A financial fever shaped by biology, contracts, and fear

In the winter of 1637, the Dutch Republic did not descend into madness so much as it revealed how quickly rational markets can lose their footing when scarcity, leverage, and psychology align. The episode remembered as Tulip Mania has long been framed as a morality play about greed and folly. That telling is convenient, but incomplete. What unfolded in the Netherlands was a localized financial crisis born from a peculiar asset, an improvised derivatives market, and a society living under the shadow of disease.

The result was not national ruin. It was something subtler and, in many ways, more instructive. A narrow market overheated, contracts outran reality, and trust dissolved almost overnight.

A flower altered by disease

The tulips that fueled the mania were not ordinary garden varieties. They were so-called broken tulips, flowers marked by dramatic flames and streaks of color that cut through white, yellow, or red petals. These patterns were not the product of careful breeding. They were caused by a virus that interfered with the plant’s pigmentation.

Still Life with Tulips. Found in the collection of Nationalmuseum Stockholm.

Here lay the central biological paradox. The same infection that made a bulb beautiful also weakened it. Infected bulbs propagated slowly and unpredictably. Supply could not be scaled to meet demand. Rarity was not manufactured; it was enforced by nature.

Among these varieties, none captured the imagination more than the Semper Augustus, a white tulip laced with vivid red flames. Contemporary accounts suggest that only a handful of such bulbs existed in the entire country. Ownership conferred status, distinction, and the promise of resale at an even higher price. The Semper Augustus tulip value became the ultimate symbol of the mania, a single bulb representing years of skilled labor and social prestige rather than ornamental worth.

Still Life with Flowers (1639), by Hans Bollongier (1623–1672), showcases the prized Semper Augustus tulip.

In modern terms, the Dutch were trading a non-replicable asset whose supply curve was fixed not by capital investment, but by biology.

Trading what could not yet be delivered

Tulips introduced a second constraint that reshaped the market. Bulbs could only be dug up and moved during the summer months when they lay dormant. For the rest of the year, they remained in the ground, inaccessible to buyers and sellers alike.

The Tulip Folly, by Jean-Léon Gérôme, 1882

Dutch merchants responded with financial ingenuity. They began trading contracts for future delivery. These agreements promised the transfer of a bulb at a fixed price once the growing season allowed it to be lifted from the soil.

This practice came to be known as windhandel [the trade of wind], a market in promises rather than possessions.

Trading rarely occurred at the formal exchange. It migrated instead to taverns, where groups known as colleges met to negotiate prices. Deals were sealed with a symbolic payment called wine money, a small fee meant to toast the agreement. No margin was posted. No collateral changed hands. A trader could commit to paying thousands of guilders months later without holding a single coin at the time of signing.

19th century painting depicting Tulip Mania, by Johannes Hinderikus Egenberger

The structure was elegant and fragile. Prices rose not because cash entered the system, but because confidence did. As long as every buyer believed there would be another buyer willing to pay more, the chain held. This system, known as Windhandel in the Dutch futures market, transformed tulips from physical objects into tradable expectations, exchanged months before any bulb could be delivered.

Related perspective: Speculation magnifies outcomes quickly. Compounding does not. Why the Early Years of Compounding Make Progress Feel Invisible explores why long-term returns build quietly before they become visible.

When price abandoned utility

By the winter of 1636–1637, tulip prices bore no relation to use or enjoyment. They were expressions of expectation.

One surviving bill of sale for a single Viceroy bulb is especially revealing. In exchange for that bulb, the buyer transferred wheat and rye by the cartload, multiple oxen and swine, wine and beer in industrial quantities, butter and cheese by the ton, a silver chalice, clothing, and a fully furnished bed. The total value was roughly 2,500 florins.

At the time, a skilled carpenter earned about 250 florins per year. One bulb equaled a decade of skilled labor.

This was not irrational exuberance in the abstract. It was rational behavior within a system that rewarded early exit and punished hesitation. Futures prices rose because spot delivery was months away and resale opportunities were immediate.

A society shaped by mortality

Any account of Tulip Mania that ignores the wider social context misses a critical driver. In 1636, outbreaks of the Bubonic Plague swept through the Netherlands. Mortality was sudden and seemingly arbitrary. Entire households vanished in weeks.

This environment altered behavior in predictable ways. Fatalism took hold. When tomorrow felt uncertain, the incentive to secure long-term stability weakened. Wages rose as labor became scarce. Inheritances arrived unexpectedly. Disposable income accumulated among artisans and merchants who might otherwise have saved cautiously.

The tavern markets offered both excitement and escape. Speculation became a social activity, conducted in public rooms, reinforced by shared belief and collective optimism.

The silence that ended the market

The collapse did not begin with a scandal or a decree. It began with silence.

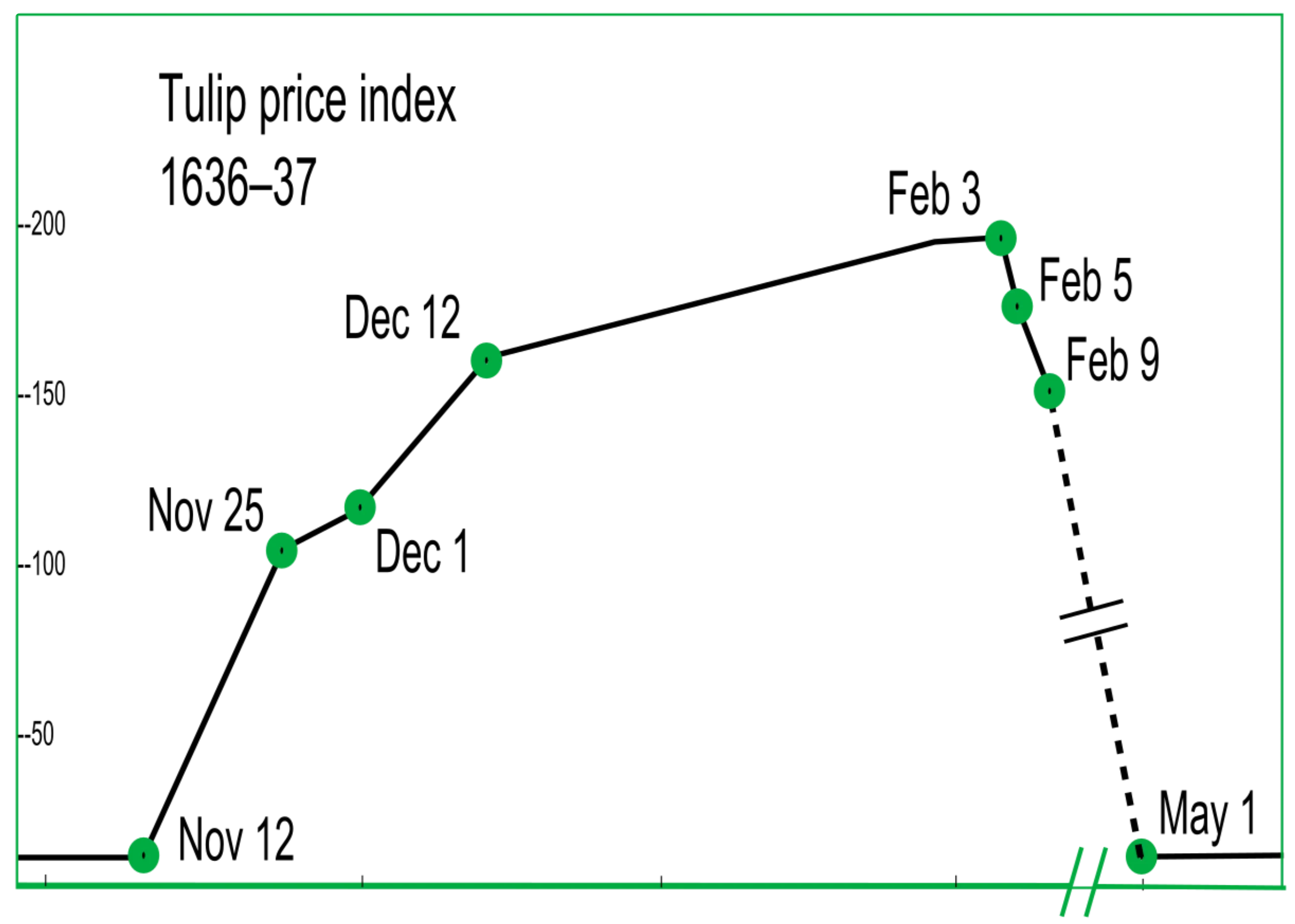

On February 3, 1637, at a routine bulb auction in Haarlem, sellers offered common tulips. No one bid. The failure was small, almost trivial, yet its implication was devastating. If buyers would not step forward for ordinary bulbs, the extravagant prices attached to rare contracts could not be defended.

A standardized price index for tulip bulb contracts, created by Earl Thompson. Thompson had no price data between February 9 and May 1, thus the shape of the decline is unknown. The tulip market is known to have collapsed abruptly in February.

Confidence evaporated in days. News traveled quickly to Amsterdam and Alkmaar. Holders of contracts attempted to enforce payment. Buyers refused, arguing that these agreements were wagers, not binding commercial obligations. The silence at the Haarlem auction marked the beginning of the tulip bulb contract price collapse, as traders realized that paper promises no longer had willing buyers behind them.

What had been a market in expectations became a dispute over definitions.

Related reading: Tulip Mania shows what happens when assets are traded without regard to underlying business value. The Philip Fisher Approach to Owning Stocks Like a Business Owner offers the opposite framework, focusing on ownership, fundamentals, and long-term thinking.

Law, reputation, and limited damage

Authorities faced a dilemma. Enforcing contracts risked bankrupting participants and inflaming unrest. Voiding them entirely threatened the credibility of commerce. The compromise was imperfect. Local councils permitted contracts to be dissolved for a fraction of their face value, often discussed as a small percentage fee. Enforcement varied. Many disputes were settled privately.

Wagon of Fools by Hendrik Gerritsz Pot, 1637. Haarlem weavers chase a wind-borne wagon flying a fool's cap flag. Flora, goddess of flowers, rides aboard to destruction in the sea with the vices Fraud, Gluttony and Avarice, Mrs. Mania, and Idle Hope/Fortuna.

Contrary to popular myth, the Dutch economy did not collapse. Trade continued. Shipyards, textile workshops, and financial houses remained active. Losses were concentrated among a relatively small circle of merchants, growers, and traders.

The most enduring damage was social. Trust fractured. Friendships ended. Reputations suffered. The lesson was absorbed quietly and carried forward.

Separating myth from history

Much of what the world believes about Tulip Mania comes from a later retelling. In 1841, the Scottish writer Charles Mackay published a dramatic account that emphasized ruin, madness, and moral decay. His work shaped popular memory but relied heavily on anecdote and exaggeration.

Modern historians, most notably Anne Goldgar, have reconstructed a more restrained picture. Participation was limited. The poor were largely absent. Bankruptcies directly attributable to tulips were rare. What failed was not the nation, but a specific speculative structure.

Why the episode still matters

Tulip Mania endures not because it destroyed an economy, but because it exposed a recurring pattern. When assets are scarce, when leverage is implicit rather than explicit, and when price depends entirely on the expectation of resale, markets can float free of fundamentals.

A Satire of Tulip Mania by Jan Brueghel the Younger (c. 1640) depicts speculators as brainless monkeys in contemporary upper-class dress. In a commentary on the economic folly, one monkey urinates on the previously valuable plants, others appear in debtor's court and one is carried to the grave.

The plague years intensified speculative bubble psychology, encouraging risk-taking in a society where mortality felt arbitrary and immediate.

The Dutch did not invent irrationality. They revealed how easily sophisticated societies can rationalize risk when the system appears self-sustaining.

The flower at the center of the story was fragile. The contracts built upon it were lighter still. When belief disappeared, value followed it into the air, leaving behind a lesson that remains uncomfortably current.

Explore CubePlus: Built for investors who focus on businesses, fundamentals, and long-term clarity.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.