Do you remember your first visit to a bank to open an account? For many of us, it was with a parent or guardian, clutching a bunch of documents we barely understood.

When the banker smiled, slid a form across the desk, and asked, ‘Which account would you like to open?’, that’s where the confusion begins.

Savings, current, rural, salary… the list seems endless. But the truth is, each account is designed for a different kind of person and a different life story. Whether you are exploring different types of savings accounts or wondering about the best type of savings account for your lifestyle, the options can seem overwhelming.

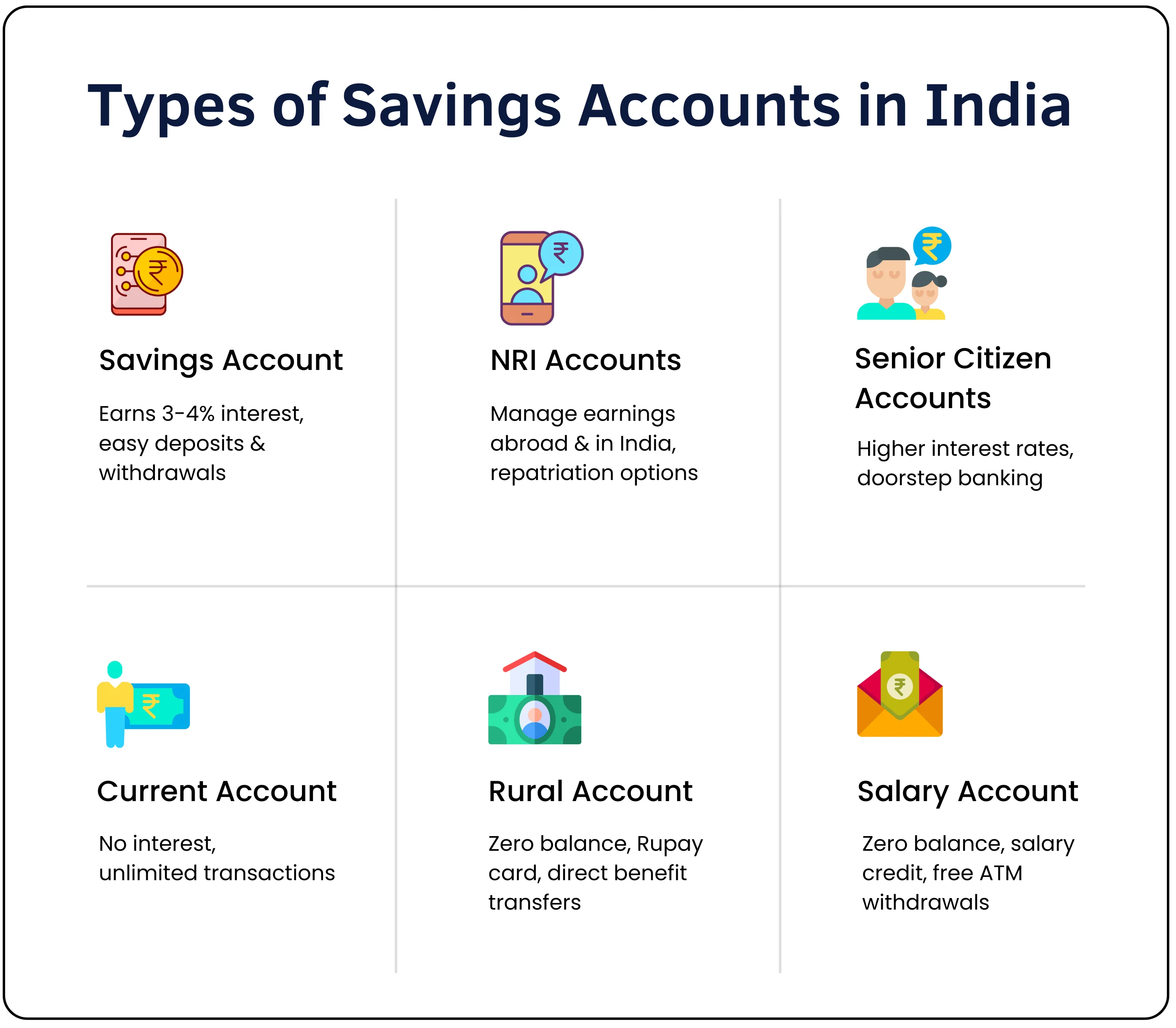

1. Savings Account

For most Indians, the savings account is the very first step into the world of banking. Think of college students who get their first stipend or families managing household budgets.

It’s simple: you deposit money, earn interest (between 3–4% per annum on average in India, depending on the bank), and withdraw when needed.

Example: Priya, a schoolteacher in Pune, keeps her monthly salary in a savings account. She uses it to pay bills, make UPI transfers, and put aside a little extra for her daughter’s school trip.

Many banks, such as SBI and HDFC, offer their own variants of savings accounts. For instance, customers often compare types of SBI savings accounts or types of HDFC savings accounts to see which features suit them better.

2. NRI Accounts

These accounts are specifically designed for Indians living abroad to manage their earnings and investments back home. There are three major types:

- NRE (Non-Resident External) lets NRIs hold and remit foreign income in India. Funds are fully repatriable and tax-free in India.

- NRO (Non-Resident Ordinary) for income earned in India, like rent, dividends, or pension. Funds are partly repatriable, and interest is taxable.

- FCNR (Foreign Currency Non-Resident) allows NRIs to maintain fixed deposits in foreign currencies, protecting them from exchange rate fluctuations.

Example: Arjun, an engineer working in Dubai, uses his NRE account to send money home to his family in Chennai. His father, meanwhile, uses an NRO account to manage the rent he earns from a property in India.

Want to know how to open an NRI account with Tradejini? Check out here

3. Senior Citizen Accounts

Created specifically for senior citizens, these accounts come with higher interest rates than regular savings accounts, flexible fixed deposit options, and additional benefits like doorstep banking, medical insurance tie-ups, and priority service.

For many retirees, this is often considered the best type of savings account for interest since banks typically offer higher deposit rates compared to standard accounts.

Example: Sulochana, a retired government employee in Kochi, parks her pension in a senior citizen account. She earns higher interest on her savings and appreciates the free home cash delivery service provided by her bank.

4. Current Account

Unlike savings accounts, current accounts don’t offer interest. But they allow high-value and frequent transactions, which makes them ideal for businesses.

Example: A small textile trader in Surat uses a current account to pay suppliers, receive bulk payments, and issue cheques. For him, flexibility and overdraft facilities matter more than earning interest.

5. Rural Accounts

India’s banking story is incomplete without financial inclusion initiatives. Schemes like the Pradhan Mantri Jan Dhan Yojana (PMJDY) have brought crores of people, especially in rural areas, into the formal banking system for the first time. Under PMJDY, individuals can open a Basic Savings Bank Deposit Account (BSBDA), which typically comes with zero minimum balance, a RuPay debit card, and access to Direct Benefit Transfer (DBT) facilities.

These initiatives represent one of the government’s largest efforts to expand access to basic savings accounts and promote financial inclusion across India.

Example: Meera, a farmer’s wife in a village near Varanasi, receives her LPG subsidy and other government welfare benefits directly into her Jan Dhan (BSBDA) account. She no longer has to depend on middlemen.

6. Salary Accounts

Most companies today tie up with banks to open salary accounts for employees. These accounts usually waive minimum balance requirements, offer faster salary credit, and provide perks like instant personal loans.

Example: Amit, who works at an IT park in Hyderabad, gets his salary credited on the last working day of every month. His salary account also gives him free ATM withdrawals across India and discounts on online shopping.

Central banks play a vital role in shaping the Indian stock market. Curious to know how? 👉 How Central Banks Influence Indian Stock Market Trends

Different types of accounts in India

| Type of Account | Who It’s For | Key Features | Example Use Case |

|---|---|---|---|

| Savings Account | Individuals, families, students | Earns 3–4% interest, easy deposits & withdrawals, UPI, and ATM access | Priya, a teacher, uses it for bills, transfers, and monthly savings |

| NRI Accounts (NRE/NRO/FCNR) | Indians living abroad | Manage earnings abroad & in India, repatriation options, tax implications | Arjun in Dubai sends money via NRE; his father uses NRO for rent income |

| Senior Citizen Accounts | Retirees and elderly citizens | Higher interest rates, doorstep banking, FD benefits, extra perks | Sulochana in Kochi earns more interest on her pension savings |

| Current Account | Businesses, traders, entrepreneurs | No interest, unlimited transactions, overdraft facilities, and cheque handling | Textile trader in Surat manages supplier payments and large transactions |

| Rural Account (PMJDY, etc.) | Villagers, farmers, rural households | Zero balance, Rupay card, direct benefit transfers, government subsidies | Meera in Varanasi village receives LPG subsidy directly in her account |

| Salary Account | Employees across companies | Zero balance, salary credit, free ATM withdrawals, and loan offers | Amit in Hyderabad gets his salary credited monthly with added shopping discounts |

So, which account should you choose?

It depends entirely on your lifestyle. A student may start with a simple savings account, an NRI may need an NRE/NRO account, while senior citizens can benefit from higher interest rates on their dedicated accounts. Entrepreneurs may need a current account, and employees often rely on salary accounts.

If you are focused on building wealth, you might also explore long-term savings options like fixed deposits or recurring deposits. And for those who want liquidity, banks offer limited withdrawal savings accounts and easy access savings accounts at Axis Bank as digital-first choices.

At the end of the day, it’s not just about where you keep your money, it’s about how your bank account fits into your story.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.