This article is a follow-up to our earlier coverage of Laurus Labs, where we examined the company's business model, its ARV-heavy revenue concentration, and management's stated ambition to reorient toward technology-led CDMO services. The central question at the time was whether that transition would show up in the numbers. FY26 results provide the clearest answer yet.

What Has Changed Since Our Last Report

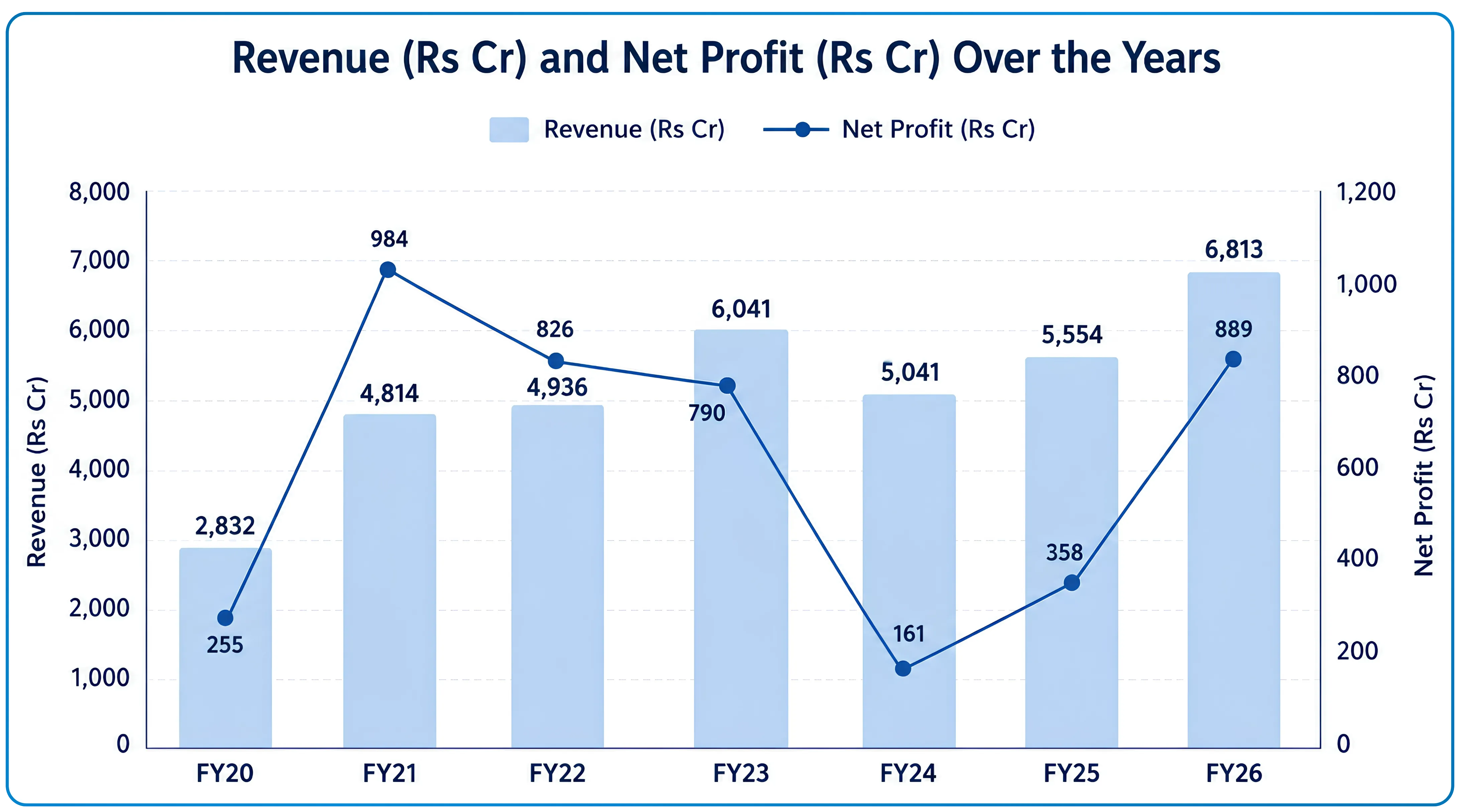

Our earlier coverage, published in April 2025, looked at Laurus Labs when the business was just finding its footing again. Revenues were at Rs 5,554 crore, profits had recovered to Rs 358 crore after a tough FY24, and the company had set itself a target of reaching Rs 6,700 to 7,300 crore in revenues by FY26. The big question was whether management would deliver on that promise? FY26 results show they did.

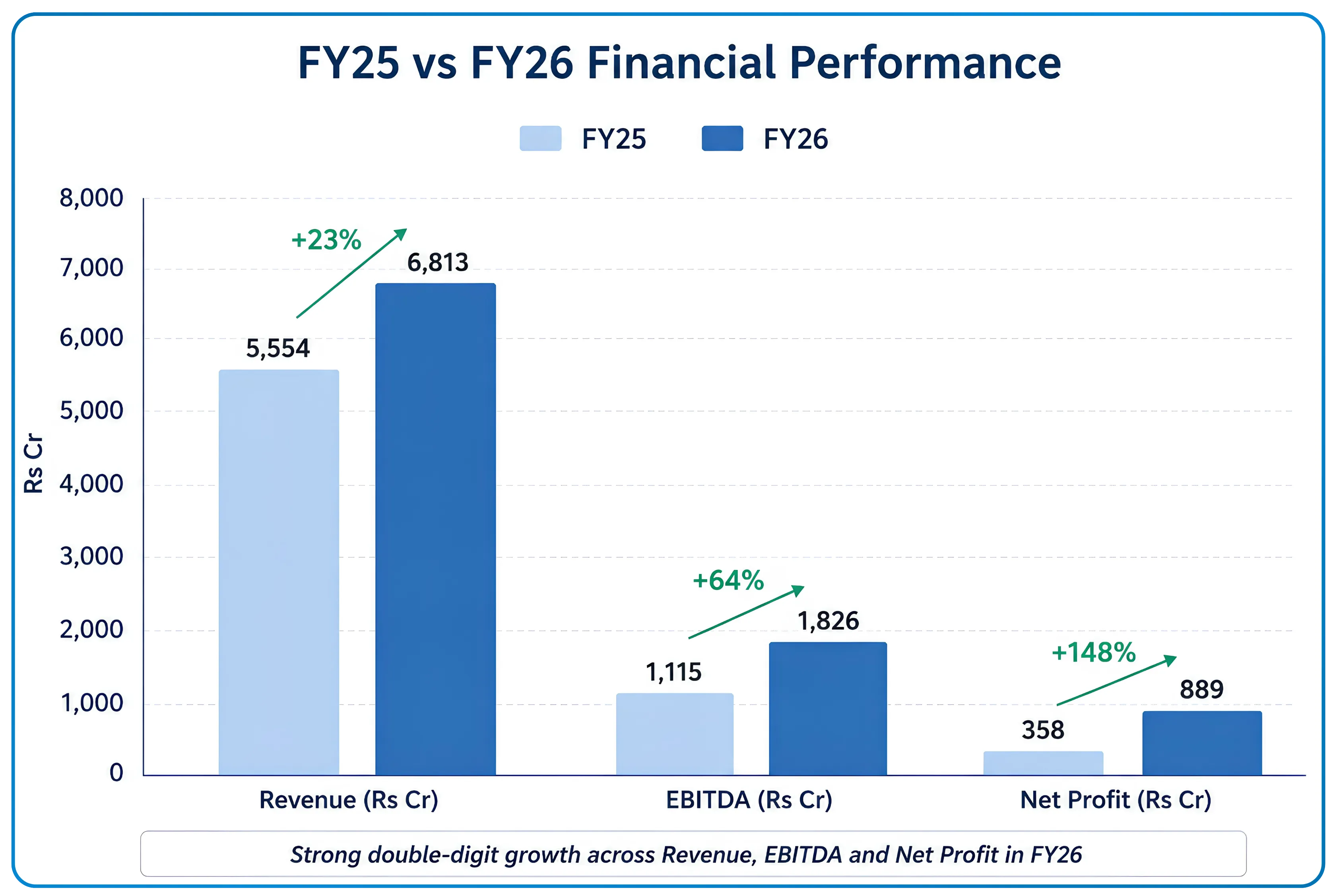

Revenue came in at Rs 6,813 crore, within the guided range. Profit margins, which had dropped sharply in FY24, have recovered strongly, with the company now retaining Rs 26.8 out of every Rs 100 it earns at the operating level, compared to Rs 20 a year ago. Net profit at Rs 889 crore is the highest in the company's history .The Rs 2,600 crore plant expansion programme we highlighted in the earlier report has been completed and the company has now committed an additional Rs 3,000 crore for the next two years.

Three things have also changed that were not part of the earlier story.

Laurus has moved into gene therapy and antibody-drug conjugate manufacturing, two advanced areas of medicine that go well beyond its traditional pharmaceutical chemistry roots.

Its CAR-T cell therapy unit, which makes a specialised cancer treatment, has tripled its production capacity.

And the company has secured a 532-acre plot in Vizag for a new large-scale manufacturing campus that will be built over the next eight years at an investment of over $600 million.

Laurus Labs Financial Recovery in Numbers

Before the FY26 detail, the multi-year context is worth stating plainly.

FY24 was the worst year in recent memory for Laurus. FY25 was a partial recovery. FY26 is the first year where revenue, profits, margins, and returns on capital all improved together.

FY26 Profit and Loss

| Metric | FY25 | FY26 | Change |

|---|---|---|---|

| Revenue (₹ cr) | 5,554 | 6,813 | +23% |

| Gross Margin | 55.4% | 60.4% | +500 bps |

| EBITDA (₹ cr) | 1,115 | 1,826 | +64% |

| EBITDA Margin | 20.1% | 26.8% | +670 bps |

| Net Profit (₹ cr) | 358 | 889 | +148% |

| Net Margin | 6.4% | 13.0% | +660 bps |

| EPS (₹) | 6.6 | 16.4 | +148% |

Revenue grew 23% to Rs 6,813 crore, with both the CDMO and generics businesses contributing. Profit margins improved across the board. For every Rs 100 in revenue, the company now retains Rs 60.4 as gross profit, up from Rs 55.4 last year, reflecting a better product mix, manufacturing efficiencies, and lower raw material costs. At the operating level, the margin widened from 20.1% to 26.8%, meaning the company is converting a larger share of its revenues into operating profit than it was a year ago. Net profit nearly tripled despite revenue growing by only 23%, which tells you that the cost structure is now working in the company's favour.

Laurus Labs Cash Flow and Returns

| Metric | FY25 | FY26 | Change |

|---|---|---|---|

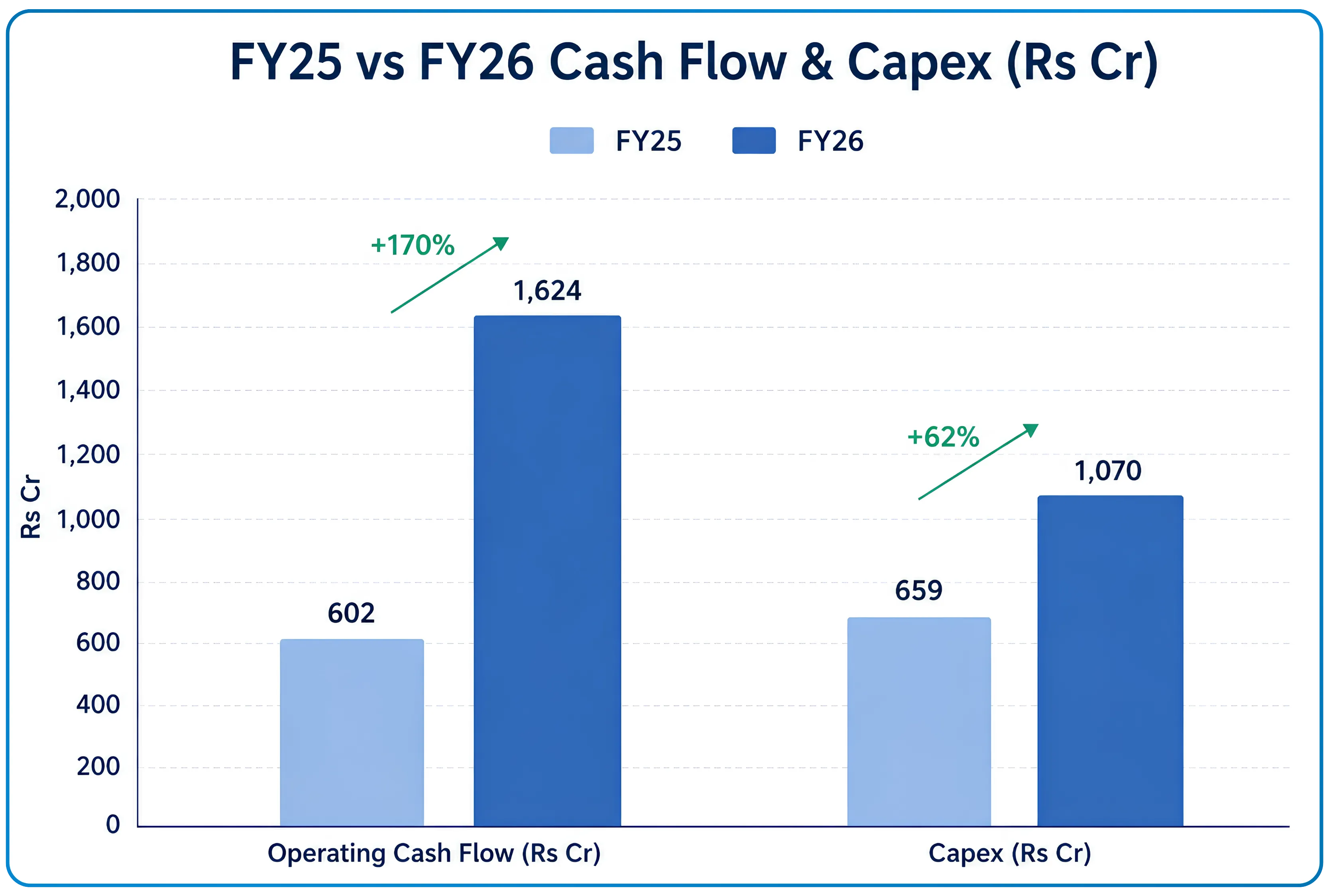

| Operating Cash Flow (₹ cr) | 602 | 1,624 | +170% |

| Capex (₹ cr) | 659 | 1,070 | +62% |

| Net Debt-to-EBITDA | 2.3x | 1.3x | -1.0x |

| ROCE | 9.7% | 17.7% | +800 bps |

The business also generated Rs 1,624 crore in cash from operations during the year, nearly three times the prior year's Rs 602 crore. This is significant because the company simultaneously spent Rs 1,070 crore on plant and capacity expansion, yet still managed to reduce its total borrowings. The ratio of net debt to annual operating profit, a measure of how comfortably a company can service its debt, improved from 2.3 times to 1.3 times. Returns on capital employed, which measure how efficiently the company is using the money invested in the business, rose to 17.7% from 9.7%, the highest level since FY22.

Q4 FY26 Snapshot

| Metric | Q4 FY25 | Q3 FY26 | Q4 FY26 | YoY | QoQ |

|---|---|---|---|---|---|

| Revenue (₹ cr) | 1,720 | 1,778 | 1,812 | +5% | +2% |

| Gross Margin | 54.5% | 60.9% | 61.4% | +690 bps | +50 bps |

| EBITDA (₹ cr) | 477 | 485 | 523 | +10% | +8% |

| EBITDA Margin | 27.7% | 27.3% | 28.9% | +120 bps | +160 bps |

| Net Profit (₹ cr) | 234 | 252 | 279 | +19% | +11% |

| EPS (₹) | 4.3 | 4.7 | 5.2 | +21% | +13% |

In Q4 specifically, revenue and operating profit both hit their highest quarterly levels ever. The margin improvement of 1.6 percentage points over the previous quarter, on revenue that grew by only 2%, suggests the operating leverage story still has room to run.

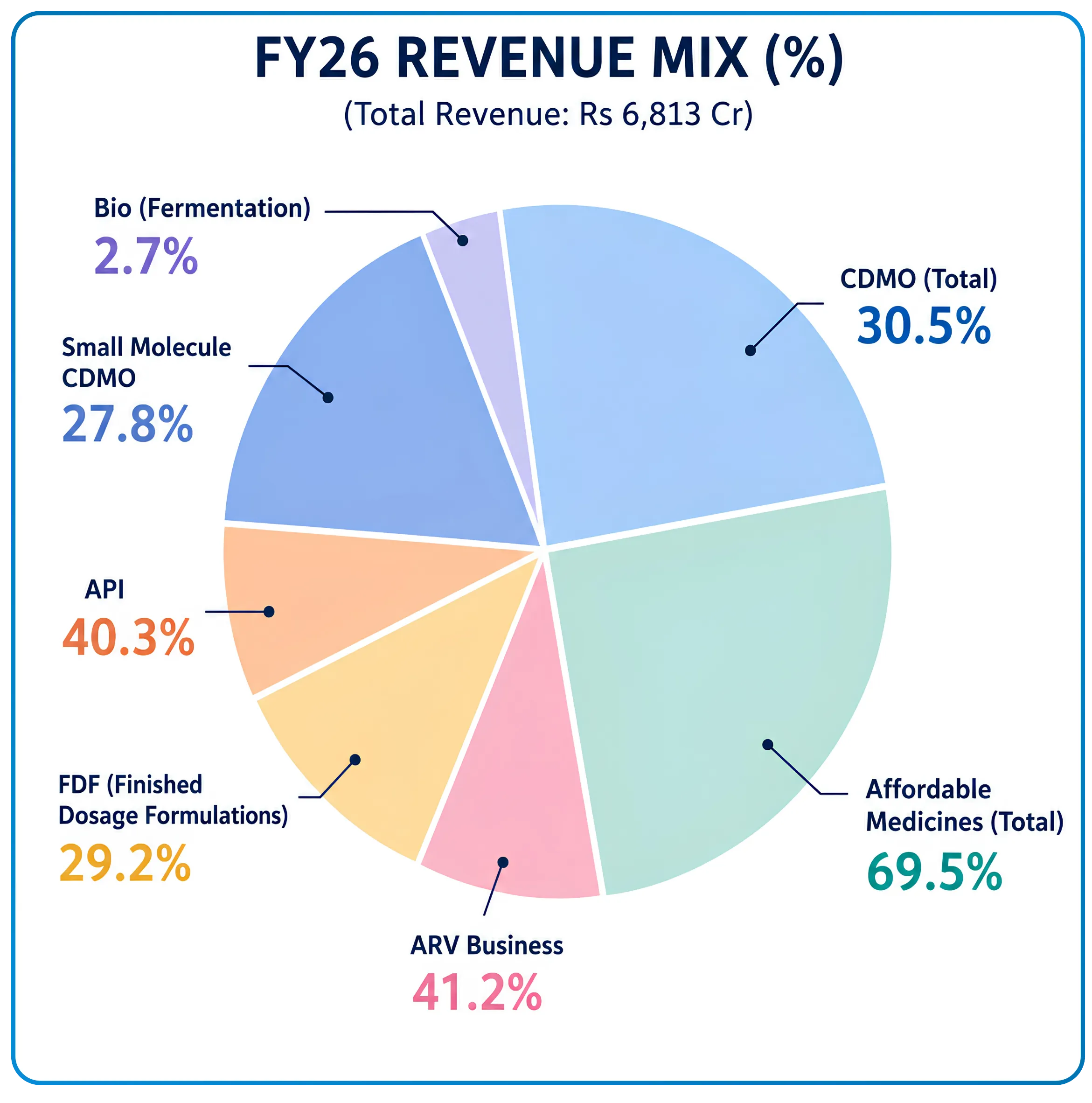

Divisional Performance

| Segment | FY26 Revenue (₹ cr) | YoY Growth | Revenue Mix |

|---|---|---|---|

| CDMO Total | 2,080 | +36% | 31% |

| Small Molecule CDMO | 1,896 | +38% | 28% |

| Bio (Fermentation) | 184 | +15% | 3% |

| Affordable Medicines Total | 4,733 | +18% | 69% |

| API | 2,746 | +13% | 40% |

| FDF | 1,987 | +26% | 29% |

| ARV (API + FDF combined) | 2,807 | +10% | 41% |

The CDMO business, where Laurus develops and manufactures ingredients for innovator pharmaceutical companies, grew 38% during the year. The primary driver was an increase in supplies of active pharmaceutical ingredients for newly approved drugs, three of which moved into full commercial production in the last 18 months. These products are still in the early stages of their commercial lives, meaning demand from innovator customers is expected to grow further as the drugs gain wider adoption in their respective markets.

The fermentation-based business, which produces biological ingredients used in medicines and other applications, contributed Rs 184 crore for the full year. While this remains a small part of the overall business, the Q4 number of Rs 65 crore was 124% higher than the same quarter last year, indicating that growth here is picking up pace.

On the generics side, the finished medicines business, which covers tablets and capsules sold to markets like the US and Europe, grew 26%, faster than the raw ingredient business which grew 13%. This reflects both the new capacity added during the year and approvals received for new products in regulated markets. The HIV medicines business, which is the largest single segment within generics, delivered Rs 2,807 crore, ahead of the Rs 2,500 crore the company had guided for, driven by full utilisation of manufacturing capacity. Medicine prices in this segment remained largely unchanged from the prior year.

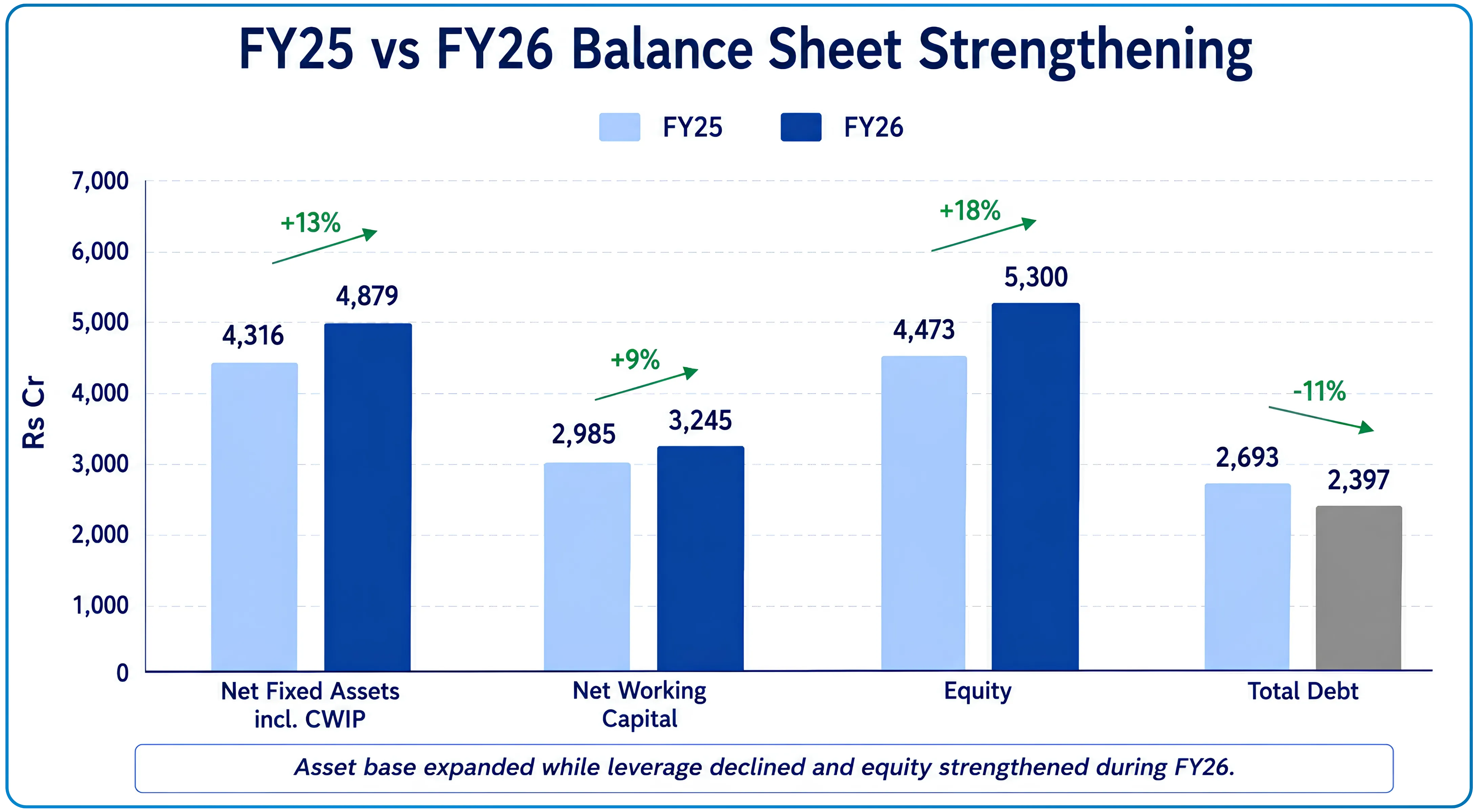

Laurus Labs Balance Sheet Improvement

| Metric | FY25 (₹ cr) | FY26 (₹ cr) | Change |

|---|---|---|---|

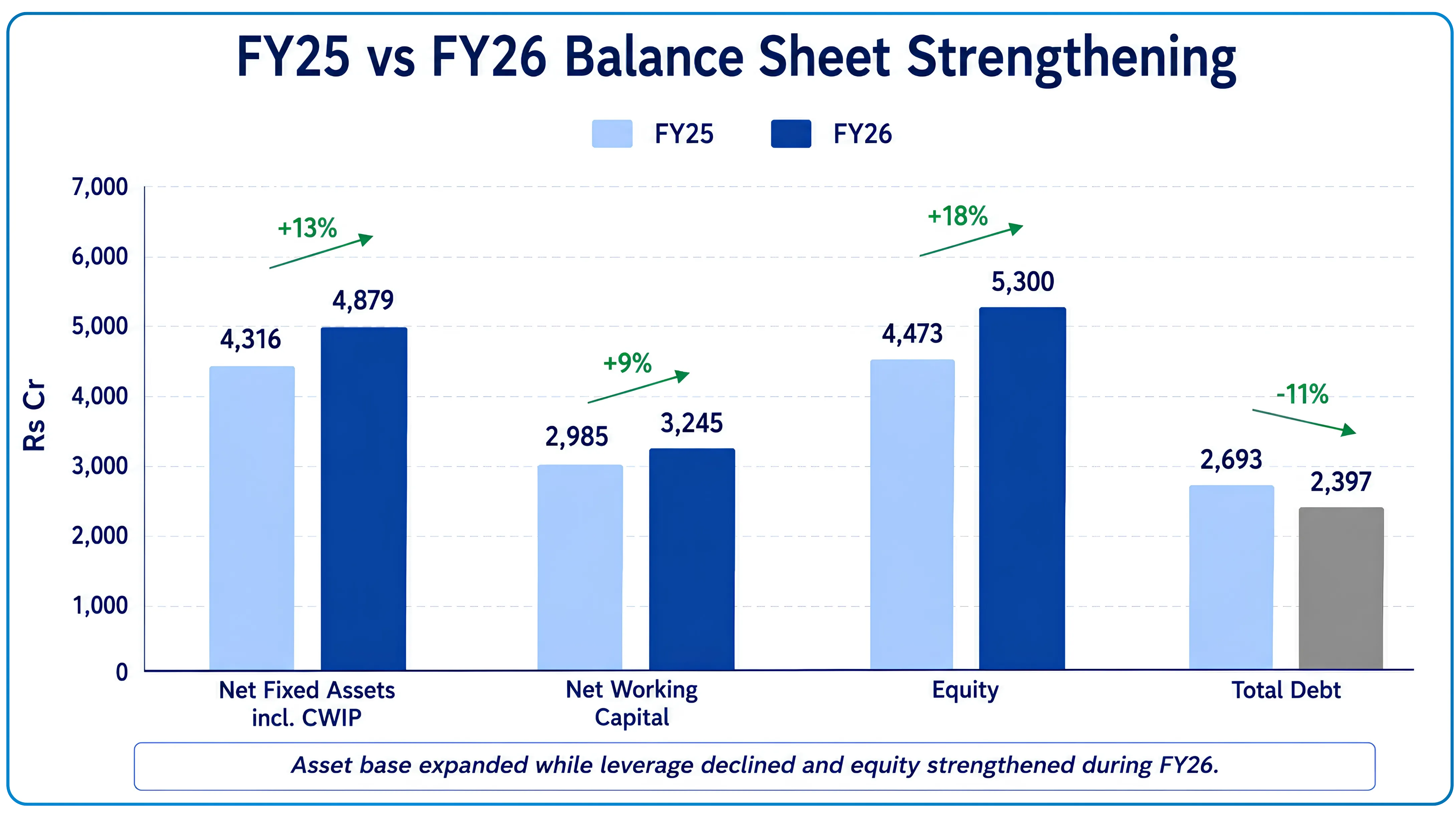

| Net Fixed Assets incl. CWIP | 4,316 | 4,879 | +563 |

| Net Working Capital | 2,985 | 3,245 | +260 |

| Inventories | 1,937 | 2,342 | +405 |

| Receivables | 2,007 | 2,155 | +148 |

| Payables | 959 | 1,252 | +293 |

| Total Debt | 2,693 | 2,397 | -296 |

| Equity | 4,473 | 5,300 | +827 |

The value of the company's physical assets, which includes its plants, equipment, and facilities under construction, grew by Rs 563 crore during the year. This reflects money spent on building the gene therapy and ADC lab in Hyderabad, expanding the finished medicines manufacturing lines, setting up commercial peptide production, and adding new chemical manufacturing blocks at Vizag.

The company is also holding more inventory and has slightly higher amounts owed to it by customers compared to last year. This is typical when a business is scaling up, as raw materials and work-in-progress tend to accumulate ahead of new capacity becoming fully operational.

On the debt side, total borrowings fell by Rs 296 crore to Rs 2,397 crore despite the company spending over Rs 1,000 crore on expansion during the year. This was possible because the business generated enough cash from its operations to fund a significant portion of the expansion without needing to borrow more.

Also Read: Samhi Hotels Limited - A Fundamental Analysis of the Turnaround Case

New Business Additions

Laurus Labs Gene Therapy and ADC

Laurus is building a new facility in Hyderabad for two advanced areas of medicine. The first is gene therapy, which involves treating diseases by modifying or replacing faulty genes in a patient's cells rather than using conventional medicines. The second is antibody-drug conjugates, or ADCs, which are a newer class of cancer treatments that deliver chemotherapy directly to cancer cells while minimising damage to healthy tissue. A research and development lab at this site has already been operational since December 2025. The full manufacturing facility, which will cost over Rs 200 crore to build, is expected to be ready by mid-2027. Laurus has also taken a stake in Aarvik Therapeutics, a company specialising in ADC development, to strengthen its capabilities in this area. This is a meaningful departure from Laurus's traditional business of manufacturing chemical ingredients for medicines, and how well the company executes here is worth watching independently of its core performance.

Laurus Labs CAR-T Through ImmunoACT

Through its associate company ImmunoACT, Laurus is involved in CAR-T cell therapy, a form of cancer treatment where a patient's own immune cells are extracted, genetically modified in a laboratory to recognise and attack cancer cells, and then reinfused into the patient. The company's treatment NexCAR19 targets blood cancers, and the number of patients treated doubled year-on-year. A new manufacturing facility in Nerul, Mumbai, commissioned in March 2026, has tripled annual treatment capacity from 600 to 2,500 patients. A partnership with Cipla to offer NexCAR19 in African markets has also been announced. Trials are underway for a second therapy targeting multiple myeloma, a type of blood cancer. Revenues from this business were Rs 75 crore in FY26, small relative to the overall company but representing Laurus's most direct bet on the future of medicine.

Laurus Labs Fermentation Expansion at Vizag

Fermentation, in a pharmaceutical context, is the process of using microorganisms like bacteria or yeast to produce biological substances used in medicines, nutrients, and industrial applications. Laurus Bio, the company's fermentation business, currently operates out of Bangalore where all available capacity is fully utilised. To meet growing demand, the company is building a much larger fermentation facility in Vizag. The first phase, which adds capacity roughly equivalent to 1.6 times what currently exists in Bangalore, is expected to be ready by end of 2026. To reduce the risk of contamination during the initial period, the new facility will first be used to produce non-pharmaceutical products such as industrial chemicals before transitioning to pharmaceutical-grade production.

Laurus Labs Capex Pipeline FY27 and Beyond

The table below summarises the key expansion projects underway, where they are located, and when they are expected to be ready. Most of these are large-scale manufacturing facilities being built simultaneously across Vizag and Hyderabad, representing the most aggressive expansion phase in the company's history.

| Project | Location | Milestone | Timeline |

|---|---|---|---|

| Unit 7 Greenfield API Plant | Vizag | First commercial validation | March 2027 |

| Four additional API blocks (2,000+ kL) | Vizag | Operational | FY28 |

| Commercial Peptide Block | Vizag | Ready for validation | Q2 FY27 |

| Laurus Bio Fermentation Phase 1 (400 kL) | Vizag | Operational | End CY2026 |

| KRKA JV Formulations Facility | Hyderabad | Phase 1 completion | Mid-2027 |

| Gene Therapy and ADC cGMP Facility | Hyderabad | Commissioning | Mid-2027 |

| 532-Acre Greenfield Campus | Vizag | Capex begins | End-FY27 |

To put the scale of this expansion in context, the company is currently generating roughly 89 paise in revenue for every rupee of assets it owns. Historically, Laurus has averaged above one rupee in revenue per rupee of assets. Closing that gap depends on the new facilities coming online and reaching their production targets on schedule.

Laurus Labs Management Guidance FY27

Going into FY27, the company's leadership has stated that they expect to at least maintain the profit margins achieved in the final quarter of FY26, if not improve on them. On raw material costs, the management acknowledged some pressure from rising solvent prices, which are chemicals used in the manufacturing process, but said this is unlikely to affect production volumes in the near term.

The HIV medicines business is expected to continue generating around Rs 2,800 crore annually, but its share of total revenues will gradually reduce as the CDMO business grows faster. On borrowings, while the company may take on slightly more debt in FY27 to fund its expansion, management expects the overall debt burden relative to earnings to remain manageable or improve further.

The longer-term target is for the CDMO business to account for half of total revenues by 2030. It currently stands at 31%, so achieving that target over four years would require the division to grow considerably faster than the rest of the business, which is broadly what the current capex programme is designed to enable.

Risks

A few areas merit attention from an investor's perspective.

On raw materials, certain chemicals used in the manufacturing process have seen price increases recently, which puts some pressure on margins in the near term. The company has confirmed there are no supply disruptions currently, but its visibility on uninterrupted supply extends only to end-June 2026. Beyond that, global trade tensions and logistics disruptions remain an unpredictable variable.

The CDMO business, while growing strongly, carries a concentration risk that is worth understanding. A significant portion of its revenues currently comes from just three newly commercialised drug ingredients. These are products where Laurus supplies the active ingredient to an innovator pharmaceutical company for a drug that has recently been approved and launched. If any of these drugs were to face a clinical issue, a slowdown in patient demand, or if the innovator company were to reduce its order quantities, the impact on Laurus's CDMO revenues could be disproportionate. Management has stated there is no such risk currently visible, but it is an area to watch quarter by quarter.

The HIV medicines business faces a longer-term structural question. A newer form of HIV treatment, involving monthly or bi-monthly injections rather than daily tablets, is gradually being adopted in some markets. Laurus currently only makes tablet-based HIV medicines and does not manufacture injectable formulations. The shift toward injectables is happening slowly due to practical challenges around patient compliance and healthcare infrastructure, but if adoption accelerates, it could affect the long-term demand for Laurus's oral HIV medicines.

Finally, the company is simultaneously building multiple large facilities across Vizag and Hyderabad while also entering entirely new areas like peptides, fermentation, and gene therapy. Executing all of this in parallel without delays is a significant operational challenge. The company's ability to recover its historical efficiency levels depends on these facilities coming online and generating revenues on schedule.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.