PG Electroplast Limited (PGEL), the flagship of the PG Group, established in 1977, has evolved into one of India’s leading Electronic Manufacturing Services (EMS) and Original Design Manufacturing (ODM) companies. It provides end-to-end solutions spanning plastic injection molding, Printed Circuit Board Assembly (PCBA), product assembly, and backward integration for over 70 Indian and global brands.

Operating across 11 manufacturing units in Greater Noida, Ahmednagar, Bhiwadi, and Roorkee, PGEL has built a strong foothold in high-growth verticals such as air conditioners, washing machines, coolers, televisions, and automotive components.

Business model

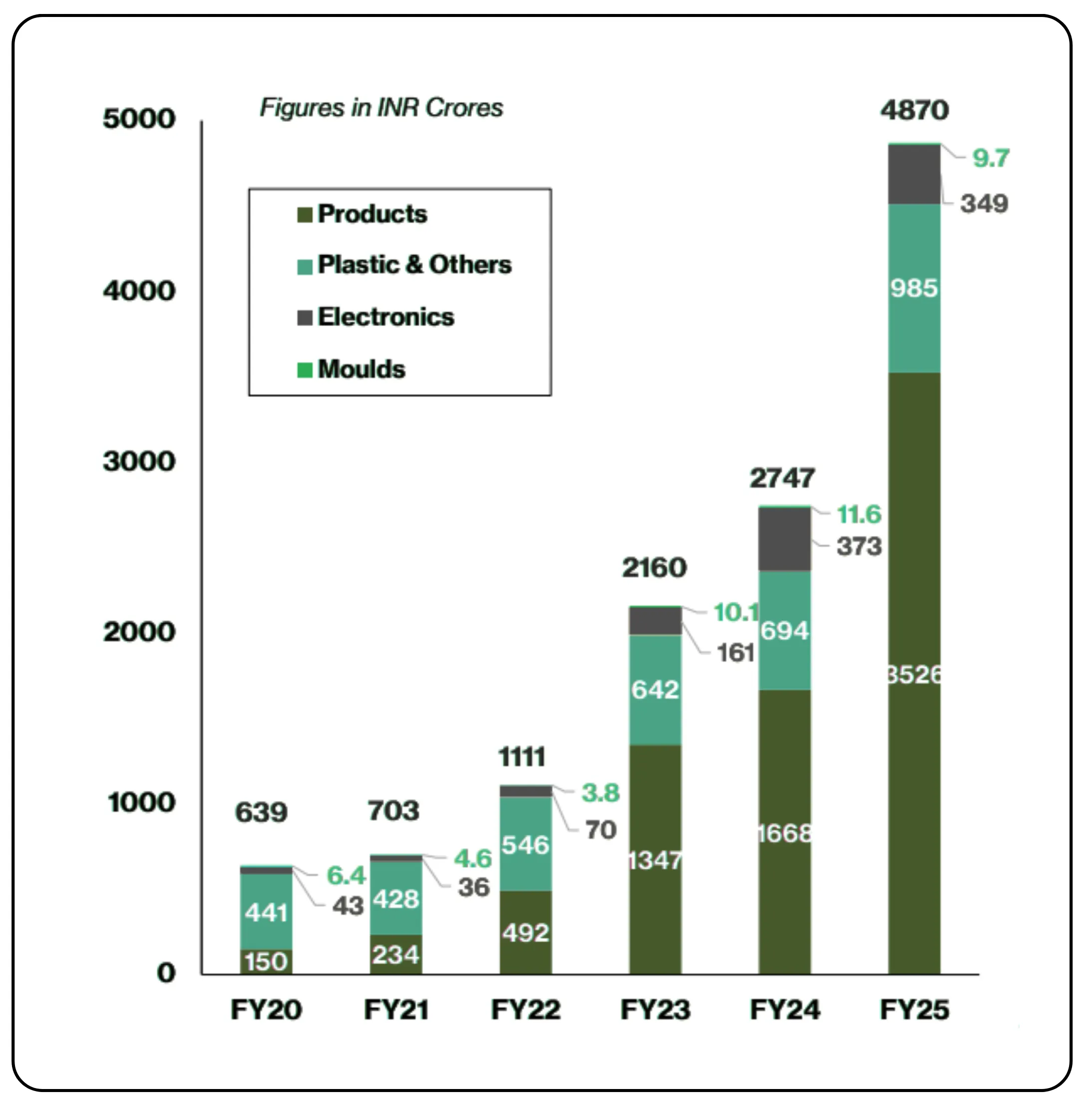

PGEL’s core business comprises three segments:

- Product business (ODM/OEM): Covers Room Air Conditioners (RACs), Washing Machines, and Air Coolers. This is the key revenue driver, contributing over 72% of total operating revenue in FY25.

-Electronics manufacturing: Includes PCB assemblies, LED TVs, and other consumer electronics.

- Plastic molding & others: Supplies precision plastic components to clients across sectors.

The company operates primarily in a B2B model, where it builds products for well-known brands (like LG, Blue Star, Godrej, Haier, etc.) across both offline and online retail channels. It benefits from long-term partnerships, rising outsourcing trends, and large-scale manufacturing efficiencies, particularly in consumer appliances and electronics.

| Year | Sales (₹ Cr) | Operating Profit (₹ Cr) | Net Profit (₹ Cr) |

|---|---|---|---|

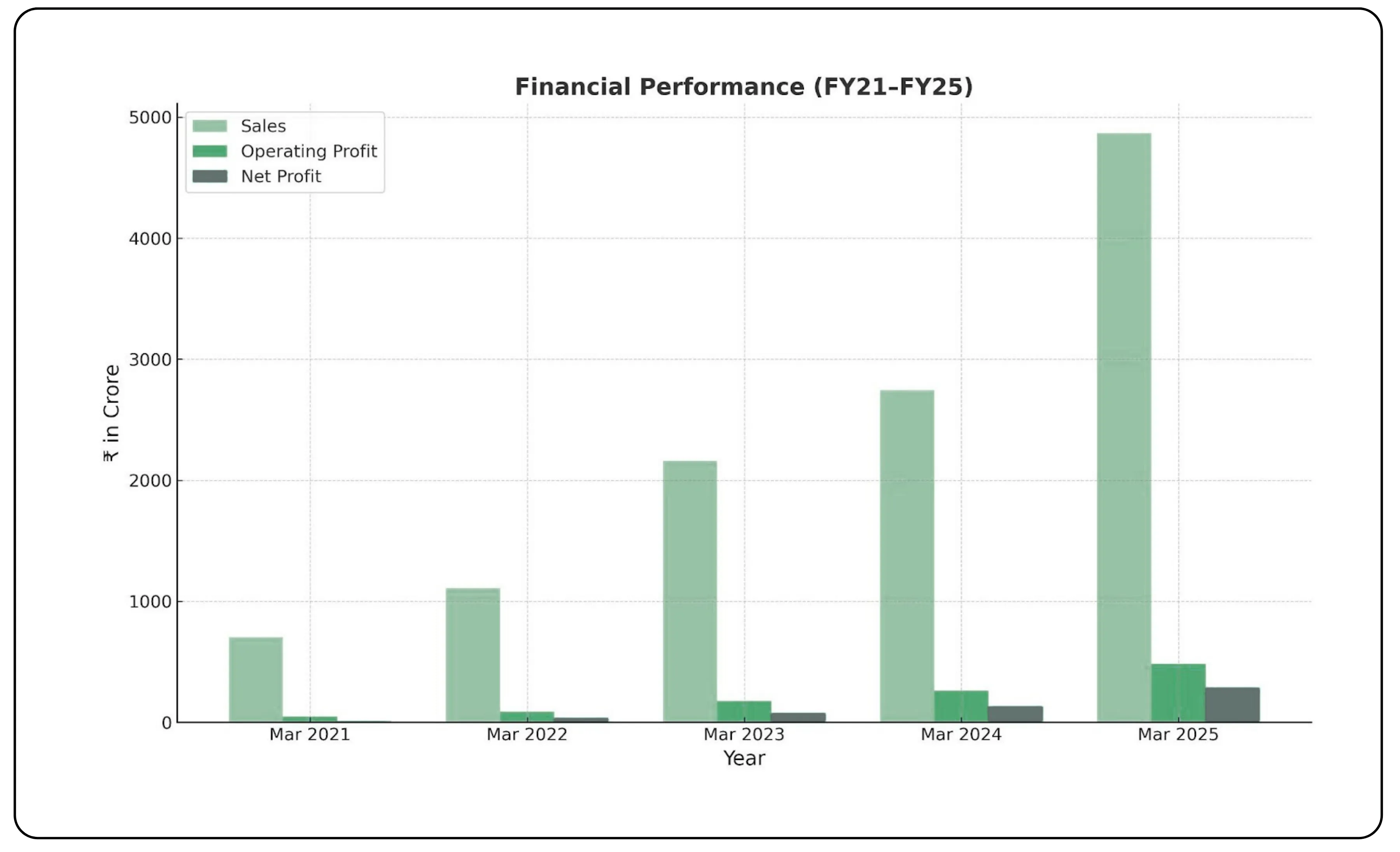

| Mar-25 | 4,870 | 484 | 288 |

| Mar-24 | 2,746 | 262 | 135 |

| Mar-23 | 2,160 | 177 | 77 |

| Mar-22 | 1,112 | 89 | 37 |

| Mar-21 | 703 | 50 | 12 |

FY25 Highlights:

Revenue: ₹4,870 crore (↑77% YoY)

EBITDA: ₹519 crore (↑89% YoY); EBITDAmargin improved to 10.7%

PAT: ₹291 crore (↑112% YoY)

Product business revenue: ₹3,526 crore (↑111% YoY)

- Air Conditioners: ₹3,009 crore (↑128%)

- Washing Machines: ₹448 crore (↑43%)

- Air Coolers: ₹448 (↑80%)

Net fixed asset turn: (Net sales/Net fixed assets) 5.08x, reflecting superior asset utilization

Net Cash: ₹980 crore; the company is now debt-free on a net basis

Guidance for FY26:

- Revenue: ₹6,345 crore (↑30%)

- Group revenue (including JV Goodworth): ₹7,200 crore (↑33%)

- Net Profit: ₹405 crore (↑39%)

- Product business expected to grow 35% to ₹4,770 crore

Also read: Engineering Defense Growth with CFF Fluid Control Ltd.

Industry outlook

Urbanization and Rise of Middle-Class Consumption:

India's urban population is experiencing rapid growth, with over 500 million people already residing in urban areas. Projections indicate that more than 40% of the population will be urban by 2030, with 70% of the GDP expected to originate from these regions. This rapid urbanization, coupled with rising disposable incomes, is a primary driver of increased consumption.

The Union Budget 2025 has introduced measures to bolster India's middle class, which is estimated to comprise over 560 million people across 126 million households (earning between ₹6 lakh and ₹36 lakh annually at 2024-25 prices). This segment is a major force behind consumption, investment, and innovation. Tax relief measures, such as income tax exemption for individuals earning up to ₹12 lakh annually, are designed to boost disposable incomes and fuel demand for consumer goods, automobiles, and housing. The middle-class population, earning between INR 2 and 10 lakh, is projected to reach 128 million by the end of 2025, accounting for 41% of the population.

Low Penetration of ACs, Washing Machines, and Refrigerators:

Despite the growing middle class, the penetration of certain consumer durables remains relatively low, indicating significant growth potential:

Air Conditioners (ACs): The Indian room air conditioner market, valued at USD 3.88 billion in 2024, is expected to reach USD 13.43 billion by 2033, growing at a robust CAGR of 14.78% from 2025-2033. Currently, urban household penetration of ACs is around 7-9%, significantly lower compared to over 90% in developed countries like the US. This low penetration, combined with increasing temperatures and urbanization, is a key growth driver. ICRA projects the Indian room air-conditioner industry volumes to grow by 8-10% year-on-year to reach 9.6-9.8 million units in FY2025.

Washing Machines: The India Washing Machine market, valued at USD 1.66 billion in 2024, is anticipated to grow at a CAGR of 7.62% through 2030. Urbanization, rising disposable incomes, and changing consumer lifestyles are driving this growth, as washing machines become essential for efficient laundry care, moving away from traditional hand washing. There's also a notable shift from semi-automatic to fully automatic machines.

Refrigerators: The Indian refrigerator market is projected to grow from USD 2.92 billion in FY2024 to USD 6.70 billion in FY2032, at a CAGR of 10.91% during FY2025-FY2032. While urban areas are the primary market with over 70% penetration, rural India still has penetration below 25%, representing a vast untapped market. Rising rural incomes and government schemes are making refrigerators more accessible.

Government Initiatives Encouraging Domestic Manufacturing:

The Indian government's proactive initiatives are significantly boosting domestic manufacturing:

Make in India: This flagship program aims to make India a global manufacturing hub. The manufacturing sector's contribution to GDP is estimated to be around 13-14% in 2025, with an ambition to reach 25% in the coming years. The initiative has encouraged both foreign and Indian investment in the secondary sector and is creating jobs.

Production Linked Incentive (PLI) Scheme: Under the PLI scheme for 14 key sectors, 764 applications have been approved, including 176 MSMEs. The scheme has incentivized domestic manufacturing, leading to increased production, job creation, and a boost in exports.

Investments and Production: The PLI scheme has attracted substantial investments, with 84 companies under the PLI Scheme for White Goods (ACs and LED Lights) committing investments of ₹10,478 crore. Overall, the PLI scheme has clocked ₹1.61 lakh crores in investment and ₹14 lakh crores in production.

Export Growth and Import Substitution: India's electronics manufacturing sector has transformed from a net importer to a net exporter of mobile phones under the PLI scheme. Electronics exports increased by 20% between 2021 and 2023. India has also achieved 60% import substitution in telecom products. The scheme has generated 11.5 lakh jobs.

Import Restrictions: The government has implemented various measures to curb the import of substandard goods and protect the domestic industry. This includes investigations (anti-dumping/safeguard/countervailing) under the Customs Tariff Act, 1975. In FY 2024-2025 (up to February 2025), 206 cases against the import of substandard goods, valued at Rs 206.62 crore, have been booked. While tariffs generally aim to reduce imports and increase domestic output, their impact on overall productivity has been a subject of debate in past studies.

This shift from insourcing to outsourcing, especially in high-volume seasonal categories like ACs and coolers, provides a multi-year growth runway for players like PGEL.

Also read: Analyzing Karnataka Bank’s Transformation and Financial Strength

Growth drivers

Diverse client base: PGEL supplies over 35 brands, mitigating customer concentration risk and capturing outsourcing tailwinds. The company’s strong order pipeline, ongoing capacity expansion, and focus on automation and innovation position it well for sustained growth.

New product launches: Expanding into refrigerators with a greenfield plant in South India; strong pipeline of ODM products in ACs and WMs.

Capacity expansion: ₹800–900 crore CAPEX planned for FY26, including:

- RAC and washing machine facilities (Bhiwadi and Greater Noida)

- New refrigerator plant (South India)

- Compressor manufacturing unit

- Backward integration in plastics and tool rooms

R&D & product development: Internal design and innovation capabilities are improving stickiness with clients and helping PGEL gain market share.

Competitive advantage

PGEL’s scale, backward integration, and R&D-led product development provide a distinct edge. Having leveraged the PLI scheme to build capacity and partnerships, it now operates from a position of strength. With high asset turns, operational leverage, and efficient capital allocation, the company is targeting sustained profitability.

Barriers to entry are increasing for new EMS/ODM players due to the capital intensity, client acquisition challenges, and lack of integration. PGEL's early mover advantage positions it well for long-term leadership.

Risks

- Seasonality & weather impact: RAC and cooler demand is susceptible to early monsoons or weak summers.

- Raw material prices: Plastic resin and metal costs are volatile and influence ASPs and margins.

- Customer inventory cycles: Channel overstocking could lead to demand deferrals.

- Execution risks: Timely commissioning of new plants and smooth ramp-up of new products like refrigerators and compressors are critical. Working Capital pressure: Elevated inventory levels impacted FY25 cash flows, though management expects normalization in FY26.

Valuation perspective

With FY25 consolidated revenue of ₹4,870 crore and a net profit of ₹288 crore, the company delivered YoY growth of 77% in topline and over 112% in bottom line. The product business, which contributes the bulk of revenue, grew by 111%, driven by strong demand in air conditioners (up 128%) and washing machines (up 43%).

From a valuation standpoint, the current market capitalization of ₹22,882 crore implies a trailing P/E of 79.4x based on FY25 PAT. While that may seem elevated at first glance, it must be evaluated in the context of the company’s growth trajectory and earnings potential.

Management has guided for FY26 revenue of ₹6,345 crore (30% YoY growth) and a net profit of ₹405 crore, representing a projected 39% increase. If PGEL delivers on this guidance, the implied forward P/E drops to ~56.5x, which looks more palatable when seen alongside its historical CAGR and expected earnings expansion.

Importantly, the company's capital efficiency has improved sharply, net fixed asset turns are now over 5x, and it ended FY25 with a net cash position of ₹980 crore, indicating strong internal accruals and prudent capital allocation. The absence of debt, combined with a planned capex of ₹800–900 crore in FY26 for product capacity expansion, suggests that future growth will be funded without straining the balance sheet.

From a PEG (Price/Earnings to Growth) lens, assuming earnings grow ~39% in FY26, the implied PEG ratio stands near 1.45, which is within range for high-growth manufacturing businesses in their scale-up phase.

While the current valuation embeds optimism, PGEL’s visible growth pipeline, deepening OEM/ODM partnerships, and sectoral tailwinds from the government’s “Make in India” push justify some premium. However, the ability to execute on guidance, ramp up new capacities efficiently, and manage working capital will remain key to sustaining valuation multiples.

Crossing the inflexion point

PG Electroplast is in a sweet spot. The company is executing well on a focused strategy: ride the consumer appliance boom through ODM manufacturing. It is investing in capacity, broadening product lines, and improving profitability, all while staying asset-light for its clients.

If it delivers on FY26 guidance and ramps up refrigerator and compressor segments as planned, PGEL could well become a cornerstone Indian player in outsourced consumer durable manufacturing.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.