For years, the Indian shipbuilding industry sat at the edges of a broader industrial story, overshadowed by sectors like banking, IT, and manufacturing . That is beginning to change. A combination of forces that rarely align at the same time is now coming together. Global shipping fleets are ageing faster than they are being replaced. Environmental regulations are forcing operators to retire vessels earlier than planned. And closer home, India is quietly putting capital, policy, and strategic intent behind building a domestic maritime ecosystem. This is not a cyclical upswing driven by freight rates. It is a structural shift.

Across the post-pandemic decade, few industries have been repositioned as deliberately as maritime, and India's maritime sector is among the most consequential of these transformations. What was once a peripheral sector is now moving closer to the centre of industrial policy, backed by defence spending, infrastructure expansion, and global regulatory change.

This report examines the structural drivers, policy environment, and competitive dynamics shaping India’s shipbuilding and maritime services industry.

Global Shipbuilding Market: Size and Structural Positioning

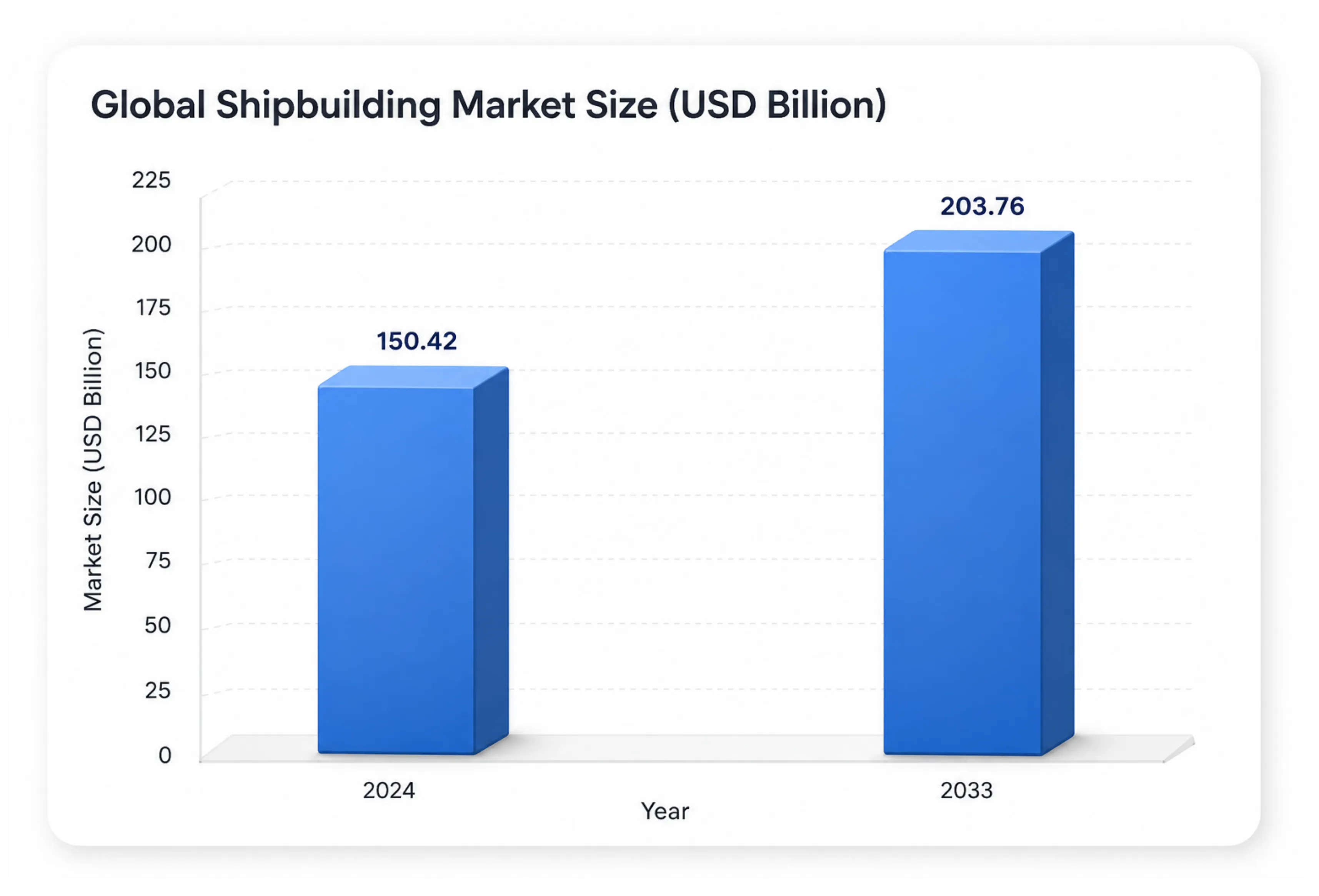

Of all manufacturing industries tied to global trade, shipbuilding carries among the longest lead times, the greatest capital intensity, and the most concentrated geographic production base. Valued at USD 150.42 billion in 2024, the global shipbuilding market is projected to reach USD 203.76 billion by 2033, expanding at a CAGR of 3.43 % over the 2025–2033 forecast period.

That growth trajectory, modest by industrial standards, understates the structural shift underway: the global order book as of early 2024 represented 12 % of deadweight tonnage, comprising 4,870 vessels and 283 million tonnes.

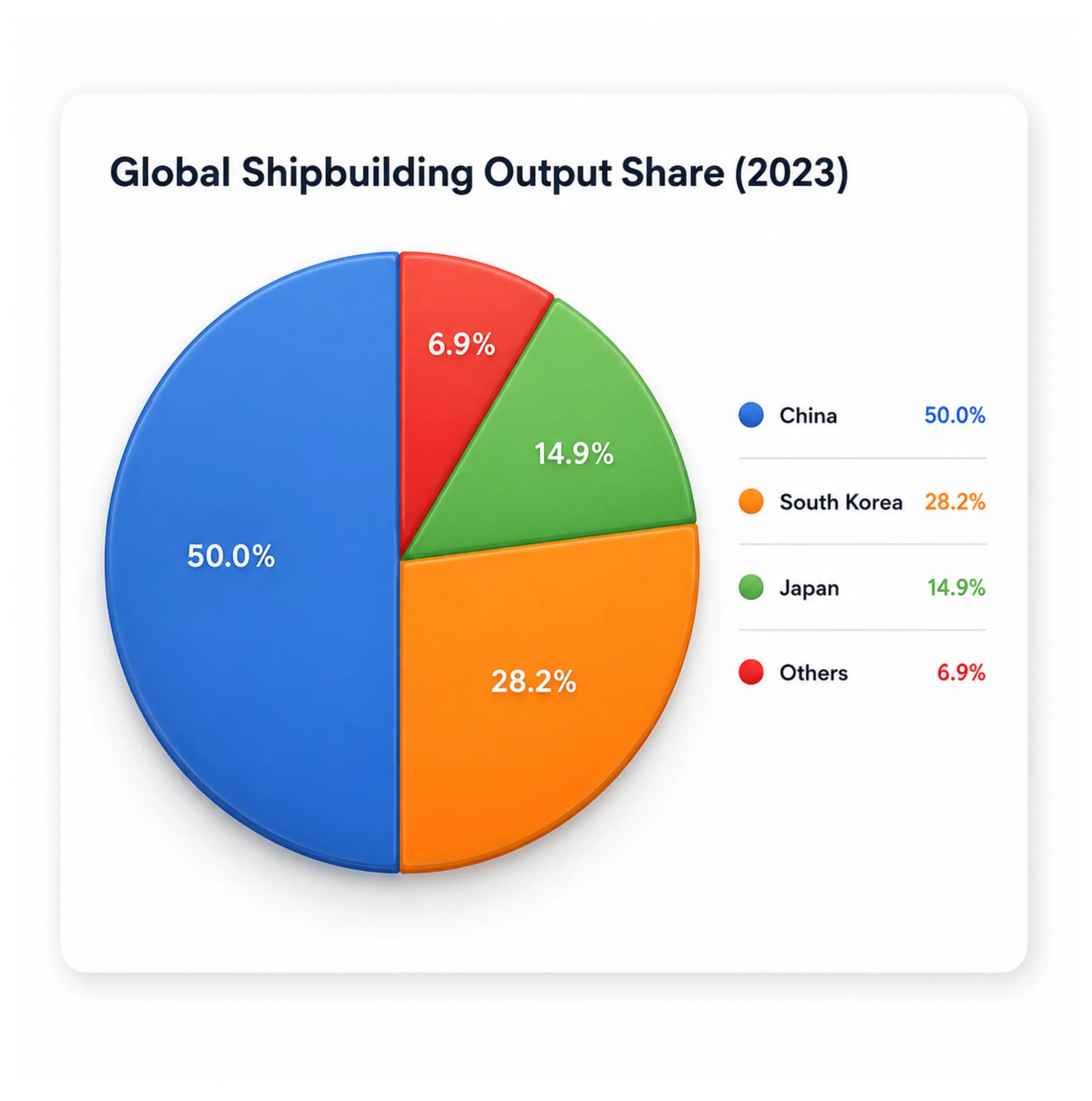

Geographic concentration in global shipbuilding remains extreme. China, South Korea, and Japan account for approximately 95 % of global output, with China alone delivering over 50 % of new ship capacity in 2023; the first time any single nation crossed that threshold. South Korea contributed 28.2% and Japan 14.9% in the same year.

For nations seeking to build maritime industrial capacity, this concentration presents both the opportunity and the challenge: demand for alternatives is real, but the cost and capability gap is substantial.

Also Read: Navigating India's Wastewater Treatment Mega Cycle

Demand Trends and Global Tailwinds

Several distinct forces are converging to sustain orderbook growth. Regulatory pressure stands out as the most non-discretionary driver. The European Union's Emissions Trading System, alongside the IMO's mandatory Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII) (both of which became compulsory in 2023) are forcing the phase-out of older, fuel-inefficient vessels at an accelerating pace. The IMO's 2023 GHG Strategy targets net-zero shipping emissions by 2050. The greening of the global order book is actively underway, with a rising share of vessels being ordered with dual-fuel or alternative-fuel capability. LNG carriers exemplified this trend: from approximately 27% of fleet capacity in 2022, LNG carrier orderbooks surged to over 51 % of that vessel class in early 2024.

Fleet ageing reinforces this replacement cycle. Global fleet ageing has accelerated this pressure, with the average vessel age rising and a growing share of ships approaching end-of-service life well ahead of earlier projections. Structural softness in earnings, paradoxically, sharpens the case for fleet renewal as operators seek newer vessels to reduce voyage costs.

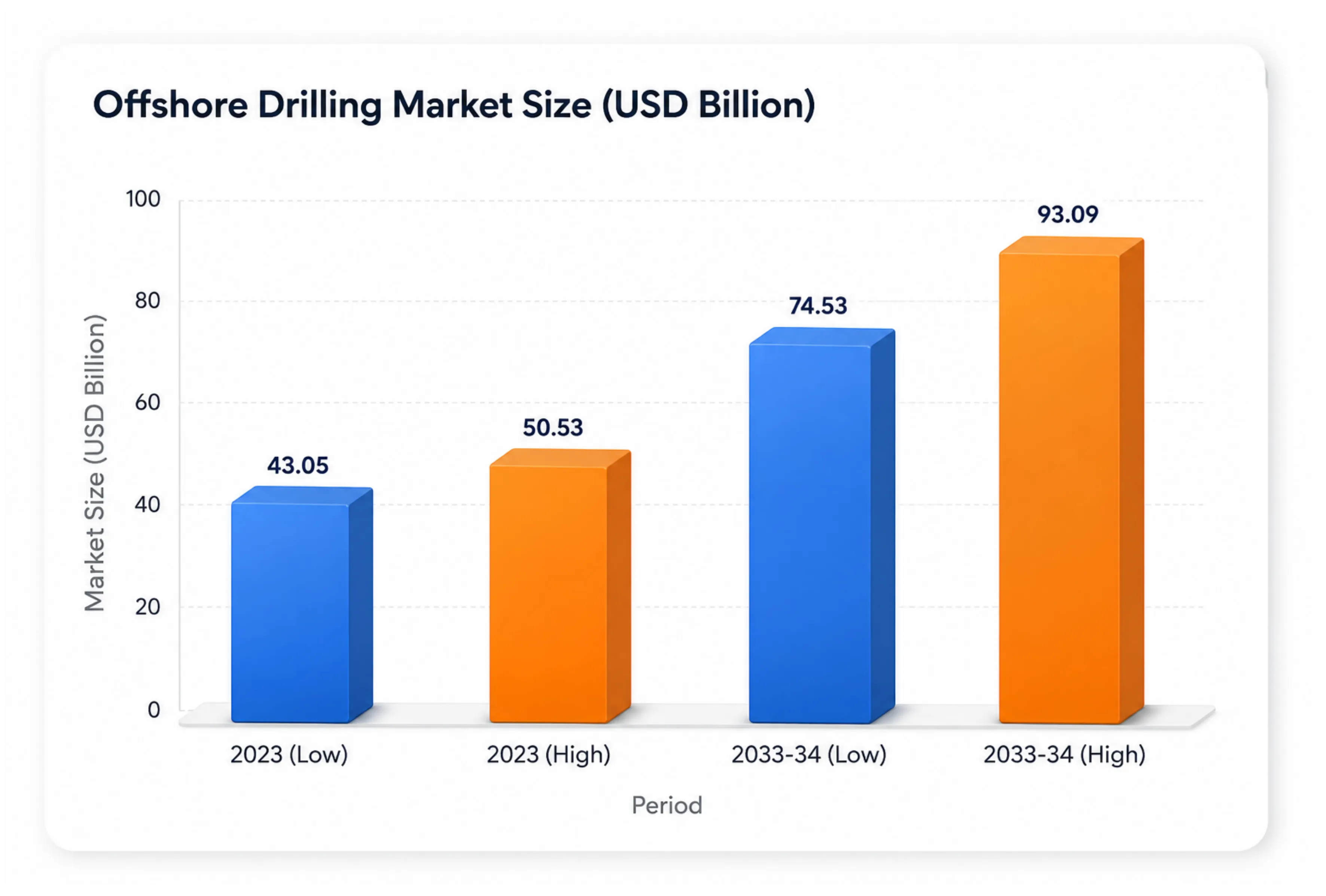

Offshore oil and gas, the primary driver for offshore support vessels, presents a separate demand stream. Global oil demand is anticipated to reach approximately 104.8 to 106.5 million barrels per day in 2026 (forecasted by International Energy Agency (IEA) and OPEC). The offshore drilling market is projected to grow from USD 43.05 to USD 50.35 billion in 2025 to reach USD 74.53 to USD 89.69 billion by 2033-2034, exhibiting a CAGR of 6.6% to 8.48% during the forecast period.

The inflection point for offshore capital expenditure is visible in India: the country imports over 85 % of its crude oil requirements, and ONGC's sustained exploration and production programmes on both the west coast (Mumbai High, Bassein) and the east coast (Krishna Godavari Basin) constitute the primary domestic demand source for offshore support vessel operators.

India Growth Outlook

Maritime trade carries approximately 95 % of India's merchandise trade by volume and 70 % by value. Against this backdrop, the government's long-term maritime roadmaps (Maritime India Vision 2030 and Maritime Amrit Kaal Vision 2047) target a position among the top ten shipbuilding nations by 2030 and top five by 2047, forming the centrepiece of India's maritime policy architecture.

The policy architecture supporting this ambition is gaining tangibility. The Sagarmala programme is projected to drive a 15-fold increase in coastal and inland waterway traffic over two decades while expanding dedicated coastal and inland port capacity nearly five times from its current 350 million tonnes, creating sustained demand for new vessels and dredging. The Union Budget 2025-26 established a dedicated Maritime Development Fund, and the Shipbuilding Financial Assistance Policy (2015) had earmarked ₹4,000 crore over ten years to provide direct financial support to shipbuilders, including customs and excise exemptions on construction materials. The Indian Naval Indigenisation Plan (INIP) 2015–2030 further mandates increasing indigenous content across warship and submarine programmes, with MDL's own indigenisation drives having measurably reduced import dependency over the five years to FY25.

Defence shipbuilding alone represents an opportunity exceeding ₹1.5 lakh crore over the next decade. The combined Indian Navy and Coast Guard fleet expansion programme (targeting 200 ships each over 15 years) implies more than 150 warship orders flowing to domestic yards over the period. Commercial shipbuilding adds a parallel dimension: coastal shipping, ferries, and gas carrier segments together represent an opportunity worth ₹12,000 to ₹15,000 crore annually, with the Sagarmala programme's push to triple the coastal and inland waterways fleet acting as the structural demand catalyst.

The ship repair opportunity, currently dominated by yards in China, Singapore, and the Middle East, offers India a clear geographic arbitrage. With 7 to 9 % of global trade passing within 300 nautical miles of India's coastline and the country's market share in global ship repair below 1 %, the addressable opportunity remains largely uncaptured.

Competitive Landscape

Core Defence & Commercial Shipbuilders (The Manufacturers)

Mazagon Dock Shipbuilders Limited ( MDL)

As the sole Indian shipyard to have built destroyers, frigates, and conventional submarines domestically, MDL occupies an unmatched position in the country's defence industrial base. The yard was conferred Navratna status in June 2024, reflecting both its strategic importance and improving financial performance. Current capacity allows simultaneous construction of ten warships and eleven submarines. A new Floating Dry Dock of 12,000-tonne capacity is under construction at the Nhava Yard, alongside a green-field development to handle large vessels and submarines in the long term.

Cochin Shipyard Limited (CSL)

Cochin Shipyard Limited occupies a unique position in the domestic maritime ecosystem, possessing the capability to construct and repair complex, large-scale platforms ranging from SuezMax carriers to India's indigenous aircraft carriers. As of early FY26, the company holds a robust order book of approximately ₹21,100 crore (dominated by defence contracts at 65%), providing strong revenue visibility, while actively tracking a massive prospective shipbuilding pipeline as estimated by the company at ₹2.85 lakh crore. Beyond its core defence focus, CSL is aggressively expanding its commercial and repair footprint. The yard's infrastructure augmentation including a New Dry Dock and an International Ship Repair Facility (ISRF) coupled with recent strategic partnerships with Drydocks World (UAE) and HD KSOE (South Korea), positions the company to compete directly for global commercial shipbuilding and ship repair contracts.

Garden Reach Shipbuilders & Engineers Limited (GRSE)

GRSE has delivered 800-plus vessels over its 65-year history and holds the distinction of having delivered 111 warships to the Indian Navy, Indian Coast Guard, and foreign navies, the highest by any domestic yard. Beyond warship construction, GRSE has diversified into zero-emission vessels, autonomous underwater vehicles, portable steel bridges, and a dedicated commercial shipbuilding division targeting export markets.

Also Read: Sector Analysis of the Indian Automotive Component Industry

Fleet Operators & Offshore Services (The Asset Owners)

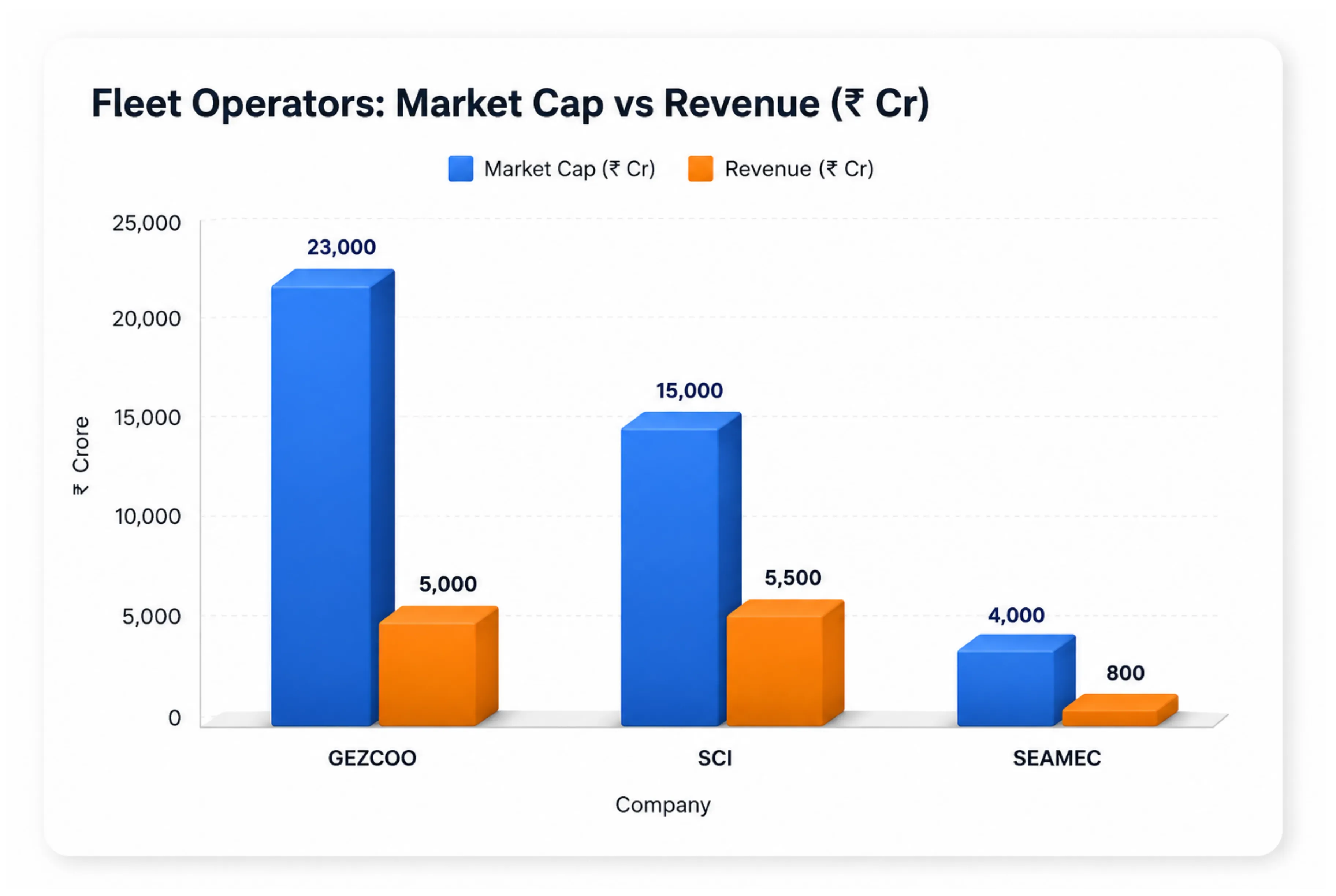

The Great Eastern Shipping Company Limited (GESCO)

The country's largest private shipping company, GESCO operates 38 vessels aggregating 3.04 million deadweight tonnes as of March 31, 2025, spanning crude tankers, product tankers, LPG carriers, and dry bulk carriers.

Shipping Corporation of India Limited (SCI)

As India's national carrier operating across tankers, bulk carriers, liners, and offshore vessels, SCI presents a diverse exposure to global shipping markets. The company's liner division operates five container vessels with a nominal capacity of 20,000 TEUs, and its dry bulk fleet of 15 vessels (eight modern Supramax and seven Panamax/Kamsarmax carriers) is relatively young at an average age of 13.1 years.

Seamec Limited

Operating in the offshore support vessel segment primarily serving ONGC's domestic exploration requirements, its business is asset-heavy with the fixed-cost nature of the DSV business.

Maritime Infrastructure (The Enablers)

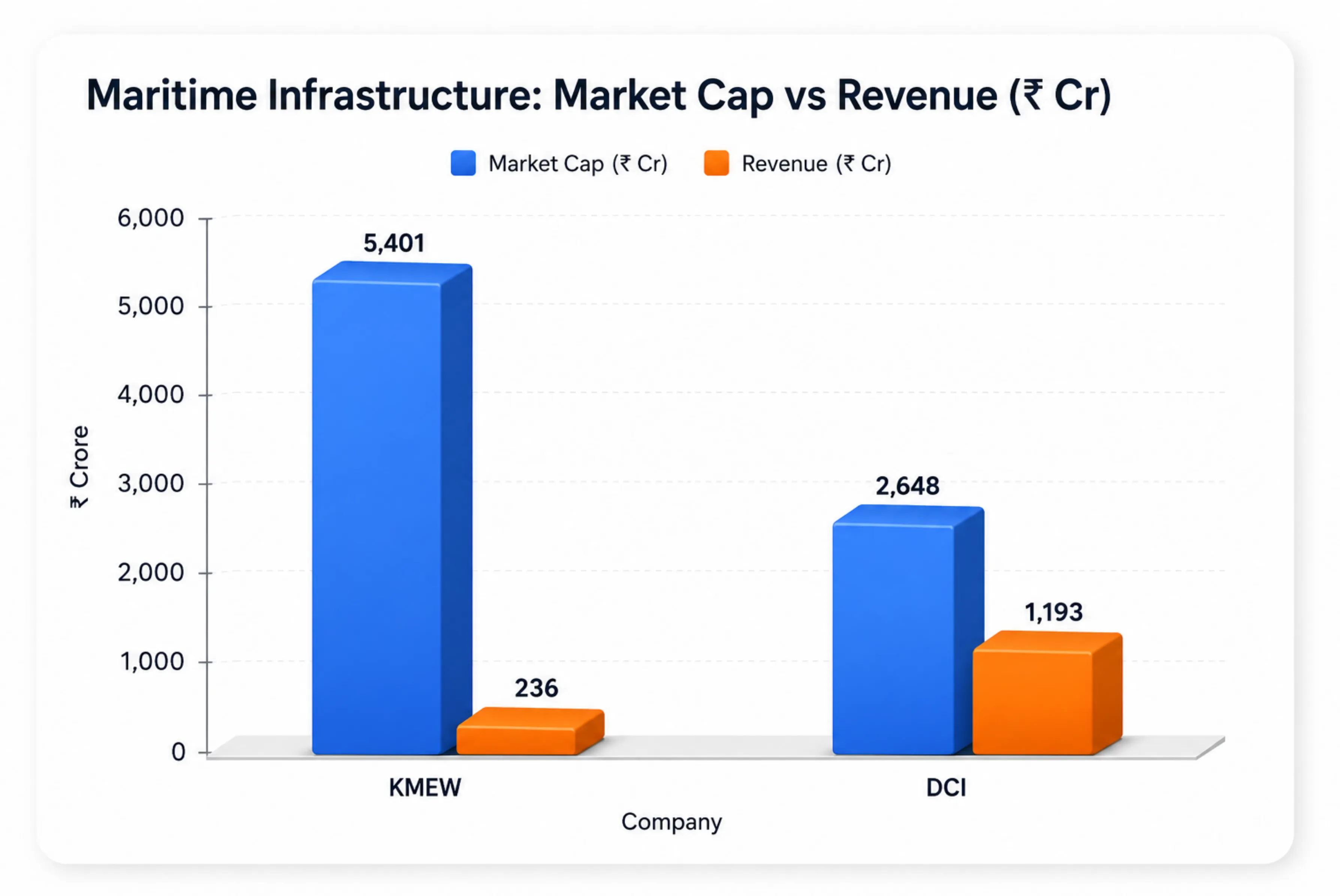

Dredging Corporation of India Limited (DCI)

DCI holds a near-monopoly position in India's port dredging market, maintaining depth at all major ports and executing capital dredging for new port infrastructure. The long-term demand outlook remains intact given port expansion plans and the Sagarmala programme, but near-term execution risk is elevated.

Knowledge Marine & Engineering Works Limited (KMEW)

While DCI dominates large-scale capital dredging, KMEW has emerged as a fast-growing private-sector player in the maritime infrastructure segment. Operating a fleet of 45 specialised crafts, the company focuses on niche areas such as river dredging, port ancillary services, and pilotage, where operational flexibility provides an advantage over larger public-sector players. As of Q3 FY26, KMEW reports strong operating margins and an order book of around ₹1,500 crore, offering multi-year revenue visibility.

Beyond traditional dredging, the company is expanding into commercial shipbuilding and long-duration green tug charter contracts with major ports, which are expected to provide more stable, annuity-like cash flows. The shift to the tonnage tax regime and participation in inland waterways-related projects could support growth, although execution and order conversion remain key variables.

Financial Comparison

For investors assessing India shipbuilding stocks, the three segments of defence manufacturers, fleet operators, and maritime enablers require entirely different valuation frameworks, as their revenue drivers, margin structures, and risk profiles share little in common.

1. Core Defence & Commercial Shipbuilders (Manufacturers)

| Company | Market Cap (₹ Cr) | Revenue (₹ Cr) | OPM / EBITDA Margin (%) | D/E Ratio | Key Driver / KPI |

|---|---|---|---|---|---|

| Mazagon Dock Shipbuilders Limited (MDL) | 1,06,492 | 12,330 | 16% | 0.05 | ₹23,758 Cr Order Book (Strong execution visibility) |

| Cochin Shipyard Limited (CSL) | 44,882 | 4,745 | 15% | 0.18 | ₹21,100 Cr Order Book (With ₹2.85 Lakh Cr pipeline) |

| Garden Reach Shipbuilders & Engineers Limited (GRSE) | 33,153 | 6,525 | 10% | 0.01 | Robust Naval Order Book (Driven by MoD contracts) |

(All figures are TTM as of December 2025 unless stated otherwise. Market capitalisation is approximate, as of April–May 2026.)

2. Fleet Operators & Offshore Services (Asset Owners)

| Company | Market Cap (₹ Cr) | Revenue (₹ Cr) | OPM / EBITDA Margin (%) | D/E Ratio | Key Driver / KPI |

|---|---|---|---|---|---|

| The Great Eastern Shipping Company Limited (GESCO) | 21,876 | 5,121 | 53% | 0.08 | 38 Vessels (Driven by Global Freight Rates) |

| Shipping Corporation of India Limited (SCI) | 14,889 | 5,592 | 35% | 0.33 | Diversified Fleet (Container, Tankers, Bulk) |

| SEAMEC Limited | 3,992 | 825 | 39% | 0.38 | Charter Utilization (ONGC & Offshore EPC contracts) |

(All figures are TTM as of December 2025 unless stated otherwise. Market capitalisation is approximate, as of April–May 2026.)

3. Maritime Infrastructure (Enablers)

| Company | Market Cap (₹ Cr) | Revenue (₹ Cr) | OPM / EBITDA Margin (%) | D/E Ratio | Key Driver / KPI |

|---|---|---|---|---|---|

| Knowledge Marine & Engineering Works Limited (KMEW) | 5,401 | 236 | 40% | 0.61 | ₹1,500 Cr Order Book (Green Tugs & Inland Waterways) |

| Dredging Corporation of India Limited (DCI) | 2,648 | 1,193 | 15% | 0.95 | Govt Port Capex (Sagarmala & Major Ports) |

(All figures are TTM as of December 2025 unless stated otherwise. Market capitalisation is approximate, as of April–May 2026.)

Government Policy and Regulatory Impact

India's maritime policy operates through multiple channels, each shaping different segments of the industry in distinct ways. For defence shipyards, single-customer concentration remains both a structural strength and a limitation. Companies like Mazagon Dock Shipbuilders Limited and Garden Reach Shipbuilders & Engineers Limited derive the majority of their revenues from the Ministry of Defence. This provides long-term revenue visibility and insulation from commercial shipping cycles, but also creates dependence on procurement timelines and budget allocations. Delays in approvals, nominations, or supplier decisions can lead to execution slippages and cost pressures, a characteristic common across global defence contractors.

For commercial shipping companies, regulation is acting in two opposing directions. On one hand, decarbonisation mandates from the International Maritime Organization and the European Union’s Emissions Trading System are accelerating vessel obsolescence, driving fresh demand for new, compliant ships. On the other hand, these same regulations impose significant capital requirements. Companies such as The Great Eastern Shipping Company Limited and Shipping Corporation of India Limited must invest in retrofits or fleet replacement, often at elevated newbuilding costs, which impacts near-term returns.

The Strategic Partnership Model introduced under India’s defence procurement framework marks a structural shift in how large naval platforms are sourced. By enabling selected private players to collaborate with global original equipment manufacturers, the policy introduces competitive intensity into a segment historically characterised by the dominance of public-sector yards. Over time, this could broaden participation in high-value shipbuilding programmes and gradually reshape the competitive landscape of Indian naval construction.

Commodity Dependence and Cyclicality

Shipbuilding's cost structure creates inherent margin vulnerability. For MDL's construction programmes, labour costs account for 10 to 15 % of total vessel cost, while equipment and material costs (including a significant share of imported components) constitute 50 to 55 %. MDL's filing notes that 65 to 70 % of critical equipment is imported, making the company exposed to both currency depreciation and global supply chain disruptions. This import intensity is not unique to MDL: the weak ancillary industrial ecosystem in India, flagged by both MDL and GRSE as a competitive constraint, means that domestic shipbuilders cannot fully substitute imported components at scale, limiting their ability to compete on cost with Chinese, Korean, and Japanese yards.

For the shipping companies in the coverage, cyclicality operates through freight rates rather than input costs: earnings can be volatile, asset values fluctuate significantly, and the same company may be highly profitable one year and barely breakeven the next depending on supply-demand balance. Great Eastern Shipping's own FY25 consolidated net profit declined to ₹2,344 crore from ₹2,614 crore the prior year, reflecting the softening in tanker and dry bulk rates described above. The company's gross debt-to-equity ratio improved from 0.22 to 0.12 over the year, reflecting a deliberate strategy of buying vessels cheap and deleveraging when markets are strong.

Dredging, while less exposed to freight volatility, faces a different form of cyclicality tied to government capital expenditure. DCI's entire revenue base is dependent on port modernisation and inland waterway development contracts, creating concentration risk. In FY2024-25, DCI reported total income of ₹1,148 crore and an operating margin of 12.33 %, a sharp deterioration from 21.34 % in FY24, and swung to a net loss of ₹27.46 crore versus a profit of ₹31.85 crore the prior year. Procurement of a new dredger added debt, long lead times in spare procurement caused operational delays, and a skilled workforce shortage further hampered execution.

In sharp contrast, agile private players like KMEW have insulated themselves from these massive capital execution risks by targeting specialized river dredging and long-tenor green tug chartering, allowing them to maintain robust 40%+ EBITDA margins.

Long-Term Tailwinds

The sector carries structural tailwinds that extend well beyond a single investment cycle. Three are particularly durable. First, India's defence ambition is non-negotiable and growing: the naval modernisation pipeline has multi-decade visibility, and indigenisation targets under Make in India create a captive demand base for domestic yards that is largely insulated from commercial shipping cycles. Second, global fleet renewal is mandatory rather than discretionary; regulatory timelines for IMO compliance cannot be deferred, and every year that passes makes the replacement cycle more compressed. Third, India's geographic position along the main east-west shipping corridor creates a natural advantage for ship repair and maintenance that has barely been monetised. The infrastructure investment now underway (new dry docks, ship lift facilities, repair clusters) will take years to show returns, but the direction of travel is clear.

Against these tailwinds, two structural constraints limit how quickly the sector realises its potential. The underdeveloped ancillary supply chain means that domestic shipbuilders remain heavily import-dependent for critical components, capping margin improvement and production ramp. And the concentration of naval orders in two public sector yards (CSL, MDL and GRSE) leaves private players with limited access to high-value platforms, even as the Strategic Partnership Model seeks to change this.

The Forward Voyage: Sector Outlook

Across the companies examined, three distinct industrial logics are operating in parallel. For the defence shipbuilders, the investment case rests on a multi-decade government programme, near-captive demand, and improving indigenisation; conditions that generate durable margin profiles with limited cyclical exposure. For the commercial operators, the earnings trajectory is governed by freight markets that softened materially in FY25 across tankers, dry bulk, and offshore services, compressing returns even for well-run balance sheets. These are not the same business dressed in similar nomenclature; they carry different risk profiles, different capital allocation frameworks, and different sensitivity to policy changes. And for the maritime enablers, value is created by capturing niche infrastructure monopolies.

What unites them is the structural underinvestment in India's maritime supply chain — the weak ancillary ecosystem, the below-1 % ship repair market share, the import dependency for critical components — which caps how quickly even the best-positioned yards can scale. The policy intent to close this gap is credible and increasingly backed by capital. Whether the execution matches the ambition over the coming decade is the operative question for anyone assessing this sector with a long horizon.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.