The Indian medical devices sector growth trajectory remains robust, fueled by rising healthcare expenditure, greater insurance penetration, supportive government programs such as Make in India, and expanding healthcare infrastructure. Historically dependent on imports for high-end devices, India now emphasizes domestic manufacturing and self-reliance through Atmanirbhar Bharat. This dynamic market spans consumables, disposables, diagnostic imaging, and advanced surgical instruments. Globally, the MedTech landscape is shifting toward minimally invasive procedures, connected devices (IoT), personalized medicine, and stricter regulations across key markets like the EU (EU MDR) and US (FDA). Companies that combine regulatory agility with R&D investment and strong distribution reach are positioned to capitalize on this Indian medical devices sector growth, forming attractive cases for Poly Medicure Limited’s investment thesis.

Also Read: A Comprehensive Industry Analysis of India's Hospital Sector

Business Snapshot & Evolution

Founded over two decades ago, Poly Medicure Limited (PML) has established itself as a significant player in the medical consumables space. Its business model revolves around the development, manufacturing, and marketing of a diverse portfolio of disposable medical devices across various clinical specialities. Key product categories include infusion Therapy (IV catheters, cannulas), Renal Care (dialyzers, blood lines), Respiratory Care, Diagnostics, and Blood Management, PML operates as a global entity, selling products in over 125 countries through an extensive distributor network alongside a strong direct presence in India.

Historically focused on high-volume consumables, PML is undergoing a strategic transformation. Recognizing the commoditization pressures in basic consumables and the higher growth potential in specialized segments, the company is actively moving up the value chain. This evolution involves significant investment in R&D and a strategic shift towards higher-margin, technology-intensive areas such as Cardiology, Critical Care/Oncology, and Orthopaedics. This transition has been accelerated by recent inorganic moves, notably the acquisition of PendraCare Group (Netherlands-based cardiology consumables) and Citeieffe Group (Italy-based trauma and extremity fixation systems) in 2025. These acquisitions provide PML with advanced technological capabilities, established European manufacturing footprints, and crucial regulatory approvals (EU MDR, FDA), enabling faster access to regulated developed markets.

Financial Performance Overview

Poly Medicure demonstrated strong financial performance in Fiscal Year 2025 (FY25), achieving consolidation revenue of INR1,669.8 crores representing a 21.4% year-over-year (YoY) growth. This growth was broad-based, driven by both domestic and export markets, which grew 18.6% and 24.0% respectively on a standalone basis. Profitability metrics also showed significant improvement in FY25, with EBITDA growing 26.6% YoY to INR452.8 crores . Consolidated EBITDA margin stood at 27.1% . The improvement was supported by a favourable product mix shift towards higher-margin categories and operational efficiencies.

However, the first quarter of FY26 (Q1 FY26) presented a mixed picture. While PAT continued strong growth at 25.5% YoY (INR93.1 crores), consolidated revenue growth moderated significantly to 4.8% YoY (INR403.2 crores). This slowdown was primarily attributed to temporary headwinds in the international market, particularly in Europe, which experienced inventory correction and market disruptions. Despite the top-line pressure, margins remained relatively resilient in Q1 FY26. Gross margin improved by 170 bps YoY to 68.4%, and PAT margin expanded by 250 bps YoY to 20.9%. The EBITDA margin saw a slight dip of 70 bps YoY to 26.3% but remained within the company’s guided range. The strong domestic performance, particularly in high-growth segments like Renal Care, helped offset the international slowdown.

Q1 FY26 snapshot

| Metric | Q1 FY26 | YoY Change | Commentary |

|---|---|---|---|

| Revenue | ₹403.2 crore | +4.8% | International headwinds; Europe inventory correction |

| PAT | ₹93.1 crore | +25.5% | Margin resilience despite slower top line |

| Gross Margin | 68.4% | +170 bps | Mix effects |

| EBITDA Margin | 26.3% | −70 bps | Within guided range |

| PAT Margin | 20.9% | +250 bps | Supported by efficiencies and mix |

Business segments breakdown

Business Segments

Infusion Therapy:

- Historically PML’s largest segment (approx. 63% of Q1 FY26 revenue), encompassing products like IV catheters and accessories. Faced challenges in Q1 FY26, registering a slight degrowth (-1.7%) due to a slowdown in Europe. However, the domestic business remains robust, with management targeting 18-20% growth for FY26.

Renal Care (Dialysis):

- A star performer exhibiting exceptional growth (60.1% in FY25 and 46.2% in Q1 FY26). Growth drivers include gaining market share, increased government reimbursement (Ayushman Bharat), policy changes, and strong service support. PML is doubling manufacturing capacity and targets around 50% growth for FY26.

Cardiology:

A key “transformative vertical.” PML has launched its own Drug-Eluting Stent (DES) and associated products. The acquisition of PendraCare bolsters this segment by providing a European manufacturing base, regulatory approvals (EU MDR, FDA), and a portfolio of guiding/diagnostic catheters. Synergies are expected from cross-selling.

Critical Care and Oncology:

- Another high-priority “transformative vertical” focused on specialized, higher-margin products like implantable ports and PICC catheters. This segment is expected to benefit significantly from government initiatives to expand oncology infrastructure. Management projects substantial growth (two and a half times) in FY26.

Orthopaedics (Via Citieffe):

- Marks PML’s entry into the resilient Trauma & Extremities segment (nails, screws). Citieffe provides a platform with strong organic growth (15% in CY24), a fully EU MDR-compliant portfolio, direct sales in key markets (Italy, US, Mexico), and very high gross margins (>90%). PML aims to double this business in five years.

International Business:

- Constituting roughly 70% of historical revenue, this segment faced a temporary dip (-0.9%) in Q1 FY26, driven by degrowth in Europe (-6.7%). Management expects a rebound, revising FY26 international growth guidance to 5-10%. Long-term drivers include recovery, the UK-India FTA, and US market entry.

Contract Design & Manufacturing (CDMO):

- An emerging area leveraging PML's manufacturing expertise. Two contracts in vascular access and pain management have been signed, with revenue contribution expected from FY27.

Also Read: India’s CDMO Boom: A Rising Global Powerhouse

Strategic moats

- Integrated Manufacturing and Cost Advantage: PML operates backward-integrated manufacturing facilities primarily in India, providing significant control over the value chain from tooling to sterilization. This allows for cost competitiveness and agility. Crucially, PML plans to leverage this cost advantage by outsourcing high-cost, manual-intensive processes from its acquired European operations (PendraCare, Citieffe) to India, aiming to improve overall group profitability.

- Focus on Innovation and R&D: PML is consciously moving up the technology ladder, investing in R&D (expenses grew 20% in Q1 FY26) to develop complex devices in Cardiology, Critical Care, and Renal segments. Its growing patent portfolio (334 granted) underscores this focus. The “reusable building blocks” approach in R&D accelerates development cycles.

- Regulatory Expertise and Platform Acquisition: Navigating complex global regulations is a key differentiator. The acquisitions of PendraCare and Citieffe are pivotal, providing PML with established platforms that possess critical EU MDR and FDA approvals. This significantly shortens the time-to-market for PML’s own advanced products (like DES) in regulated Western markets.

- Strong Domestic Distribution and Service: In India, PML leverages a large direct sales farce (targeting 630+ associates) to deepen penetration into Tier - 2/3 cities and increase wallet share in hospitals. In the Renal segment, its emphasis on service, training, and engineering support differentiates it from competitors, particularly lower-cost Chinese players.

- Proven Quality and reliability: PML highlights its track record of zero product liability claims in its 28-year history, building trust with healthcare providers. Long-term (20-year) product support commitments further enhance customer stickiness.

Growth drivers and expansion plans

- Domestic Market Acceleration: PML targets aggressive 30% domestic revenue growth in FY26, driven by sales force expansion (adding 100 associates), deeper penetration into the private sector (growing at 25%), and scaling up new Cardiology and Critical Care divisions.

- Renal Segment Leadership: Aiming for 50% growth in FY26 and targeting a market share increase from 8-9% to 15-17% in 2-3 years, supported by capacity doubling (by end of FY26) and favourable policy tailwinds. Development of an HDF machine is underway for mid/late 2026 launch.

- Inorganic Growth Integration and Synergies: A key focus is integrating PendraCare and Citieffe to realize projected synergies. This includes generating EUR3-4 million incremental EBITDA from PendraCare over 3-4 years through procurement optimization, cross-selling (PML’s DES via PendraCare network, PendraCare products in India), and outsourcing manufacturing to India. For Citieffe, the priorities are launching plates, expanding in the US, and achieving cost reduction via Indian manufacturing, aiming to double the business in 5 years.

- Capacity Expansion (Organic CAPEX): PML is in a significant CAPEX cycle, investing INR 400-500 crores over FY26-FY27 to build three new plants in India (Palwal, Haridwar, Medical Device Park). These facilities, expected to be commissioned around mid-2026, will provide necessary capacity for Renal, Cardiology, and Critical Care segments beyond FY27. FY26 Capex guidance is INR250 crores.

- International Market Recovery and Expansion: While Q1 FY26 saw headwinds, PML expects a rebound in Europe and targets 5-10% international growth for FY26. Longer-term drivers include leveraging the UK-India FTA, penetrating the US market ($15-20M target in 2-3 years via GPO contracts), and establishing a direct B2C presence in Brazil.

Also Read: Entero Healthcare Solutions and the Transformation of Healthcare Distribution

Risks and industry headwinds

- Macroeconomic and geopolitical uncertainty: International business (major revenue contributor) is vulnerable to global slowdowns, geopolitical tensions, currency fluctuations, and trade disruptions (ex, US tariffs, Chinese dumping in Europe), as evidenced by the Q1 FY26 performance.

- High European operating costs: The acquired European assets (PendraCare, Citieffe) have significantly lower EBITDA margins compared to their high gross margins, attributed to higher labour, sales, marketing, and overhead costs in Europe. Failure to realize planned cost synergies through outsourcing to India poses a key risk to margin improvement goals.

- Integration Risk: Successfully integrating two sizable European acquisitions simultaneously, aligning cultures, and achieving operational efficiencies presents execution challenges. Management has indicated a pause in further M&A to focus on absorption.

- Competition: Entering specialized segments like interventional cardiology and orthopaedics pits PML against large, established global MedTech MNCs with significant R&D budgets and market presence.

- Regulatory Hurdles: While acquisitions provide regulatory platforms, delays in obtaining necessary approvals for new products or facility changes (ex., PendraCare consolidation) under stringent regimes like EU MDR remain a potential bottleneck.

- Working Capital: Although PML has a strong balance sheet, aggressive domestic expansion involving credit extension to distributors and inventory build-up can lengthen the working capital cycle. Customer-side delays in the defence-like procurement cycles for some government business can also strain cash flows.

Valuation and market view

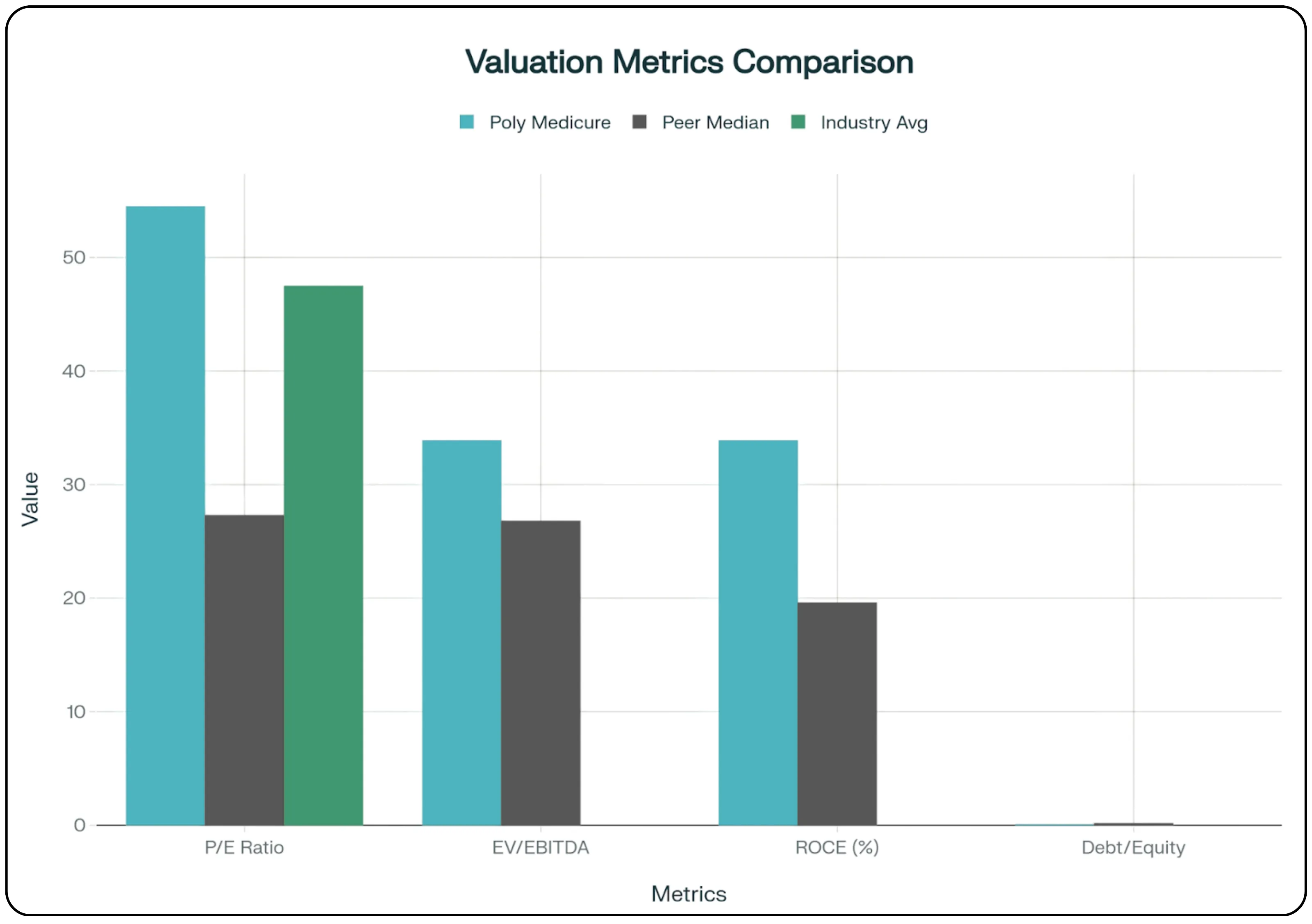

Poly Medicure Limited (PML) consistently trades at premium valuation multiples compared to the broader market and many peers within the medical equipment and supplies sector. As of recent data the stock trades at a Price-to-Earnings (P/E) ratio of approximately 54.5x, notably higher than the industry P/E of around 47.5x and the median P/E of its peer group. Similarly, its Enterprise Value-to-EBITDA (EV/EBITDA) multiple stands near 33.9x, above the peer median of roughly 26.8x.

This premium valuation reflects strong investor confidence rooted in PML’s consistent track record of high revenue growth (targeting 20%+ annually), superior profitability metrics (EBITDA margin consistently in the 26-27% range), and robust return ratios, evidenced by a higher Return on Capital Employed (ROCE) of approximately 33.9%. The market appears to be pricing in the company’s successful strategic shift towards higher-margin specialized verticals (Cardiology, Critical Care, Renal) and the significant growth potential anticipated from both organic capacity expansion in India and the synergistic integration of its recent European acquisitions (PendaCare and Citieffe).

The acquisitions were executed at EV/EBITDA multiples deemed reasonable for specialized MedTech assets possessing critical regulatory approvals (13x for PendraCare, 10.2x for Citieffe). While the market acknowledges the strategic rationale, continued support for the premium valuation hinges on PML’s ability to effectively integrate these businesses, realize projected cost and revenue synergies (particularly improving the lower EBITDA margins of the European entities), and successfully navigate the temporary international market headwinds while maintaining strong domestic growth momentum. The company's exceptionally strong balance sheet, characterized by zero net debt and a very low Debt-to equity ratio of 0.07 provides substantial financial stability and flexibility, underpinning investor confidence in its capacity to fund tis ambitious growth plans without undue leverage

Bottom Line

Poly Medicure stands out as a high-quality company within a structural growth sector, successfully executing a strategic transformation towards higher-margin, specialized medical technologies. It profiles as a potential long-term compounder, particularly noting its fundamental strength amidst recent market corrections. The company combines a robust, cash-generating domestic business which is significantly driven by its rapidly expanding Renal Care segment, and a strategic international expansion plan accelerated by value-accretive acquisitions that provide crucial regulatory and market access platforms. While near-term international headwinds and the integration of lower-margin European assets pose challenges, the company’s strong execution track record, pristine, debt-free balance sheet, and clear synergy roadmap position it well for sustained, profitable growth. Although the stock has seen some valuation correction from its peaks, bringing multiples down slightly, it still commands a premium. A valuation closer to the peer median or industry P/E would represent a more conventional accumulation zone relative to historical norms. Execution on integrating acquisitions and realizing synergies remains a key monitorable for validating this outlook and its transformation into a more specialized, global MedTech player.

Stay ahead of market trends with in-depth analysis. Join CubePlus and invest smarter.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.