You have probably seen this before. The stock market is making headlines, touching record highs. Everyone around you is talking about how much money they have made. And yet, you are sitting on a big chunk of cash in your bank account, waiting.

Why? Because you are worried the market might crash. Or maybe you are waiting for the “perfect time” to invest, when prices come down. It feels safe to keep your money in the bank. After all, nothing bad can happen there, right?

But here is the catch: that safety comes at a price. While you wait, the market keeps moving up, and you miss out on gains that could have grown your money. That is what we call the hidden cost of holding cash. Let us see why it matters.

Why do people sit on cash in bull markets?

It usually comes down to fear. Fear that the market has gone up too much and a crash is just around the corner. Fear of losing hard-earned money in something that feels unpredictable.

You have seen headlines warning that “markets are overheated,” or you remember stories of people losing money during past crashes, like in 2008 or during COVID. That memory sticks. So you think, “I will wait for prices to fall before I invest.”

Sometimes it is not even past experience; it is just comfort. Seeing a big balance in your bank account feels safe. There is no risk of it going down tomorrow. Stocks, on the other hand, can feel like a roller coaster, and that uncertainty is scary.

Here is the problem: the “safe” choice often turns out to be expensive during a bull market. While your money sits idle, prices keep climbing, and you miss out on returns that could have grown your wealth.

The real cost of playing it safe

Let us put this in perspective. Say you had ₹10 lakh in March last year. Instead of investing when the market started picking up, you left it in your savings account, earning about 3% interest per annum.

Fast forward a year, and the Nifty 50 has gone up by roughly 15%. If you had invested, your ₹10 lakh could have turned into ₹11.5 lakh. But in your savings account, it turned into ₹10.3 lakh, and that’s before tax.

That’s ₹1.2 lakh gone. Not because you lost money, but because you didn’t make money. And the story doesn’t end there. That extra ₹1.2 lakh could have earned more returns for you in the next 5 or 10 years. Miss one rally, and you are not just losing today’s gains, you’re losing future wealth too.

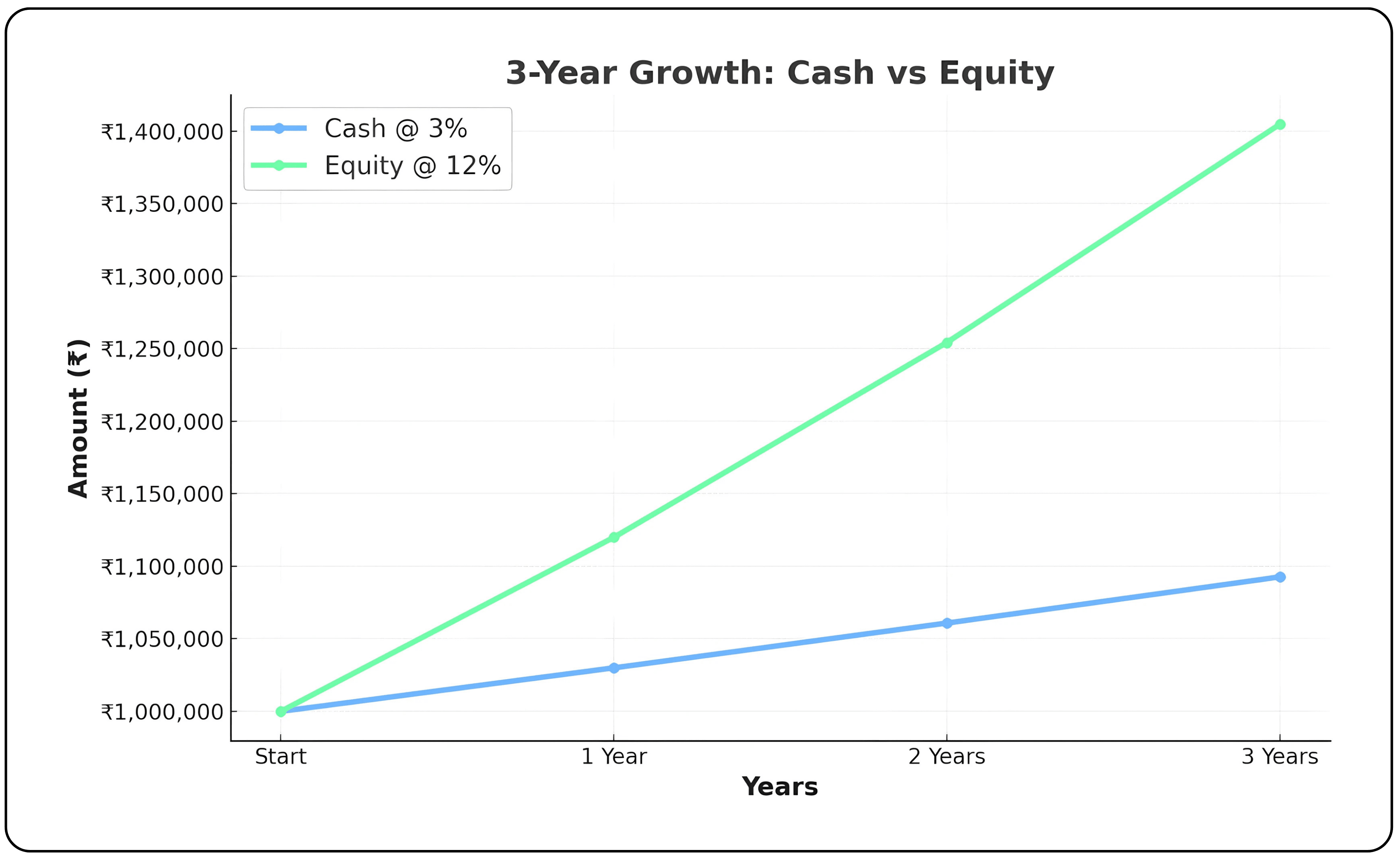

Here’s how it looks over three years if you keep your money in cash versus investing in equity:

| Year | Cash @ 3% p.a. | Equity @ 12% p.a. |

|---|---|---|

| Start | ₹10,00,000 | ₹10,00,000 |

| 1 Year | ₹10,30,000 | ₹11,20,000 |

| 2 Years | ₹10,60,900 | ₹12,54,400 |

| 3 Years | ₹10,92,727 | ₹14,04,928 |

Graph comparing holding cash versus investing in equities over a 3-year period

Notice how the gap keeps getting bigger each year? That is the power of compounding working for equity, and against idle cash. The longer you wait, the more you miss out.

Also read: Credit Card Mistakes Every Student Should Avoid

How inflation makes it worse

While your money sits idle in a savings account, prices don’t stay still. Inflation quietly eats away at your purchasing power every year. At 5% inflation, ₹10 lakh today will only buy what ₹9.5 lakh buys a year from now. Stretch that over three years, and you’re effectively losing more than ₹1.5 lakh in real terms.

So not only are you missing out on market gains, but the value of your cash is shrinking in the background. It’s a double hit that most people don’t notice until it’s too late.

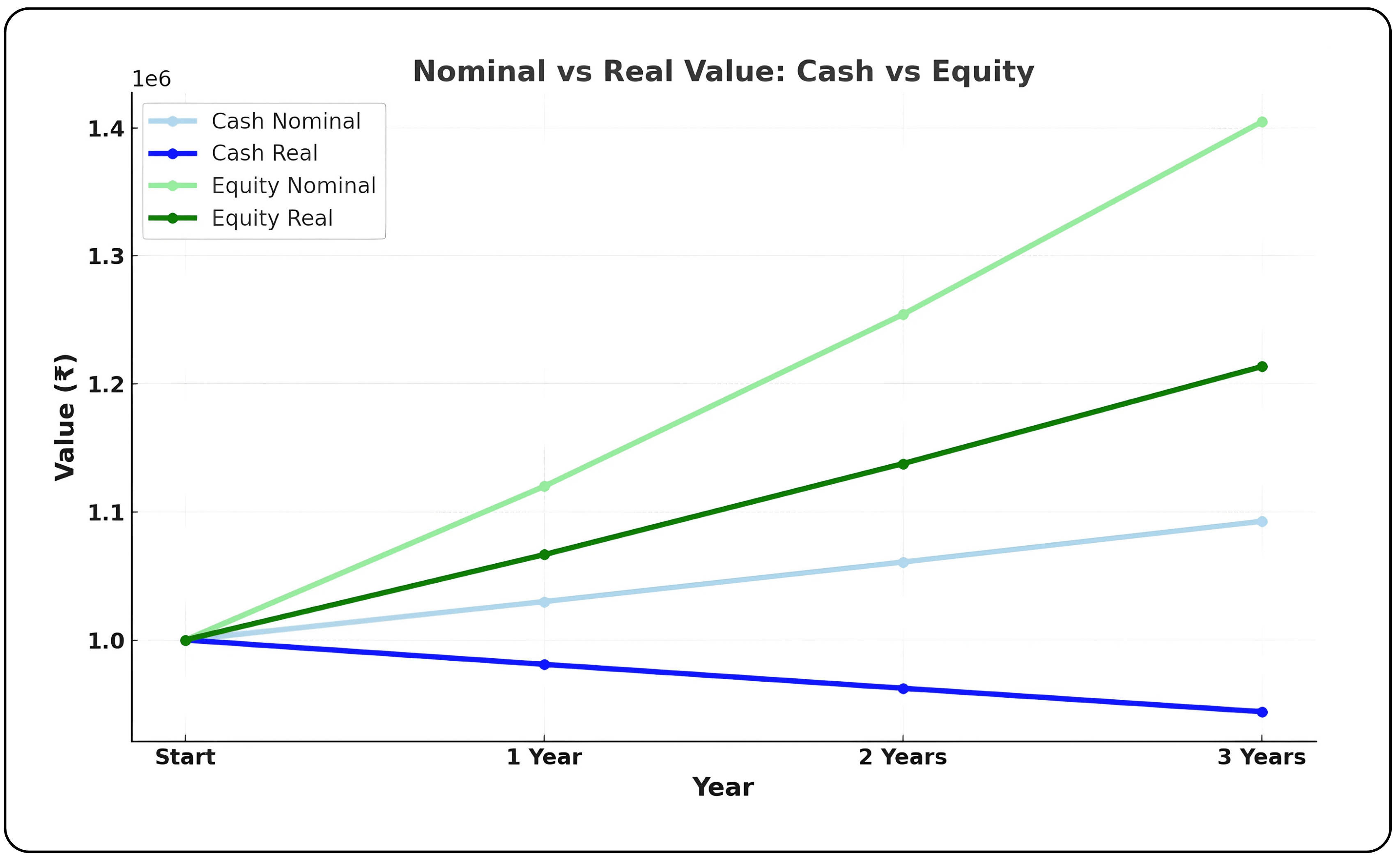

Here is how it looks when we adjust for inflation:

| Year | Cash Nominal (₹) | Cash Real (₹) | Equity Nominal (₹) | Equity Real (₹) |

|---|---|---|---|---|

| Start | 10,00,000 | 10,00,000 | 10,00,000 | 10,00,000 |

| 1 Year | 10,30,000 | 9,80,952 | 11,20,000 | 10,66,667 |

| 2 Years | 10,60,900 | 9,62,268 | 12,54,400 | 11,37,778 |

| 3 Years | 10,92,727 | 9,43,939 | 14,04,928 | 12,13,630 |

What does this mean?

Even though your bank shows ₹10.9 lakh after three years, in terms of purchasing power, it is actually worth less than when you started, around ₹9.4 lakh. Equity, on the other hand, not only beats inflation but also grows your wealth significantly.

Graph comparing Nominal Value and Real Value to show the impact of inflation

What the chart shows:

The green lines (equity) climb much faster than the blue lines (cash). See how the darker lines, the real values, trail behind the lighter ones? That is inflation at work.

Your cash balance may look bigger over time, but in reality, its purchasing power is shrinking. Equity, despite its ups and downs, stays well ahead of inflation and grows your wealth.

This is why holding too much cash for years can quietly drain your wealth. Inflation works in silence, but it never stops.

History has a lesson for us

Think back to the last big market crashes. In 2008, when the global financial crisis hit, markets tanked. Many people pulled out or froze, waiting for “the right time” to get back in. But here is what happened: the recovery was swift, and those who sat on cash missed a big chunk of the rebound.

The same thing happened after the COVID crash in 2020. Stocks fell like a rock in March, and by the time most investors felt “safe” again, markets had already climbed back. Those first few months after a crash often deliver the strongest gains, but if you are waiting for prices to “come down a little more,” you end up watching from the sidelines while others ride the rally.

The Nifty 50 chart shows a sustained bull run since the COVID market crash.

Bull runs don’t just last a day or two; they can go on for years. If you keep waiting for the perfect dip, you will miss opportunity after opportunity, and by the time you finally jump in, the big gains are gone.

Here is the truth: nobody rings a bell to announce the bottom. The perfect moment to invest only exists in hindsight.

Also read: Gold’s Journey Through Markets, Technology & Global Power Plays

The psychology that trips us up

Why do smart people keep making this mistake? Two big reasons: fear of losing and fear of regret. We hate the thought of investing today and watching prices drop tomorrow. So, we wait.

Here is the hard truth: Nobody can perfectly time the market. No bell rings at the bottom to tell you it's time to buy. History shows us that after major crashes, like in 2008 and 2020, the markets recovered much faster than anyone expected. The people who waited for more certainty missed out on the biggest gains.

The bottom line

Holding cash in a rally feels safe, but safety can be expensive. Every day your money sits idle, you are losing out on potential growth. The market does not reward timing; it rewards time.

The sooner you start, the better your chances of building real wealth.

So next time you are tempted to “wait it out,” ask yourself: Can I afford the cost of doing nothing?

Ready to put your money to work? Start investing in mutual funds with CubePlus today.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.