For an updated look at FY26 performance trends, read our latest analysis – A Performance Review of Gravita India, VA Tech Wabag, and Deep Industries. It revisits these companies’ financials, margins, and strategic progress since our previous analyses.

When we think of infrastructure, we often picture roads, railways, or metro systems. But there’s one silent hero that’s just as vital water infrastructure and VA Tech Wabag Ltd is quietly leading the way. As a pioneer in modern watertech solutions, Wabag leverages advanced purification and recycling systems to ensure water availability in even the harshest environments.

Unlike typical infrastructure companies involved in cement or steel, Wabag is a pure-play water technology company. It specializes in designing, building, and operating water treatment plants across the world. With more than 6,500 plants commissioned globally, Wabag has already improved the lives of over 88 million people.

Their expertise covers the full spectrum of water management, from purification and desalination to recycling and reuse. They clean water to make it drinkable, treat industrial wastewater to prevent environmental damage, recycle water to ensure sustainability, and desalinate seawater where freshwater is scarce.

Wabag operates through a flexible business model. In some cases, it builds the plant and hands it over. In others, it builds, owns, and operates (BOO & BOOT) the plant for several years before transferring it. A growing portion of their work is also through government-backed Hybrid Annuity Models, where a part of the payment is made upfront and the rest is received over time.

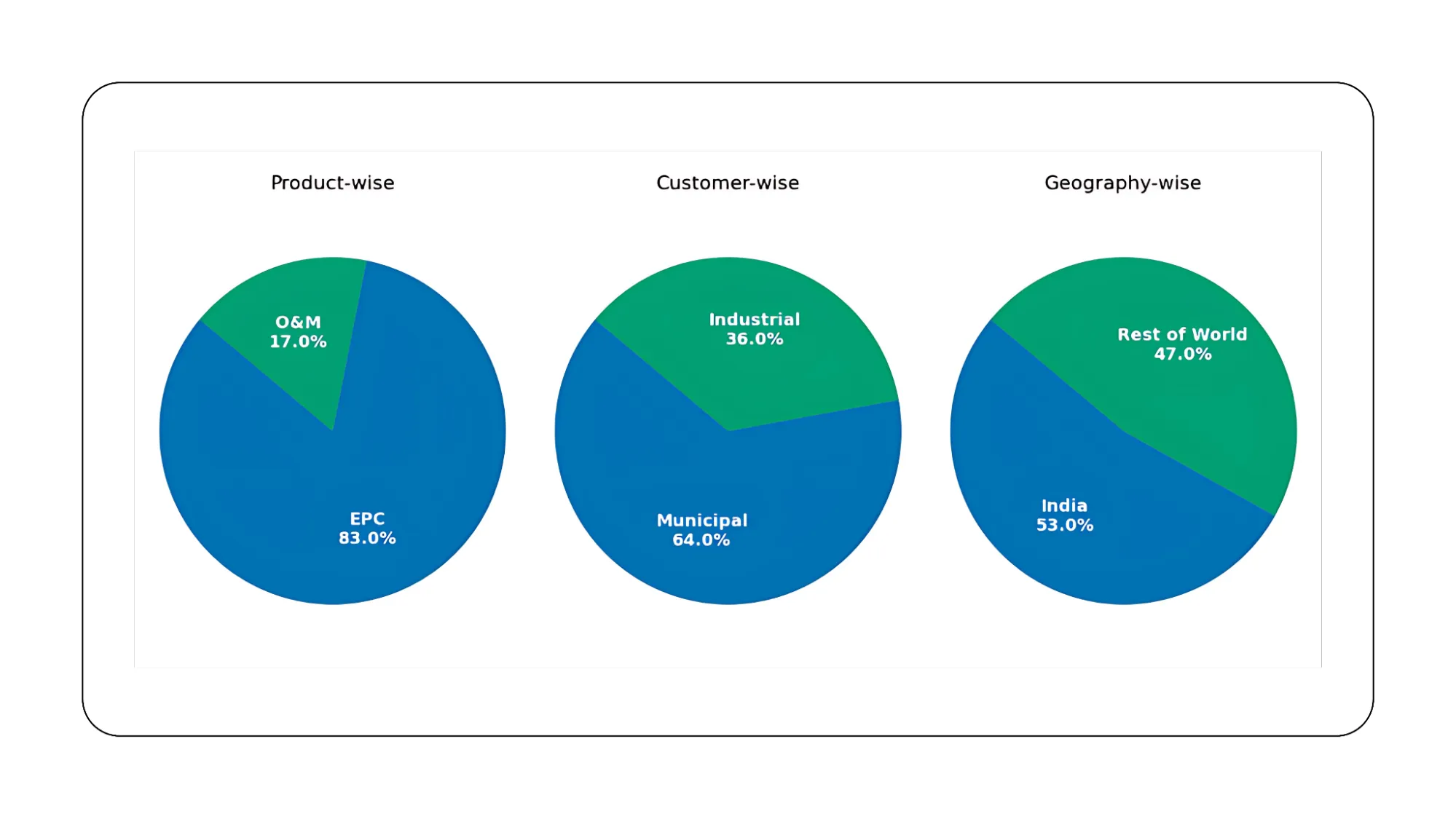

Revenue model

The pie chart illustrates VA Tech Wabag’s business mix across three key dimensions: product type, customer segment, and geographical distribution.

On the product side, 83% of the company's revenue comes from EPC (Engineering, Procurement, and Construction) projects. These are contracts where Wabag is responsible for designing, sourcing materials, and building water treatment plants. The remaining 17% is from O&M (Operations and Maintenance) services, where Wabag manages the day-to-day functioning of water plants, often over multi-year periods. This ensures consistent performance and recurring revenue. The company's operating model balances efficiency and scale, maximizing output across both domestic and international projects.

From a customer perspective, the business is largely driven by municipal clients, accounting for 64% of revenues. These include state and local government bodies seeking clean water supply and wastewater treatment infrastructure. Industrial clients, such as manufacturing plants and power companies, make up the remaining 36%, requiring tailored water solutions for their operations.

Geographically, India remains Wabag’s largest market with 53% of the business coming from domestic projects. However, the company has a strong international presence as well, with the Rest of the World contributing 47%, underlining its global footprint in water technology solutions. Its growing international business showcases Wabag’s push toward globalization and market scalability

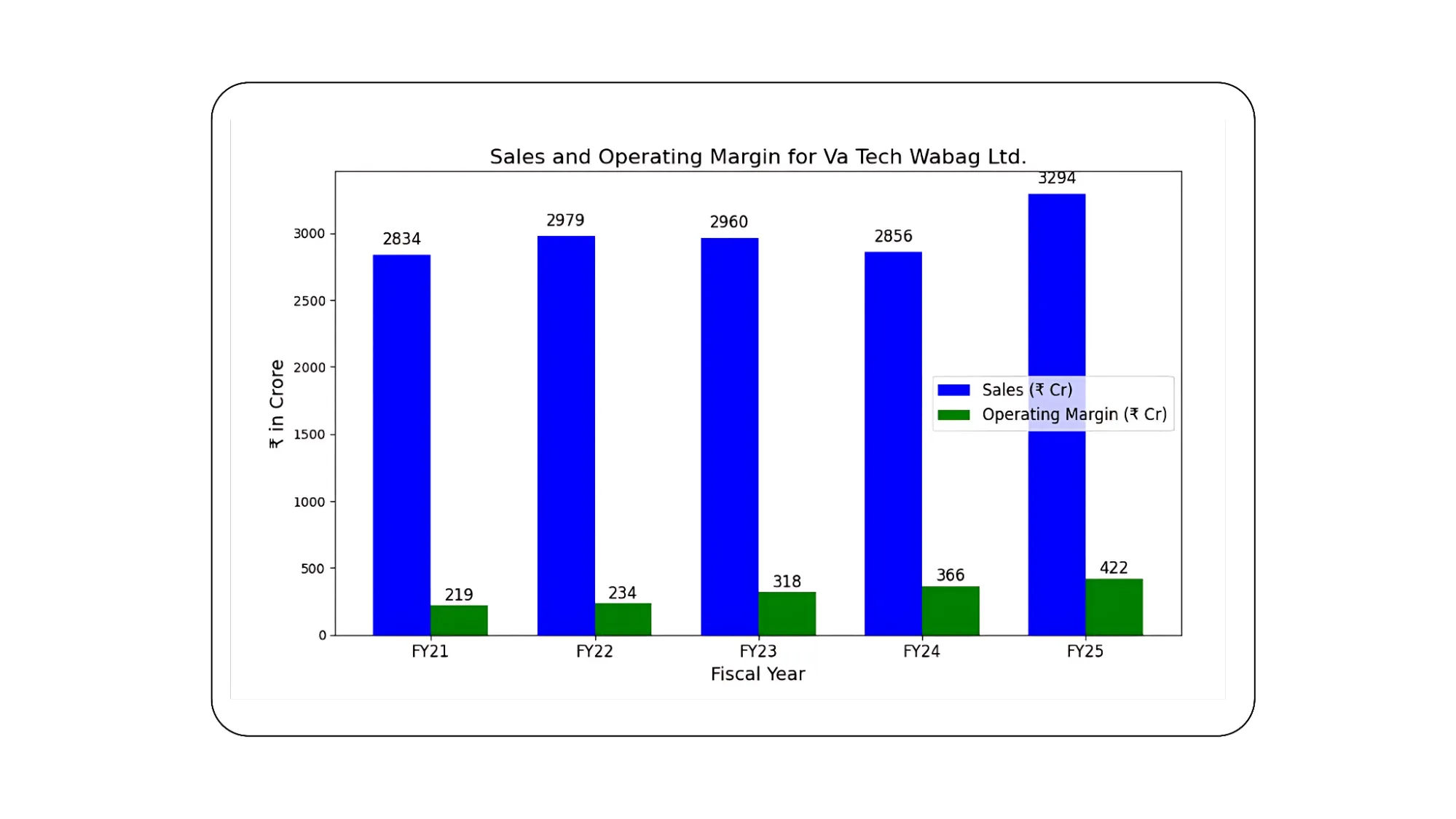

Financial highlights

| Consolidated (INR Crore) | FY25 | Q4 FY25 |

|---|---|---|

| Order Backlog | ₹13,667 ▲ 19% YoY | |

| Revenue | ₹3,294 ▲ 15.3% YoY | ₹1,156 ▲ 23.8% YoY |

| EBITDA | ₹430.2 ▲ 14.2% YoY | ₹140.8 ▲ 21.9% YoY |

| PAT | ₹295.3 ▲ 20.2% YoY | ₹99.5 ▲ 37.4% YoY |

These consistent financial gains reflect Wabag’s operational efficiency and innovation-driven execution in diverse environments.

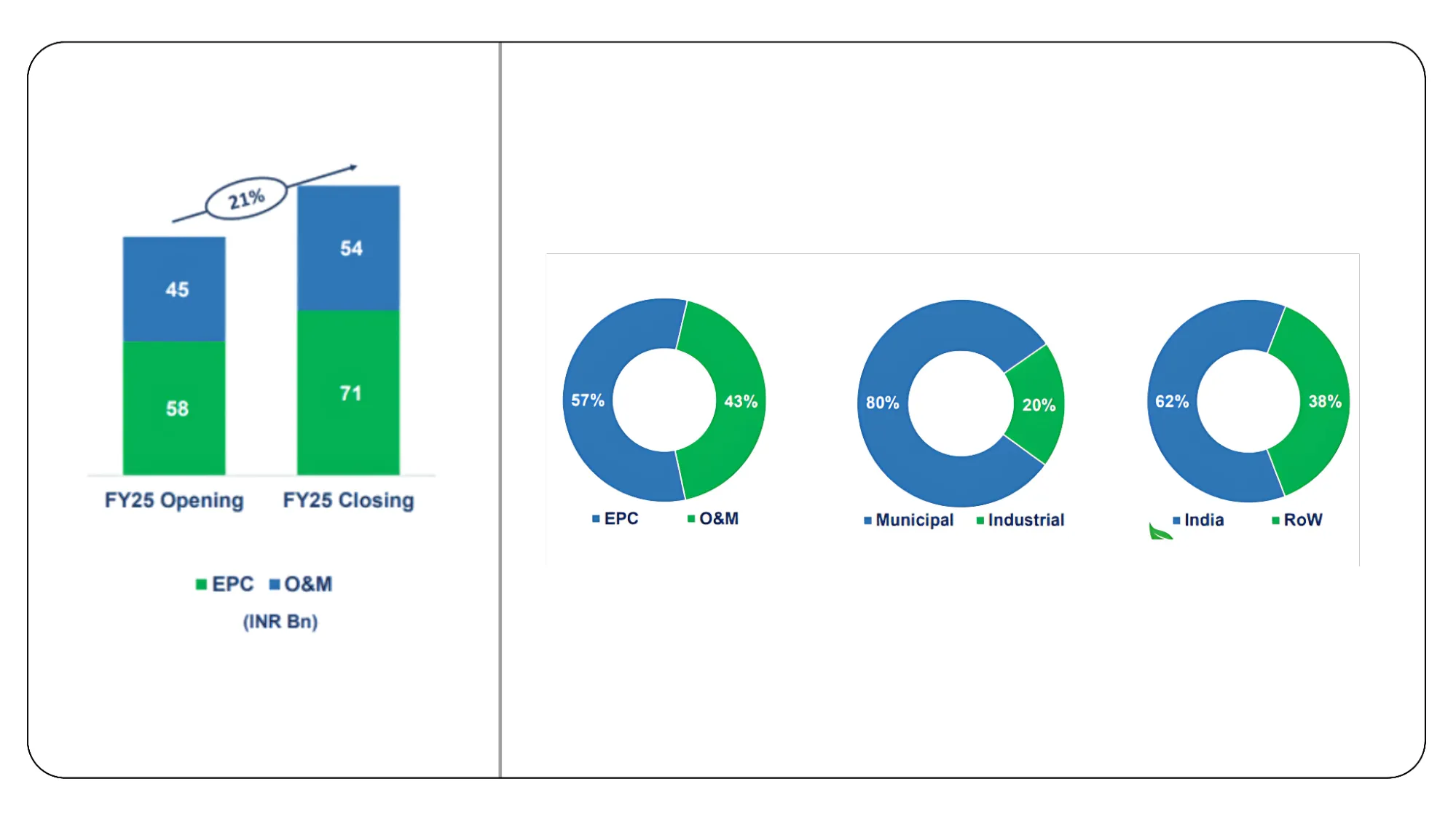

Order book and project pipeline

As of FY25, the order book stood at ₹13,667 Cr, up from ₹10,100 Cr in FY22.

Closing Backlog – FY25 (INR Crore)

By Business Offering & Customer Segment

| Offering | Municipal | Industrial | Total (INR Crore) |

|---|---|---|---|

| EPC | 5,785.1 | 1,325.0 | 7,110.1 |

| O&M | 4,242.2 | 1,131.5 | 5,373.6 |

| Framework | 1,183.0 | ||

| Grand Total | 10,027.3 | 2,456.5 | 13,666.7 |

By Geography

| Geography | Total (INR Crore) |

|---|---|

| India | 7,711.2 |

| Overseas | 4,772.6 |

| Framework | 1,183.0 |

| Grand Total | 13,666.7 |

Major project highlights

Wabag’s global execution reflects its scalability and deep domain expertise in diverse watertech applications.

| Project | Location | Key Highlights |

|---|---|---|

| 400 MLD Desalination Plant(₹4,400 Cr) | Perur, Chennai (India) | Offshore works ahead of schedule; full-scale onshore construction; deliveries ongoing. |

| 200 MLD Pagla STP | Bangladesh | Pile casting at peak momentum; sand filling nearing completion; supply in progress. |

| 69 MLD KUKL-Kodku STP | Nepal | Construction in full swing; major supplies ordered; key deliveries expected by Q2. |

| 270 MLD CIDCO WTP | Mumbai (India) | Supply deliveries almost complete; substructure works nearing completion. |

| 200 MLD WWTP | Al Haer, KSA | Site works and civil construction started; basic engineering approved. |

| 20 MLD WWTP | Ras Tanura, KSA | Engineering completed; project expected by FY27; procurement finalized. |

| 50 MLD SWRO Plant | Senegal | Equipment delivered; installation ongoing; mechanical completion by Q2 FY26. |

| O&M of 40 MLD WWTP | Bahrain | 5-year O&M completed; 100% plant availability; 0.6 million safe man-hours. |

Key clients

Serving municipal and industrial clients worldwide, Wabag delivers purification and conservation solutions tailored to each sector’s needs.

| Category | Clients |

|---|---|

| Municipal | PUB Singapore, Delhi Jal Board, Maynilad, Haya Water, SONEDE, Qatar Public Works Authority, Uttar Pradesh Jal Nigam, CMWSSB (Chennai), Malaviya Jal Nigam, CIDCO, BWSSB (Bangalore), CMA (Morocco), Kathmandu Upatyaka, Bahrain Housing Ministry, BUIDCO, Manila Water |

| Industrial | Dangote, MARAFIQ, Reliance Industries, GAIL (India), NMDC, INDOSOL, HMEL, SIBUR, BAPCO, Indian Oil, ONGC, MRPL, PETRONAS, CPCL, Nayara Energy |

| Funding Agencies | India Exim Bank, KfW (Germany), JICA (Japan), Asian Development Bank (ADB), European Investment Bank, Asian Infrastructure Investment Bank (AIIB), World Bank (IBRD-IDA), Namami Gange |

| Client Sectors Served | Municipal Water & Wastewater, Oil & Gas, Power Plants, Steel, Food & Beverages, Fertilizer and Industrial Parks |

R&D and innovation initiatives

Wabag has more than 125 patents for its technologies and runs research centers in both India and Europe to develop new and better water treatment solutions supporting its mission of innovation and global scalability. It is focused on “manufactured water” through desalination and reuse technologies, aligning with global trends in sustainability and water scarcity.

In FY24, Wabag launched the “BLUE SEED” initiative to fund water-tech startups and partnered with Peak Sustainability Ventures to develop 100 Bio-CNG plants across various regions, targeting a business potential of $200 million targeting a scalable business potential of $200 million in the clean energy and watertech ecosystem.

Divestments and asset strategy

The company completed the sale of its Romanian subsidiary in August 2024 for €1.2 Mn to reduce European exposure. In FY24, to maintain an asset-light balance sheet, the company inducted equity partners in two out of its three HAM-based Special Purpose Vehicles (SPVs). This strategic move allowed it to share project ownership and funding responsibilities, thereby reducing capital intensity and limiting the burden of large assets and associated debt on its books. This shift supports a more efficient, asset-light model focused on margin improvement and return on capital.

Market outlook

Va Tech Wabag is well-positioned to benefit from strong opportunities in both domestic and international markets, driven by rising demand for water and wastewater treatment solutions designed around conservation, recycling, and efficiency.

India is a key growth market, supported by government initiatives like Jal Jeevan Mission and Namami Gange. The Ministry of Jal Shakti has been allocated around ₹99,500 crore, with additional projects worth ₹45,000 crore expected to be awarded soon. Growth in power, refining, petrochemicals, and green energy (e.g., Bio-CNG, solar, hydrogen) will further drive demand for water treatment solutions.

In Indonesia, driven by urban expansion, the wastewater treatment market is expected to grow at a CAGR of 6.6% between 2024 and 2030, backed by a government investment of ₹83,000 crore under the National Strategic Plan.

Singapore is increasing its water recycling target from 40% to 55% by 2060. The market is set to grow from ₹12,450 crore in 2023 to ₹17,430 crore by 2030. Vietnam's water sector is projected to grow at a CAGR of 13.68% during 2024–2032, while Malaysia’s industrial wastewater treatment market is expected to grow at a CAGR of 4.2% during 2024–2030.

In the Middle East, water consumption is expected to rise by 62% by 2025. With 63% of the region's water supplied through desalination and rising reuse of treated wastewater, the demand for advanced water infrastructure remains high.

Saudi Arabia has committed ₹2.65 lakh crore for desalination by 2027, including ₹99,600 crore through PPP projects under its Vision 2030 strategy.

The United Arab Emirates has announced an investment of ₹17,300 crore in desalination, alongside initiatives focused on sustainability and water security. In Africa, rising investments in desalination (particularly in northern and western regions) and increased adoption of PPP and EPC+F models are driving growth. The Africa Water Investment Action Plan aims to mobilize ₹2.5 lakh crore annually for water and sanitation by 2030.

Competitive advantage of Va Tech Wabag

Va Tech Wabag stands out as a leading global water technology company with several strong competitive advantages. It is ranked among the top three desalination players globally and has established a strong brand presence, particularly in the Middle East and Africa (MEA) region. The company benefits from economies of scale and cost efficiency through energy optimization and smart technologies.

Its diversified portfolio spans municipal, industrial, desalination, and recycling projects, supported by proprietary technology and in-house R&D. Wabag’s global reach, with operations in over 25 countries,has enabled it to scale operations efficiently and bring its watertech solutions to emerging and developed markets alike, accelerating globalization and market scalability.

Strategic expansion into new geographies like GCC, Africa, and Central Asia, along with a strong offshore team and long-standing client relationships, further bolster its market leadership. The company’s collaborative approach, focus on sustainability, and AI-driven operational efficiencies position it well for continued growth in the evolving water infrastructure sector.

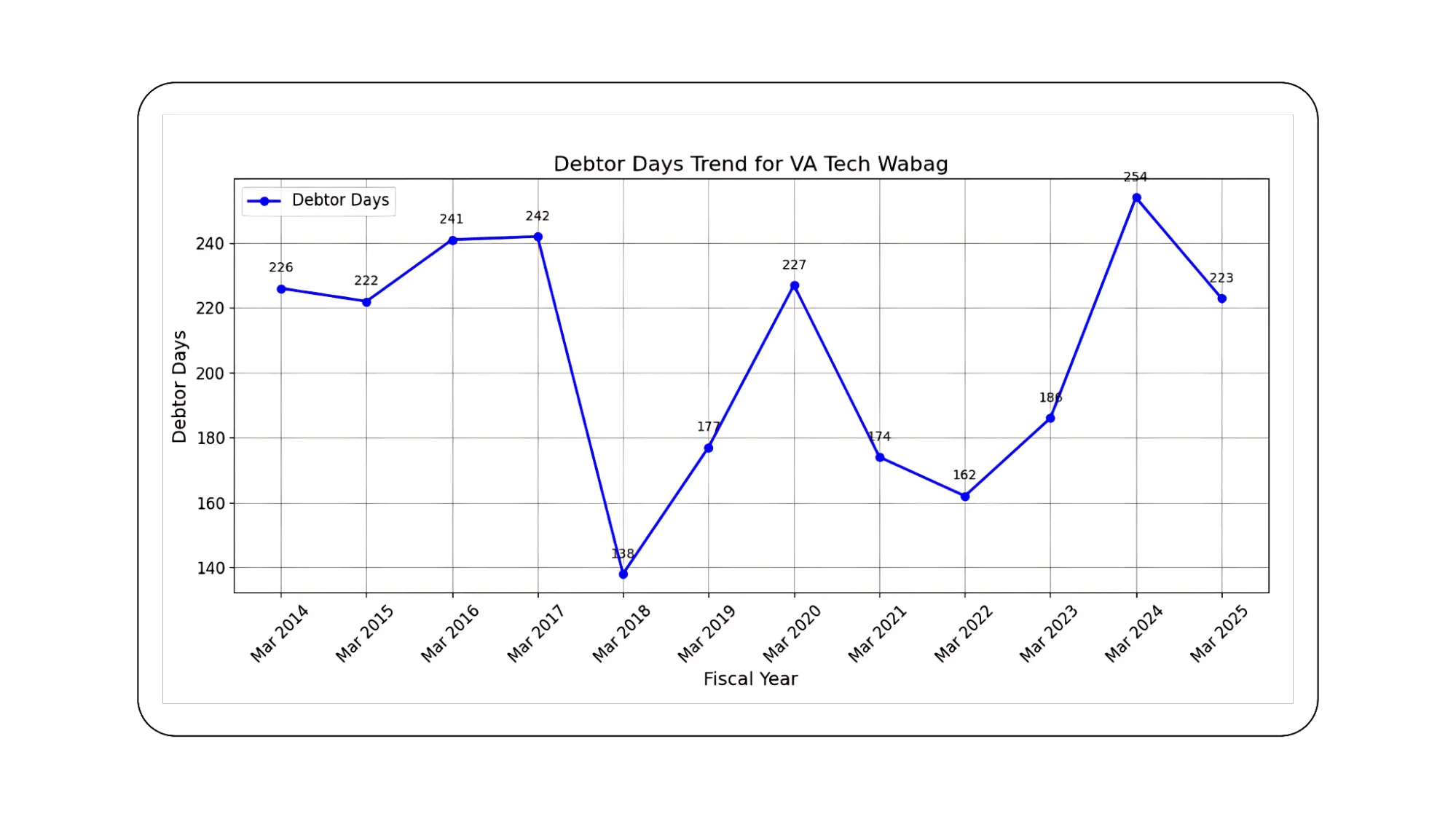

Understanding Debtor Days and Their Impact on VA Tech Wabag Ltd.

Debtor days, also known as days sales outstanding (DSO), measure the average number of days it takes a company to collect payments from its customers after a sale is made. For EPC (Engineering, Procurement, and Construction) and O&M (Operations & Maintenance) companies like VA Tech Wabag, this metric is a key indicator of working capital efficiency and cash flow health.

Historically, Wabag’s debtor days have been volatile, ranging from 138 to 254 days over the past 12 years. In FY24, the debtor days rose to 254, indicating a longer cash conversion cycle, before slightly improving to 223 in FY25. Higher debtor days can strain liquidity, especially in capital-intensive businesses like water infrastructure where project execution costs are front-loaded. It may lead to greater reliance on short-term borrowings to fund operations, affecting profitability through increased interest costs.

A high DSO is particularly concerning in municipal contracts, where payment delays are common due to government bureaucracy or project-level clearances. This can delay reinvestment into new projects or expansions, potentially slowing down growth. Conversely, reducing debtor days improves cash flow, lowers dependency on external funding, and enhances operational agility—an important goal as Wabag continues to scale up its order book and move into hybrid and annuity models where steady cash inflows are critical.

Going forward, a tighter grip on receivables, better project structuring, and more selective client engagement could help Wabag optimize its debtor cycle, thus supporting both margins and balance sheet strength. Streamlining receivables not only boosts efficiency, but also strengthens Wabag’s ability to reinvest in R&D and cutting-edge watertech.

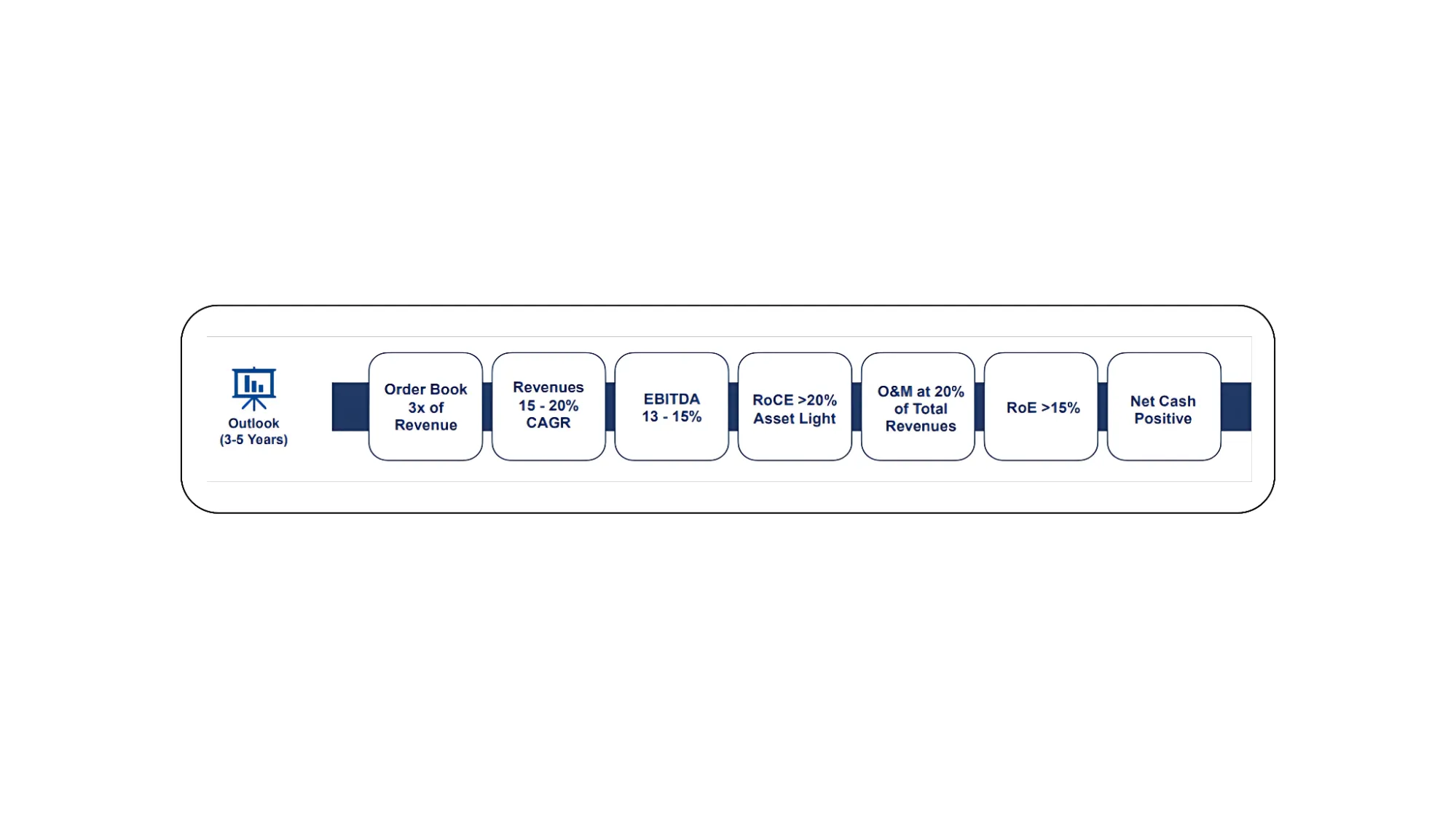

Valuation based on future plans

Revenue growth: Targeting 15–20% CAGR over FY27–FY29

Order book: Maintain ~3x revenue -Geographic focus: India & MEA(Middle East and Africa) to drive growth

Revenue mix target:

- 50%+ International

- 30% Industrial

- 20%+ from O&M

Technology and sustainability: Continued focus on circular economy, ESG-aligned solutions, and IP-driven execution

Current valuation

Current market Cap: ₹10,055 Cr

Current price: ₹1,617

Stock P/E: 34.1

Projected estimated PE

| Metric | FY27E | FY28E | FY29E |

|---|---|---|---|

| Revenue (₹ Cr) | 4,373 – 4,758 | 5,029 – 5,710 | 5,782 – 6,851 |

| Net Profit (₹ Cr) | 392 – 426 | 450 – 512 | 517 – 614 |

| EPS (₹) | 65.3 – 71.0 | 75.0 – 85.3 | 86.2 – 102.3 |

| Forward P/E (₹1,617) | 24.8x – 22.8x | 21.6x – 18.9x | 18.8x – 15.8x |

Va Tech Wabag stands as a strong player in the global water technology space. With a healthy order book, innovation-focused model, and expanding international footprint, the company is well-positioned to capitalize on growing demand for sustainable water infrastructure, particularly in emerging markets like Middle East and Africa (MEA) and South Asia.

Also Read: Gravita India’s Recycling Leadership with a Global Edge

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

©️ 2025 — Tradejini. All Rights Reserved.