Are Indian investors paying a high price for DMart shares compared to its global peers? The simple answer is generally yes, but this premium is often justified by its unique position and growth prospects. DMart’s valuation, especially when stacked up against global retail giants like Carrefour or industry averages across developed markets, looks sky-high. Its P/E multiple isn’t just higher; it’s in another league altogether.

But here’s the thing: high prices in the market often reflect high conviction. What investors are buying into isn’t just today’s numbers; it’s the future potential, the runway for growth, and the consistency of execution.

This comparison dives into whether that premium is irrational exuberance or a calculated bet on a high-quality retail business operating in a still-evolving Indian market. We’ll line up the facts, contrast them with Carrefour, and understand why DMart commands the kind of valuation it does, and whether it’s justified.

Let's break it down with facts and figures:

| Carrefour France (Focus on French Operations & Group Data) |

DMart (Avenue Supermarts Ltd) |

|---|---|

| Primary Market | |

|

France and international markets (Part of Carrefour Group) |

India (Listed as Avenue Supermarts Limited on NSE) |

| Business Model | |

|

Multi-format: Hypermarkets, supermarkets, convenience stores, cash & carry, e-commerce. Focus on private label, digital transformation, and sustainable food sourcing ("Food Transition"). |

EDLC–EDLP (Everyday Low Cost, Everyday Low Price). Direct procurement, owned stores, operational efficiency, and limited promotions. |

| Store Locations | |

|

Urban, suburban, and local areas; Often anchor tenants in shopping centers. |

Primarily suburban; mostly owned properties with simple, no-frills layouts. |

| Product Mix | |

|

Wide range of food (fresh, organic, processed) and non-food (electronics, apparel, home goods). |

Essentials-focused: groceries, staples, personal care, general merchandise, limited apparel. Food dominates. |

| Supply Chain | |

|

Complex, global, and local sourcing; multiple distribution centers. |

Direct procurement from manufacturers and farmers; quick vendor payments (e.g., within 11 days). |

| Customer Focus | |

|

Broad audience across formats; A growing push toward healthy and sustainable products. |

Middle-class Indian households seek consistent low prices and value. |

| Marketing & Promotions | |

|

Traditional and digital advertising, loyalty programs, frequent promotions. |

Relies on word-of-mouth, in-store promotions, and low everyday prices over discounts. |

| E-commerce Strategy | |

|

Strong omnichannel push: home delivery, click & collect, partnerships. |

"DMart Ready" app and web platform; supportive to physical stores, not central to the business. |

| Real Estate Strategy | |

|

Mix of owned and leased properties; Often part of shopping centers. |

The majority of stores owned; reduces rental costs and builds a strong asset base. |

Financial comparison

| Carrefour France (French Ops & Group Data) |

DMart (Avenue Supermarts Ltd) |

|---|---|

| Sales Growth | |

|

Q1 2025 LFL: +2.9% France LFL: -1.7% FY24 LFL: +9.9% |

Q4 FY25: +16.7% YoY FY25 LFL: +8.4% 5yr CAGR: 18.55% |

| P/E Ratio (Trailing) | |

| ~11.36x – 12.0x (typical mature retailer) |

96.4x – 97.6x (growth expectations) |

| PEG Ratio | |

| ~0.83 to -0.22 (low/negative EPS growth) |

16 – 48.2 (Trailing) 5yr PEG: ~3.25 |

| Cost Management | |

| €1.2B savings target by 2025 |

Lean ops, tight control despite inflation |

| Valuation Trend | |

| Low: EV/Rev ~0.1x EV/EBITDA ~1.5x |

High: P/E 97x EV/EBITDA ~55x |

| Debt Level | |

| Manageable for a large retailer |

Almost debt-free |

| Market Maturity | |

| Mature, saturated, competitive |

High-growth, large expansion potential |

| Strategic Challenges | |

|

Price wars, digital shift, inflation, weak sales, regulatory pressure |

Managing fast growth, service levels, margins, online competition |

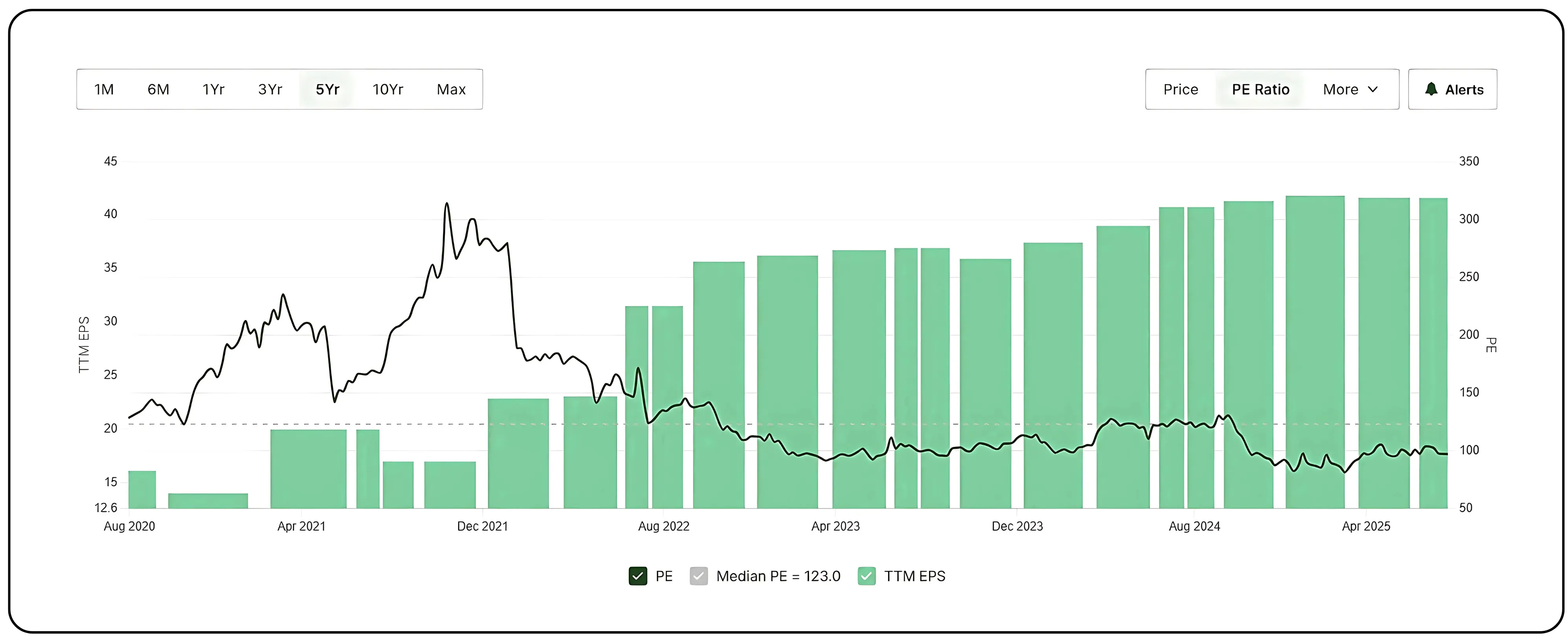

The high price tag: DMart's P/E ratio

As of July 2025, DMart (Avenue Supermarts Limited) consistently trades at a significantly higher P/E (Price-to-Earnings) ratio compared to major global retail giants like Carrefour, or even the broader retail industry averages in developed markets.

- DMart's Trailing P/E ratio: Approximately 96x - 97x (as of recent data). Historical data shows it has often traded above 100x and has reached as high as ~170x-189x in previous years.

Carrefour S.A.'s Trailing P/E Ratio: around 11x - 12x (as of recent data).

Global retail industry average: The P/E ratio for "Grocery Stores" globally tends to be in the low to mid-20s (e.g., around 22x). Even for "Discount Stores," the average is around 30x.

Indian retail industry average: while DMart is an outlier, the broader Indian retail distribution industry also has a higher average P/E, recently seen around 30x-40x, still significantly lower than DMart's.

This stark difference clearly indicates that Indian investors (and global investors participating in the Indian market) are willing to pay a substantial premium for DMart's earnings.

Also read: PG Electroplast Where India's Consumer Electronics Take Shape

Justification: Why the premium?

The high valuation of DMart is not without reason. Several factors contribute to this phenomenon:

Exceptional growth trajectory in a nascent market:

India's retail story: Unlike mature markets like France, where organized retail is saturated, India's organized retail sector is still in its growth infancy, transitioning from unorganized kirana stores. This offers immense headroom for expansion.

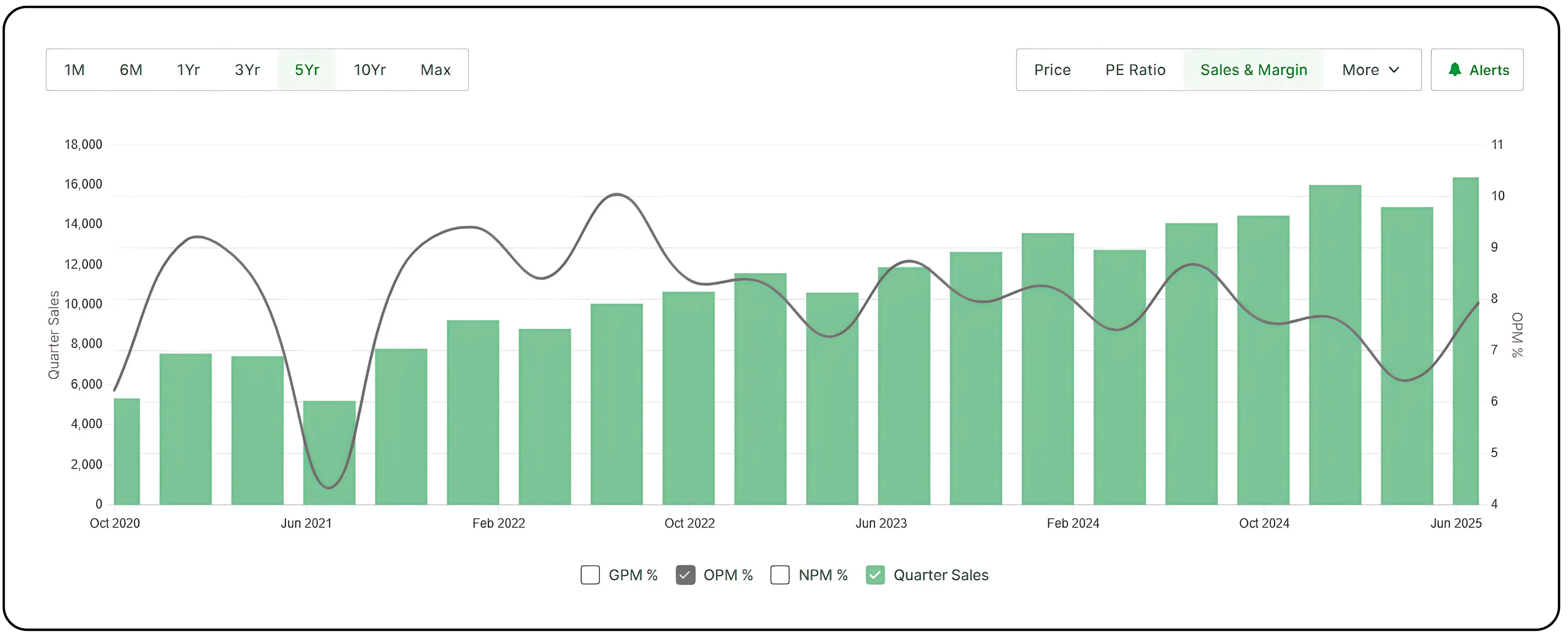

DMart's consistent growth: DMart has demonstrated a remarkable ability to capture this growth. Its 5-year sales CAGR (Compound Annual Growth Rate) has been impressive at around 18-19%, with recent quarterly revenue growth still in the high teens (e.g., +16.7% YoY in Q4 FY25).

Global Comparision: This performance is significantly higher than the single-digit or even negative growth seen in mature retailers like Carrefour France.

- Store expansion: DMart continues to aggressively expand its store network, adding dozens of new stores annually, particularly in cluster-based approaches that maximize efficiency.

Highly profitable and scalable business model (EDLC-EDLP):

Cost efficiency: DMart's "Everyday Low Cost, Everyday Low Price" (EDLC-EDLP) model is incredibly efficient. By directly procuring from manufacturers, owning most of its stores (reducing rent costs), and maintaining a no-frills approach, it operates with superior cost control.

High Inventory Turnover: DMart excels at moving inventory quickly, leading to efficient capital utilization.

Strong unit economics: Each new DMart store, once mature, tends to be highly profitable, contributing positively to the overall bottom line.

Strong moat and brand loyalty:

Customer trust: DMart has built immense trust and loyalty among Indian middle-class consumers by consistently delivering value. This makes it a preferred shopping destination.

Efficient supply chain: Its strong and efficient supply chain gives it a competitive edge that is difficult for new entrants to replicate quickly.

Almost debt-free balance sheet:

- DMart's balance sheet is remarkably strong, with very low debt. This provides financial flexibility for expansion and resilience against economic downturns, making it a "safer" growth bet for investors.

Scarcity premium:

- In the Indian equity market, truly high-quality, high-growth retail stocks with a proven track record like DMart are relatively scarce. This scarcity also contributes to a premium valuation as investors are willing to pay more for such an asset.

Future growth potential (PEG Ratio Perspective):

- While DMart's trailing PEG ratio can appear high, investors often focus on forward PEG ratios, factoring in projected earnings growth. Even with a high P/E, if the expected earnings growth is also exceptionally high and sustainable for several years, a higher PEG might be tolerated by growth investors. The consensus is that DMart's growth runway in India is still very long.

In conclusion, while Indian investors are indeed paying a much higher price for DMart shares when compared to global retail peers, this is largely justified by DMart's superior and consistent sales growth in a rapidly expanding market, its highly efficient and profitable business model, strong brand moat, and robust financial health. It's a classic case of growth stock valuation, where investors are pricing in significant future earnings potential, accepting a lower current earnings yield in anticipation of substantial capital appreciation.

Also read: Praveg Ltd. Positioned for Margin Expansion and Long-Term Profitability

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.