India’s ‘India Recycling Industry’ Growth is in the middle of a major transformation. Stricter environmental rules, rapid technological progress, and a Circular Economy India 2025 focus are reshaping how waste and resources are managed. The industry spans several fast-growing segments electronic waste, tire recycling, lead and plastic recovery, and advanced water treatment. Together, they’re building one of the strongest sustainability-linked markets in the country.

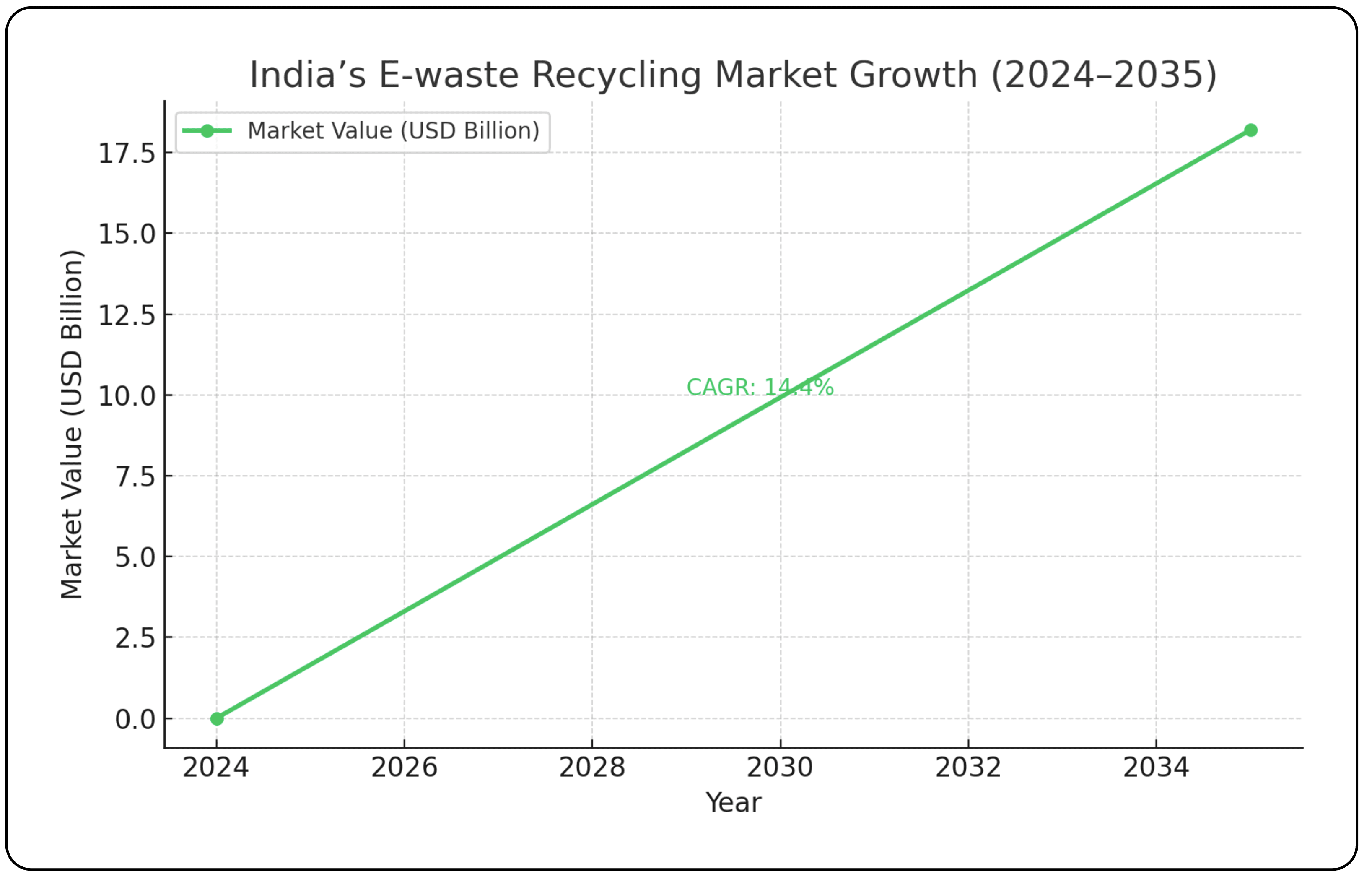

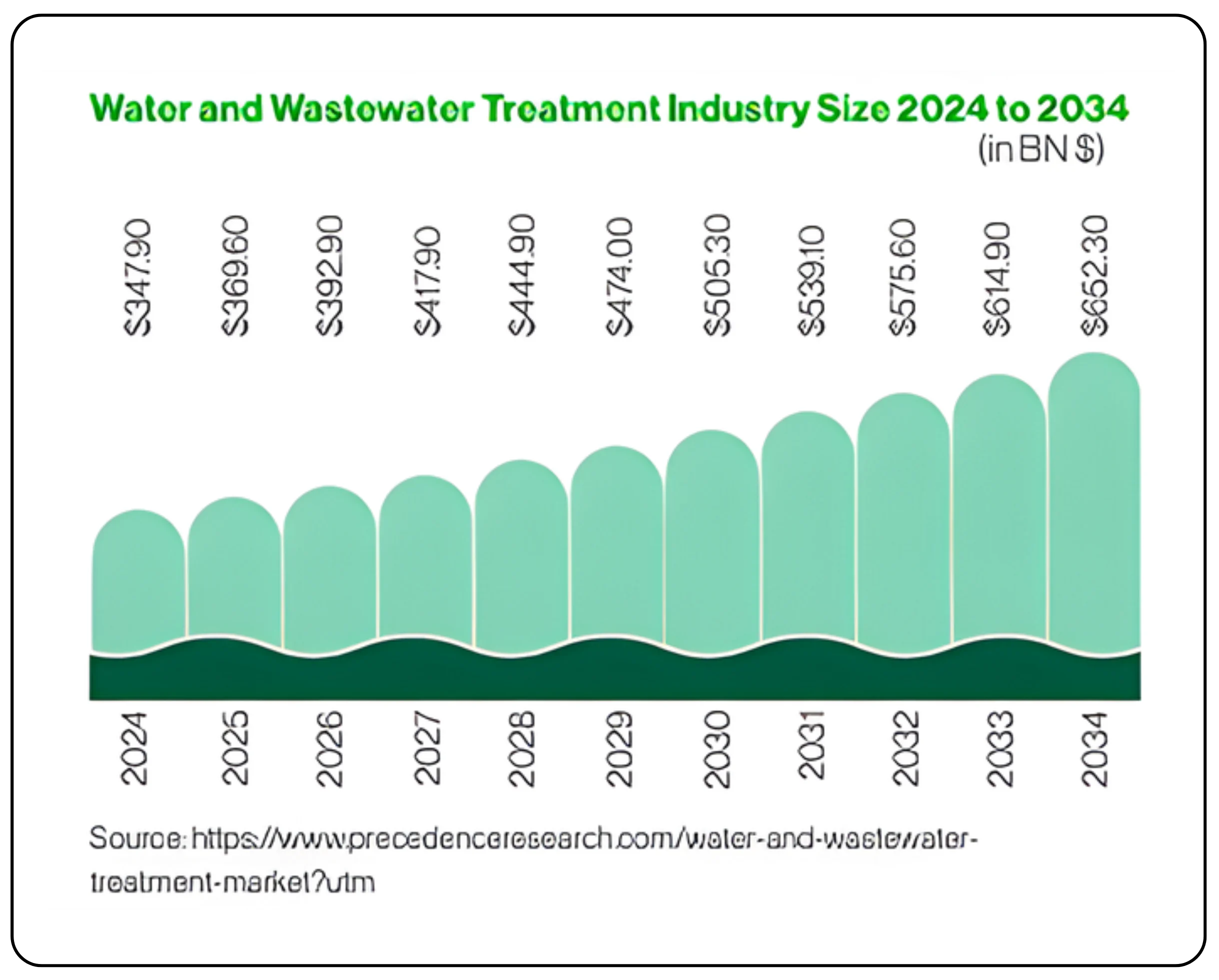

The momentum is clear in the numbers. India’s e-waste recycling market alone is projected to reach USD 18.2 billion by 2035, growing at a 14.4% CAGR. Globally, the water and wastewater treatment industry is expected to expand from USD 347.9 billion in 2024 to USD 652.3 billion by 2034, a steady 6.5% CAGR.

Regulatory support is also fueling this shift. Policies like Extended Producer Responsibility (EPR) and tighter environmental compliance norms are pushing companies to rethink how they handle waste and resources. With India maintaining over 6.5% GDP growth, businesses involved in material recovery, processing, and environmental technology are well placed to ride this wave aligning profitability with sustainability as the economy grows cleaner and more efficient.

What is Extended Producer Responsibility (EPR)?

Extended Producer Responsibility, or EPR, is an environmental policy that makes producers responsible for their products even after customers are done using them. In simple terms, if a company manufactures, sells, or imports a product, it’s also responsible for what happens to that product at the end of its life whether it’s collecting, recycling, or disposing of it safely. This shifts the responsibility of waste management away from local governments and consumers, placing it firmly on the producer.

The main idea behind EPR is accountability. When companies are made to handle the waste their products generate, they have a strong incentive to design products that last longer, use fewer materials, and are easier to recycle. This not only reduces environmental impact but also drives efficiency within the production process. For instance, a packaging company that knows it must collect and recycle used plastic will likely invest in lighter, recyclable materials to cut future costs.

EPR also benefits companies in ways that go beyond compliance. It enhances brand image. Today’s consumers are far more aware of sustainability issues, and they tend to trust and support brands that take visible responsibility for their waste. A strong EPR program signals environmental commitment, which helps companies attract eco-conscious buyers and ESG-focused investors.

From a business standpoint, EPR can also improve cost management and open doors to innovation. Redesigning products for recyclability often leads to material savings and operational efficiency. Meanwhile, new recycling technologies or reuse systems can create fresh revenue streams. Some EPR systems even reward companies that design eco-friendly products with lower fees, making sustainability financially attractive.

Lastly, EPR ensures companies stay compliant with evolving regulations. Countries across the world, including India, have introduced mandatory EPR rules for industries like plastics, electronics, batteries, and packaging. Meeting these requirements protects companies from penalties and helps them maintain access to markets where sustainability standards are becoming non-negotiable.

In short, EPR turns waste into a shared opportunity for cleaner environments, smarter design, and stronger brands. It’s not just about managing what happens after a product is sold; it’s about rethinking how it’s made in the first place.

Market structure and segmentation

Electronic Waste Recycling Segment

The electronic waste recycling segment is emerging as one of the fastest-growing parts of India’s recycling ecosystem. With rising consumption of electronic devices across IT, telecom, consumer durables, and healthcare, the volume of discarded electronics has surged creating both an environmental challenge and a significant business opportunity. The growth is supported by rapid digitization, incentives under the Production Linked Incentive (PLI) scheme, and tighter rules enforcing proper e-waste collection and recycling.

Organized recyclers today run integrated operations that go well beyond basic waste processing. Their business models combine precious metal recovery, data destruction, IT asset disposition (ITAD), and EPR compliance support for producers and corporates. Many also earn from high-value services such as secure data disposal, rare earth metal recovery, and battery recycling areas gaining traction with the rise of electric mobility.

What’s driving this momentum is not just regulation but also corporate responsibility. As companies strengthen their ESG commitments and data protection policies, demand for compliant and certified recyclers continues to climb. Together, these forces are positioning e-waste recycling as a critical enabler of both environmental sustainability and circular value creation in India’s technology-driven economy.

Tire and Rubber Recycling Segment

The tire and rubber recycling segment has moved far beyond simple shredding, embracing advanced technologies that enable full-scale material recovery. Techniques like pyrolysis, devulcanization, and cryogenic processing allow recyclers to extract valuable outputs such as carbon black, reclaimed rubber, and fuel oil. India, producing around 6–7% of the world’s end-of-life tires, has a consistent supply of feedstock, supporting the growth of organized recycling operations.

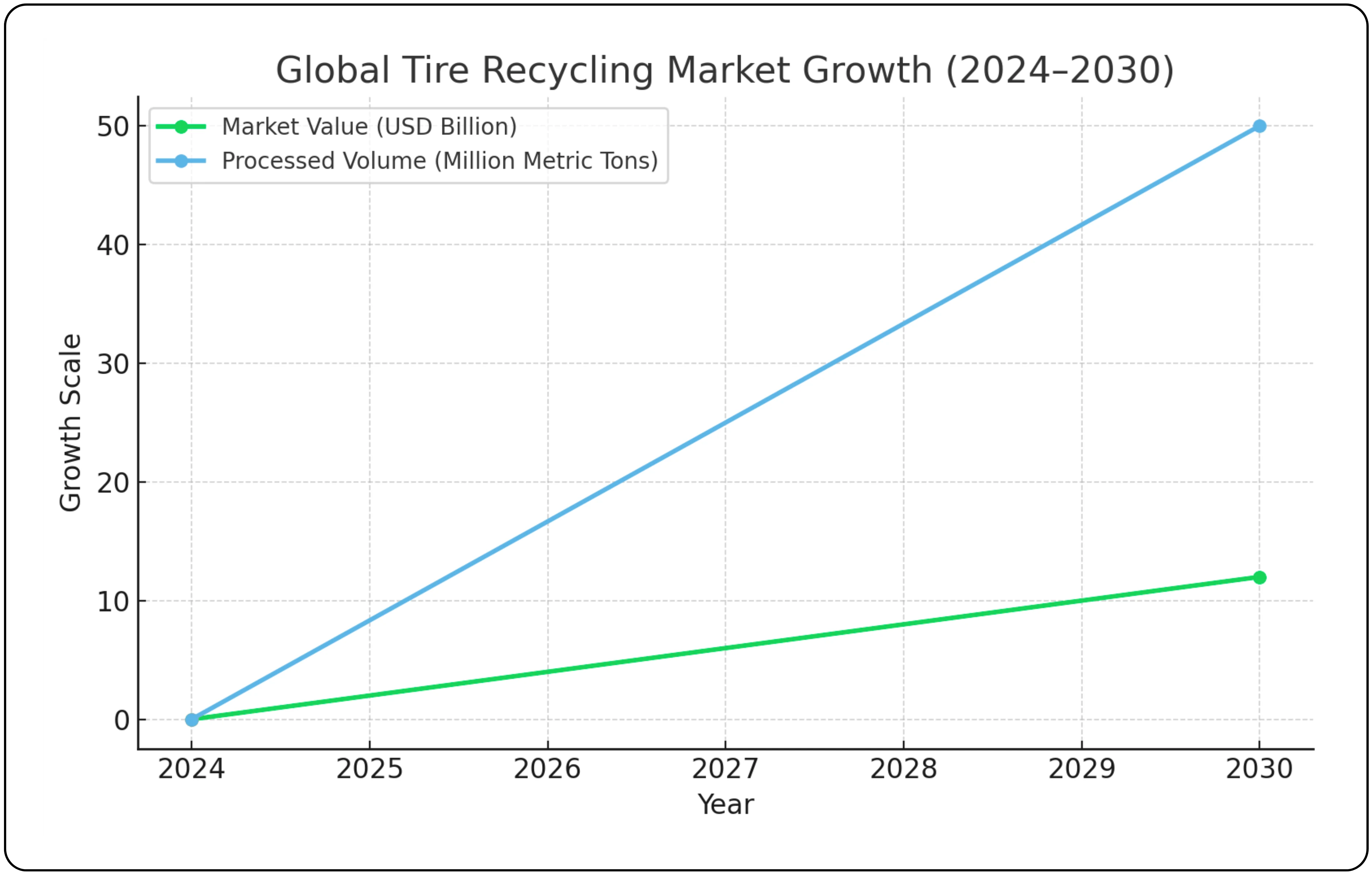

This segment serves a wide range of applications, from infrastructure projects and industrial uses to steel production and consumer products. Recycled materials find their way into road construction, rubberized bitumen, sports surfaces, and cement additives, creating multiple revenue streams. Globally, the tire recycling market is expected to hit USD 12 billion by 2030, growing at a 14.6% CAGR, while processed volumes could reach 50 million metric tons at a 10.7% CAGR.

India’s large waste base, combined with technology adoption and diverse end markets, positions this segment as a high-potential growth area within the recycling industry.

Metal Recycling and Processing

The metal recycling segment, with lead recycling at its core, shows strong fundamentals supported by steady industrial demand. India, as the world’s second-largest refined lead producer, relies on recycled lead for about 85% of domestic consumption, creating significant opportunities for integrated recycling businesses. Lead-acid batteries, widely used in automotive, telecom, renewable energy storage, and backup power applications, provide a stable and predictable demand base.

Beyond lead, secondary aluminum and plastic recycling are also gaining momentum. Growing industrial demand for sustainable materials, coupled with supportive policies like customs duty exemptions and domestic recycling incentives, is making these segments increasingly viable. Advances in chemical recycling are now allowing processing of mixed or degraded plastics that were previously unrecyclable, expanding the addressable market and enhancing the economic prospects for recyclers. Together, these trends position metal and material recycling as a critical component of India’s circular economy push.

Water Treatment and Environmental Technology

The water treatment sector is a cornerstone of India’s environmental services, tackling the twin challenges of rising demand and limited freshwater resources. With just 4% of the world’s freshwater supporting 18% of the global population, India faces immense pressure from urbanization, industrial growth, and population expansion. Advanced treatment, desalination, and water recycling technologies are increasingly critical to meeting these needs.

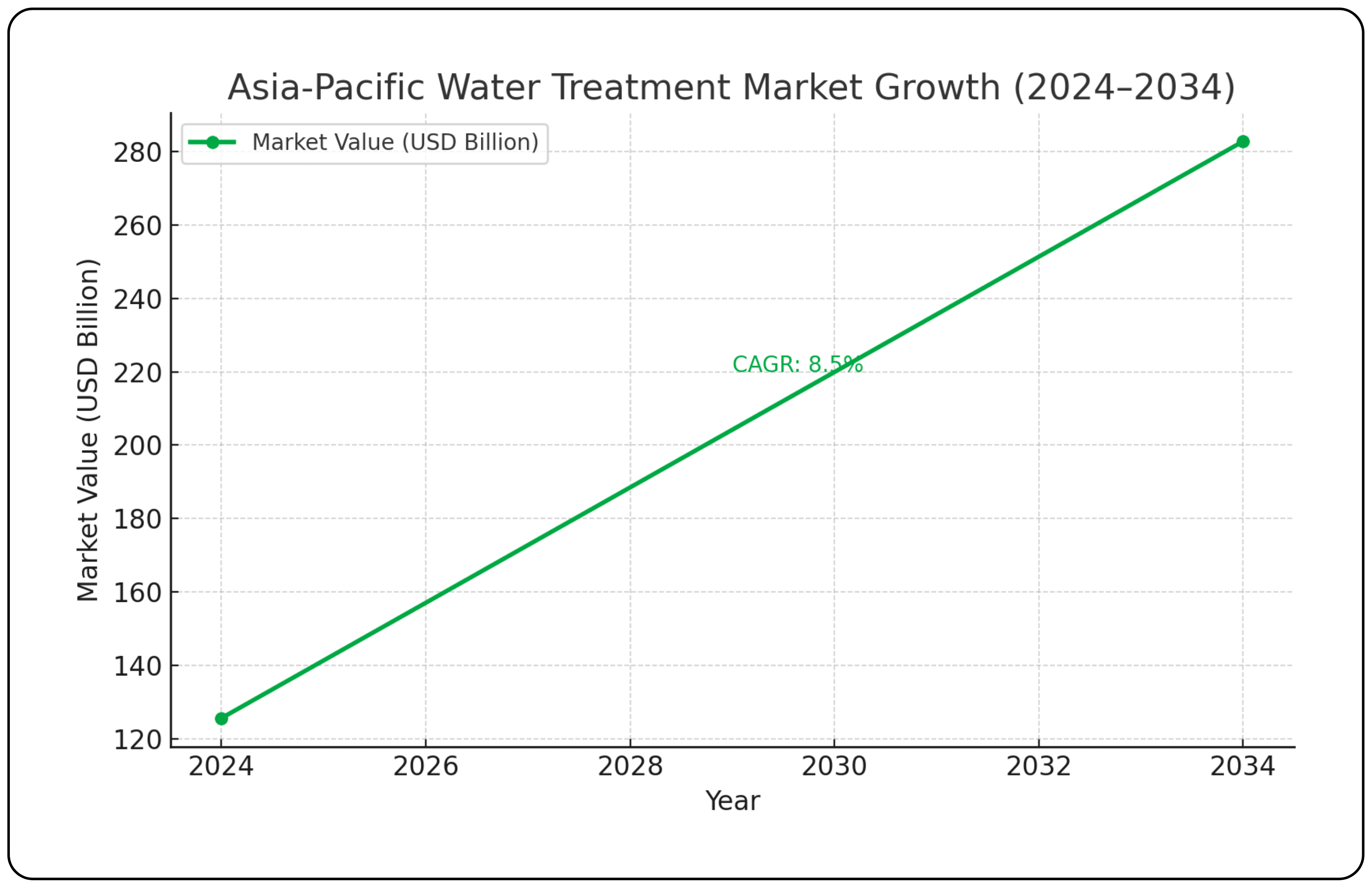

Government programs such as the Jal Jeevan Mission, AMRUT 2.0, and the Namami Gange Programme are driving large-scale infrastructure development. The Jal Jeevan Mission alone has provided tap water connections to over 15.19 crore households, covering nearly 79% of rural India, reflecting the massive investment underway in water infrastructure. The Asia-Pacific water treatment market mirrors this momentum, projected to grow from USD 125.6 billion in 2024 to USD 282.8 billion by 2034 at an 8.5% CAGR, highlighting both the scale of the challenge and the opportunity for companies in this space.

Key players in the industry

India’s recycling and environmental services sector is anchored by a handful of companies that have not only built scale but also shaped the country’s sustainability agenda. Each of these players operates in a distinct niche—water treatment, electronic waste recovery, rubber recycling, or metal reprocessing—together forming the foundation of India’s transition toward a circular economy.

VA Tech Wabag Ltd.

Headquartered in Chennai, VA Tech Wabag is a global leader in water treatment and desalination with nearly a century of legacy. Operating across 25 countries, the company offers end-to-end solutions in drinking water, industrial wastewater, desalination, water reuse, and zero liquid discharge systems. Backed by over 125 proprietary technologies and two R&D centers in Europe and India, Wabag has executed more than 6,500 projects worldwide. In FY2024–25, it reported consolidated revenue of ₹33,38.6 crore and a robust order book of over ₹15,000 crore, reflecting strong demand visibility. Beyond conventional water treatment, Wabag is expanding into sustainability-driven solutions such as green hydrogen, biogas recovery, and water recycling, positioning itself among the world’s top three private water operators.

Curious about VA Tech Wabag’s business and future potential? Read the full fundamental analysis.

Eco Recycling Limited (Ecoreco)

Ecoreco is India’s oldest and largest integrated e-waste management company, operating at the intersection of technology and sustainability. It specializes in e-waste recycling, IT asset disposition (ITAD), lithium-ion battery recycling, and EPR compliance. With certifications such as R2v3, ISO, NAID, and TERRA, the company adheres to stringent global standards in data security and environmental safety. In FY2025, Ecoreco delivered a 57% jump in revenue to ₹43.94 crore, driven by growth in rare earth and precious metal recovery and rising demand for responsible battery recycling. Its long-term strategy aligns closely with India’s Critical Mineral Mission and circular economy policies, emphasizing ESG compliance and digital traceability to ensure transparent, sustainable operations.

Tinna Rubber and Infrastructure Ltd.

Tinna Rubber has been a pioneer in tire and rubber recycling since 1987. The company transforms end-of-life tires into high-value materials such as crumb rubber, micronized rubber powder, and reclaimed steel, serving industries ranging from infrastructure to consumer goods. With six manufacturing facilities in India and Oman—and expansion plans in Saudi Arabia and South Africa—Tinna has emerged as one of the country’s largest ELT recyclers. Its revenue mix remains well diversified, with infrastructure contributing 48%, industrial 22%, steel 13%, and consumer 7%. The company’s focus on advanced devulcanization, cryogenic processing, and carbon footprint reduction underscores its commitment to sustainable material reuse and long-term circular economy integration.

Gravita India Ltd.

Gravita India is a global force in non-ferrous metal recycling, particularly lead, aluminum, and plastic. Founded in 1992, the company operates across 70 countries, with more than half its revenues coming from exports. Its vertically integrated model spans the entire value chain—from collection and recycling of lead-acid batteries to refining and alloy manufacturing. With operations in India, Africa, Europe, and Asia, Gravita plays a central role in India’s lead ecosystem, meeting roughly 85% of the country’s domestic demand through recycled sources. The company’s growth strategy focuses on clean smelting technologies, operational digitization, and expanding its footprint among the top five global recyclers by 2026.

Curious about Gravita India’s business and future potential? Read the full fundamental analysis.

Other key players in the recycling industry

| Company Name | Market Cap (₹ Cr) | OPM (%) | Revenue/Sales (₹ Cr) | Current Price (₹) | Business Focus |

|---|---|---|---|---|---|

| POCL | 4,032 | 6.0 | 2,215 | 1,337.00 | India's largest secondary lead manufacturer for lead-acid batteries |

| MSTC LTD | 3,629 | 57.0 | 319 | 517.00 | Government-owned metal scrap trading corporation |

| EMS LIMITED | 2,970 | 26.0 | 987 | 541.00 | Water and wastewater treatment EPC services |

| AWHCL (Antony Waste) | 1,476 | 21.0 | 959 | 520.00 | Municipal waste management with ~20 years experience |

| GANECOS (Ganesha Ecosphere) | 1,232 | 14.0 | 1,466 | 1,230.60 | Leading PET waste recycling company |

| GRP LTD (GRP) | 1,147 | 12.0 | 548 | 2,150.00 | Reclaimed rubber and engineered products from waste tyres |

| NAMO EWASTE-SM | 464 | 10.0 | 122 | 200.05 | E-waste management and compliance services |

| NRL | 453 | 9.0 | 174 | 65.11 | Non-ferrous metal scrap recycling |

| ELGIRUBCO (Elgi Rubber) | 315 | 2.0 | 373 | 62.00 | Tyre sector rubber recycling solutions |

| APEXECO-SM | 174 | 15.7 | 71 | 132.00 | Small-cap waste management company |

The sector encompasses a range of business models, from government-run trading operations to advanced recycling technologies, each displaying different profitability patterns based on their market focus and operational efficiency.

Technology and innovation drivers

Advanced Processing Technologies

The recycling and environmental services industry is seeing a surge in technological innovation that’s transforming how materials and resources are managed. Digital tools like IoT-enabled logistics, AI-driven waste sorting, and blockchain-based traceability are boosting efficiency while ensuring compliance with regulations. Advanced recycling technologies are now able to process materials that were once considered non-recyclable, improving recovery rates and cutting operational costs.

Water treatment is also being reshaped by technology. Solutions such as reverse osmosis, UV disinfection, chemical treatments, and hybrid desalination systems are becoming more sophisticated. Smart water management, using digital monitoring, remote sensing, and AI analytics, allows for predictive maintenance and more flexible operations. Collectively, these advancements are strengthening circular economy practices by maximizing resource recovery and minimizing waste.

Research and Development Investment

Top companies in the recycling and environmental services space are investing heavily in R&D to build proprietary technologies and strengthen their intellectual property portfolios. Their research focuses on energy-efficient treatment systems, low-footprint processing methods, and solutions that advance the circular economy. Collaborations with universities and development agencies further enhance capabilities while keeping innovations aligned with market needs and environmental standards.

These innovation ecosystems also enable region-specific and scalable solutions, particularly around energy efficiency and operational adaptability. Companies holding more than 125 intellectual property rights illustrate the sector’s commitment to using technology not just for sustainability, but also as a source of competitive advantage.

Regulatory environment and policy framework

Extended Producer Responsibility Implementation

Extended Producer Responsibility (EPR) frameworks are reshaping how waste is managed by creating structured incentives for recycling. Through mechanisms like certificates, financial benefits, and priority access to recyclable materials, EPR encourages companies to integrate sustainable practices into their operations. Its application spans multiple waste streams—including electronics, batteries, packaging, and automotive components—ensuring accountability across the entire product lifecycle.

Recent regulations are further strengthening this trend. The E-Waste Management Rules 2022 impose stricter EPR compliance, boosting demand for scientific recycling and secure data destruction services. Similarly, the Battery Waste Management Rules require collection and recycling of used batteries, with minimum recycled content targets starting in FY 2028. Together, these frameworks not only drive long-term demand for organized recycling but also help formalize the industry, creating predictable and sustainable growth opportunities.

Government Policy Support

Government policies are playing a key role in supporting India’s recycling and environmental services industry. Flagship programs targeting water security, waste management, and sustainable development are creating a more structured and favorable environment for growth. Initiatives like the Critical Mineral Mission, which offers customs duty exemptions on 25 critical minerals and supports domestic recycling, are particularly beneficial for precious metal recovery operations. At the same time, the National Infrastructure Pipeline is driving investment in water, energy, and environmental projects, leveraging collaboration between central and state governments and private players.

Regulatory reforms are further shaping the sector. Policies promoting water reuse, enhanced monitoring systems, and public-private partnerships are encouraging more formalized and efficient infrastructure development. Mechanisms like Reverse Charge Mechanism (RCM) and Tax Deducted at Source (TDS) aim to bring recycling transactions into the formal economy, reducing the dominance of the informal sector and creating a more transparent, accountable market.

Market dynamics and growth drivers

Supply-Demand Fundamentals

The recycling and environmental services industry in India is underpinned by strong supply-demand fundamentals. On the supply side, rising waste generation provides a steady stream of materials—over 275 million waste tires are produced annually, and electronic waste continues to grow alongside rapid digitization and infrastructure expansion. Lead consumption is also expected to rise, with 65–70% of demand projected to be met through recycled sources by 2030.

On the demand side, businesses are increasingly turning to recycled materials across construction, consumer goods, and industrial applications, driven by sustainability mandates and cost advantages. Corporate ESG commitments are further accelerating the shift toward circular economy models, creating a predictable, long-term market for recycled products and environmental services. This alignment of waste availability with growing material demand is a key driver of the sector’s sustained growth.

Economic Value Creation

The recycling and environmental services sector offers compelling economic value, driven by asset-light models and significant operating leverage potential. Margins differ across material categories, with high-value operations like precious metal recovery and specialized services delivering stronger EBITDA compared to conventional recycling. EPR compliance adds another layer of stability, generating predictable, fee-based income that enhances operational efficiency.

Water treatment businesses also enjoy strong economic fundamentals, supported by robust order books and revenue visibility underpinned by government guarantees and multilateral funding. By aligning closely with infrastructure development and regulatory compliance, the sector benefits from steady, systematic demand growth, making it both economically attractive and strategically important for sustainable development.

Operational challenges and risk factors

Infrastructure and Processing Constraints

Despite strong growth prospects, the recycling and environmental services industry faces significant infrastructure and processing challenges. Collection networks remain inadequate, especially in rural areas, leading to supply chain disruptions and higher operational costs. Quality feedstock is often limited due to contamination and poor waste segregation, making processing more difficult.

Different materials degrade at varying rates, complicating recycling operations and affecting the quality of recovered outputs. At the same time, informal recyclers continue to operate outside regulatory frameworks, creating competitive pressure through lower costs and non-compliance. Addressing these constraints is critical for scaling organized recycling and realizing the sector’s full economic and environmental potential.

Market and Economic Pressures

Recycling businesses also navigate significant market and economic pressures. Fluctuating commodity prices and shifting demand for recycled materials create revenue volatility, while competition from cheaper virgin materials—especially when oil prices are low—puts downward pressure on pricing. Rising operational costs, from energy to raw waste procurement, further strain margins.

Maintaining consistent quality is another challenge. Contamination and variations in material composition or recycling methods limit the use of recycled outputs in high-value applications. Standardizing recycled materials for performance-critical products remains difficult, highlighting the need for better processing technologies and quality control systems to sustain growth and competitiveness.

Regulatory and Compliance Risks

Companies in the recycling and environmental services sector operate under a complex regulatory landscape, which exposes them to compliance and geopolitical risks. Varying environmental standards and labor laws across regions can affect operations and increase costs, while climate-related events such as floods or extreme weather may disrupt infrastructure and supply chains.

Reliance on government projects adds another layer of vulnerability, as policy shifts can affect revenues. However, established players often mitigate this risk through backing from multilateral financial institutions and sovereign guarantees. At the same time, intense competition from both domestic and international firms in processing and infrastructure segments creates constant pressure to maintain efficiency, compliance, and market positioning.

Growth opportunities and market outlook

Regulatory and Policy Tailwinds

The regulatory environment is emerging as a strong growth driver for India’s recycling and environmental services industry. As EPR frameworks advance and recycling targets approach full compliance, demand for organized recycling services is becoming more predictable. Recycled content mandates are also creating direct market pull for processed materials, further strengthening the sector’s economic case.

Technology-Driven Expansion

Technology is becoming a key enabler of growth in the recycling and environmental services sector. Robotics and automation are improving productivity, cutting labor costs, and enhancing workplace safety, while digital tools support product-as-a-service models and predictive maintenance, extending equipment lifecycles and boosting operational efficiency.

Advanced processing technologies are also expanding the range of materials that can be recycled, improving recovery rates and lowering costs. Innovations in bio-based additives and hybrid processing compounds are further enhancing the quality and applications of recycled materials, opening new markets and creating additional revenue streams for companies in the sector.

Market Expansion and Diversification

The recycling and environmental services market is expanding rapidly, fueled by sustainability commitments, regulatory mandates, and cost advantages. The Asia-Pacific region, in particular, is emerging as a key growth hub, driven by the automotive sector, supportive policies, and efficient processing methods. Rising electric vehicle adoption is further boosting demand for materials and generating additional waste, providing a steady feedstock for recyclers.

Water infrastructure development is another major growth avenue. Government initiatives, industrial expansion, and urbanization are driving investments in treatment and desalination projects. The desalination market alone is projected to reach USD 49.8 billion by 2032, growing at an 8.6% CAGR, with hybrid technologies enhancing both energy efficiency and water output. Together, these trends are creating diverse opportunities for market expansion and service diversification in the sector.

Circular Economy Integration

The push toward circular economy practices is creating tangible economic value by maximizing resource use and minimizing waste. Companies are increasingly incorporating recycled materials into production, reducing dependence on virgin resources while supporting jobs in recycling and related sectors.

This shift also opens opportunities for diversification, from developing secondary products and recovering valuable resources to generating renewable energy through waste processing. Advances in processing technologies and innovative applications are expanding the range and usability of recycled materials, helping businesses penetrate new markets and create additional revenue streams.

Investment thesis and strategic outlook

India’s recycling and environmental services sector offers strong investment potential, underpinned by regulatory support, favorable supply-demand dynamics, and technological innovation. The industry is further bolstered by India’s economic growth and its emergence as a global manufacturing hub amid broader supply chain diversification.

Companies that combine integrated business models with advanced technologies and regulatory expertise are well positioned to benefit from the shift from informal to formal operations, capturing market share while adhering to environmental and safety standards. Long-term growth is supported by urbanization, rising environmental awareness, strengthening regulations, and corporate sustainability commitments, all of which drive consistent demand for recycling and environmental services.

Success in this sector depends on operational excellence, compliance capabilities, geographic reach, and strategic focus on high-value materials and services. With regulatory support, technological advancement, and strong market demand converging, the industry is set for sustained expansion and meaningful value creation.

Turn research into action and explore smarter investing opportunities with CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.