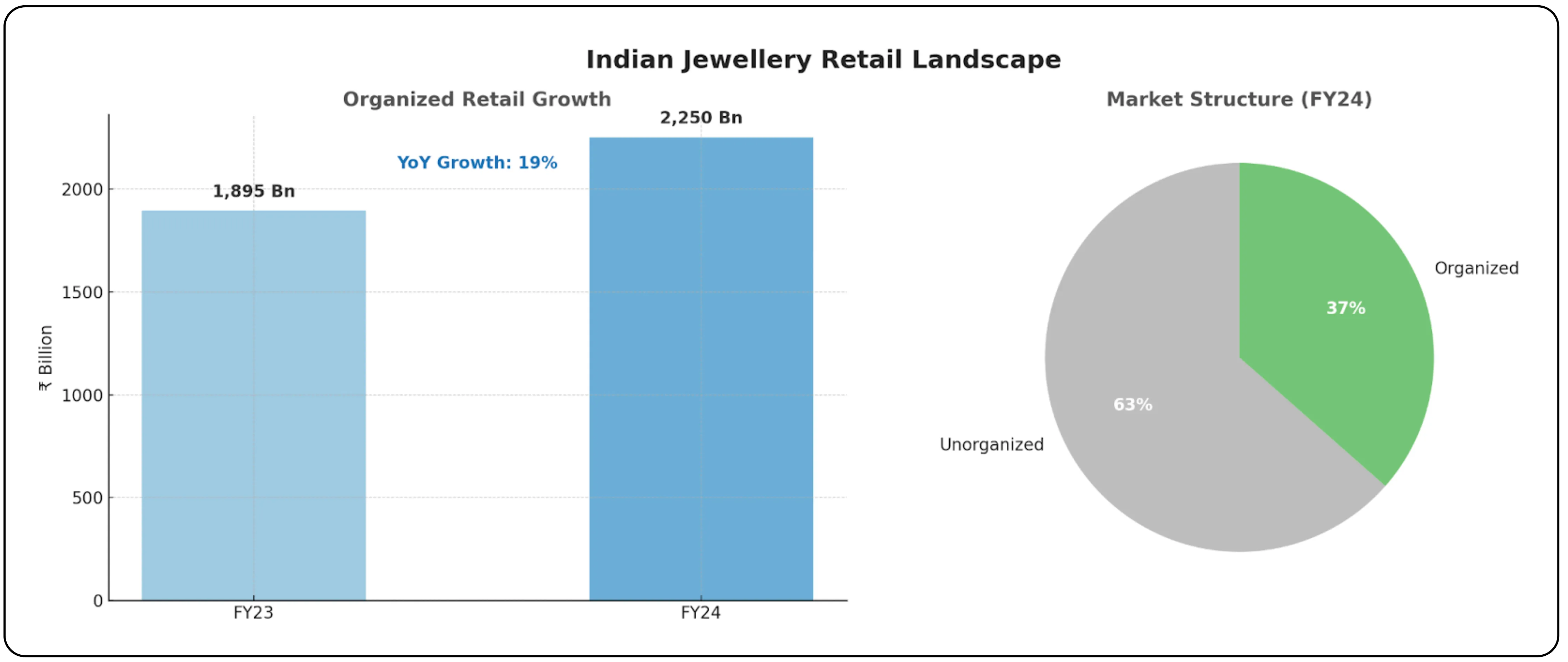

Organized vs. Unorganized market

The jewellery industry continues to witness a significant structural transition from unorganized to organized retail.

Organized players have grown rapidly, with market share rising from ₹1,895 billion in FY23 to ₹2,250 billion in FY24, reflecting 19% year-on-year growth. Despite this progress, unorganized players still account for 62–65% of the market, leaving ample room for consolidation. Government reforms such as hallmarking and GST, compliance and the automatic route for 100% FDI have further accelerated this shift.

Explore the Muthoot Model and How the Gold Rally Impacts Earnings

Competitive landscape

Store Network and Expansion Strategies

Titan Company had initially targeted aggressive jewellery store expansion, aiming to open over 170 new stores in FY25, including Tanishq, Mia, and CaratLane outlets across India and international markets. However, by September 2025, Titan added only 19 new jewellery retail locations in Q1 FY26—3 Tanishq, 7 Mia, and 9 CaratLane stores—with the pace expected to accelerate in Q2 ahead of the festive season. The tempered expansion reflects industry caution caused by gold price volatility and softer consumer demand. Titan still maintains a strong nationwide presence with 3,322 total stores, including 23 overseas locations, while focusing on quality additions, lighter product lines, and selective international growth across North America, GCC, and Singapore.

Kalyan Jewellers plans to expand by opening 170 new stores in FY26, largely via a franchise model to reduce debt, with 90 Kalyan stores (including 7 overseas in the UK, US, and Middle East) and 80 lifestyle brand Candere stores targeting non-south Indian tier I-IV cities. The company is focused on strengthening manufacturing capabilities by consolidating contract manufacturers in Thrissur and expects continued market share growth and double-digit same-store sales growth driven by a favorable monsoon tailwind.

PN Gadgil Jewellers is undertaking one of its fastest expansions during Navratri 2025 by launching 6 new standalone stores and 4 LiteStyle shop-in-shop counters across Maharashtra and Central India in key cities such as Pune, Kolhapur, Lucknow, Kanpur, and Mumbai. Their offers during the expansion include generous discounts on making charges to attract customers. The company is emphasizing accessibility while retaining its heritage values of purity and craftsmanship.

Thangamayil Jewellers is focusing on regional growth by adding 15 new showrooms in FY26, having already opened several stores in Tamil Nadu and planning 11 more primarily centered around Chennai. This expansion is backed by ₹510 crore raised through rights issue proceeds, supporting long-term growth.

Senco Gold & Diamonds anticipates adding 18-20 new stores in Q4 FY25, including 10-12 franchises, aiming to exceed 170 locations. The company recently launched its first international outlet in Dubai and is targeting further global expansion into the US and Europe in the coming years.

Malabar Gold & Diamonds completed opening 12 new stores by March 2025 with ₹600 crore invested and plans to open another 60 globally in 2025, expanding its footprint in the Middle East, UK, and Canada. This will bring their store count to 391 across 13 countries.

Financial performance

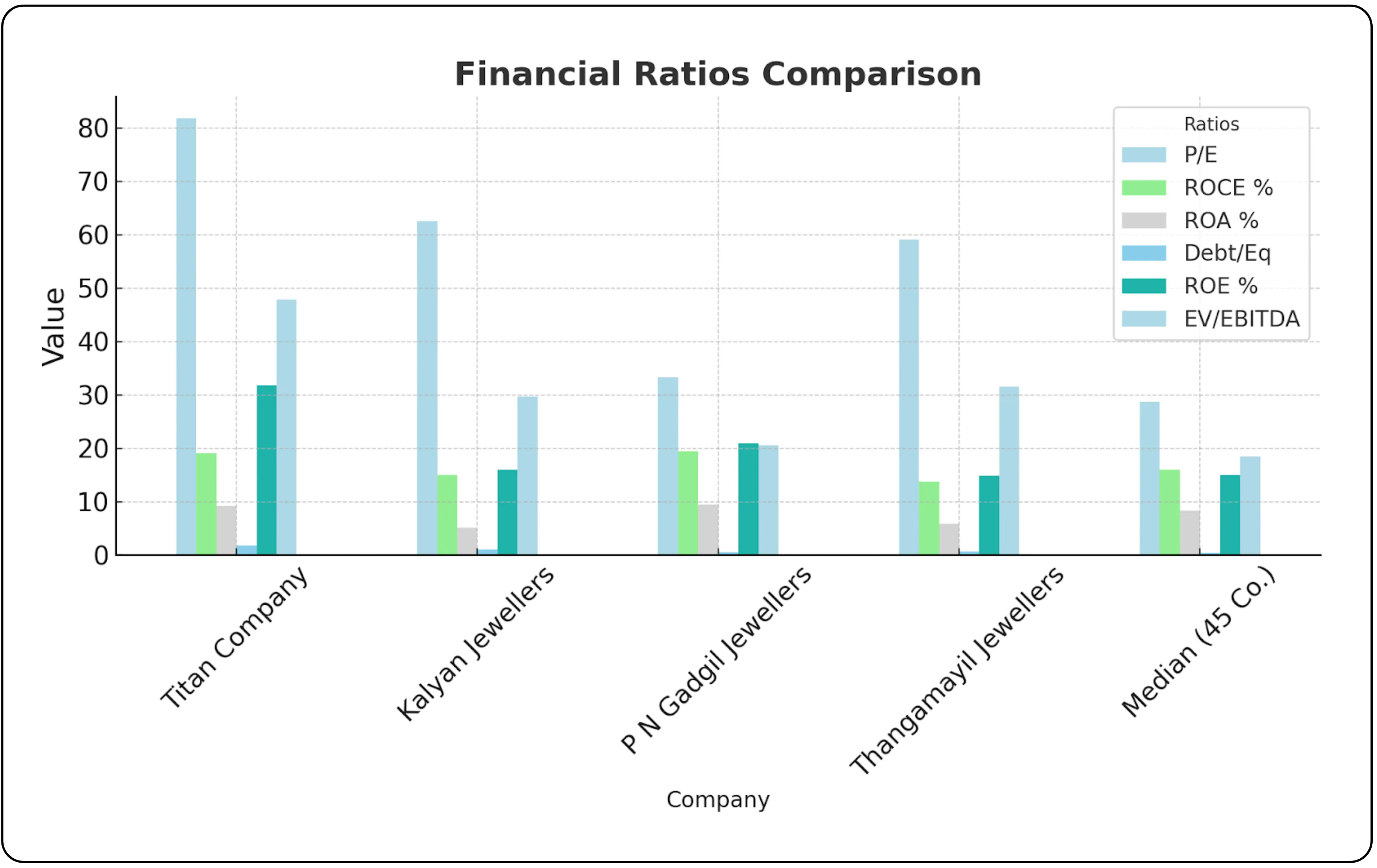

| Metric | Titan Company | Kalyan Jewellers | P N Gadgil Jewellers | Thangamayil Jewellers | Median (45 Co.) |

|---|---|---|---|---|---|

| CMP Rs. | 3425.15 | 485.25 | 618.15 | 2053.15 | 221.35 |

| P/E | 81.87 | 62.56 | 33.25 | 59.14 | 28.72 |

| Mar Cap Rs.Cr. | 304080.09 | 50104.66 | 8388.80 | 6381.61 | 1136.48 |

| ROCE % | 19.14 | 15.02 | 19.41 | 13.74 | 15.99 |

| ROA 12M % | 9.24 | 5.13 | 9.50 | 5.88 | 8.29 |

| Debt/Eq | 1.79 | 1.03 | 0.60 | 0.72 | 0.38 |

| ROE % | 31.75 | 15.95 | 20.97 | 14.88 | 14.96 |

| Sales growth % | 21.47 | 36.07 | 18.64 | 28.28 | 28.28 |

| Profit growth % | 7.50 | 26.91 | 48.58 | -11.00 | 31.23 |

| Sales Var 3Yrs % | 28.04 | 32.29 | 44.03 | 30.83 | 24.39 |

| Profit Var 3Yrs % | 14.64 | 47.40 | 56.08 | 45.49 | 43.63 |

| EV/EBITDA | 47.90 | 29.72 | 20.56 | 31.52 | 18.42 |

| Inventory Days | 216.77 | 162.38 | 104.47 | 163.66 | 152.65 |

| Cash Cycle | 208.12 | 128.79 | 93.65 | 161.56 | 161.44 |

| OPM % | 9.85 | 6.21 | 4.92 | 4.19 | 7.05 |

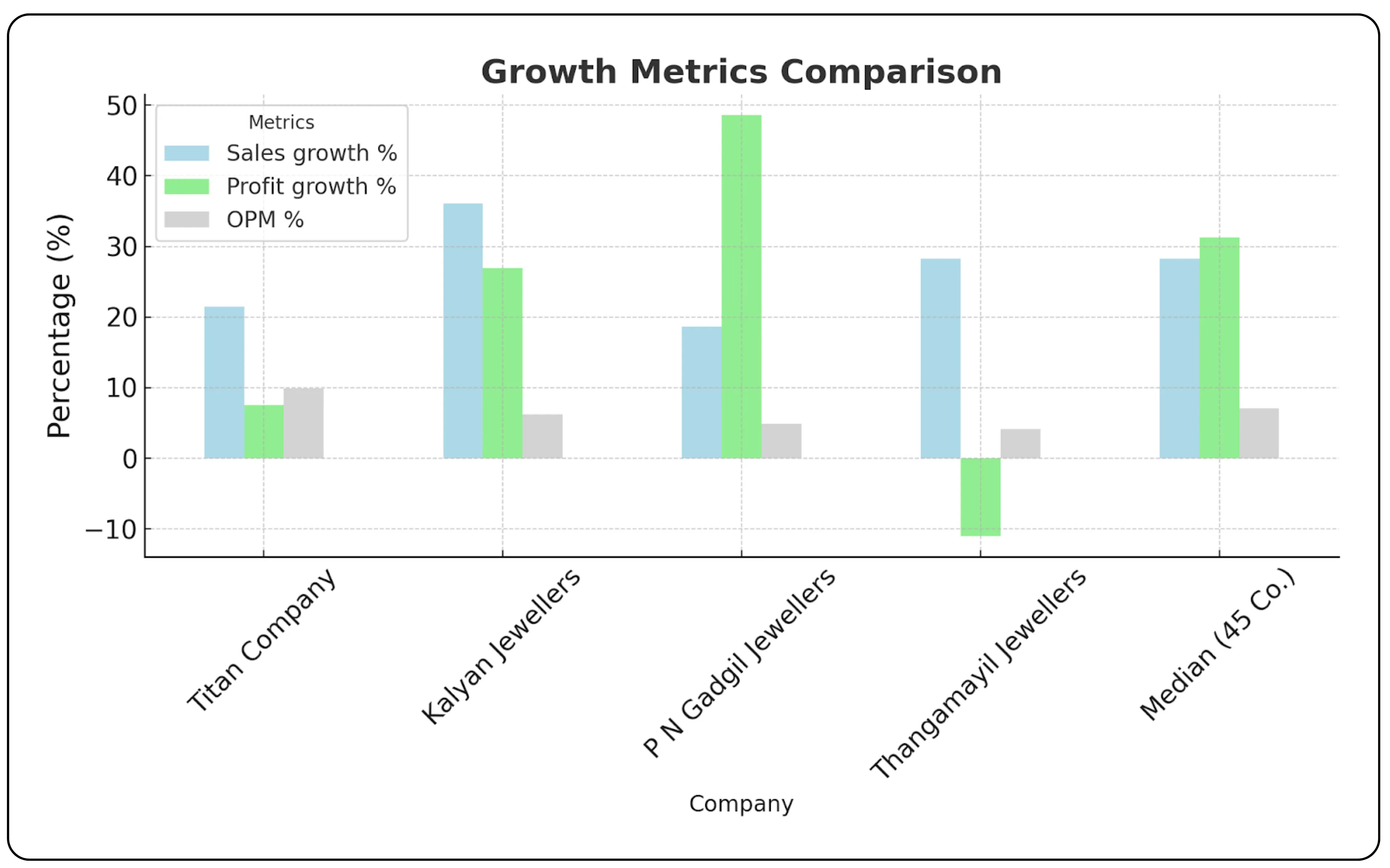

Titan dominates the jewellery space with the largest market cap of ₹3 lakh crore and industry-leading return ratios (ROE 31.8%, ROCE 19.1%). Kalyan, while much smaller in scale, is showing stronger topline momentum with 36% sales growth and healthy profit growth of 26.9%. P N Gadgil stands out for profitability, delivering the highest 3-year profit CAGR at 56% and the strongest ROCE among peers at 19.4%, with low leverage (Debt/Equity 0.6). Thangamayil, though regionally focused, shows steady sales growth at 28% but is struggling with profitability, posting an 11% decline in profit growth. Compared to the industry median (ROE 15%, ROCE 16%), Titan and P N Gadgil remain well above averages, while Kalyan leads on growth metrics.

Certification is driving trust in jewellery retail. Check our analysis of International Gemmological Institute (India).

Industry trends and growth drivers

Digital transformation

E-commerce jewellery sales India are expected to account for 18–21% of jewellery sales by 2029, marking a significant structural shift in the industry. Online jewellery sales are projected to grow at a CAGR of 19–21% through 2028, supported by technological innovations such as AR/VR-enabled virtual try-ons and AI-driven personalization tools, which are playing a pivotal role in enhancing customer engagement and building trust.

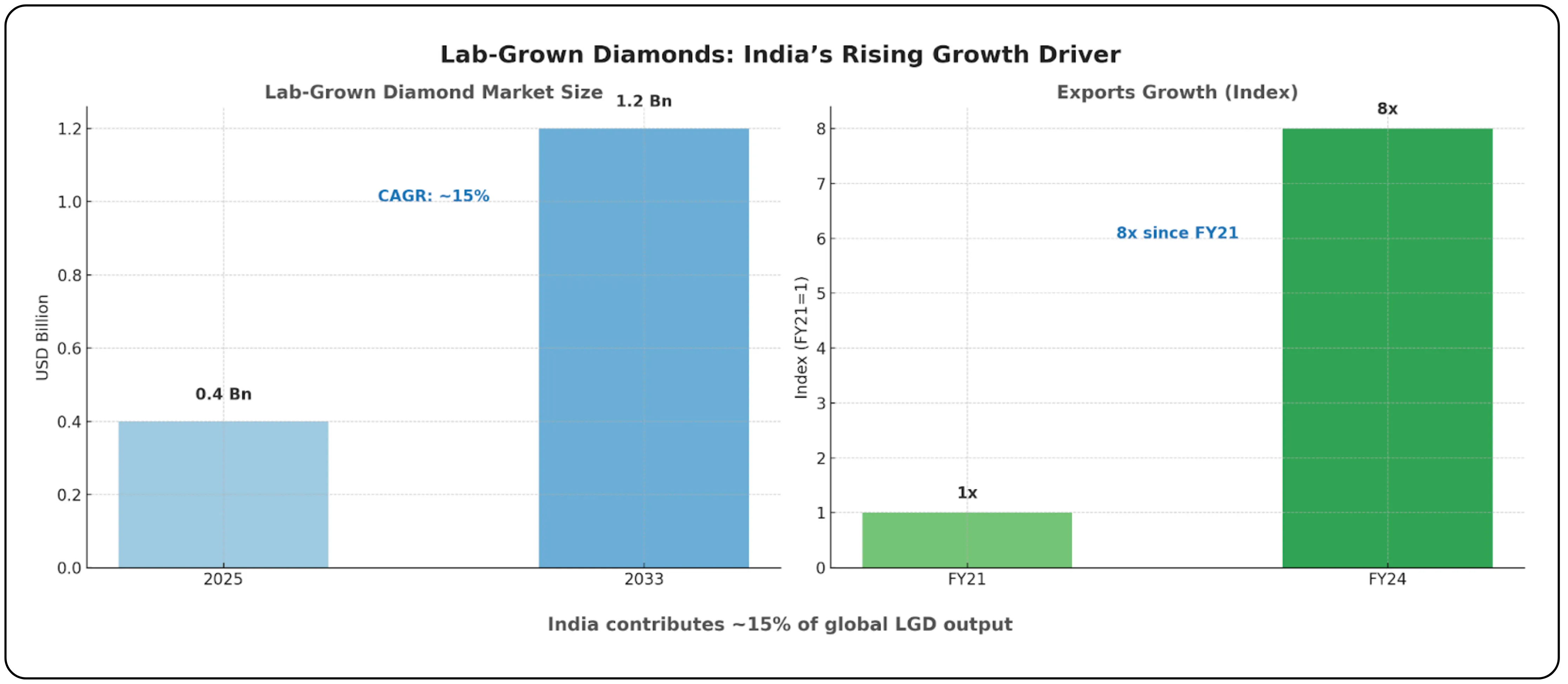

Lab-grown diamonds (LGDs)

The lab-grown diamonds India segment is rapidly emerging as a major growth driver in the Indian jewellery market. The market is projected to reach USD 1.2 billion by 2033, expanding at a CAGR of nearly 15%. Exports have already increased eightfold since FY21, reflecting strong global demand. India now contributes around 15% of global LGD output, underscoring the country’s strengthening position in this high-potential category.

Silver in the Indian Jewellery Industry

Silver plays a crucial role in India’s jewellery sector, making it one of the largest and most dynamic silver markets globally. According to the World Silver Survey 2025, India accounts for 39.2% of global silver consumption. Jewellery fabrication grew 3% worldwide in 2024, with India contributing the largest share.

The Indian silver jewellery market has expanded notably in recent years. Exports rose 9.83% year-on-year to $233.97 million in Q1 2024 but declined 37.84% to $770.83 million between April and December due to price volatility and economic uncertainty. Silver imports reached a record 7,669 tons in 2024, more than double the previous year, driven by lower import duties, a strong rural economy, and rising demand for higher purity silver.

Investment demand is also rising, with silver ETF inflows reaching ₹17.59 billion in July and ₹19.04 billion in August 2025, well above the previous year’s monthly average of ₹6.7 billion. Industry projections indicate silver imports in 2025 may range between 5,500 and 6,000 tons, supported by robust industrial demand and strong investment inflows.

Changing consumer preferences

Consumer behaviour in the jewellery market is undergoing a distinct transformation, particularly among younger buyers who increasingly view jewellery as a fashion and lifestyle product rather than solely an investment. There is a growing preference for lightweight, daily-wear designs and personalized collections that align with modern lifestyles. Women already account for 43% of online jewellery shoppers, and this proportion is expected to rise further as digital adoption deepens across demographics.

Investment opportunities and strategic considerations

Consolidation potential

The fragmented nature of the Indian jewellery industry presents attractive investment opportunities in Indian jewellery, especially for organized players. With 62–65% of the sector still in the unorganized space, there is ample room for consolidation. As consumer preferences shift toward trusted and branded formats, organized jewellery companies in India are well-positioned to scale operations and capture additional Indian jewellery market share.

Tier-II/III cities

Tier 2 Tier 3 cities jewellery market is gaining traction. These underpenetrated regions offer significant growth potential due to rising affluence and increasing demand for branded jewellery.

Technology

Adoption of digital tools is becoming central to competitive differentiation. Investments in ERP, CRM, AI-powered personalization, and omnichannel integration are enhancing efficiency, improving customer engagement, and strengthening the ability of organized players to deliver a seamless shopping experience.

Exports

India’s global leadership in diamond cutting and polishing continues to anchor its export strength. In FY25, jewellery exports reached USD 28.5 billion, with key markets including the United States, the UAE, Hong Kong, and Belgium. Sustained export growth is expected to remain a vital driver for the industry, backed by both craftsmanship and strong cost competitiveness.

For insights beyond jewellery, explore our detailed analysis of the Indian Hospital Industry, covering growth drivers, challenges, and investment outlook.

Risk factors and challenges

Gold price volatility

Gold price volatility India directly influences consumer demand as well as the valuation of inventory. Periods of high volatility often lead to cautious buying behaviour, while also impacting the margins of jewellers holding large stock positions.

Supply chain dependencies

Heavy reliance on imported raw materials, particularly gold and diamonds, makes the industry vulnerable to external shocks, posing a significant Indian jewellery industry challenge.

Competition

Competition in the Indian jewellery industry is intensifying, driven by the expansion of large national chains and the rise of digital-first brands. This is putting pressure on traditional jewellers to adapt their strategies, invest in branding, and strengthen omnichannel presence to retain market share.

Regulatory compliance

Compliance requirements around hallmarking, GST, and customs duties add to both cost pressures and operational complexity to the Indian jewellery industry. Organized players with robust systems are better placed to manage these obligations efficiently. In contrast, players in the unorganized jewellery market India often struggle with regulatory compliance, facing higher relative burdens that affect profitability and scalability.

Future outlook and investment thesis

Growth outlook

The Indian jewellery market size is projected to expand to USD 145 billion by FY28, driven by urbanization, rising disposable incomes, and favourable demographic trends. Within this landscape, organized retail is expected to outpace overall industry growth, as players invest in omnichannel models, differentiated product designs, and robust compliance frameworks to strengthen consumer trust.

Strategic priorities for investors

From an investment standpoint, companies that demonstrate strong omnichannel capabilities and effective use of technology are likely to build sustainable advantages. Geographic diversification into the underserved tier 2 and tier 3 cities jewellery market provides a meaningful runway for growth, supported by rising affluence in these markets. In addition, expansion into high-potential categories such as lab-grown diamonds offers opportunities to capture emerging demand. Underpinning all of these strategies, sound financial discipline and efficient capital deployment will remain critical markers of long-term value creation.

Long-term view

The Indian jewellery industry presents a compelling long-term opportunity, combining deep cultural roots with structural modernization. As the market continues to evolve, Investors should focus on scalable, organized players with brand strength, operational sophistication, and adaptability to evolving Indian jewellery market trends.

Turn research into action and explore smarter investing opportunities with CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.