Most investors begin with a simple expectation: if they invest regularly and stay disciplined, their wealth should grow at a pace they can see. Yet the early years often feel strangely unrewarding. The numbers move slowly, the portfolio barely expands, and progress appears far smaller than the effort behind it. This early phase is not an error in the system; it is the system’s natural starting point of compounding. For most investors, this journey begins through a systematic investment plan, or SIP, where discipline matters long before results become visible.

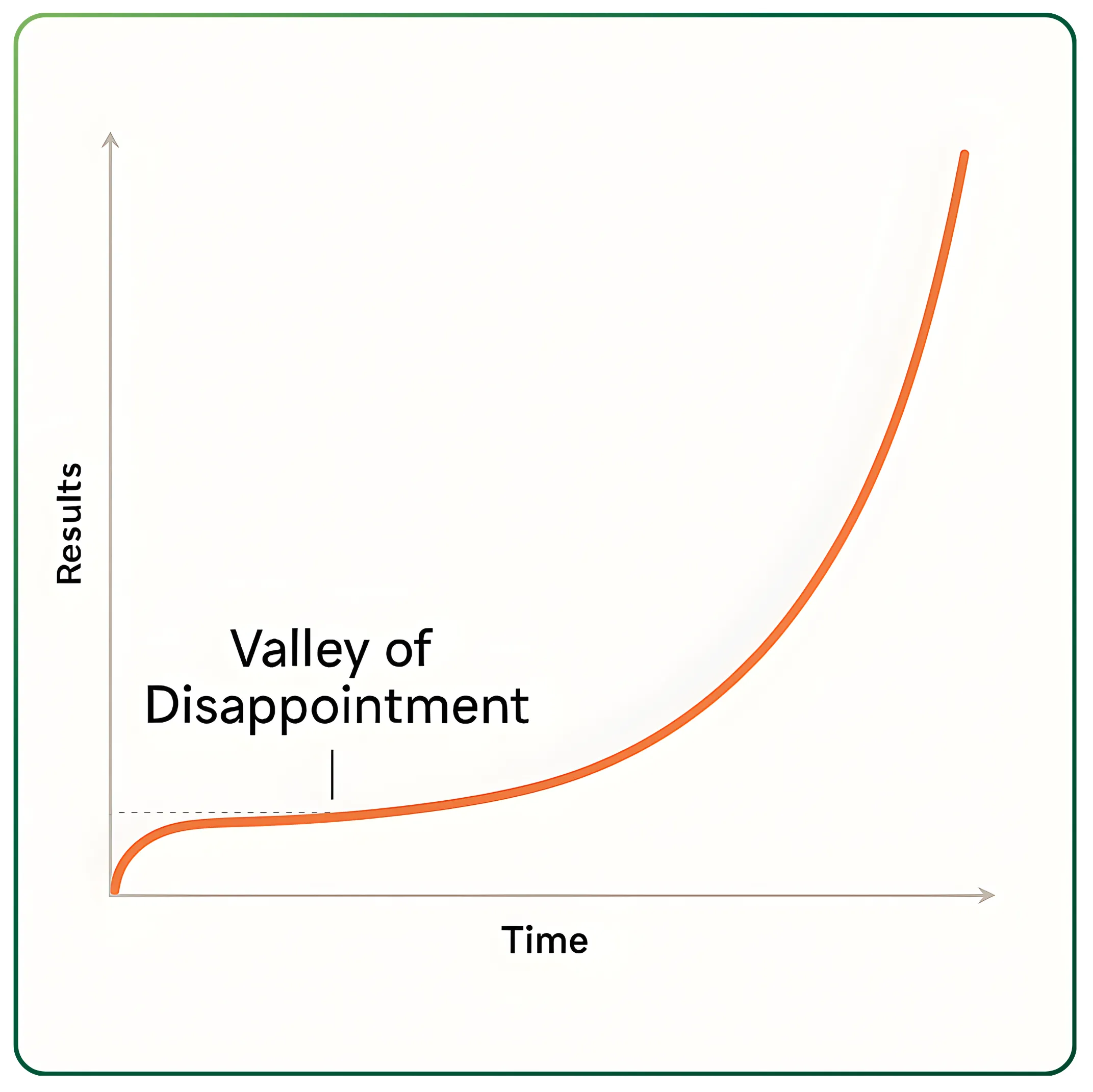

The early struggle: The Valley of Disappointment

The valley of disappointment describes the period when your contributions seem to matter far more than your returns. Compounding, despite its reputation for creating long-term wealth, begins quietly. When the invested base is small, even a strong return produces only modest gains.

This mismatch between expectation and reality often frustrates new investors. They imagine a steady upward curve, but what they see instead is a flat line that tests their patience. Many abandon their strategy here, not because it has stopped working, but because the early results feel too insignificant to inspire confidence.

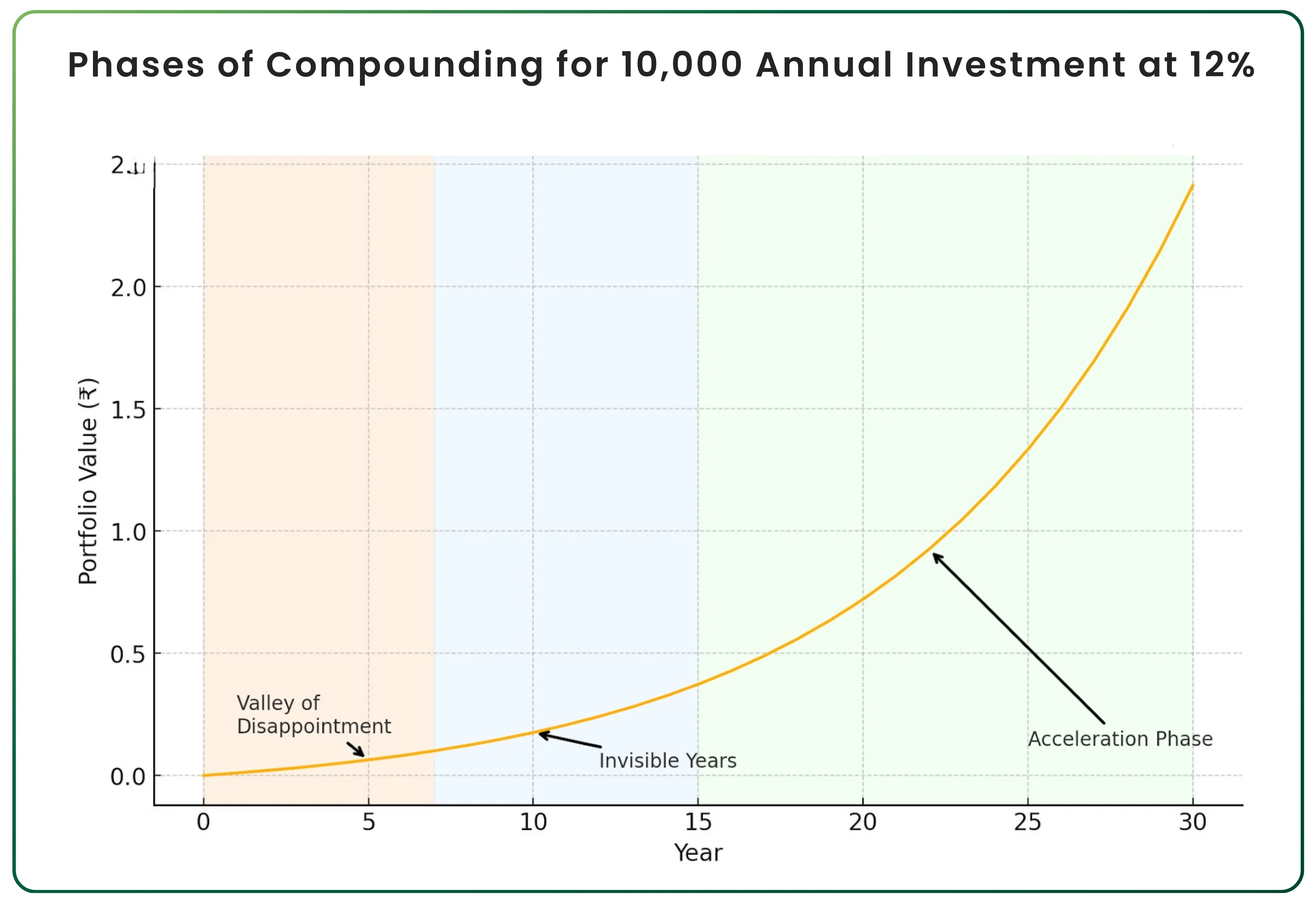

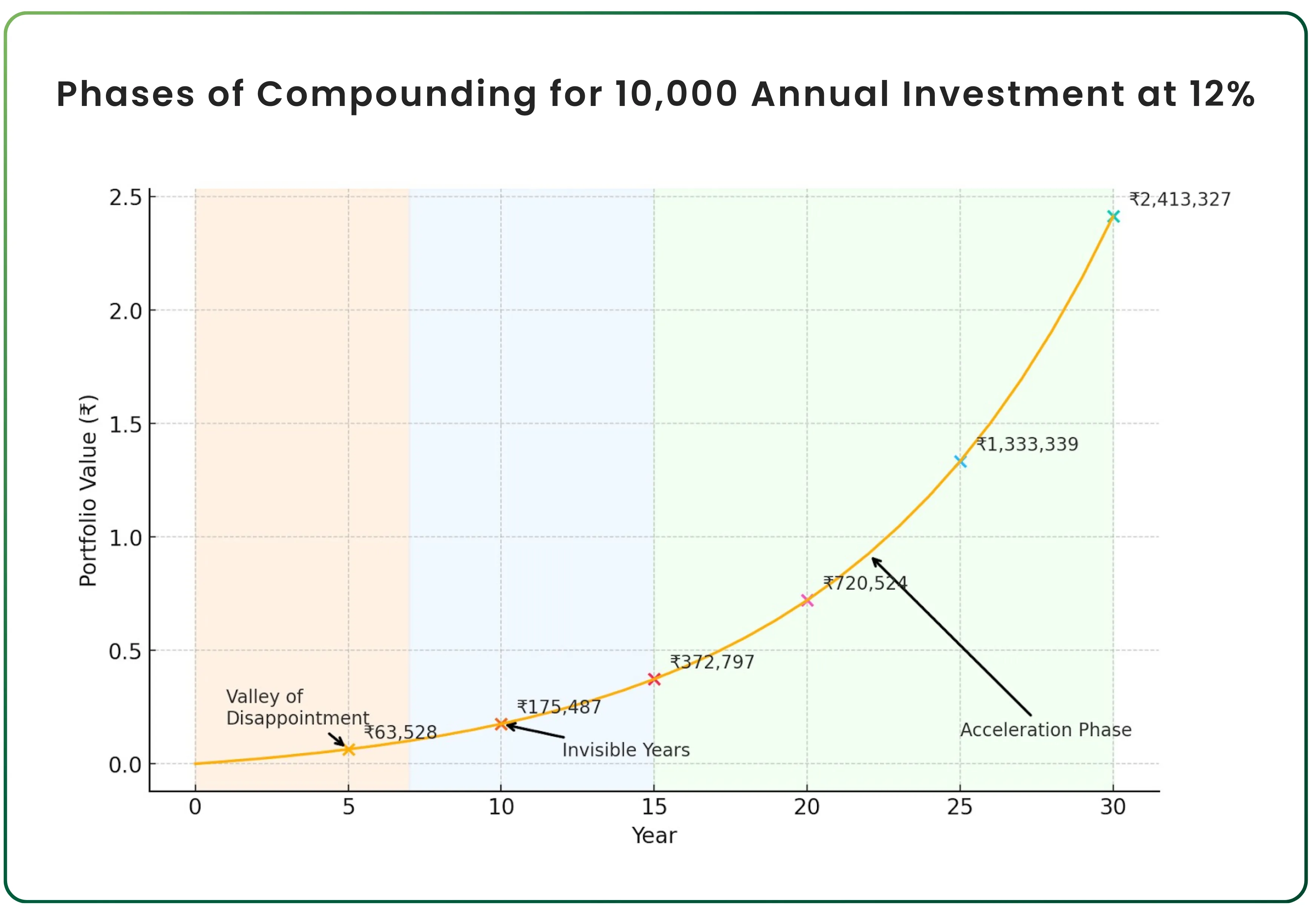

The quiet middle: The Invisible Years

After the first stretch, results do improve, but still not dramatically enough to command attention. These are the invisible years: a long-term period within the investment time horizon when growth is real but subtle. Your portfolio expands steadily, yet the increases are gradual enough to escape notice. It is easy to mistake this stability for stagnation.

In truth, these years are essential. They build the foundation on which compounding accelerates. Without this period of slow, steady accumulation, the later surge simply cannot occur.

Also read: The Philip Fisher Approach to Owning Stocks Like a Business Owner to understand how long-term investors think beyond price movements and focus on business quality.

When the curve begins to rise

At a certain point, the portfolio reaches a size where returns start to make a meaningful impact, and the return curve begins to bend upward. The same percentage gain now produces a larger monetary jump. What once felt slow suddenly begins to accelerate.

A simple example makes this clear. Suppose an investor contributes ten thousand rupees each year and earns a twelve percent annual return.

After five years, the portfolio stands at around seventy-eight thousand.

After ten years, it is just under two lakh.

At this stage, the numbers still feel modest.

But then the effect of scale becomes visible.

By the fifteenth year, the total grows to roughly 3.8 lakh.

By the twentieth year, it crosses 6.3 lakh.

By the twenty-fifth year, it exceeds 10 lakh.

By the thirtieth year, it reaches nearly 18 lakh.

What is striking is that a large portion of the final value appears in the last few years. Nothing changed except time. The return rate stayed the same. The contribution stayed the same. But the base grew large enough for compounding to exert its full influence.

Also read: How Peter Lynch Picked Winning Stocks – A Simple Look at His Investment Strategy to see how everyday observations and long-term thinking shaped some of the most successful stock picks.

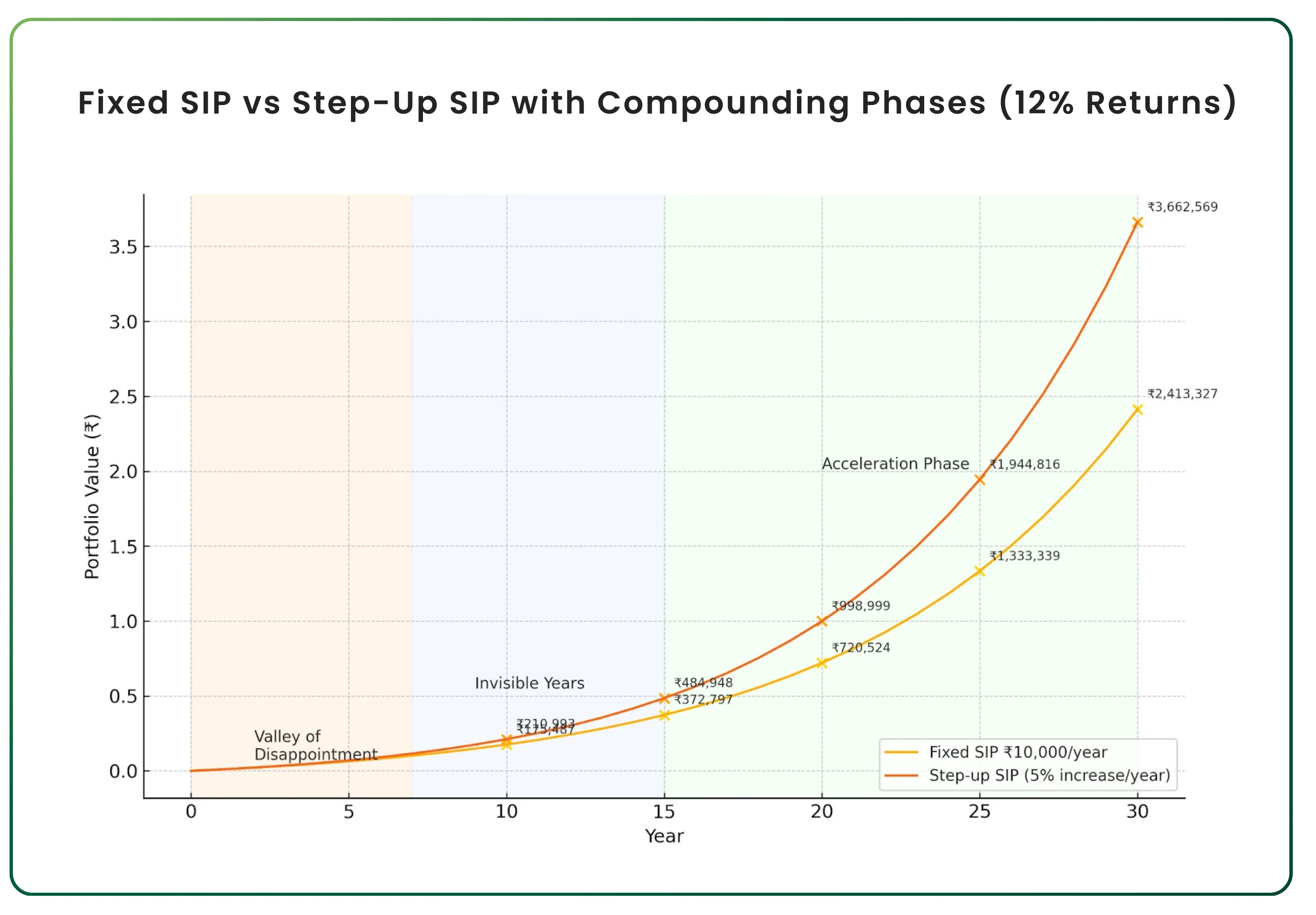

What happens when you step up your contributions each year

A fixed investment creates a clear illustration of compounding, but real investors rarely keep their contributions unchanged for decades.Income grows, responsibilities shift, and strong savings discipline allows contributions to rise with time. A modest annual increase in contributions can reshape the curve far more than most people expect.

Consider the same example: an investor begins by investing ten thousand rupees in the first year, but increases this amount by five percent every year. The return rate remains twelve percent. The mathematics now behaves differently. The portfolio is no longer growing only through returns; it is expanding through a rising stream of contributions that compound on their own schedule.

The early years still look restrained, although the lift is slightly stronger. By the tenth year, the invested amount itself is meaningfully higher than in the fixed-SIP scenario. By the fifteenth and twentieth years, the portfolio begins to separate from the earlier curve, creating a wider and wider gap. The acceleration in the later years becomes even more pronounced because both the return base and the contribution base are growing simultaneously.

A step-up plan does not rely on dramatic increases. Even a five percent annual rise (barely noticeable in any given year) creates a visible difference over a long horizon. Investors often underestimate this effect, assuming that only market returns matter. In reality, disciplined contribution growth is one of the most reliable levers for long-term wealth creation.

The message is simple: if time gives compounding its strength, rising contributions give it its reach. Combining both turns a slow early journey into a powerful long-term engine.

A rising SIP is not only a tool for accelerating wealth; it is also a practical response to inflation. The cost of living increases every year, and so does the earning capacity of most investors. A fixed contribution, if left unchanged for decades, loses its real strength as inflation steadily erodes the value of money. A five percent annual increase mirrors the gradual rise in income and ensures that the investing effort does not fall behind the pace at which prices move. In effect, the step-up protects the purchasing power of your future corpus while allowing compounding to work with a growing stream of contributions. It is a simple adjustment, yet over long horizons, it makes the investment journey far more resilient.

Time as the true multiplier

Many investors concentrate on chasing higher returns, but the more powerful factor is simply staying invested long enough for compounding to work. The early years are quiet, the middle years are understated, and the later years carry the real weight. Understanding this progression can help investors maintain discipline during the dull stretches when the temptation to change strategies is strongest. This phase demands investment patience, not constant decision-making.

Those who recognise the value of time avoid unnecessary tinkering. They accept that progress will look modest before it becomes meaningful. This patience, rather than any form of market expertise, is what eventually creates significant wealth.

The long-term reward

Compounding does not offer quick results. It offers reliable results to those who allow it to function without interruption. The valley of disappointment and the invisible years are not signs of failure; they are evidence that the process is unfolding as intended. This is the foundation of long-term wealth creation.

The acceleration that arrives later is simply the delayed consequence of years of steady investing. Once it begins, it often feels sudden, but it is the product of quiet growth accumulated over time.

The lesson is straightforward: if you stay invested and give your money enough time, the curve eventually tilts in your favour. What appears slow at first often becomes remarkable later, forming the basis of sustainable financial growth.The difference lies not in complex strategies, but in the willingness to wait.

If you want to apply these long-term investing principles in real markets, you can explore CubePlus, our platform designed for disciplined trading and investing.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.