Established as a Oval Projects Engineering private Limited is an infrastructure services company engaged in providing engineering, procurement, and construction (EPC) as well as operations and maintenance (O&M) solutions in the oil and gas sector. Incorporated in 2013 and headquartered in Agartala, Tripura, the company has built a strong reputation for executing complex projects across India.

Oval Projects caters to both public-sector undertakings and private clients, delivering turnkey solutions that span design, procurement, construction, and ongoing operations. Over the years, the company has completed multiple large-scale projects and built a reputation for timely delivery, safety standards, and engineering excellence.

With an expanding presence across the oil & gas value chain, the company today plays an important role in India’s push for clean energy, city gas expansion, and industrial infrastructure development.

IPO details

| Particulars | Details |

|---|---|

| IPO Type | BSE SME (Book Built Issue) |

| Fresh Issue | 54,99,200 equity shares |

| Face Value | ₹10 per share |

| Price Band | To be announced |

| Lot Size | To be announced |

| Issue Opens | August 28, 2025 |

| Issue Closes | September 01, 2025 |

| Allotment Date | To be announced |

| Listing Date | Proposed on BSE SME |

| Market Maker | SMC Global Securities Ltd |

| Registrar | MAS Services Ltd |

Use of Proceeds – Fresh Issue Allocation

| Purpose | Amount (₹ crore) |

|---|---|

| Long-term working capital | 37.03 |

| General corporate purposes | Balance (≤15% of net proceeds) |

| Total | 100% of IPO proceeds |

Business model

| Segment | Activities | Revenue Type | Clients |

|---|---|---|---|

| EPC Projects (Primary Revenue Driver) | Design, procurement & construction of pipelines (CGD & cross-country) - Setting up CNG stations, terminals & related infra - Turnkey execution: engineering → procurement → construction → commissioning | One-time, project-based revenue | PSUs, private oil & gas companies |

| Operations & Maintenance (O&M) | Long-term contracts for pipeline & CGD maintenance - Preventive maintenance, manpower supply, monitoring & safety services | Recurring, stable income | Gas distribution companies, refineries |

| Civil & Industrial Infrastructure | Specialized civil works - Infrastructure support for oil & gas & urban development projects | Supplementary revenue | Industrial & infra clients |

| Client Base | Primarily government entities (90%+) - Select private sector contracts | Mix of stable govt projects & competitive private sector contracts | Public sector undertakings (PSUs), private EPC clients |

| Order Book Driven Model | Revenue linked to execution of ~₹4,530 crore order book (as of Apr 2025) - Multi-year visibility with milestone-based payments | Ensures predictable pipeline but cash flows depend on project timelines | Government contracts, large EPC projects |

Also read : Tata Communications ambitious digital transformation story

Industry Overview

Oval Projects Engineering Limited operates in the oil & gas EPC (Engineering, Procurement & Construction) and infrastructure services industry, which plays a critical role in India’s energy and urban development ecosystem.

Market Size & Growth

The Indian oil & gas EPC sector has witnessed steady growth, expanding at a CAGR of nearly 10% over the last five years. With India targeting to increase the share of natural gas in its energy mix from about 6% at present to 15% by 2030, the industry is poised for significant expansion. This transition is expected to generate large-scale opportunities in pipeline infrastructure, city gas distribution (CGD), and CNG networks. In fact, investments worth an estimated ₹1.5–2 lakh crore are projected in CGD networks alone over the coming decade, highlighting the sector’s strong growth potential and government-backed momentum.

Key Demand Drivers

India’s oil & gas sector is being reshaped by multiple demand drivers. Urbanization and the clean energy transition are fueling a steady rise in demand for piped natural gas (PNG) and compressed natural gas (CNG) as cleaner alternatives to LPG and conventional fuels. Strong government initiatives, including the expansion of CGD licenses across more than 400 districts and mega projects such as the North East Gas Grid and JHBDPL (Urja Ganga) pipeline, are creating large-scale infrastructure opportunities. At the same time, the automotive sector’s shift towards CNG vehicles is driving the need for additional filling stations nationwide. Furthermore, ongoing refinery and petrochemical capacity expansion—through modernization and new units—aims to meet both domestic consumption and export demand, strengthening the long-term growth prospects of the sector.

Sector Trends

The Indian oil & gas EPC sector is witnessing a massive infrastructure push, with cross-country pipelines and CGD projects forming the core of the government’s energy policy. This momentum is being reinforced through public-private partnerships (PPPs), where PSUs such as GAIL, IOCL, and BPCL are working alongside private players to accelerate the development of gas distribution and pipeline infrastructure. At the same time, EPC outsourcing is gaining traction as large oil & gas companies increasingly rely on specialized contractors like Oval Projects for project execution, ensuring cost efficiency and timely delivery. Additionally, there is a growing focus on safety, quality, and compliance, with higher emphasis on adhering to environmental standards and operational best practices across infrastructure development.

Industry Challenges

Despite strong growth prospects, the oil & gas EPC sector faces several challenges. The industry is characterized by high working capital intensity, with EPC players often dealing with delayed payments and significant cash flow pressures. There is also a persistent execution risk, as project delays, cost overruns, and logistical hurdles are common in large-scale infrastructure works. Moreover, the sector remains heavily policy-dependent, with growth closely tied to government investments, licensing rounds, and regulatory frameworks. These factors make financial discipline, operational efficiency, and diversified client exposure critical for companies operating in this space.

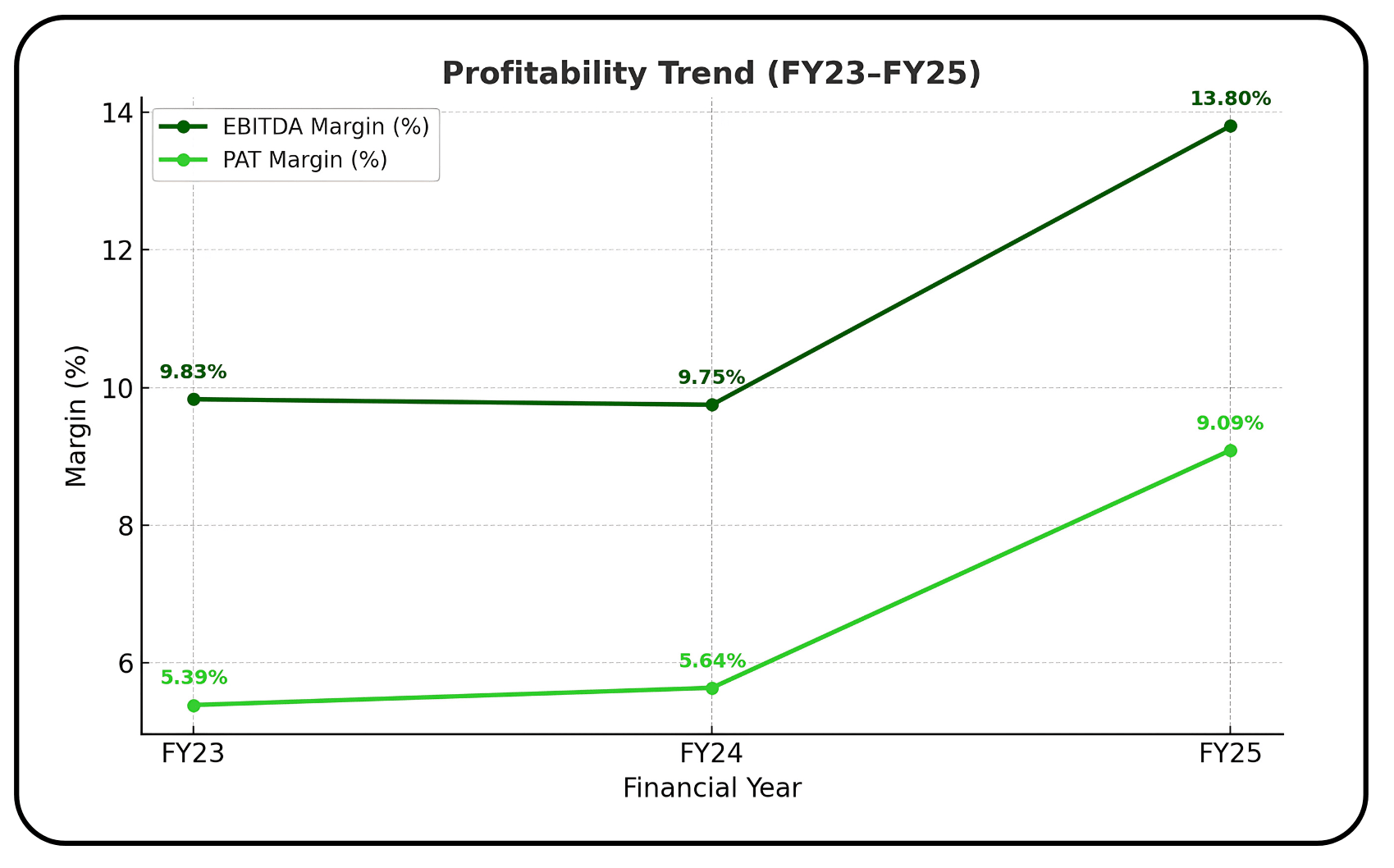

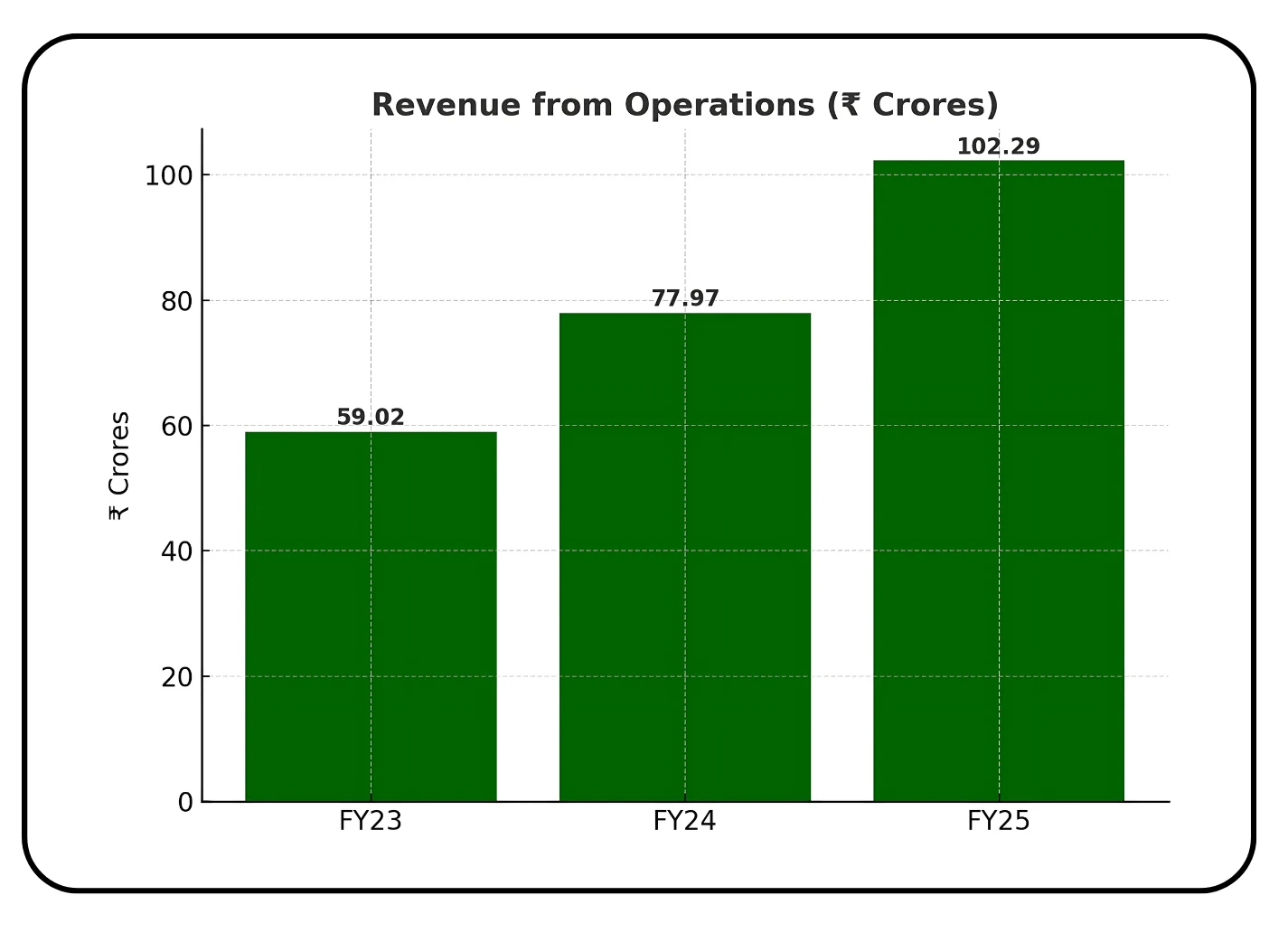

Financials (₹ in Crores)

| Particulars | FY23 | FY24 | FY25 | CAGR / Trend |

|---|---|---|---|---|

| Revenue from Operations | 59.02 | 77.97 | 102.29 | 31.6% CAGR |

| Total Income | 64.09 | 78.99 | 103.44 | Rising steadily |

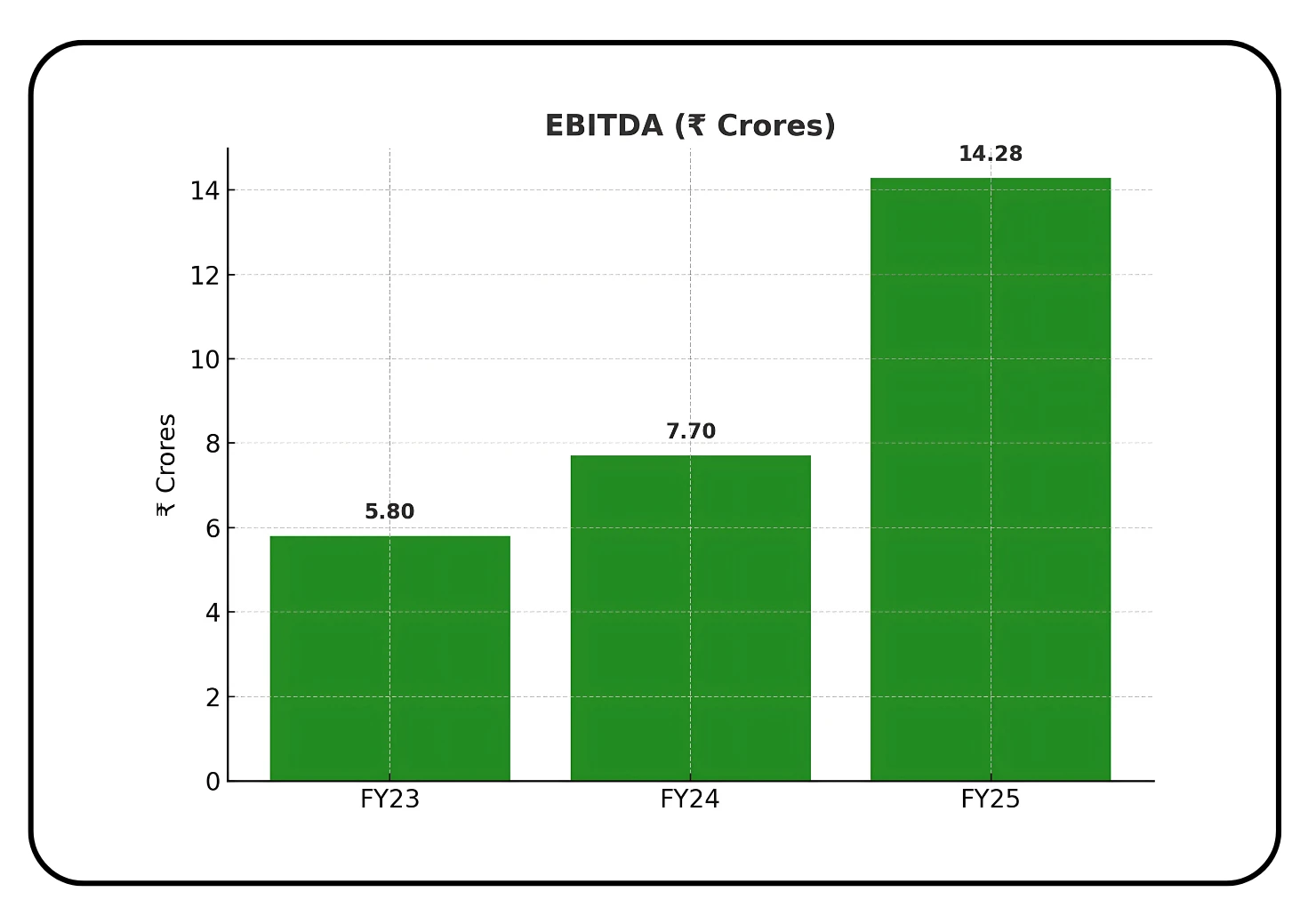

| EBITDA | 5.80 | 7.70 | 14.28 | Strong jump in FY25 |

| EBITDA Margin (%) | 9.83% | 9.75% | 13.80% | Improved |

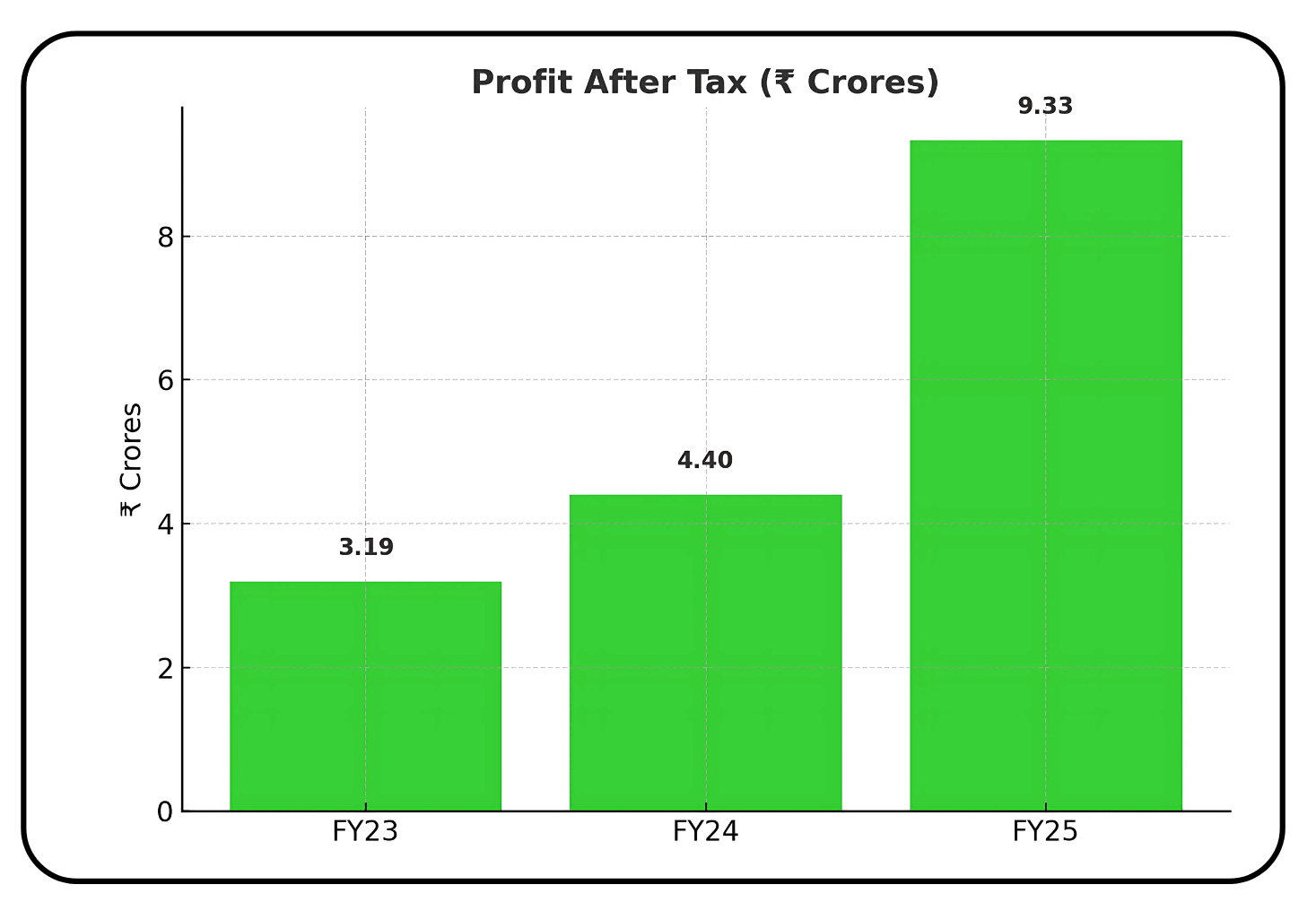

| Profit After Tax (PAT) | 3.19 | 4.40 | 9.33 | Nearly 3x in 3 yrs |

| PAT Margin (%) | 5.39% | 5.64% | 9.09% | Improving |

| Net Worth | 17.75 | 33.67 | 55.88 | Strengthened |

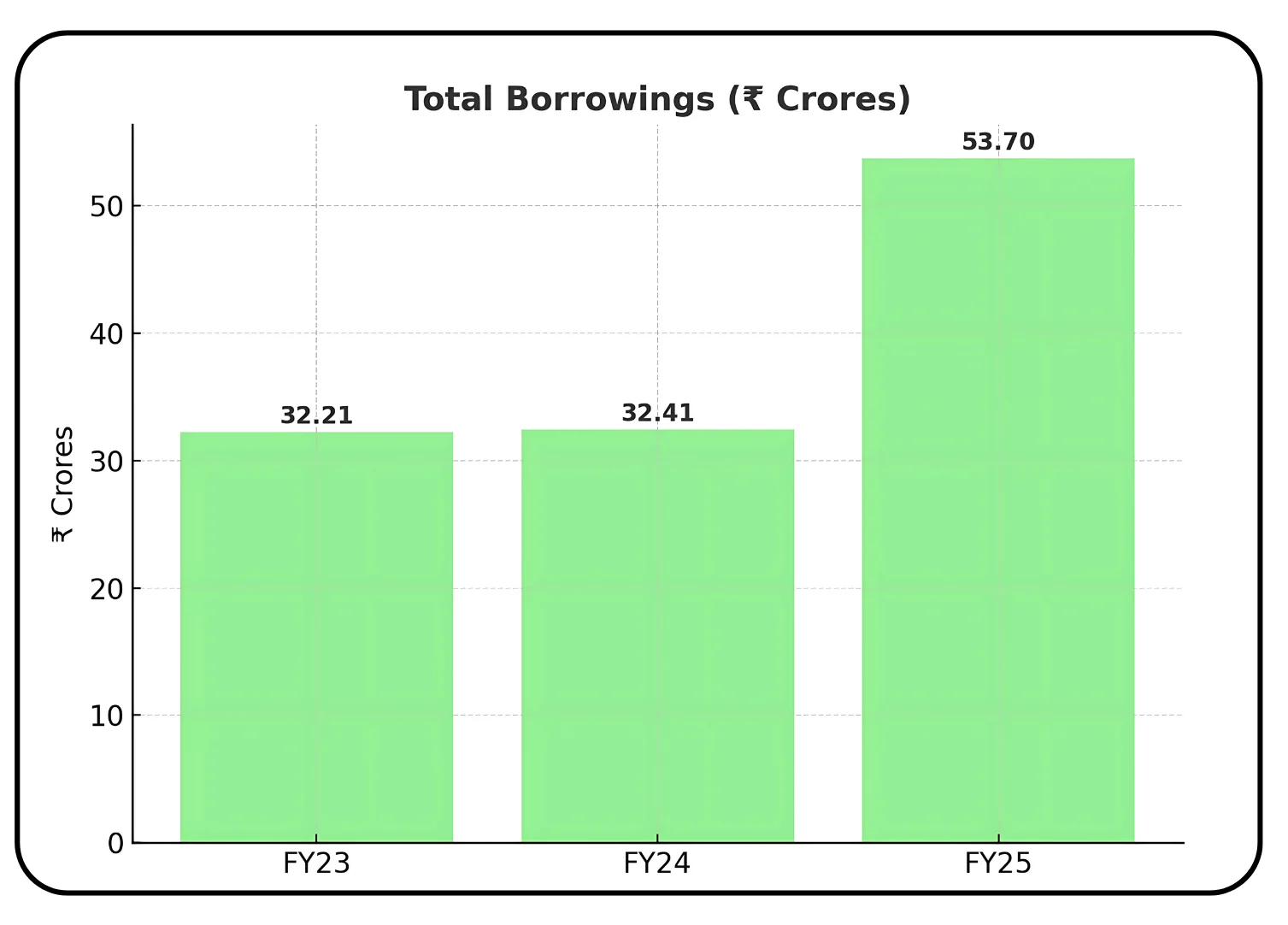

| Total Borrowings | 32.21 | 32.41 | 53.70 | Rising debt |

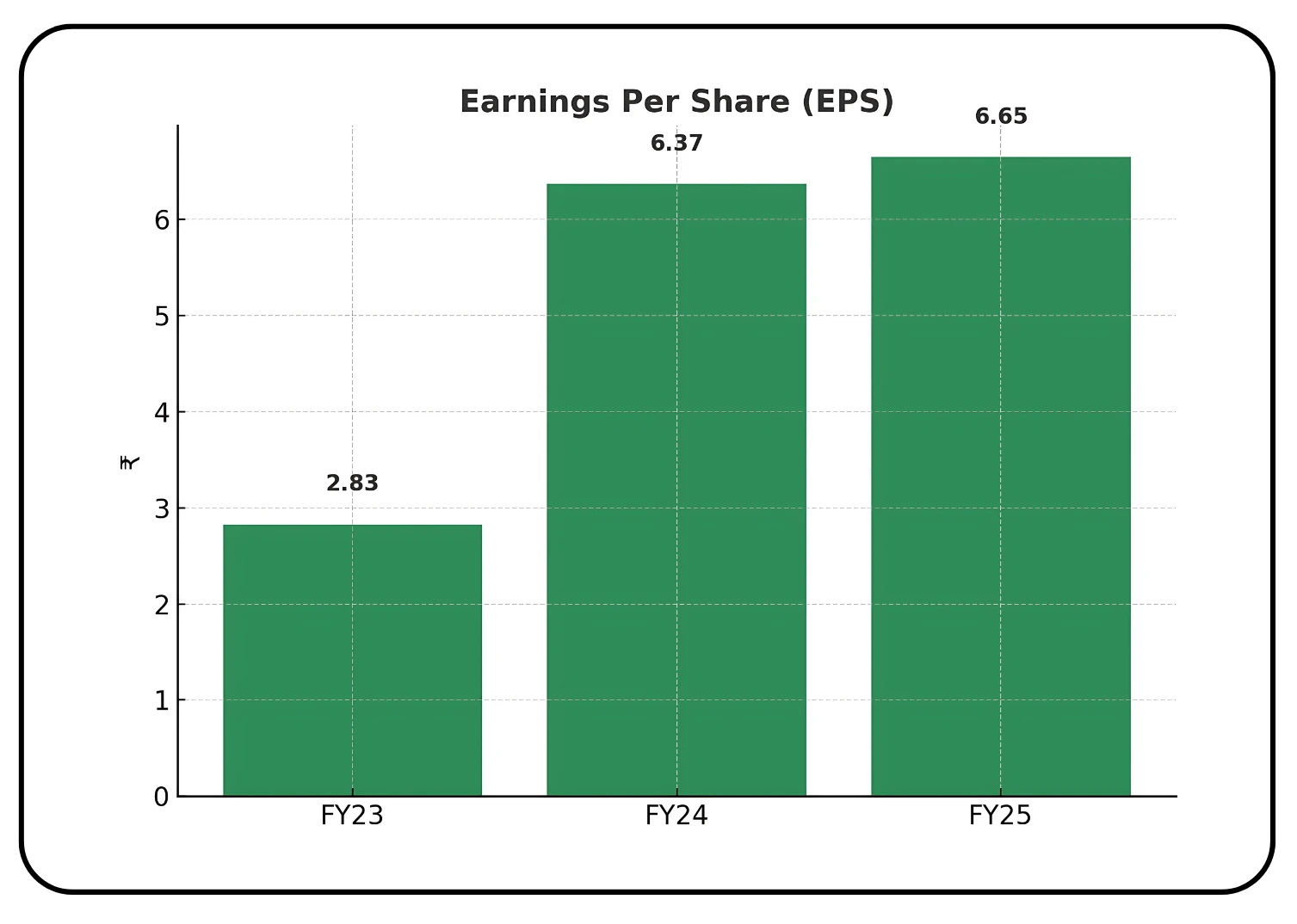

| EPS (₹) | 2.83 | 6.37 | 6.65 | Stable |

| RoNW (%) | 19.71% | 17.12% | 20.85% | Healthy returns |

Revenue from Operations

Oval Projects’ revenue grew from ₹59.02 crore in FY23 to ₹102.29 crore in FY25, reflecting a strong CAGR of ~32%. This growth highlights the company’s expanding project execution capacity and rising order book.

EBITDA

EBITDA increased from ₹5.80 crore in FY23 to ₹14.28 crore in FY25, showing operational scale benefits. Margins improved to 13.8% in FY25, indicating better cost efficiency.

Profit After Tax (PAT)

PAT nearly tripled from ₹3.19 crore in FY23 to ₹9.33 crore in FY25, with profitability strengthening year-on-year. PAT margins improved from 5.39% to 9.09%, reflecting healthier bottom-line performance.

Borrowings

Total borrowings rose from ₹32.21 crore in FY23 to ₹53.70 crore in FY25, underlining the working-capital-intensive nature of the EPC business. While leverage supports growth, it also adds financial risk.

Earnings Per Share (EPS)

EPS improved from ₹2.83 in FY23 to ₹6.65 in FY25, aligning with rising profitability. The trend shows consistent value creation for shareholders, though future dilution depends on IPO pricing.

Strengths

- Strong order book (₹4,530 crore) with visibility.

- Proven expertise in oil & gas EPC projects.

- High demand drivers: CGD, CNG, and refinery expansion.

- Consistent revenue and profitability growth.

- Experienced promoters with domain expertise.

Also read : Ajax Engineering A Strong Play on India’s Infrastructure Mechanisation

Peer comparison

According to the RHP, Oval Projects Engineering has identified listed peers in the infrastructure & EPC space for benchmarking.

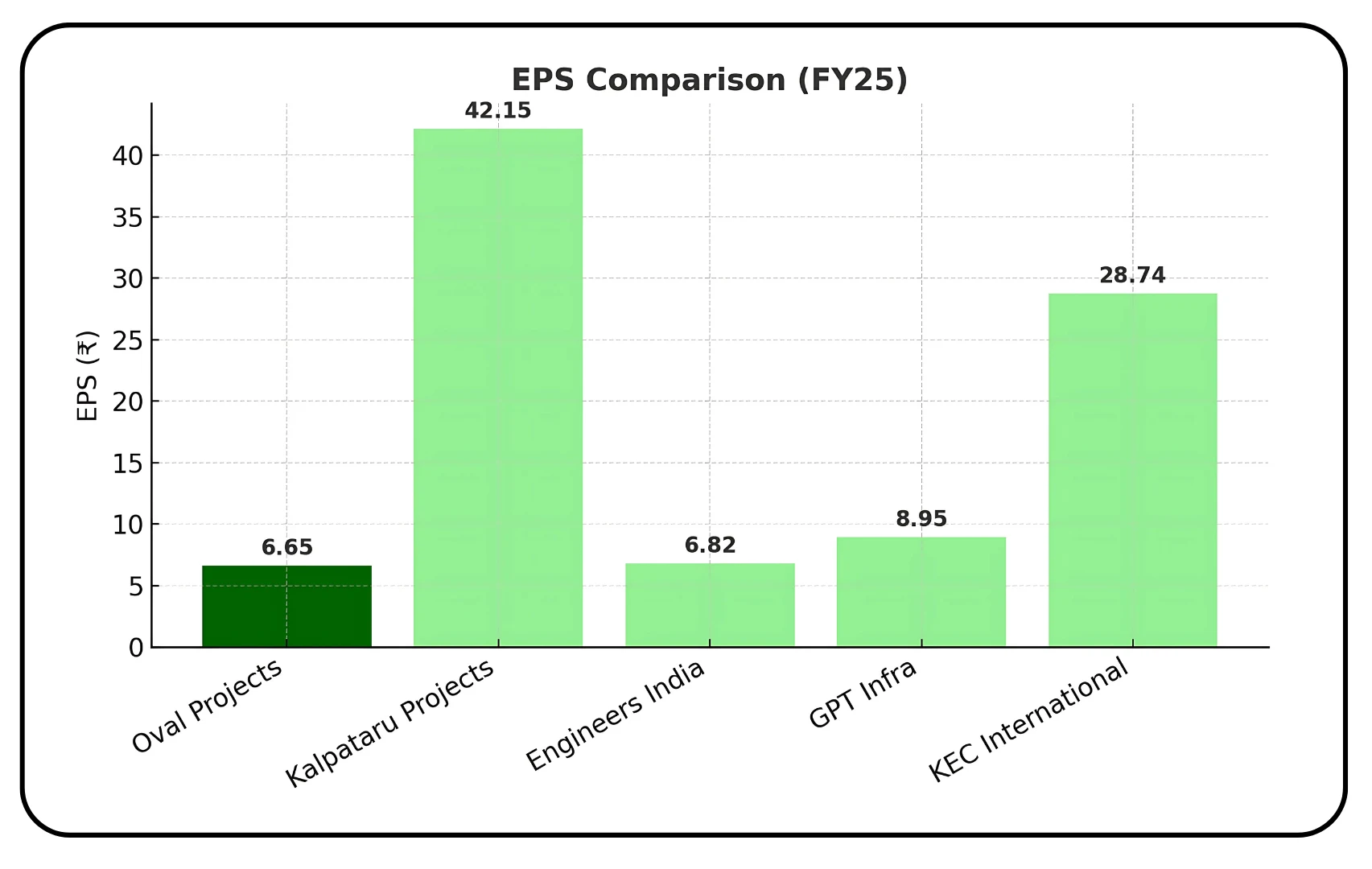

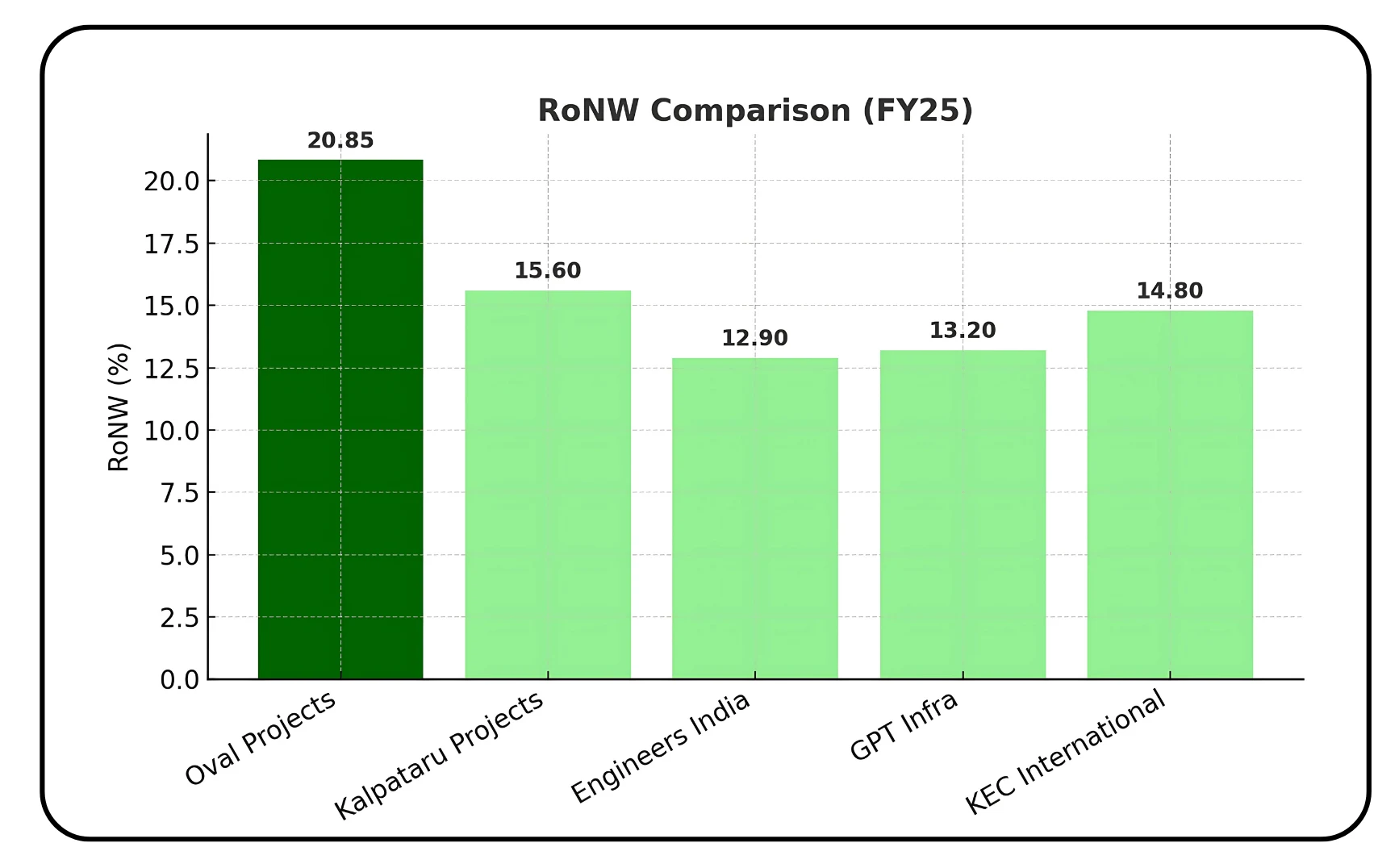

| Company | Revenue (₹ Cr) FY25 | EPS (₹) FY25 | RoNW (%) | NAV (₹) | P/E (at CMP) |

|---|---|---|---|---|---|

| Oval Projects | 102.29 | 6.65 | 20.85 | 31.89 | To be announced |

| Kalpataru Projects International Ltd | 19,075+ | 42.15 | 15.6 | 310.4 | 18.2x |

| Engineers India Ltd | 4,820+ | 6.82 | 12.9 | 58.6 | 24.7x |

| GPT Infraprojects Ltd | 1,050+ | 8.95 | 13.2 | 72.1 | 16.5x |

| KEC International Ltd | 21,000+ | 28.74 | 14.8 | 185.6 | 21.3x |

(Peer financials taken from FY25 results disclosed in RHP and public filings. EPS and RoNW are annualized for comparability.)

EPS Comparison

Oval Projects reported an EPS of ₹6.65 in FY25, which is comparable to Engineers India (₹6.82) and GPT Infra (₹8.95), despite being much smaller in scale. Larger players like Kalpataru and KEC deliver higher EPS in absolute terms, but Oval Projects holds its ground well among peers.

RoNW Comparison

Oval Projects delivered a RoNW of 20.85%, higher than all listed peers including Kalpataru (15.6%) and KEC (14.8%). This indicates superior capital efficiency and effective utilization of equity compared to industry standards.

Profitability Trend (FY23–FY25)

Oval Projects EBITDA margin improved from ~9.8% in FY23 to 13.8% in FY25, reflecting stronger cost efficiency and scale benefits. The PAT margin also rose from 5.4% to 9.1%, showing clear bottom-line improvement.

Risks

- 90%+ dependency on government contracts → concentration risk.

- Working capital-intensive business with rising debt.

- Negative operating cash flows in recent years.

- Vulnerable to execution delays & cost overruns.

- Sector concentration: primarily oil & gas infra.

Also read : Vigor Plast India IPO overview

Conclusion

Oval Projects Engineering Limited has established itself as a growing player in the oil & gas EPC and infrastructure services sector, with a strong order book, consistent revenue growth, and improving profitability. Its expertise in pipeline projects, CGD networks, and CNG station development positions it well to benefit from India’s energy transition and urban infrastructure push.

On the flip side, the business is working-capital heavy, with rising borrowings and dependence on government contracts posing potential risks. Execution challenges and policy-linked growth add to the uncertainties.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.

%252FAnalysis%2520of%2520FII%2520Positioning%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D1405f6f4-6738-4f13-99c7-288e6fede0b6&w=3840&q=75)

%2520Every%2520Trader%2520Should%2520Know%252FCAS%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D397e2566-b93f-4420-b41d-378b1483f837&w=3840&q=75)