Idle cash often feels like a temporary situation. In a bank account, money waits for the next opportunity, the next expense, or the ideal time to enter the market. It's assumed that it's okay because it's accessible and safe.

Here’s the thing. Cash sitting idle quietly loses value. Inflation works against it every day, and low interest rates ensure the erosion goes unnoticed. Over time, this drag adds up, especially when large sums or recurring surpluses are involved.

Parking your idle money isn’t about chasing high returns. It’s about making sure cash earns something reasonable while staying safe, liquid, and ready to be used. In India, there are several options that do this far better than letting money sit untouched in a savings account.

This guide walks through those options in a practical way, focusing on liquidity, safety, taxation, and actual returns rather than headline numbers.

Parking Your Idle Money Starts with Understanding the Purpose

Idle money usually exists for a reason. It could be surplus salary waiting to be invested, business cash flows between cycles, funds set aside for utility bills, or an emergency buffer. The mistake most investors make is treating all idle cash the same.

Money needed for daily expenses should stay easily accessible. Money that won’t be touched for a few weeks or months deserves to work harder. The goal is not speculation but intelligent cash management.

Once you think in terms of time horizon instead of habit, better options naturally emerge.

The Savings Account Trap

A savings account is the default place for idle cash because it feels effortless. There’s instant access, zero paperwork, and no visible risk. But convenience comes at a cost.

Most banks still offer modest interest rates, and that interest is fully taxed as per your income tax slab. After tax, the real return is often barely positive. Over time, this turns savings accounts into parking lots rather than productive tools.

Savings accounts are necessary for transactions and expenses. They are rarely optimal for surplus cash that does not need same-day access.

New to investing and wondering why progress feels slow? Read our explainer on Why the Early Years of Compounding Make Progress Feel Invisible

Liquid Mutual Funds: Designed for Idle Cash

Liquid mutual funds exist for one purpose: managing short term cash efficiently. They invest in high-quality short term debt instruments such as treasury bills, commercial papers, and certificates of deposit, all with very short maturities.

Because of this structure, liquid funds show minimal volatility. NAV movements are small, liquidity is high, and regulatory safeguards are strict. SEBI mandates tight rules on portfolio quality and liquidity buffers, which significantly reduces risk.

For most retail investors, liquid mutual funds represent a meaningful upgrade from savings accounts. Returns are higher, access is quick, and the risk profile remains conservative.

Liquid Funds vs Savings Accounts: A Practical Comparison

The difference between a savings account and a liquid fund isn’t complexity, it’s efficiency. A savings account offers instant access but poor post-tax returns. Liquid funds offer near-immediate access with better yield.

For money that doesn’t need to be withdrawn the same day, liquid funds tend to deliver superior outcomes without compromising safety. This is why many investors now use liquid funds for surplus cash, emergency buffers beyond immediate needs, and short term parking.

Overnight Funds: For Extremely Short Holding Periods

Overnight funds take conservatism one step further. They invest only in instruments that mature the next business day. This makes them one of the lowest risk mutual fund categories available.

These funds are useful when money needs to be parked for just a few days. Businesses use them extensively for managing daily cash flows. Individual investors use them between transactions or while waiting for deployment into longer-term investments.

Returns are modest but stable, and liquidity is excellent. For high-income investors, the tax treatment can make overnight funds more efficient than savings accounts despite similar headline yields.

Liquid and Arbitrage Funds: Not the Same Thing

Liquid funds and arbitrage funds are often mentioned together, but they work very differently. Liquid funds earn returns from interest on short term debt instruments. Arbitrage funds earn returns by exploiting price differences between the cash market and the futures market.

Arbitrage funds are classified as equity-oriented for tax purposes, which can make them attractive for investors in higher tax brackets. However, their returns depend on market conditions, especially spreads in the futures market. They are not substitutes for liquid funds in all environments.

Understanding this distinction is critical before choosing between the two.

Treasury Bills: Safety Above All Else

Treasury bills are short term instruments issued by the Government of India. They carry no credit risk and offer clearly defined maturity dates.

Returns are usually lower than liquid mutual funds, but the safety is unmatched. For investors who prioritise capital protection above everything else, treasury bills remain a dependable option for parking idle cash.

They are especially relevant for conservative investors, institutions, and those who want certainty without relying on bank credit quality.

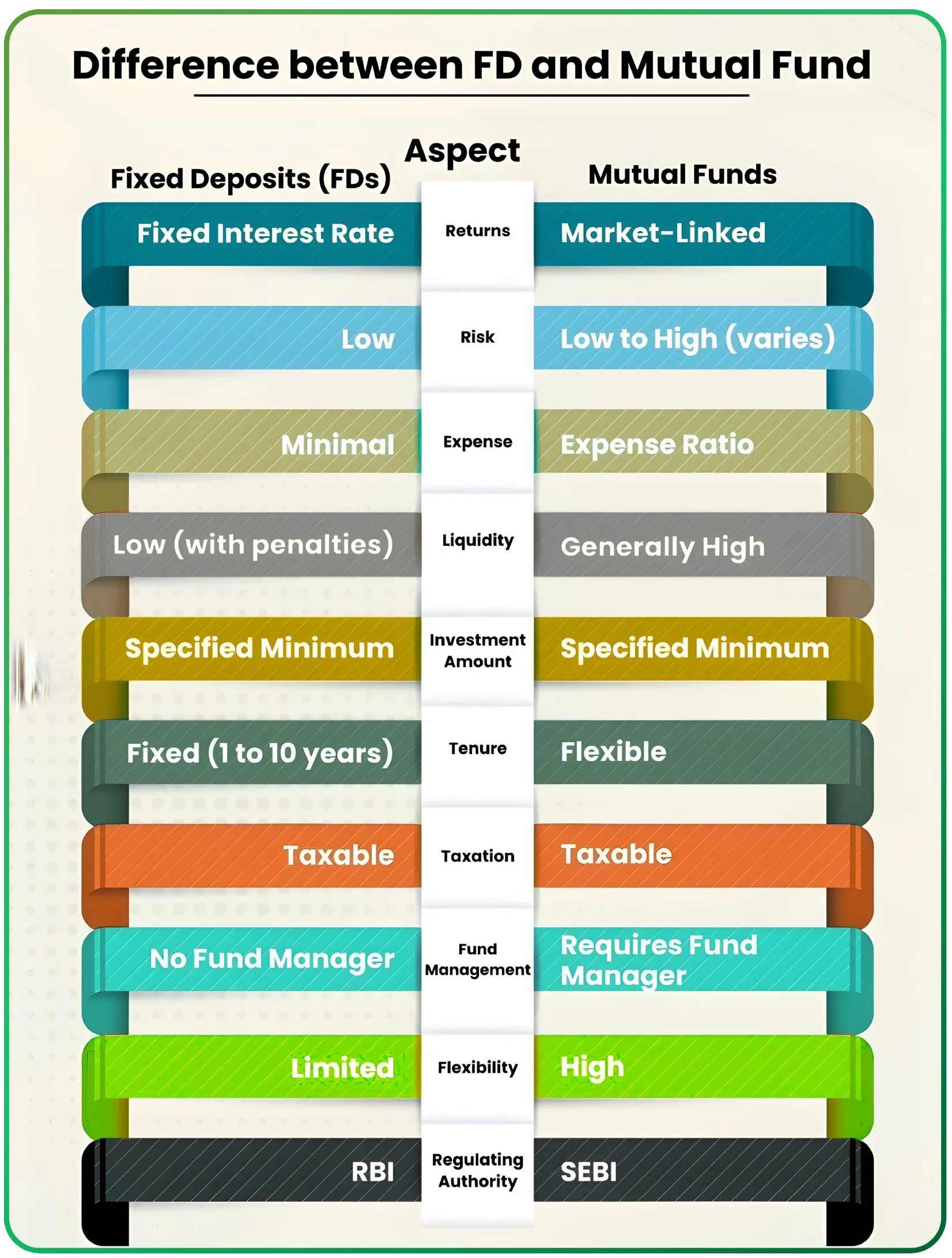

Fixed Deposits: Certainty with Constraints

Fixed deposits remain popular because they are simple and predictable. You know exactly how much you will receive at maturity. There are no NAV fluctuations and no market-linked movement.

The trade-off is liquidity. Premature withdrawals usually attract penalties, and interest income is fully taxed. For short term goals with a fixed timeline, fixed deposits still serve a purpose. For uncertain cash needs, they can be restrictive.

Fixed deposits are best used deliberately, not by default.

Debt Funds for Short Term Goals

Short term debt funds sit between liquid funds and longer-duration bond funds. They invest in slightly longer maturity instruments, which allows them to generate higher yields but also introduces some sensitivity to interest rate changes.

These funds suit investors with a clear holding period and the ability to tolerate small NAV movements. Reading scheme-related documents carefully becomes more important here, as credit quality and duration choices vary across funds.

If you’re building wealth beyond short-term parking, The Philip Fisher Approach to Owning Stocks Like a Business Owner is a useful read on long-term ownership thinking.

Building an Emergency Fund the Smart Way

An emergency fund must be safe and accessible, but it doesn’t all need to sit idle in a savings account. A common approach is to keep immediate expense coverage in a bank account and place the remaining portion in liquid or overnight funds.

This structure preserves liquidity while improving overall returns. The key is accessibility, not maximum yield.

Taxation: The Real Decider of Returns

Taxation often matters more than interest rates. Savings account interest and fixed deposit interest are taxed fully. Mutual fund investments are taxed as capital gains, which can improve post-tax outcomes depending on holding period and income slab.

For investors in higher tax brackets, liquid and overnight funds often deliver better actual returns even if the pre-tax difference looks small. Arbitrage funds can be tax-efficient in certain scenarios, but they carry different risks and should be chosen with care.

Exit Load, Liquidity, and Practical Details

Before investing, investors should understand exit load structures, redemption timelines, and settlement cycles. Liquid funds typically impose exit loads only for very short holding periods. Overnight funds usually have none.

These details matter when money is parked for utility bills, expenses, or short term commitments.

Understanding Risk Without Overreacting

Even low risk mutual funds are not risk-free. Credit events and interest rate movements can affect returns, although the probability and impact are limited in short duration products.

This is why diversification, fund manager discipline, and adherence to regulatory frameworks matter. There are no guaranteed returns outside sovereign-backed instruments, and that reality should be acknowledged upfront.

Matching Options to Investor Profiles

Retail investors benefit most from combining savings accounts for transactions with liquid funds for surplus cash. Investors with defined short term goals can add fixed deposits or treasury bills for certainty. Higher tax bracket investors may find overnight and arbitrage funds useful when chosen thoughtfully.

The best option is always the one that matches time horizon, liquidity needs, and tax situation.

Final Thoughts

Idle cash doesn’t need to sit idle. With the right tools, it can remain safe, liquid, and productive at the same time. The Indian market offers enough choice for investors to manage short term money intelligently without taking unnecessary risks.

The real advantage comes from clarity. When you know why the money exists and when you’ll need it, choosing where to park it becomes straightforward. The difference between idle cash and managed cash is rarely dramatic in the short run, but over time, it compounds into meaningful wealth preservation.

Explore mutual funds and manage idle cash more effectively on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.