India's water and wastewater treatment sector occupies a structurally privileged position among infrastructure verticals. It is driven by chronic sanitation deficits, rapid urbanisation, and a sustained escalation in government spending. What distinguishes this sector from others is the near-complete absence of private-sector demand substitution; revenue flows almost entirely from Central and State government disbursements, making policy continuity the single most consequential variable for investors. Order books are swelling to extreme multiples of their revenue base, execution timelines remain tight, and margin structures are broadly stable, with the strongest players generating return ratios well above the cost of capital even in a high-receivable, long-cycle business.

Market Size and Industry Structure

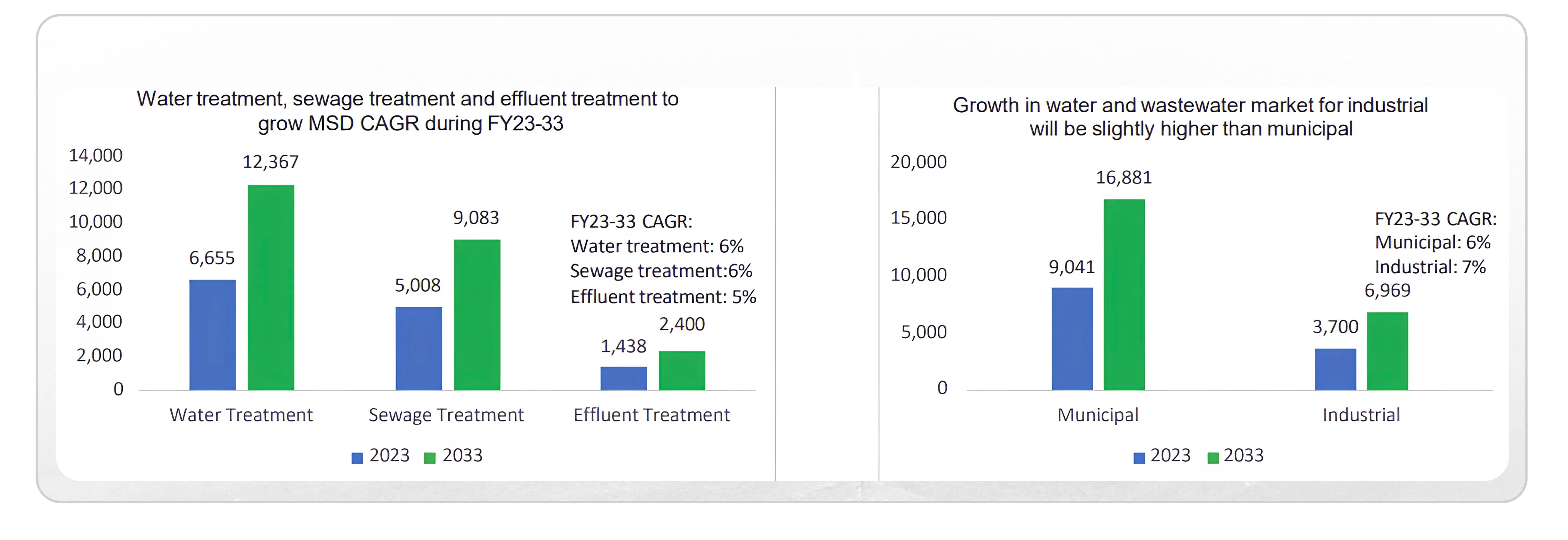

The specialized wastewater segment, currently valued at an estimated ₹96,000 crore is projected to reach ₹1.66 lakh crore by FY2028-29, expanding at a CAGR of 11.60%. This trajectory is backstopped by multi-year government programme commitments that have already been funded and partially disbursed.

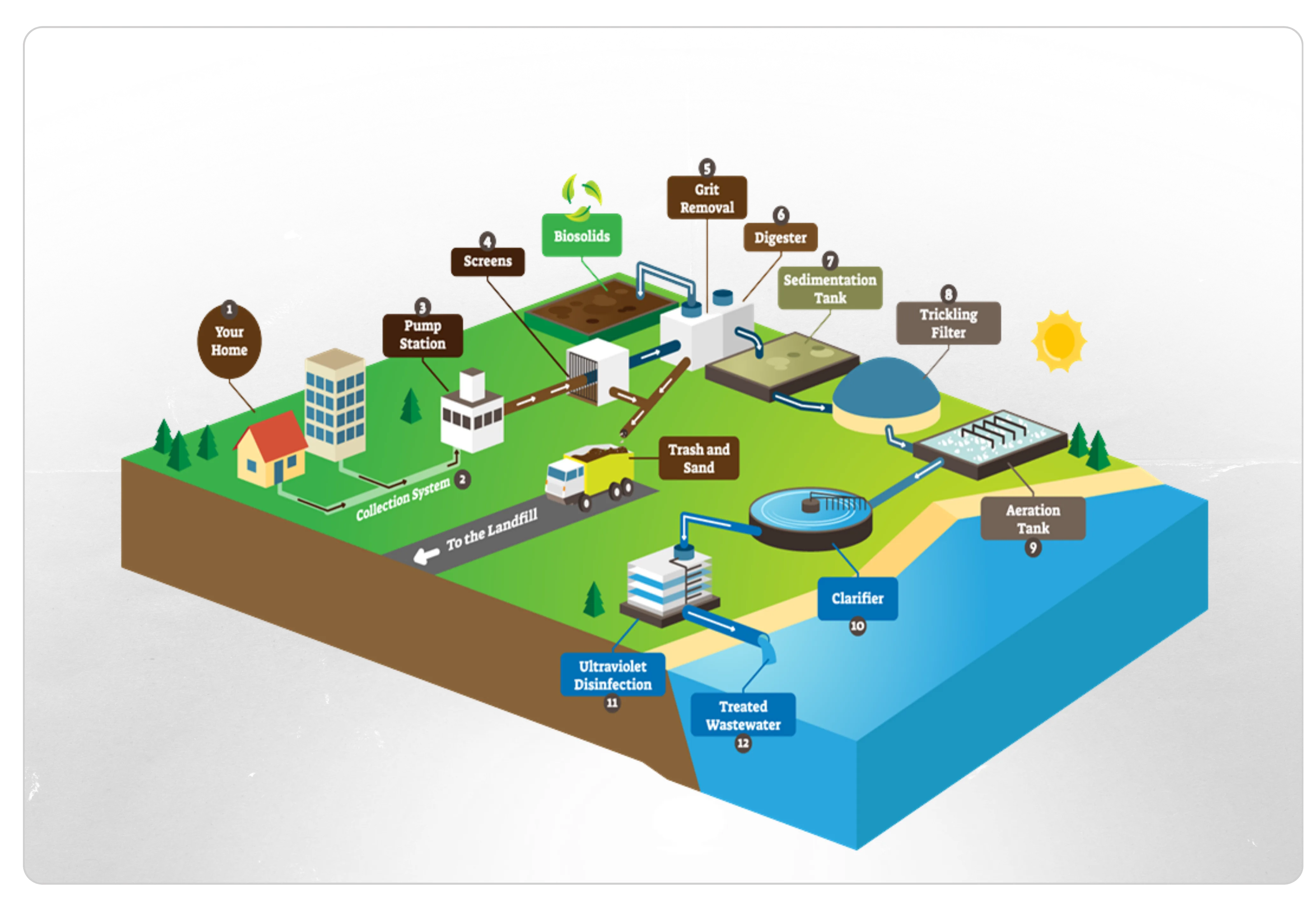

The sector encompasses two broad segments: potable water supply infrastructure (treatment, transmission, storage, and distribution) and municipal wastewater management (sewage collection, conveyance, pumping, and treatment). A third and growing segment includes industrial and river treatment, anchored by programmes like Namami Gange.

Within these, the industry operates through Engineering, Procurement, and Construction (EPC) contracts and post-construction Operation and Maintenance (O&M) agreements. O&M contracts are emerging as a key differentiator, providing stable, long-duration revenue streams with relatively lower working capital intensity compared to EPC execution.

Demand Drivers and Structural Tailwinds

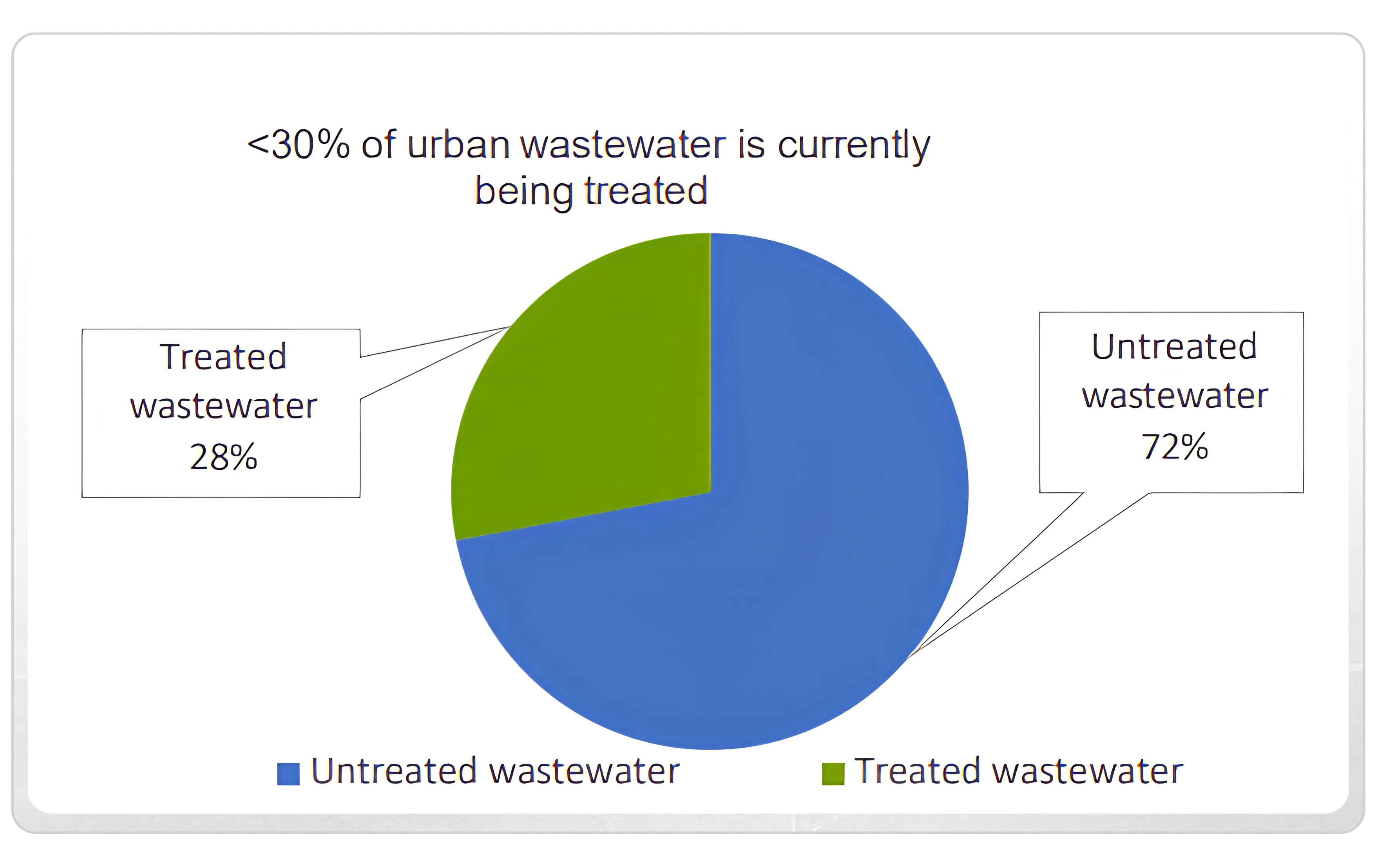

Urbanisation and Wastewater Generation Urban India generates wastewater at roughly double the per-capita rate of rural India, a direct consequence of higher water consumption and greater household connectivity. As migration continues to press population density into tier-1 and tier-2 cities, the aggregate volume of untreated sewage entering water bodies is increasing even as treatment capacity struggles to keep pace. This gap is structural and self-reinforcing. Inadequately treated sewage degrades source water quality, which in turn raises the treatment burden on potable water systems, creating compounding demand across both segments of the sector.

Rural Water Access The Jal Jeevan Mission (JJM), India's most ambitious rural drinking water programme, has achieved tap connectivity to more than 80% of rural households as of 2025. While this represents a landmark achievement in access, it has also generated a massive secondary wave of demand: infrastructure built must be operated, maintained, and eventually upgraded. Sewage treatment in rural clusters (presently far below urban standards) is now emerging as a budget priority in its own right.

Industrial Effluent Requirements Regulatory tightening around industrial discharge standards has created a growing demand for effluent treatment plants, particularly in pharmaceutical, textiles, chemicals, and food processing clusters. This demand is less cyclical than municipal spending, as it is compliance-driven rather than discretionary, and thus less susceptible to state budget compression.

There is an emerging opportunity in resource recovery from wastewater: biogas from anaerobic digestion, phosphorus for agricultural application, and treated water for industrial reuse. Though nascent, this segment is beginning to appear in project briefs, particularly in the context of circular economy mandates and rising water scarcity pressures.

Competitive Landscape

The wastewater treatment sector in India is structured as a specialist oligopoly. A small number of EPC and technology players with demonstrated execution capability, established government relationships, and the balance sheet strength to support long working capital cycles dominate project awards. Prequalification requirements in government tenders specify prior project completion credentials, minimum net worth thresholds, and joint venture arrangements for large-scale contracts, raising the bar considerably for new entrants.

VA Tech Wabag is India's largest pure-play water company by revenue and its most internationally diversified. Having executed over 6,500 municipal and industrial projects across 25 countries, it has developed a level of technical capability that domestic-focused competitors are unlikely to match in the near term. Its solution portfolio covers the full water lifecycle, drinking water treatment, industrial and process water, desalination, biological and membrane-based wastewater treatment, sludge management, and water recycling.

Revenue visibility is a notable strength. The company carries an order book of ₹16,300 Crore, approximately three times its current annual execution rate, providing a reasonable degree of forward earnings coverage. The 400 MLD desalination plant in Chennai is a relevant reference point; it reflects the company's ability to deliver at a project scale that most domestic competitors are not currently positioned to bid for.

Ion Exchange (India) is the only major listed company in the sector that combines water treatment chemicals, Ion exchange resins, engineered systems, and consumer water purification within a single business. Established in 1964, it is among the oldest water management companies in India and has completed over 100,000 installations worldwide.

The engineering segment covers end-to-end project delivery across zero liquid discharge systems, effluent and sewage treatment, desalination, and process water applications. An active bid pipeline of ₹9,556 Crore in the engineering segment indicates a reasonable pipeline of potential work heading into FY27.

EMS Limited EMS Limited has recorded the strongest revenue growth in this group

It delivers end-to-end water and wastewater projects, spanning construction, operations and maintenance, and in-house manufacturing of treatment components, with its client base concentrated in municipal and state government bodies. The business currently has no significant private sector or international presence.

Its unexecuted order book of ₹2,236 Crore represents approximately 2.3 times its annual revenue, which provides a measurable degree of near-term earnings predictability independent of new order inflows.

Enviro Infra Engineers Limited (EIEL) is a Delhi-based company engaged in designing, constructing, and operating water and wastewater treatment infrastructure for government clients. Its project portfolio covers sewage treatment plants, common effluent treatment plants, and water supply schemes, with work aligned to central government programmes such as AMRUT, Jal Jeevan Mission, and Namami Gange.

The company operates through EPC and Hybrid Annuity Model contracts and has completed 28 water and wastewater projects across seven states over the past seven years. Its current order book stands at approximately ₹1,960 Crore in EPC contracts and over ₹750 Crore in operations and maintenance work, representing a reasonable pipeline of executable revenue.

The business is concentrated entirely in the domestic government segment, with no private sector or international presence. This limits diversification but provides a degree of revenue predictability, as projects are funded through central and state government allocations. Management has guided for EBITDA margins of around 25% and a revenue growth rate of 35–40% over the next four to five years, supported by in-house design capabilities and an expanding project eligibility threshold.

SPML Infra is the oldest water infrastructure company in this peer group, incorporated in 1981 and historically one of the largest players in civic water supply and sewage treatment. The company continues to secure significant JJM-linked awards, reflecting the market’s recovery expectations associated with a larger legacy player accessing incoming state fund-lines.

Comparative Peer Financial Snapshot

(Values in ₹ Cr)

| Company | TTM Revenue (Dec, 2025) | EBITDA Margin (%) | Trailing PE | Market Cap | Order Book / Pipeline |

|---|---|---|---|---|---|

| VA Tech Wabag | 3,686 | 12% | 27 | 9,297 | 16,300 |

| Ion Exchange | 2,886 | 10.74% | 30 | 5,847 | 9,556 |

| EMS Limited | 883 | 21% | 15.9 | 2,083 | 2,236 |

| SPML Infra | 765 | 7% | 28.5 | 1,695 | N/A |

| Jash Engineering | 746 | 11% | 45.2 | 2,511 | 923 |

| Enviro Infra Engineers | 1,111 | 27% | 17.2 | 3,617 | 2,732 |

Wabag and Ion Exchange command significantly higher market capitalisations and richer valuations, justified by their technology differentiation, international presence, order book scale, and (in Ion Exchange's case) the recurring chemicals business. EMS stands out on margin quality; its EBITDA margin is structurally superior to every peer. The divergence in EBITDA margins (from 21% at EMS down to 7% at SPML) underscores how meaningfully execution quality, project mix, attached O&M clauses, and contract selectivity determine profitability within a sector where everyone is broadly working for the same government clients.

Also Read: Sector Analysis of the Indian Automotive Component Industry

Supply Chain: Pump, Valve and Equipment Manufacturers

Water and wastewater treatment infrastructure depends on an extensive supply chain of pumps, motors, membranes, aerators, and electrical systems. Among these, pumps are the most capital-intensive and service-intensive component, making pump manufacturers relevant ancillary participants in the sector's growth.

India's pumps market was valued at approximately ₹38,050 crore in FY25 and is projected to reach ₹59,190 crore by FY30, at a CAGR of 9.2%. The submersible pump segment (critical for sewage lifting stations and rural water supply) was valued at ₹11,300 crore in FY2023-24 and is expected to reach ₹19,600 crore by FY2028-29 at a CAGR of 11.7%.

Positive displacement (PD) pumps, manufactured by companies such as Roto Pumps, serve wastewater treatment in the chemicals, sludge handling, and biogas applications segments. Roto Pumps reported revenue of ₹240.37 crore in FY25, with exports accounting for 60.3% of turnover, reflecting the strong global demand for Indian pump manufacturing.

Specialized mechanical equipment providers such as Jash Engineering supply the mission-critical water control gates and mechanical screening arrays required at treatment facilities. Functioning as a high-margin structural supplier, Jash holds a commanding combined order book of ₹923 Crore (as of Q3FY26), deriving significant traction from global municipal exports alongside domestic utility modernization.

Commodity Dependence and Cyclicality

Wastewater treatment projects are materials-intensive, drawing on steel, cement, piping, membranes, and mechanical equipment. Raw material cost volatility (particularly in structural steel and copper) directly affects bid pricing and execution-phase margins. Companies that engage in backward integration or long-term supply agreements carry a structural advantage over those that procure at spot.

The business is not cyclical in the classic industrial sense; demand does not compress with the economic cycle since it is predominantly government-funded and non-discretionary. However, it exhibits a distinct policy cyclicality: order inflows cluster around budget announcements and programme launches, followed by execution lags driven by land acquisition, environmental clearances, and state-level administrative friction. This pattern produces episodic working capital pressure even in years of strong revenue growth.

The most consequential financial characteristic of the sector is the length of the receivable cycle. Any investor analysis of this sector must treat receivable quality, not merely revenue growth, as the primary financial risk variable.

| Metric | VA Tech Wabag | Ion Exchange | EMS Limited | SPML Infra | Jash Engineering | Enviro Infra Engineers |

|---|---|---|---|---|---|---|

| Days Receivable | 223 | 151 | 142 | 187 | 112 | 70 |

Government Policy Impact

No other infrastructure vertical in India is as comprehensively shaped by government programmes as water and wastewater treatment. The following schemes collectively define the demand landscape for sector participants through at least FY2028:

Jal Jeevan Mission (JJM): Funded at INR 67,000 Crore under the Union Budget 2025-26 specifically earmarked for JJM, the mission's current focus has shifted from greenfield connection delivery to quality assurance, sustainability of supply, and grey water management in villages. The Department of Drinking Water and Sanitation received INR 74,226 Crore in total under Budget 2025-26. This is not a single-year allocation, it is part of a structural commitment by the Central government to maintain rural water infrastructure as a priority for the remainder of the decade.

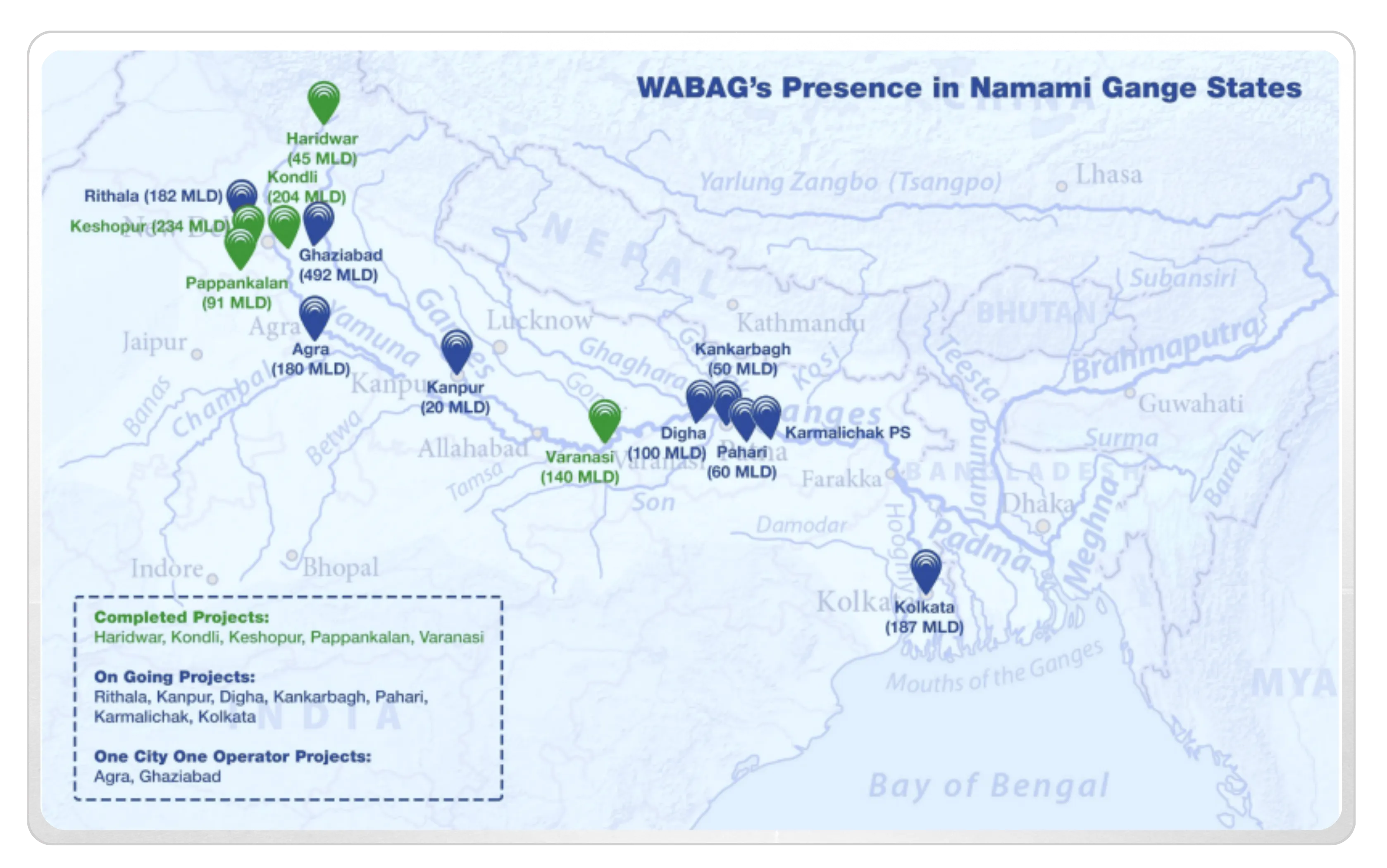

National Mission for Clean Ganga (NMCG): NMCG targets the development of 7,000 million litres per day (MLD) of sewage treatment capacity along the Ganga river system by December 2026. To deliver this, 200 projects have been sanctioned, targeting 6,217 MLD of sewage treatment capacity and the creation of a 5,282 km sewerage network. This programme alone represents a multi-year, multi-thousand-crore procurement pipeline for EPC players with sewage treatment capability.

Pradhan Mantri Krishi Sinchai Yojana (PMKSY): Allocated INR 93,068 Crore between FY2022 and FY2026, with INR 37,454 Crore in Central government support, PMKSY addresses irrigation infrastructure an adjacent segment that overlaps with water treatment through canal lining, distribution system upgrades, and micro-irrigation mandates.

AMRUT 2.0 and Swachh Bharat Mission (Urban): Atal Mission for Rejuvenation and Urban Transformation (AMRUT) 2.0 specifically targets water supply and sewage networks in urban local bodies. Combined with Swachh Bharat Mission (Urban), these programmes ensure that municipal wastewater treatment capacity addition remains a funded commitment across hundreds of cities simultaneously, not merely in large metros.

The collective implication is significant: India has assembled an interlocking grid of Central programmes that ensure demand for water and wastewater infrastructure will not be entirely a function of short-term state budget cycles. Most programmes carry multi-year fund commitments, creating forward visibility for companies. Welspun Corp, serving as an infrastructural proxy for macro pipeline transport, explicitly benefits from these interlocking commitments, recently highlighting a colossal bulk pipeline order book of ₹INR 23,600 Crore.

India Growth Outlook

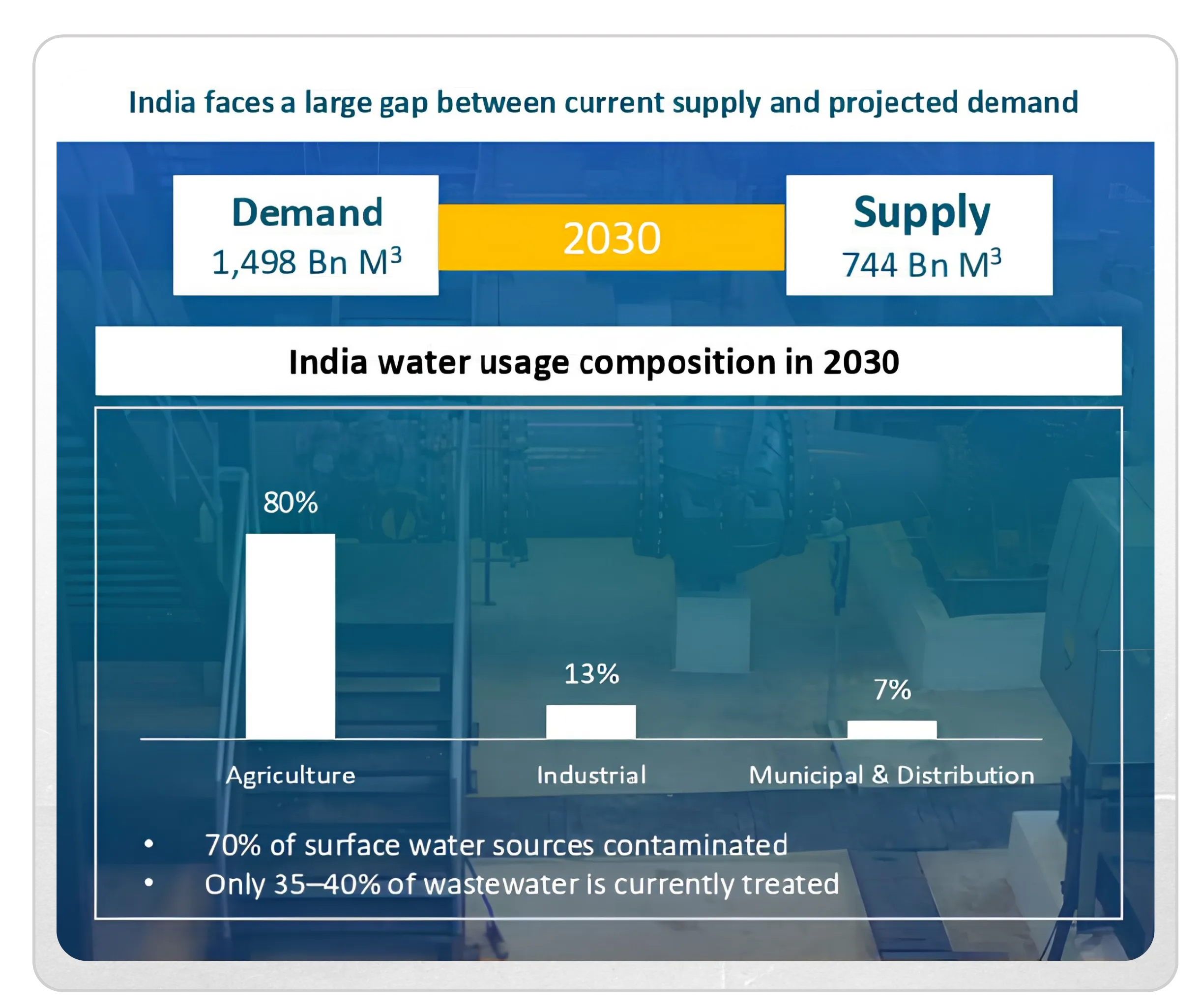

India's water supply and sanitation industry is characterised by one defining structural feature: supply has historically lagged demand by a wide margin. As of 2025, the country remains significantly underpenetrated in sewage treatment capacity relative to its wastewater generation volumes, particularly outside the top 20 cities. This gap is the fundamental growth driver. Unlike sectors where demand is created by aspiration or income growth, demand in wastewater treatment exists at scale already, it is merely a question of how rapidly the government can fund and deploy the infrastructure to address it.

The sector's CAGR of 11.60% through FY2028-29, is consistent with the aggregate capital expenditure commitments visible in Union and state budgets. There is limited scenario under which this growth would materially decelerate unless fiscal conditions force a broad infrastructure freeze, a low-probability outcome given water's status as an essential public health expenditure.

Also Read: Strategic Outlook of The Indian Tea and Coffee Sector

Geographical Dynamics

Demand for wastewater treatment infrastructure is geographically concentrated in states with large urban agglomerations and active programme participation. The Namami Gange programme anchors activity in the Gangetic belt (Uttar Pradesh, Bihar, West Bengal, and Uttarakhand) while AMRUT 2.0 distributes work across urban local bodies nationally. Maharashtra has emerged as a dominant market, particularly through its own schemes such as the Magel Tyala Saur Krushi Pump Yojana and state-specific infrastructure pipelines.

The customer base is entirely in the public sector, with projects concentrated in municipal sewage and potable water segments. The concentration risk is partially mitigated by the diversity of Central programmes and state-level counterparts, which means no single government client dominates the revenue mix even within a broadly B2G model.

Key Risks

Policy and Programme Continuity: The sector's revenue is almost entirely contingent on government programme persistence. Central scheme extensions beyond their original sunset dates (as seen with JJM) are historically common, but periods of policy uncertainty can cause tender moratoriums and order award delays. Companies with diversified programme exposure are better insulated than those concentrated in a single scheme.

Receivable Cycle and Liquidity: Government clients are slow payers in the Indian infrastructure context. Project completion retentions can be held for extended periods, and disputes over variation claims are common. This creates structural working capital pressure that even profitable companies must actively manage.

Raw Material Price Volatility: Steel and copper price fluctuations directly affect EPC margins. Contract structures typically do not include price escalation clauses for short-duration contracts, exposing companies to cost overruns when commodities spike between bid submission and execution.

Execution and Skilled Labour Risk: Water and wastewater plants require technical specialisation in civil works, mechanical assembly, and process commissioning. Attrition in specialised workforce and subcontractor availability in specific geographies can introduce execution delays that trigger liquidated damages under government contracts.

Competition and Bid Pricing: As large Central programmes scale, competition for project awards intensifies. Aggressive bidding by financially weaker players can erode market pricing, compressing margins for disciplined competitors even when they win contracts.

Long-Term Tailwind Assessment

The long-term tailwind case for India's wastewater treatment sector is among the strongest in the infrastructure universe, resting on three independent and durable pillars:

The sheer scale of the unmet need. India's urban sewage treatment capacity remains severely inadequate relative to wastewater generation volumes. Even with years of programme-driven capacity addition, the gap is wide enough to sustain double-digit sector growth through the remainder of this decade without relying on incremental policy support.

The institutional permanence of government commitment. Water and sanitation have been elevated from programme-level priorities to constitutional and geopolitical commitments, connected to SDG rankings, diplomatic signalling, and domestic political outcomes. The probability that Central government spending on this sector reverts to pre-JJM levels is low, regardless of which political formation governs at the Centre.

The O&M revenue tail. Every wastewater treatment plant commissioned today becomes a long-duration O&M revenue source for companies with the operating capability to service it. As installed capacity grows, the O&M segment (currently ancillary for most players) will transition into a material and recurring revenue line with more predictable cash flow characteristics than construction.

The primary risk to this thesis is not demand but execution: whether India's EPC ecosystem can develop the manpower, financial depth, and technology capability to absorb the scale of orders that government programmes are designed to release. Companies that resolve this constraint (through workforce development, technology partnerships, and selective tendering) are positioned to compound revenue and return ratios simultaneously across what appears to be a structurally advantaged multi-year cycle.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.