Peter Lynch, one of the most successful fund managers of all time, built his reputation on a simple but powerful investment strategy. His stock selection process focused on understanding companies deeply before buying them — an approach many still use to learn how to pick stocks like Peter Lynch.

Most investors chase trends. Peter Lynch didn’t. He believed the best ideas often come from what you already know — the brands you use, the shops you visit, and the products you see people buying more of. His style wasn’t about timing markets or reading economic forecasts; it was about finding great businesses early and holding them long enough for the story to play out.

Here’s how Lynch broke down his investment process, step by step.

Start With What You Know

Lynch’s investing framework started with everyday observation. When you notice a new product catching on or a company’s stores always crowded, you might be seeing a winning business before Wall Street does.

He often said the best stock ideas come from daily life — not analyst reports. The rule was simple: if you understand what a company does and why people like it, that’s a good starting point.

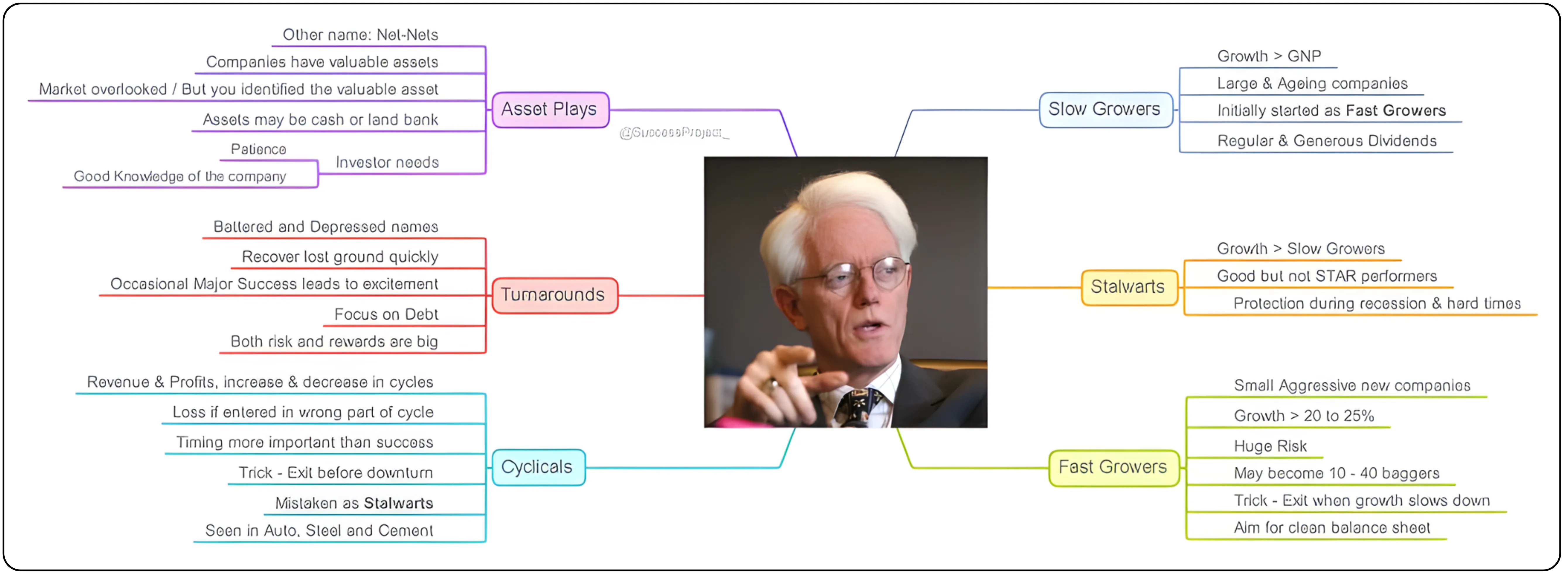

Know What You’re Buying: Peter Lynch’s Six Types of Stocks

Peter Lynch believed not all stocks are created equal. Each company falls into a certain category, and understanding which one you’re dealing with is key to setting the right expectations. Here’s how he broke them down.

1. Asset Plays

These are companies sitting on hidden assets that the market hasn’t fully recognized — things like cash reserves, real estate, valuable subsidiaries, or even intellectual property. Sometimes, the market focuses so much on earnings that it ignores what’s buried in the balance sheet.

The opportunity lies in spotting this disconnect early. Lynch often called them “net-nets” — businesses trading below the value of their assets minus liabilities. But patience is essential here; unlocking that value can take years, and you need deep company-specific knowledge to know what you truly own.

2. Turnarounds

Turnarounds are the comeback stories of the stock market — companies that have fallen out of favor but have the potential to recover sharply. These are often businesses hit by short-term problems, restructuring issues, or industry slowdowns.

When things go right, the returns can be spectacular. But they’re not for the faint-hearted. Lynch warned that the line between a turnaround and a failure is thin. The focus here should always be on debt levels and balance sheet strength — because a highly leveraged company can run out of time before its turnaround happens.

3. Cyclicals

Cyclical stocks move in tandem with the economy. Their revenues and profits rise when demand is strong and fall sharply when the cycle turns down. Think autos, steel, cement, commodities, or shipping.

The trick with cyclicals isn’t about predicting growth — it’s about timing. You want to buy when earnings are depressed and sentiment is low, and sell when the cycle peaks. Many investors mistake cyclicals for steady “stalwarts” when times are good, only to be caught off guard when profits collapse. Lynch’s rule here: always exit before the downturn.

4. Slow Growers

These are large, mature companies that have long passed their high-growth phase. Their earnings typically rise slower than the overall economy (or GNP, as Lynch framed it).

While they won’t make you rich quickly, slow growers compensate investors with steady dividends and stability. Most started out as fast growers decades ago but now focus on preserving market share and rewarding shareholders with regular payouts. Lynch didn’t dislike them — he just saw them as income plays, not growth stories.

5. Stalwarts

Stalwarts are dependable performers — not too exciting, but rarely disappointing. They’re typically large, well-established companies with stable earnings and modest but reliable growth, often around 10–12% annually.

These stocks tend to hold up well in recessions and offer a safe harbor when markets turn volatile. Lynch liked owning stalwarts for balance in a portfolio — they might not be multibaggers, but they provide consistent returns and peace of mind.

6. Fast Growers

Fast growers are Lynch’s favorites — the potential multibaggers. These are smaller, aggressive companies expanding sales and profits at 20–25% or more each year. If you find one early, it could be a 10-, 20-, or even 40-bagger.

But growth stocks are fragile. The same speed that drives them up can send them crashing down if momentum fades. Lynch’s advice was simple: enjoy the ride, but sell when growth slows. Clean balance sheets and strong cash flows were must-haves; debt-fueled growth often ended badly.

This categorization became the foundation of Peter Lynch’s investment strategy, helping investors recognize risk and reward across different stock types.

For a fresh perspective on strategy in investing, check out What Sun Tzu Can Teach Modern Traders and Investors.

Build a Simple Story

Lynch wanted every investment idea to have a clear, one-line story — something even a non-investor could understand.

It could be “this retailer is expanding rapidly into new cities” or “this company benefits from rising demand for affordable housing.” If you can’t explain the business or its growth driver in plain English, you probably don’t understand it well enough to own it.

Do the Homework

Once the story made sense, Lynch turned to the numbers — because a good narrative only matters if it’s backed by solid fundamentals. His research wasn’t about complicated models or forecasts; it was about finding proof that the business was healthy, growing, and fairly valued.

Earnings Growth:

The first thing he looked for was steady, predictable earnings growth — ideally between 15% and 30% a year. This range was the sweet spot: fast enough to compound meaningfully, yet realistic and sustainable. Lynch didn’t get excited by one good quarter; he wanted to see a clear upward trend over several years. To him, consistent profit growth signaled a company with strong demand, pricing power, and good management execution.

Debt Levels:

Debt was one of his biggest red flags, especially in cyclical or turnaround stocks. High leverage can make companies look more profitable in good times but crush them when the cycle turns. Lynch preferred businesses that could fund their own expansion through internal cash generation. His logic was simple — the less a company owes, the more control it has over its destiny.

Cash Flow:

Strong operating cash flow was another must. Earnings can be manipulated on paper, but cash doesn’t lie. Lynch wanted to see that profits were translating into real money coming into the business. Consistent cash inflow meant the company could reinvest for growth, pay dividends, or reduce debt — all without external help.

Profit Margins:

He also studied profit margins — both gross and net — to gauge whether the company had a durable business model. Expanding margins told him the company was becoming more efficient or gaining pricing power. Shrinking margins were an early warning that competition was eating into profits or costs were out of control. Lynch liked companies that could protect or grow margins even in tough markets.

PEG Ratio:

Finally, Lynch often used the PEG ratio (Price-to-Earnings divided by Growth rate) to decide whether a stock’s valuation made sense. A PEG near or below 1 usually indicated that investors were paying a fair or discounted price for the company’s growth.

- A PEG below 1 = undervalued growth

- Around 1 = fairly valued

- Above 1 = possibly overpriced

It was his quick, practical way to separate bargains from hype.

Lynch didn’t look for perfection — he looked for consistency, clarity, and common sense. A company didn’t need to tick every box, but it had to show that the fundamentals supported the story. In his words, “Behind every stock is a company. Find out what it’s doing.”

Curious how smart investors anticipate market reactions? You might like How Game Theory Can Help You Predict Moves in the Indian Stock Market.

Check the Balance Sheet

A strong balance sheet keeps a company alive through tough times. Lynch preferred firms that didn’t rely too much on debt and had enough cash to fund growth internally. He often avoided businesses where interest costs could wipe out profits in a downturn.

Watch What Management Does

Actions matter more than words. If management was buying its own stock, Lynch saw that as a positive sign. It meant they believed the company was undervalued and had confidence in its future. Insider buying often spoke louder than any investor presentation.

Focus on Valuation

Lynch didn’t want to overpay, even for great companies. He compared a company’s P/E ratio with its growth rate. If earnings were growing faster than the P/E, the stock was attractive. If not, it was probably overhyped.

This simple rule — growth should justify price — helped him avoid expensive mistakes.

Know Your Edge

This was the heart of how Peter Lynch picked stocks — combining real-world observation with financial evidence to find what the market missed.

Before buying, he always asked:

“What do I know that others don’t?”

That edge could be spotting a new trend earlier, understanding a niche business better, or simply paying attention to something most investors overlooked. Lynch’s advantage came from combining observation with research — not insider info or complicated models.

Stay Patient

Lynch’s favorite holding period was as long as the story stays true. He held stocks for three to five years, sometimes longer, letting compounding work in his favor. Short-term volatility didn’t bother him; declining earnings or fading fundamentals did.

Sell When the Story Changes

He sold when the original reason for buying disappeared — when growth slowed, competition strengthened, or the management lost direction. Price alone wasn’t a reason to sell; fundamentals were.

Peter Lynch’s Checklist Before Buying a Stock

I understand what the company does.

I know which category it belongs to.

The growth story makes sense and is backed by numbers.

Debt is under control, and cash flow is solid.

The valuation looks fair relative to growth.

Management owns stock and believes in the business.

I have a reason to think others are missing this story.

I’m ready to hold it long enough for the thesis to play out.

The Bottom Line

If you want to learn how to pick stocks like Peter Lynch, start by understanding the businesses around you, check the numbers, and stay patient. That simple investing framework has stood the test of time — and still works today.

Peter Lynch’s approach made investing less about prediction and more about understanding. You don’t need to outsmart the market — just recognize good businesses early, pay a fair price, and give them time to grow.

Start building your own Peter Lynch-style watchlist today. You might already be using the next multibagger without even realizing it.

Turn research into action and explore smarter investing opportunities with CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.