India’s food delivery space has seen a notable new entrant, and it comes from a player outside the usual duopoly. Rapido, best known for its bike taxi services, has launched ‘Ownly,’ a fixed-fee food delivery platform. The move directly positions Rapido against Swiggy, one of its investors, is adding a new layer of complexity to the competitive landscape.

Read also: FristCry a Consolidation Play in India’s Childcare Sector

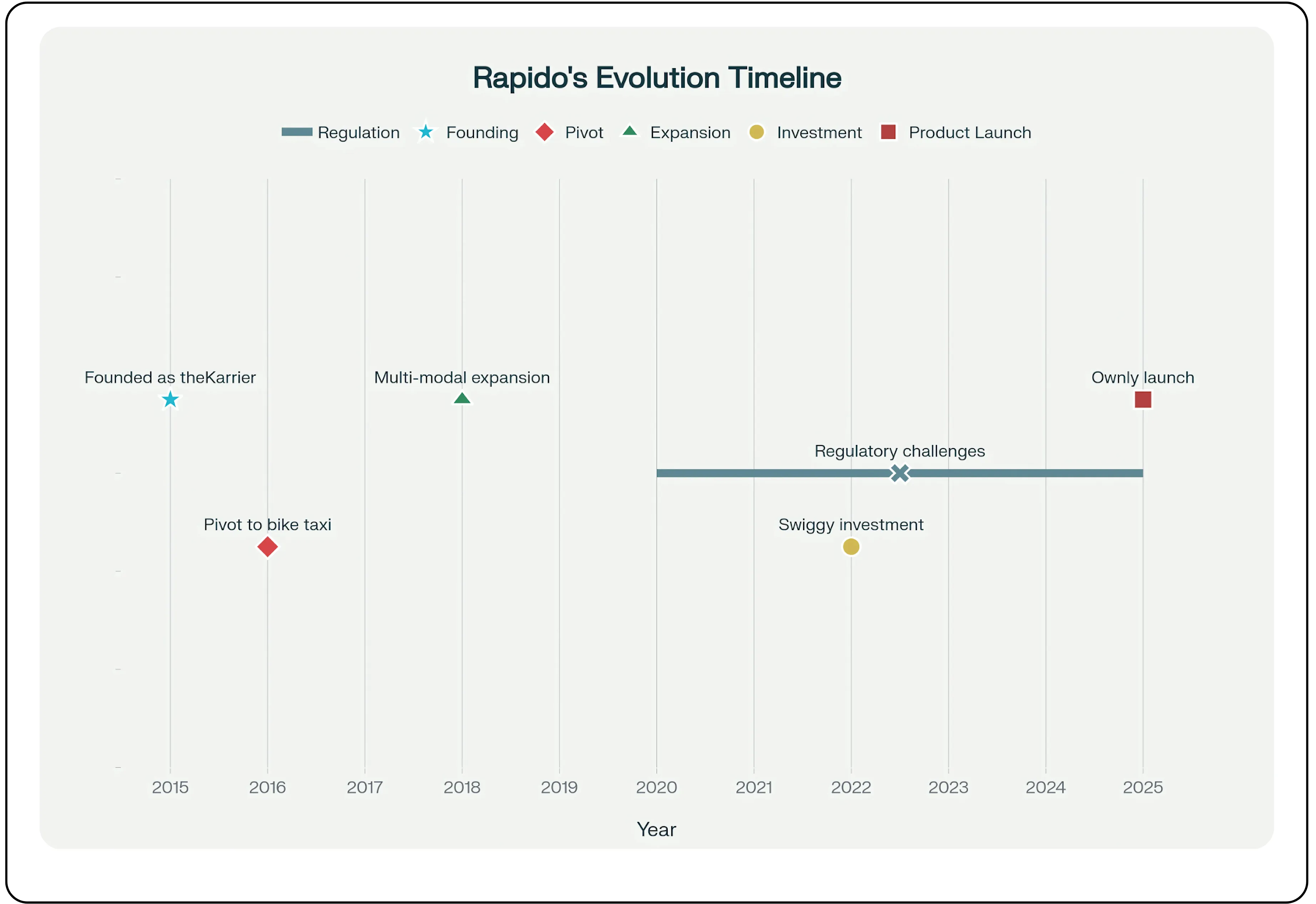

From bike taxis to a multi-service platform

Founded in 2015 by Aravind Sanka, Pavan Guntupalli, and Rishikesh SR, Rapido initially started as a B2B logistics provider under the name theKarrier. It pivoted to bike taxis after identifying that two-wheelers, which account for about 75% of vehicles in India, were an underutilized asset for urban mobility.

The company grew by prioritizing driver acquisition and predictable earnings rather than deep consumer discounts. This approach helped Rapido expand to over 100 cities, with 1.5 million drivers and 25 million customers.

Over time, regulatory challenges emerged, with some states imposing restrictions on bike taxi operations without commercial permits. Rapido responded by diversifying into autos, cabs, parcel delivery, and logistics while keeping its focus on transparent and predictable partner incentives.

Swiggy’s strategic investment

The strategic investment in Rapido in April 2022 saw the food giant, Swiggy acquire a 12–15% stake at an $830 million valuation as part of a $180 million funding round. The partnership aimed to improve fleet utilization for Swiggy during off-peak hours while giving Rapido additional demand from Swiggy’s food, grocery (Instamart), and courier (Genie) services.

The collaboration was intended to build shared logistics capabilities and enhance earning potential for delivery partners across both platforms.

Launch of Ownly

In June 2025, Rapido announced its plan to enter the food delivery market. By August 2025, the Ownly food delivery service was rolled out, making it the newest food delivery app in Bengaluru. The platform’s key differentiator is its fixed-fee food delivery model, a sharp contrast to competitors.

No commissions for restaurants

Transparent customer delivery fees, ₹25 for orders under ₹400, ₹50 for orders above

No platform fees, price markups, or hidden charges.

Restaurants retain control over menu pricing and get access to customer data for direct engagement. This reduces their effective cost to around 8–15%, compared to 20–30% on Swiggy and Zomato.

Rapido’s operational strength comes from its 4 million rider network, significantly larger than Swiggy’s 530,000 and Zomato’s 440,000. Years of operating as Swiggy’s logistics partner also give it insight into delivery operations.

Swiggy’s response and stake sale

In July 2025, Swiggy publicly acknowledged a “potential conflict of interest” and began reassessing its investment. This conflict answers the question of why Swiggy is selling its Rapido stake, with reports indicating an intent to divest for ₹2,500 crore (roughly $300 million) - a 2.5x return on its original investment. This would value Rapido between $2.2 - $2.5 billion.

Parallely, Swiggy is reinforcing its competitive position through in-house delivery network expansion and affordability initiatives such as Instamart (10 mins quick commerce service), 99-store (₹99 meals), and SNACC ( Standalone quick service food delivery app). Notably, Bolt and SNACC now account for 12% of Swiggy’s order volumes across major cities.

| Aspect | Incumbents (Swiggy/Zomato) | Rapido (Ownly) |

|---|---|---|

| Restaurant Commission | 20–30% per order (+ ads, promos) | Zero commission; Fixed fee (₹25 / <₹400, ₹50 / ≥₹400) |

| Menu Pricing | Often marked up above dine-in rates | Same as dine-in price |

| Platform Fee (Consumer) | Typically ₹2–10 / order | None |

| Restaurant Data Access | Restricted; platform owns customer data | Shared with restaurants (for remarketing) |

| Delivery Partner Pay | Per-order fixed plus incentive (platform sets payout) |

Flexible per order; supply cross-utilized from multi-modal ops |

| Transparency | Platform, delivery, menu fees all additive | Transparent; fixed fee visible upfront |

| Primary Model Incentive | Incentivizes platform; variable/opaque cost to partners |

Predictability for restaurant/consumer; aligned supply incentives |

| Restaurant Onboarding | Digital, but requires margin flexibility | Focused, with promise of fixed cost |

A comparative breakdown of business models : Incumbents vs Rapido (Ownly)

Implications

Rapido’s entry tests the viability of fixed-fee, commission-light models in a market dominated by commission-heavy players. The economies are attractive- especially with high supply density and idle-hour utilization - but scalability will rely on maintaining service quality and managing operational complexity

If Ownly succeeds in its pilot markets, the competitive pressure may force Swiggy and Zomato to revise their take-rate structures. Conversely, limited adoption could confine Ownly to niche status, preserving the existing comfortable duopoly

This development underscores the risks inherent in strategic cross-investments. What began as a logistics partnership evolved into direct competition, compelling Swiggy to weigh short-term investment gains against long-term strategic control.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.