To understand Karnataka Bank’s business, it’s essential to first grasp how the banking sector operates. Banks are not just custodians of public deposits, they play a vital role in the economy by channeling funds from savers to borrowers, facilitating transactions, and managing financial risks. Understanding how banks generate revenue, manage costs, and create value for shareholders provides the foundation for analyzing any bank’s performance, including that of Karnataka Bank.

Understanding the banking sector

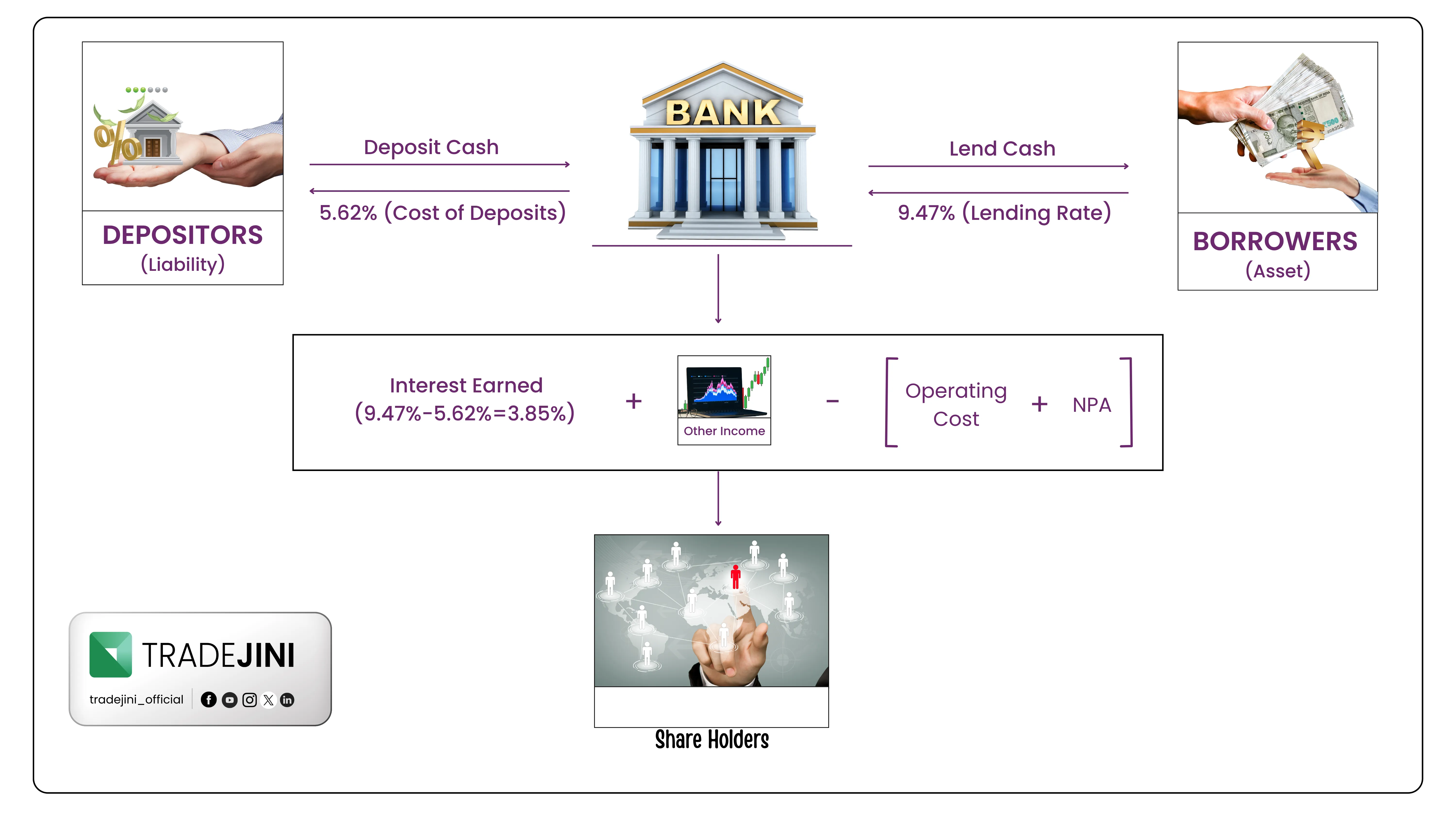

The banking sector functions as the backbone of an economy by facilitating the flow of money between individuals, businesses, and governments. Banks primarily operate by accepting deposits from customers and lending that money to borrowers, earning interest on loans as their main source of income. They offer a range of financial services such as savings and current accounts, credit and debit facilities, investment products, and wealth management. Central banks regulate the sector to ensure stability, liquidity, and consumer protection, while commercial banks drive financial inclusion and economic growth. By mobilizing savings, extending credit, and enabling secure transactions, the banking sector plays a crucial role in supporting development and maintaining financial stability.

How do banks make money?

Banks make profits primarily by acting as financial intermediaries, earning income from the difference between the interest they pay on deposits and the interest they earn on loans, known as the net interest margin. When customers deposit money, banks pay them a relatively low interest rate. The bank then lends that money to borrowers at a higher rate, generating a profit from the spread. In addition to interest income, banks also earn non-interest income through fees and commissions on services like ATM usage, account maintenance, fund transfers, investment advisory, and loan processing. Some banks also profit from trading and investment activities, such as buying and selling securities, foreign exchange, or derivatives. Together, these revenue streams contribute to a bank’s profitability while managing risks like loan defaults and market volatility. In the case of Karnataka Bank, ‘Other Income’ accounts to ₹1200 crore from trading and investing activities

Also read: Watertech Leader Transforming Dirty Water into Liquid Gold

Fundamental analysis of Karnataka Bank Ltd.

Karnataka Bank Ltd. is a century-old Indian private sector bank, headquartered in Mangaluru, Karnataka. The Bank offers a comprehensive range of financial services including retail, corporate banking and para-banking activities in addition to treasury and foreign exchange business. Karnataka bank operates 952 branches and 1,516 ATMs and recyclers as of March 2025, maintaining a strong presence especially in semi-urban and rural India.

It partners with PNB Metlife, LIC, HDFC Life, ICICI Lombard and Bharti AXA for life insurance, and with Universal Sompo and Bajaj Allianz for general insurance products. In 2024, it collaborated with FISDOM to offer 3-in-1 investment accounts via its KBL Mobile Plus app.

Karnataka bank’s business model

Karnataka Bank functions as a universal bank, offering a comprehensive suite of financial services across key verticals. In retail banking, it provides housing loans, personal loans, gold loans, and vehicle loans. The MSME and agriculture segment focuses on loans tailored for self-employed individuals, farmers, self-help groups (SHGs), and small businesses. In corporate banking, the bank is increasingly concentrating on mid-sized corporates while consciously reducing its exposure to non-banking financial companies (NBFCs) and opportunistic large-ticket lending. Its digital capabilities are anchored by platforms such as the ‘KBL Mobile Plus’ app and KBL ONE for corporate mobile banking, supported by fintech partnerships that enable faster onboarding and co-lending at scale.

To drive growth, the bank follows a four-channel strategy: branch-led acquisition, sales-led acquisition focusing on CASA, third-party products (TPP), and the Retail, Agri, and MSME (RAM) segments; digital acquisition powered by analytics; and partnership-based models such as co-lending, wealth management products, and fintech collaborations.

Financial highlights (FY25)

A. Balance sheet highlights

| Metric | Value |

|---|---|

| Gross Advances (Total amount lent to various customers including Retail & Corporate) |

₹77,959 Cr (↑6.8% YoY) This number has grown 6.8% compared to last year, demonstrating Karnataka Bank’s growing advances book across retail and MSME sectors. |

| Deposits (Money collected via savings and fixed deposits) |

₹1,04,807 Cr Reflecting strong liability-side growth supported by diversified deposits across regions. |

| Retail Term Deposits | ₹64,600 Cr |

| CASA | ₹33,281 Cr |

| Capital Adequacy Ratio (CRAR) | 19.85% (Tier 1: 18.35%) |

Also read: Entero Healthcare Solutions and the Transformation of Healthcare Distribution

B. Profit & loss highlights

| Metric | Value |

|---|---|

| Net Interest Income (NII) | ₹3,310 Cr |

| Net Profit (PAT) | ₹1,272 Cr |

| Adjusted PAT (excluding one-offs) |

₹1,467 Cr (↑12.3%) |

| Net Interest Margin (NIM) | 3.19% (↓33 bps) Adjusted: 3.23% |

| Other Income (fees, commissions, treasury gains) |

₹1,270 Cr |

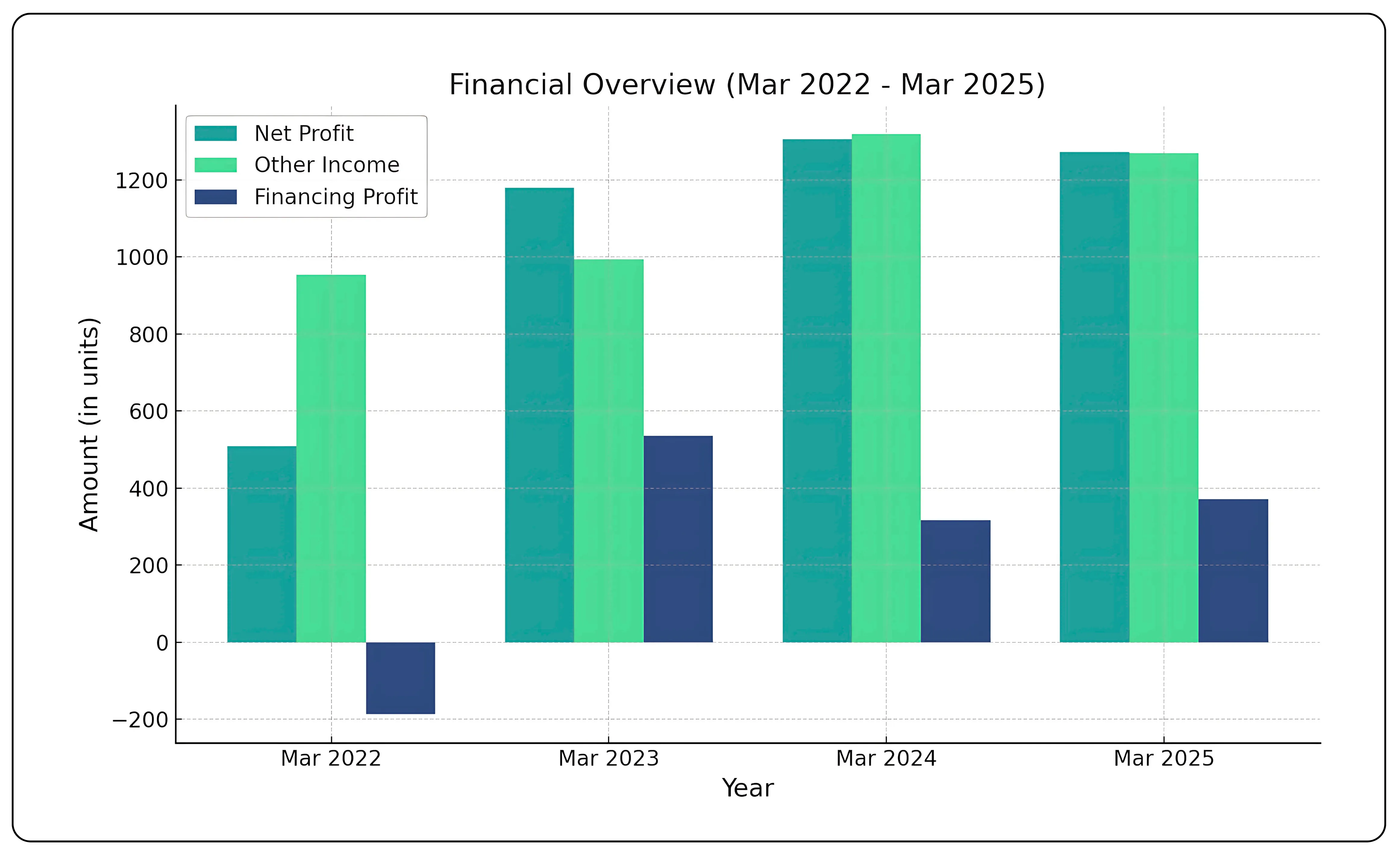

The graph illustrates Net Profit, Other Income, and Financing Profit for Karnataka Bank Ltd. over the fiscal years March 2022 to March 2025:

Net Profit (light blue) shows a strong upward trend from ₹509 crore in FY22 to ₹1,306 crore in FY24, with a slight decline to ₹1,272 crore in FY25—indicating sustained profitability.

Other Income (green) remains consistently high, peaking in FY24 at ₹1,319 crore, highlighting strong revenue from non-interest sources.

Financing Profit (dark blue) improved from a loss of ₹186 crore in FY22 to a profit of ₹371 crore in FY25, reflecting better cost control or financial efficiency. Overall, the bank displays strong financial recovery, diversified income sources, and improved financial stability over the four years.

Other Income breakup for FY24 (₹ in Crores)

| Particulars | 31-Mar-2024 |

|---|---|

| I. Commission, Exchange and Brokerage | ₹612.56 Cr |

| II. Profit/(Loss) on Sale of Investments (Net) | ₹8.724 Cr |

| III. Profit/(Loss) on Revaluation of Investments (Net) | ₹104.80 Cr |

| IV. Profit/(Loss) on Sale of Land, Buildings and Other Assets (Net) | ₹0.42 Cr |

| V. Profit/(Loss) on Exchange Transactions (Net) | ₹10.92 Cr |

| VI. Income from Dividends from Subsidiaries/Joint Ventures | ₹0.00 Cr |

| VII. Miscellaneous Income | ₹581.48 Cr |

| Total Other Income | ₹1,318.90 Cr |

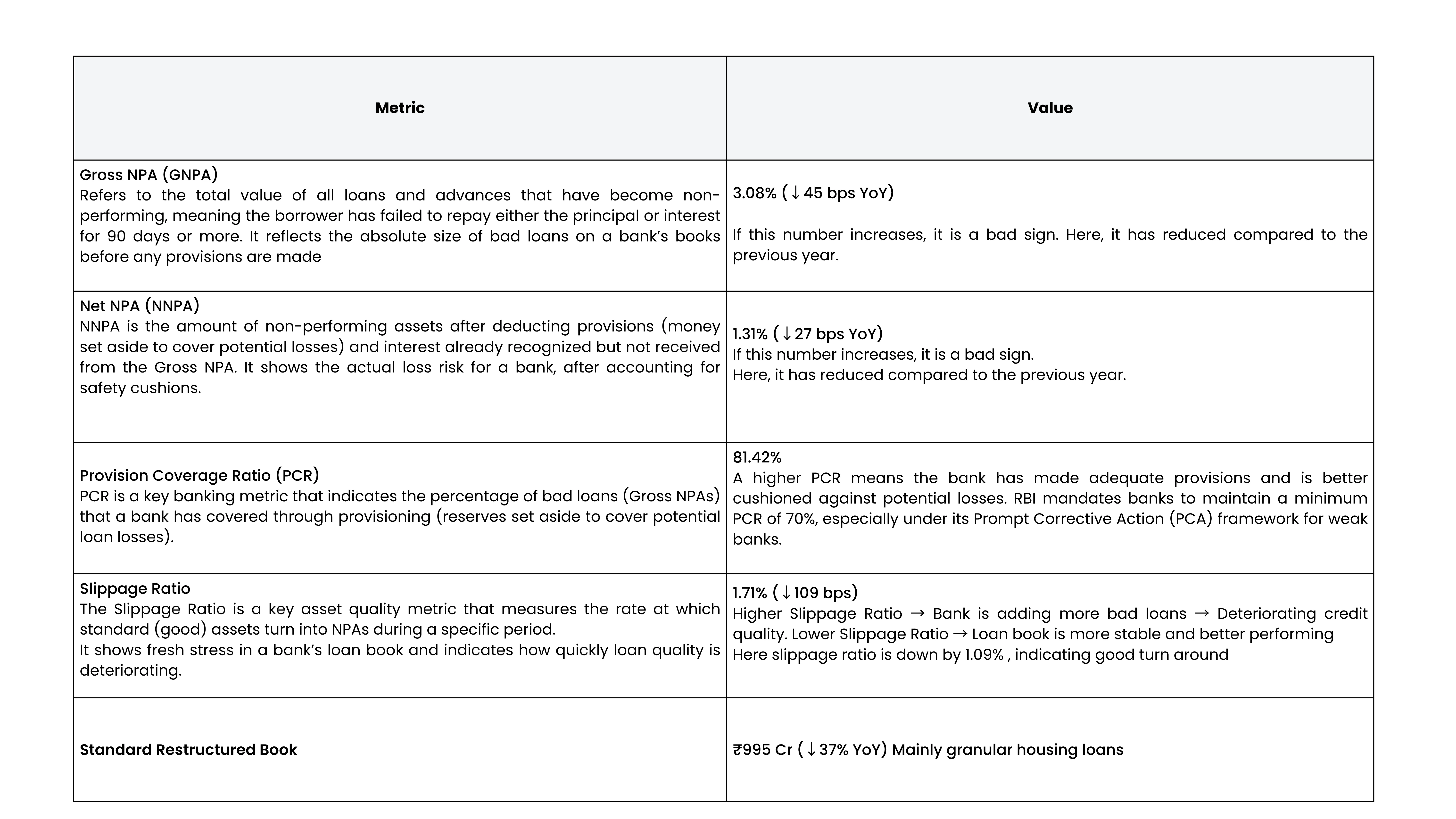

C. Asset quality metrics

Industry outlook & positioning

India’s banking sector continues to demonstrate resilience, supported by a recovery in GDP-led credit demand, improved liquidity conditions, and accelerated digital adoption. In this evolving environment, Karnataka Bank is well-positioned to capitalize on the economic rebound, particularly due to its strong rural footprint and strategic focus on the MSME and agriculture segments.

Several differentiators set Karnataka Bank apart. The bank maintains Tier 1 capital ratio of 18.35%, providing a solid cushion for growth and risk absorption. It has sharpened its emphasis on granular, high-yield retail and MSME lending, ensuring a more sustainable and diversified asset base. Additionally, the bank is undergoing a significant digital transformation, integrating customer relationship management (CRM) systems, advanced analytics, co-lending platforms, and a mobile-first banking approach to enhance customer engagement and operational efficiency. Importantly, Karnataka Bank is also actively reducing its dependence on bulk and NBFC exposures, leading to a measurable improvement in overall credit quality.

Also read: Senores Pharma Capitalizing on CDMO Tailwinds for Global Ascent

Valuation perspective

As of June 2025, Karnataka Bank had a market capitalization of ₹7,397 crore. The earnings per share (EPS) for FY25 stood at ₹33.7, with a trailing price-to-earnings (P/E) ratio of approximately 5.8x, indicating relatively attractive valuations compared to peers. The bank also benefits from a strong capital buffer and high provisioning levels, reinforcing its financial resilience.

Karnataka Bank is currently undergoing a structured transformation—from a legacy bank into a modern, technology-driven institution with a strong focus on retail and MSME lending. While FY25 saw some margin pressures arising from regulatory changes and actuarial provisioning, the adjusted profit growth and continued improvement in asset quality suggest a path of long-term sustainability.

Looking ahead, the bank is well-positioned for a potential re-rating over the next 12 to 18 months. This outlook is underpinned by several positive factors: a high capital adequacy ratio (CRAR), steadily improving asset quality, low credit costs, and the scaling impact of its digital investments, many of which are set to gain traction in FY26. If the expected expansion in net interest margins (NIM) materializes, it could further strengthen earnings and investor sentiment.

Karnataka Bank is an old bank modernizing itself. They’re shifting focus to personal and small business loans, improving customer service with better tech, and reducing risky loans. Despite regulatory headwinds, the bank managed good profits and continues to build strong financials.The bank’s performance is underpinned by core banking fundamentals; growing advances and deposits, improved CASA ratio, and declining slippage. Strategic focus on treasury income and fintech-led expansion further enhances its ability to adapt to a dynamic financial environment.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

©️ 2025 — Tradejini. All Rights Reserved.