The cash flow statement is one of the most critical financial documents for understanding a company’s financial health. Unlike the Profit and Loss (P&L) statement, which may include non-cash transactions like depreciation, the cash flow statement provides a clear picture of how much cash a company generates and spends. It tracks the actual cash moving in and out of the business, categorized into three main activities: operating, investing, and financing. In this blog, we’ll break down these concepts with simple examples to help you grasp the essence of the cash flow statement.

Why the cash flow statement matters

While the P&L statement shows profitability, it doesn’t always reflect the cash a company has on hand. For instance, a business might report high profits but still face cash shortages due to credit sales or heavy capital expenditures. The cash flow statement bridges this gap by focusing solely on cash transactions, giving investors a transparent view of a company’s liquidity, working capital management, and ability to sustain operations.

Let’s dive into the three core components of the cash flow statement with relatable examples.

Also Read: What is percentage gain?

1. Cash flow from operating activities

Operating activities are the core business functions that generate revenue, such as selling products or services. This section of the cash flow statement shows how much cash the company generates from its primary operations, which is a key indicator of financial health. A positive cash flow from operations suggests the business is self-sustaining, while a negative one may signal operational inefficiencies. There are two methods to calculate this: the direct method, which lists all cash disbursements and receipts, and the indirect method, which starts with net income and adjusts for non cash expenses like depreciation and changes in working capital.

Example: Imagine a small bakery, "Sweet Delights," which sells cakes and pastries. In a given month, the bakery earns ₹10,000 from cash sales and ₹5,000 from credit sales (to be paid later). It pays ₹4,000 for ingredients, ₹2,000 for rent, and ₹1,500 for employee salaries, all in cash. Additionally, it receives ₹3,000 from a customer who paid off a previous credit sale. Using the direct method, the cash flow from operating activities would be calculated as:

Cash inflows: ₹10,000 (cash sales) + ₹3,000 (credit sale collections) = ₹13,000

Cash outflows (or cash disbursements): ₹4,000 (ingredients) + ₹2,000 (rent) + ₹1,500 (salaries) = ₹7,500

Net cash flow from operating activities: ₹13,000 - ₹7,500 = ₹5,500

Alternatively, using the indirect method, Sweet Delights would start with its net income, add back non cash expenses like depreciation, and adjust for changes in working capital (e.g., receivables or payables). This positive cash flow indicates that Sweet Delights is generating enough cash from its core operations to cover its expenses, a sign of operational strength.

2. Cash flow from investing activities

Investing activities involve cash transactions related to long-term assets, such as purchasing equipment, property, or investments, or selling these assets. This section typically shows cash outflows, as companies invest in capital expenditures to grow their business, but it can also include inflows from asset sales.

Example: Sweet Delights decides to expand by purchasing a new oven for ₹8,000 and a delivery van for ₹12,000, both paid in cash. These purchases are examples of capital expenditures. It also sells an old mixer for ₹1,500. The cash flow from investing activities would be:

Cash outflows: ₹8,000 (oven) + ₹12,000 (van) = ₹20,000

Cash inflows: ₹1,500 (mixer sale)

Net cash flow from investing activities: ₹1,500 - ₹20,000 = -₹18,500

The negative cash flow here reflects the bakery’s investment in growth, which is typical for businesses aiming to expand. However, consistent negative cash flow from investing activities should be evaluated to ensure the investments are sustainable.

3. Cash flow from financing activities

Financing activities involve transactions with the company’s owners or creditors, such as issuing shares, borrowing loans, repaying debt, or making dividend payments. This section shows how a company funds its operations and manages its company’s capital structure, which includes equity and debt. It also includes cash flows related to interest paid on loans and dividend payments to shareholders.

Example: To fund its expansion, Sweet Delights takes a ₹15,000 bank loan and issues new shares to investors, raising ₹10,000 in cash. It also repays ₹5,000 of an existing loan and pays ₹2,000 in dividend payments to shareholders, along with ₹500 in interest paid on the loan. The cash flow from financing activities would be:

Cash inflows: ₹15,000 (loan) + ₹10,000 (share issuance) = ₹25,000

Cash outflows: ₹5,000 (loan repayment) + ₹2,000 (dividend payments) + ₹500 (interest paid) = ₹7,500

Net cash flow from financing activities: ₹25,000 - ₹7,500 = ₹17,500

This positive cash flow shows that Sweet Delights is raising funds to support its operations and growth, likely to offset the cash spent on capital expenditures. The inflows and outflows reflect changes in the company’s capital structure, balancing debt and equity to fund its activities.

Also Read: Understanding Stock Valuation Through Key Financial Ratios

Net cash flow and its significance

The net cash flow is the sum of cash flows from operating, investing, and financing activities. It represents the overall change in a company’s cash position over a period.

Example: For Sweet Delights, the net cash flow for the month is:

- Operating activities: +₹5,500

- Investing activities: -₹18,500

- Financing activities: +₹17,500

- Net cash flow: ₹5,500 - ₹18,500 + ₹17,500 = ₹4,500

A positive net cash flow of ₹4,500 means the bakery’s cash reserves increased by that amount, which is reflected in its balance sheet under cash and cash equivalents. A negative net cash flow, on the other hand, would indicate that the company is spending more cash than it’s generating, potentially dipping into reserves or requiring additional financing.

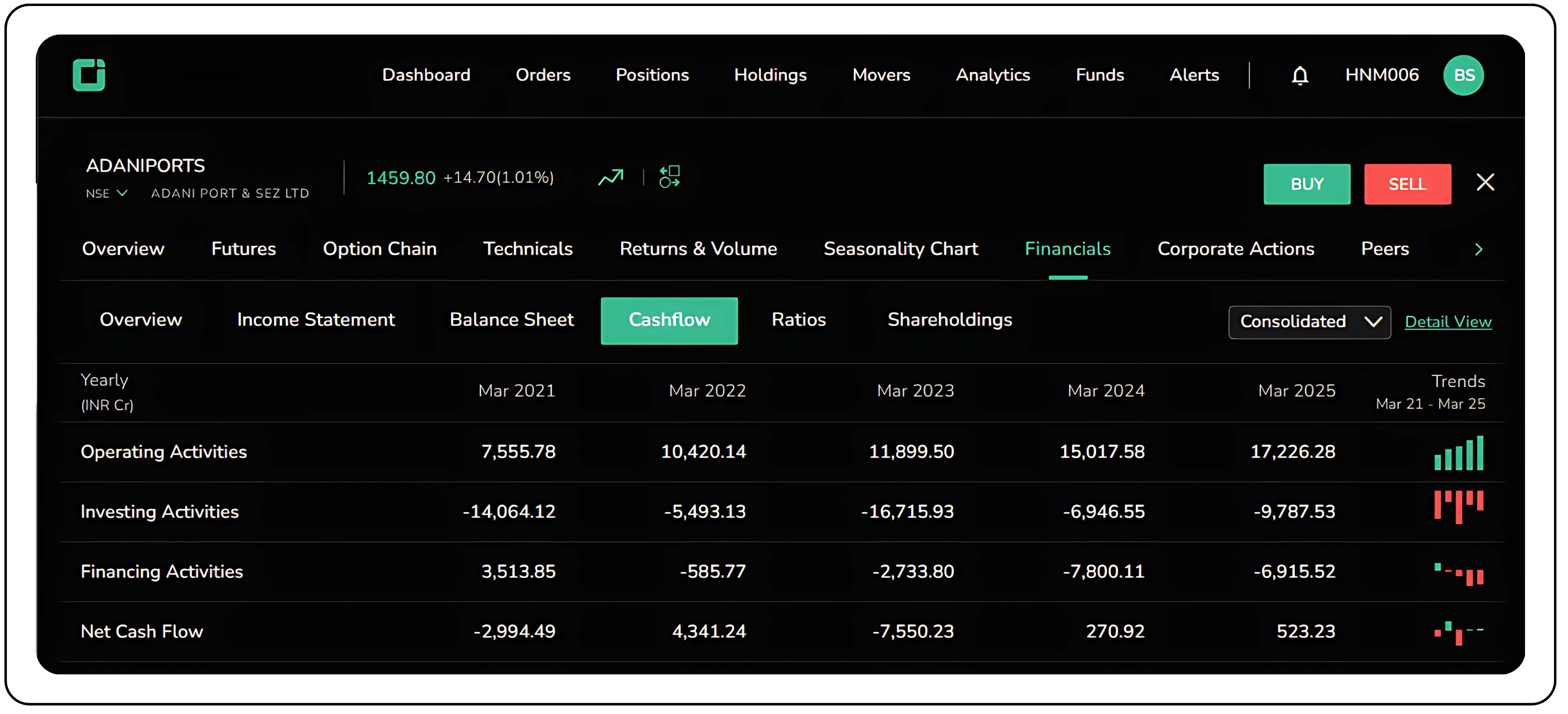

Example from Tradejini

Interpretation of the statement:

Operating Cash Flow is growing each year, which is very positive.

Investing Cash Flow is mostly negative (as expected), reflecting business expansion.

Financing Cash Flow turned negative, showing debt repayment or lower borrowing.

Net Cash Flow dipped in FY23 but became positive in FY24 and FY25 – indicating better financial balance.

Key takeaways for investors

The cash flow statement is a powerful tool for assessing a company’s financial health. Here are some insights to focus on:

Positive Operating Cash Flow: A company with consistent positive cash flow from operations, calculated using either the direct method or indirect method, is likely efficient and sustainable, as it can cover expenses without relying on external funding.

Investing Cash Flow: Negative cash flow from investing activities, often due to capital expenditures, isn’t always bad, it often signals growth through asset purchases. However, investors should ensure these investments align with the company’s long-term strategy.

Financing Cash Flow: Large inflows from loans or share issuances may indicate growth plans, but high debt repayments, interest paid, or dividend payments could strain cash reserves. The company’s capital structure plays a key role in balancing these cash flows.

Net Cash Flow: The final number ties into the balance sheet, showing how the company’s cash position evolves. It’s a critical metric for understanding liquidity and working capital management.

Connecting the cash flow statement to other financial statements

The cash flow statement doesn’t exist in isolation; it’s closely linked to the P&L statement and balance sheet. For instance, the profit after tax from the P&L statement flows into the balance sheet’s reserves, but the cash flow statement clarifies how much of that profit is actual cash, excluding non cash transactions like depreciation or non cash expenses. Similarly, changes in assets (like inventory) or liabilities (like loans) on the balance sheet, which affect working capital, are reflected in the cash flow statement’s operating and financing sections.

Example: If Sweet Delights reports a ₹7,000 profit on its P&L statement but only ₹5,500 in perating cash flow, it suggests that ₹1,500 of the profit is tied up in receivables (credit sales). This insight, drawn from the cash flow statement, helps investors understand the bakery’s actual cash position and working capital dynamics.

Also Read: Are Neo Banks the Next Big Fintech Shift?

Conclusion

The cash flow statement is like a financial GPS, guiding investors through a company’s cash movements. By breaking down cash flows into operating, investing, and financing activities, it reveals how a business sustains itself, invests in growth through capital expenditures, and manages its funding within its company’s capital structure. Always read company’s cash flow statement to uncover the real story behind its financials.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.