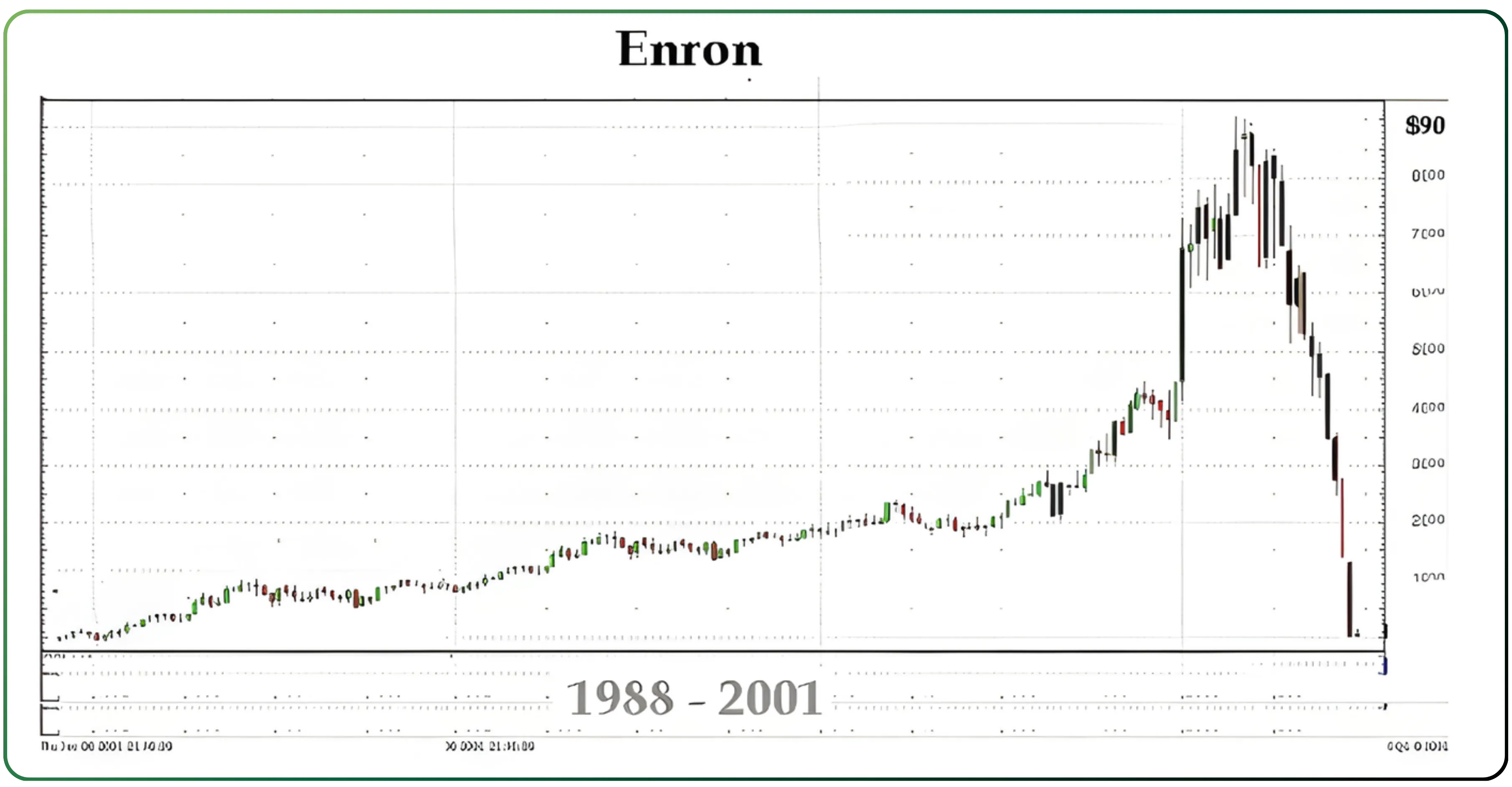

In the closing years of the twentieth century, Enron Corporation stood as a symbol of modern capitalism. It was admired for its innovation, trusted by investors, and praised for redefining how markets could function. When it collapsed, the failure was not merely corporate. It marked a reckoning with an era that had confused complexity with intelligence and confidence with truth.

The Conditions That Made the Fraud Possible (early 1990s)

The early 1990s were defined by faith. Inflation had receded, globalisation was accelerating, and free markets were no longer debated but assumed. In the United States, deregulation was treated not as policy, but as principle. Markets, it was believed, possessed an internal discipline stronger than oversight.

This belief reshaped corporate behaviour. Innovation was rewarded reflexively. Complexity inspired admiration rather than suspicion. If a business appeared difficult to understand, the fault was assumed to lie with the observer.

Accounting, too, began to evolve in this environment. Estimates, models, and projections gained legitimacy. The boundary between what had happened and what was expected to happen grew less rigid. This was not yet fraud. It was a shift in temperament.

It was within these conditions that Enron would rise.

How Enron Learned to Manufacture Earnings (1985–1996)

Enron was formed in 1985, through the merger of Houston Natural Gas and InterNorth. For several years, it remained a conventional pipeline company, earning stable but unremarkable returns from regulated energy transport.

The turning point came with energy deregulation in the late 1980s and early 1990s. Natural gas prices were freed. Electricity markets began to open. Volatility entered a sector that had once been predictable.

Enron saw opportunity where others saw uncertainty. Rather than owning assets, it would trade contracts. It would connect buyers and sellers, manage price risk, and earn margins from market activity. Energy, the company argued, could be traded like oil, currencies, or interest rates.

This shift accelerated after 1996, when Jeffrey Skilling became chief executive. Skilling believed Enron was not an energy company at all, but a markets company. Physical assets, in his view, were constraints. Financial engineering was liberation.

To support this model, Enron adopted the mark-to-market accounting method on a wide scale. Long-term contracts, sometimes spanning twenty years, were valued immediately based on projected future profits. Those projected profits were then booked as earnings the moment the deal was signed.

A contract no longer needed to succeed. It only needed to be signed.

To investors, earnings appeared strong and consistent. What they did not see was that cash often lagged far behind reported profit. Enron’s success increasingly depended on assumptions holding true for decades into the future.

For a historical parallel, explore Tulip Mania and the Birth of Financial Bubbles, the first recorded episode of market-wide speculation.

The Earnings Targets That Could Not Be Missed (1997–1999)

By the late 1990s, Enron’s identity was bound to its share price. Analysts expected steady earnings growth every quarter. Executives were compensated largely through stock and options. The market’s belief in Enron’s model had become essential to its survival.

This created a structural problem. If projected profits failed to materialise, earnings would fall. If earnings fell, the share price would weaken. And if the share price weakened, confidence in the entire model would begin to crack.

Internally, the pressure to meet expectations was relentless. Assumptions used in mark-to-market valuations were adjusted to preserve earnings continuity. Deals were structured not for long-term cash generation, but for immediate accounting impact.

Enron did not report volatility. It reported certainty. Enron’s financial reporting increasingly reflected projected outcomes rather than realised cash flows.

At this stage, the deception was subtle. Numbers were not invented. They were engineered. The future was brought forward and treated as fact.

Who Controlled the Machinery (1999)

The shift from aggressive accounting to outright fraud occurred around 1999, when Enron began using special purpose entities at scale.

In theory, these entities existed to manage risk. Losses from volatile investments could be transferred to independent outside partnerships, protecting Enron’s balance sheet. This was common practice, provided the entities were genuinely independent.

They were not.

Under the direction of CFO Andrew Fastow, Enron created partnerships such as LJM. Fastow himself controlled these entities while remaining Enron’s chief financial officer. This was a direct conflict of interest, concealed from investors. The arrangement represented a fundamental breakdown in corporate governance, bypassing internal controls that should have been overseen by the audit committee.

Enron would transfer underperforming assets to these partnerships at favourable prices. On paper, the sale generated profit. In reality, Enron still bore the risk. The partnerships were capitalised largely with Enron stock or guarantees tied to Enron’s share price.

Losses did not disappear. They were hidden.

Investors were told Enron had reduced risk. In truth, it had concentrated it.

How the Losses Were Hidden (1999–2001)

Between 1999 and 2001, Enron relied increasingly on these structures to maintain the appearance of financial strength.

As investments failed to perform, they were moved off Enron’s balance sheet. Earnings were preserved. Debt remained out of sight. The company appeared profitable even as cash flow deteriorated.

The critical weakness was circularity. The partnerships that absorbed Enron’s losses depended on Enron’s own stock as collateral. As long as the share price rose, the system held. If the share price fell, the guarantees would collapse.

This was not risk management. It was delay.

Auditors, including Arthur Andersen, approved the structures. Analysts accepted management explanations. The complexity itself discouraged scrutiny. Understanding Enron required faith, and faith was abundant.

What investors saw was a company that claimed to have solved volatility. What existed was a company postponing recognition of failure. In retrospect, these structures would become central to how the Enron scandal was later classified among the most significant accounting scandals in modern markets.

To understand how disciplined ownership differs from speculative excess, read The Philip Fisher Approach to Owning Stocks Like a Business Owner.

The Trigger That Broke the Illusion (2000–2001)

The collapse of the dot-com bubble in 2000 did not cause Enron’s fraud, but it transformed the environment in which that fraud could persist.

During the late 1990s, markets rewarded narrative. After the technology crash, they demanded evidence. Cash flow regained importance. Balance sheets were examined more closely. Confidence alone was no longer sufficient.

Enron’s weaknesses had been present for years. But once scepticism returned to markets, tolerance vanished.

By mid-2001, Enron’s share price began to decline. That decline triggered collateral clauses within the special purpose entities. The partnerships demanded more Enron stock to remain solvent. Enron’s risk, once hidden, rushed back onto its own balance sheet.

The system began to consume itself.

The Largest Corporate Bankruptcy of Its Time (2001)

In October 2001, Enron disclosed significant losses and acknowledged issues related to its off-balance-sheet arrangements. Confidence collapsed rapidly. Credit rating agencies downgraded the company. Trading partners withdrew.

In December 2001, Enron filed for bankruptcy.

At the time, it was the largest corporate bankruptcy in United States history, involving over $60 billion in assets. Tens of thousands of employees lost their jobs. Many saw retirement savings wiped out, having been encouraged to hold Enron stock in pension plans.

There was no dramatic confrontation. The market simply stepped away.

What remained was an empty structure, exposed once belief had withdrawn. Enron’s bankruptcy in December 2001 marked a defining moment in corporate history.

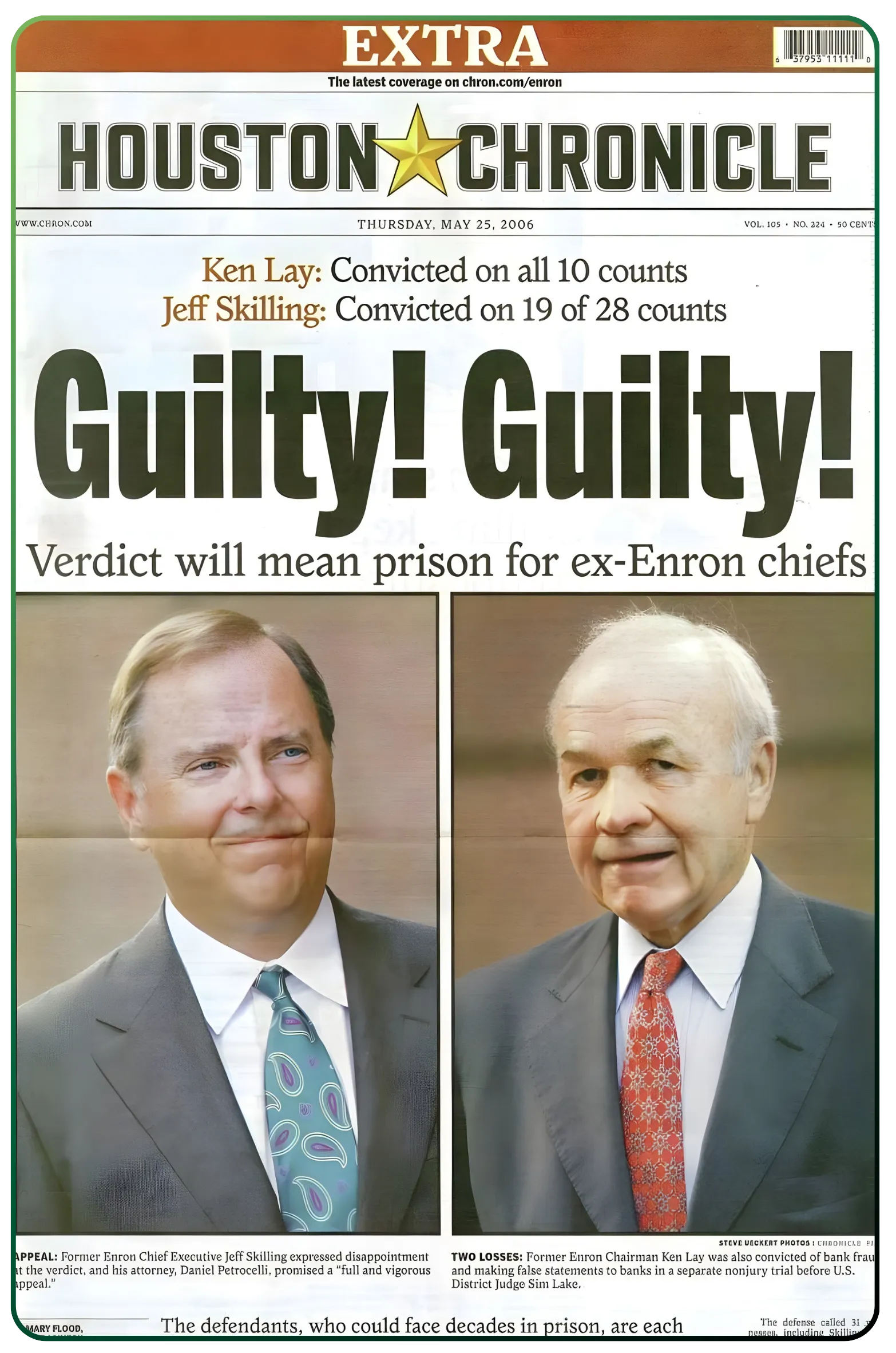

Trials, Consequences, and Market Impact (2002 onward)

The aftermath was severe.

Andrew Fastow was convicted and sentenced to prison. Jeffrey Skilling was convicted on multiple counts related to fraud and conspiracy. Enron’s founder, Kenneth Lay, died before sentencing.

Arthur Andersen, once one of the world’s most respected accounting firms, collapsed after being convicted (and later technically overturned) for obstruction of justice related to Enron’s audits. The firm never recovered.

In 2002, regulatory scrutiny intensified. Corporate reporting standards were tightened. The Sarbanes-Oxley Act reshaped governance, accountability, and audit oversight. The collapse of Arthur Andersen reinforced the consequences of audit failure in large accounting scandals.

Markets did not abandon complexity. They demanded proof.

Closing Perspective

Enron did not invent corporate fraud. It refined a version suited to its time. It exploited an era that trusted intelligence more than evidence, models more than cash, and confidence more than verification.

Its collapse stands as a reminder that markets are not undone by deception alone. They fail when belief is allowed to outrun reality, and when complexity is permitted to substitute for truth.

That lesson, once learned, remains expensive to forget.

Explore CubePlus: Built for investors who focus on businesses, fundamentals, and long-term clarity.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.