The Indian logistics industry stands as the backbone of the nation's economic growth, facilitating the freight movement of goods and services across India, one of the world's most geographically diverse countries. Currently valued at approximately ₹9 lakh to 12 lakh Crores, India's logistics sector plays a vital role in connecting manufacturers with consumers, businesses with markets, and rural areas with urban centers. Despite facing challenges such as high logistics costs and infrastructure gaps, the industry is undergoing a remarkable transformation driven by government initiatives, technological innovations, and increasing formalization.

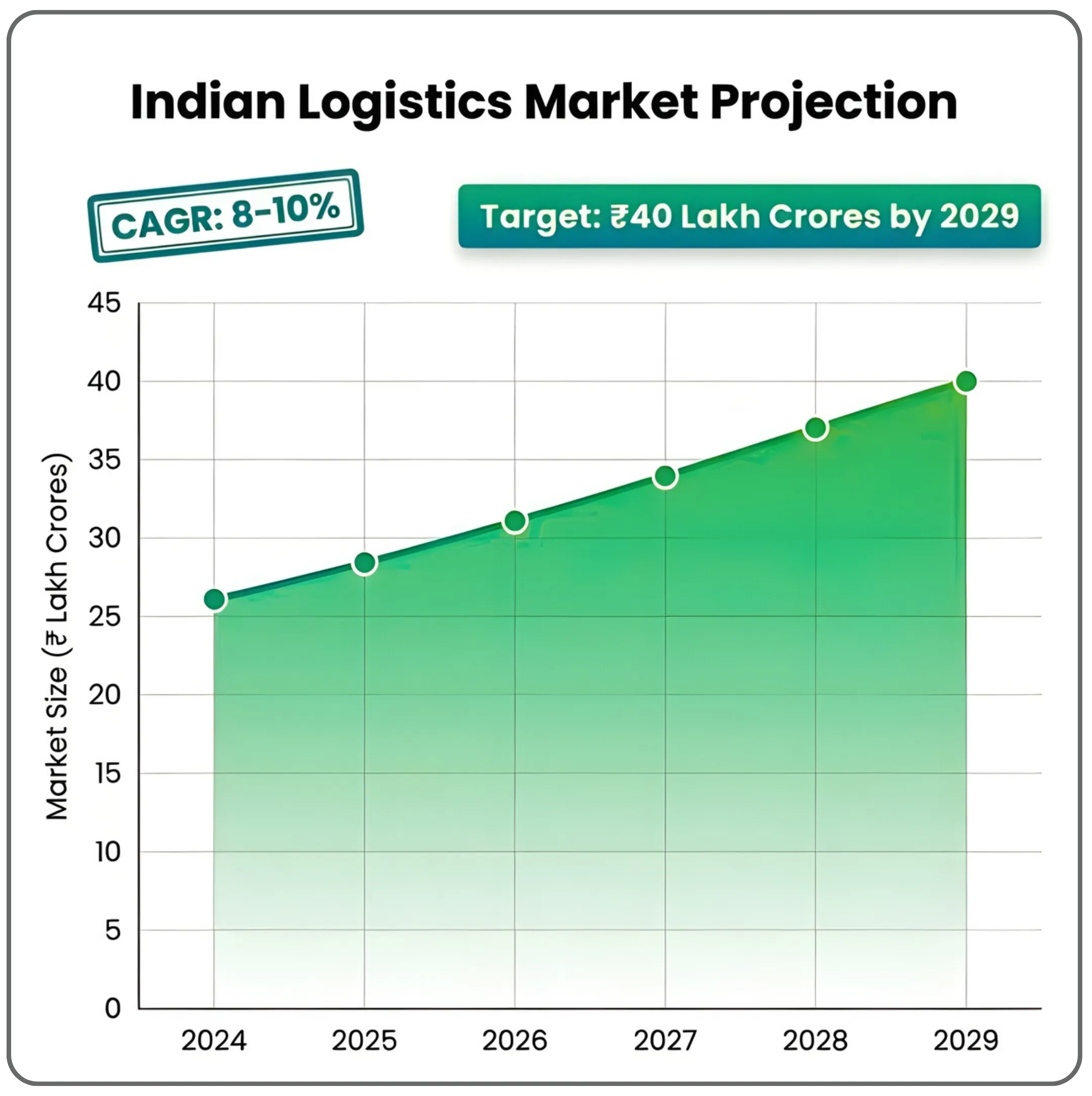

The logistics market is projected to grow at a robust compound annual growth rate (CAGR) of 8-10% over the next five years, potentially reaching ₹40 lakh crores by 2029. This rapid growth trajectory positions India as one of the most promising logistics companies destinations globally, attracting substantial investments from domestic and foreign investors while creating millions of job opportunities.

Industry Overview: The Foundation of Economic Growth

The logistics sector in India encompasses a wide range of services and activities that facilitate the movement, storage, and distribution of goods. Think of it as the circulatory system of the economy; just as blood vessels transport nutrients throughout the body, supply chains move products from farms and factories to stores and homes across the country.

Logistics costs in India are estimated at 13–14% of GDP, higher than the 8–10% seen in developed economies. This higher percentage indicates both the sector's significance and the room for improvement in operational efficiency. The industry in India employs over 2.2 crore (22 million) people directly and indirectly, making it one of the largest employment generators in the country.

What Makes Indian Logistics Unique?

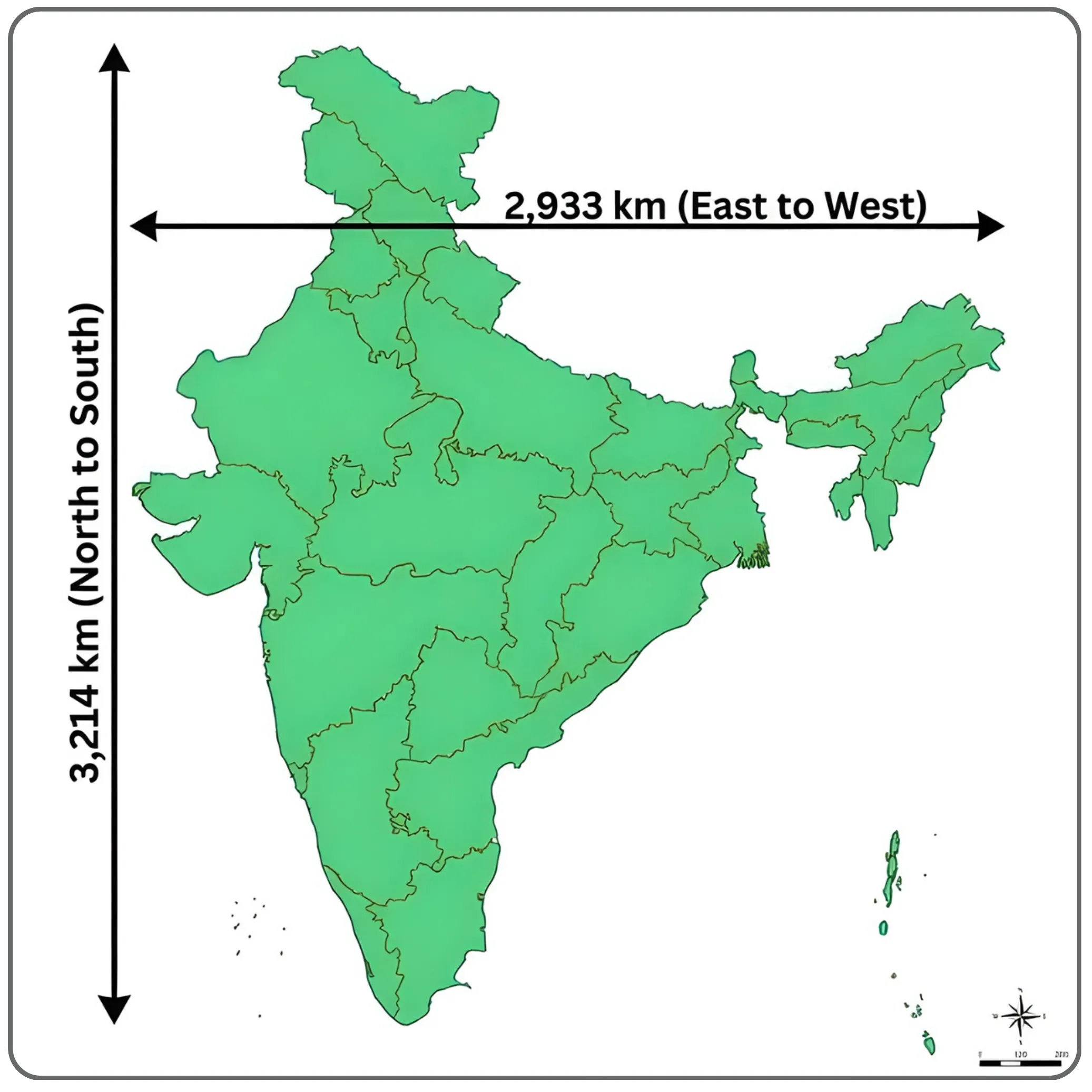

India's logistics landscape is shaped by several distinctive characteristics. First, the sheer geographical expanse and diversity present both challenges and opportunities. From the mountainous terrains of the Himalayas to the coastal regions spanning 7,500 kilometers, from dense urban metros to remote rural villages, logistics providers must navigate an incredibly varied operational environment.

North to South: The country spans roughly 3,214 km & East to West: The country spans roughly 2,933 km.

Second, India's population of over 1.4 billion creates massive demand for goods movement. Every day, millions of parcels, industrial materials, agricultural products, and consumer goods travel across the nation, creating one of the world's most dynamic logistics markets.

Third, the industry remains largely fragmented, with thousands of small and medium transport company operators alongside a growing number of organized players. This fragmentation, while presenting challenges, also offers significant consolidation opportunities for well-capitalized and professionally managed leading logistics companies

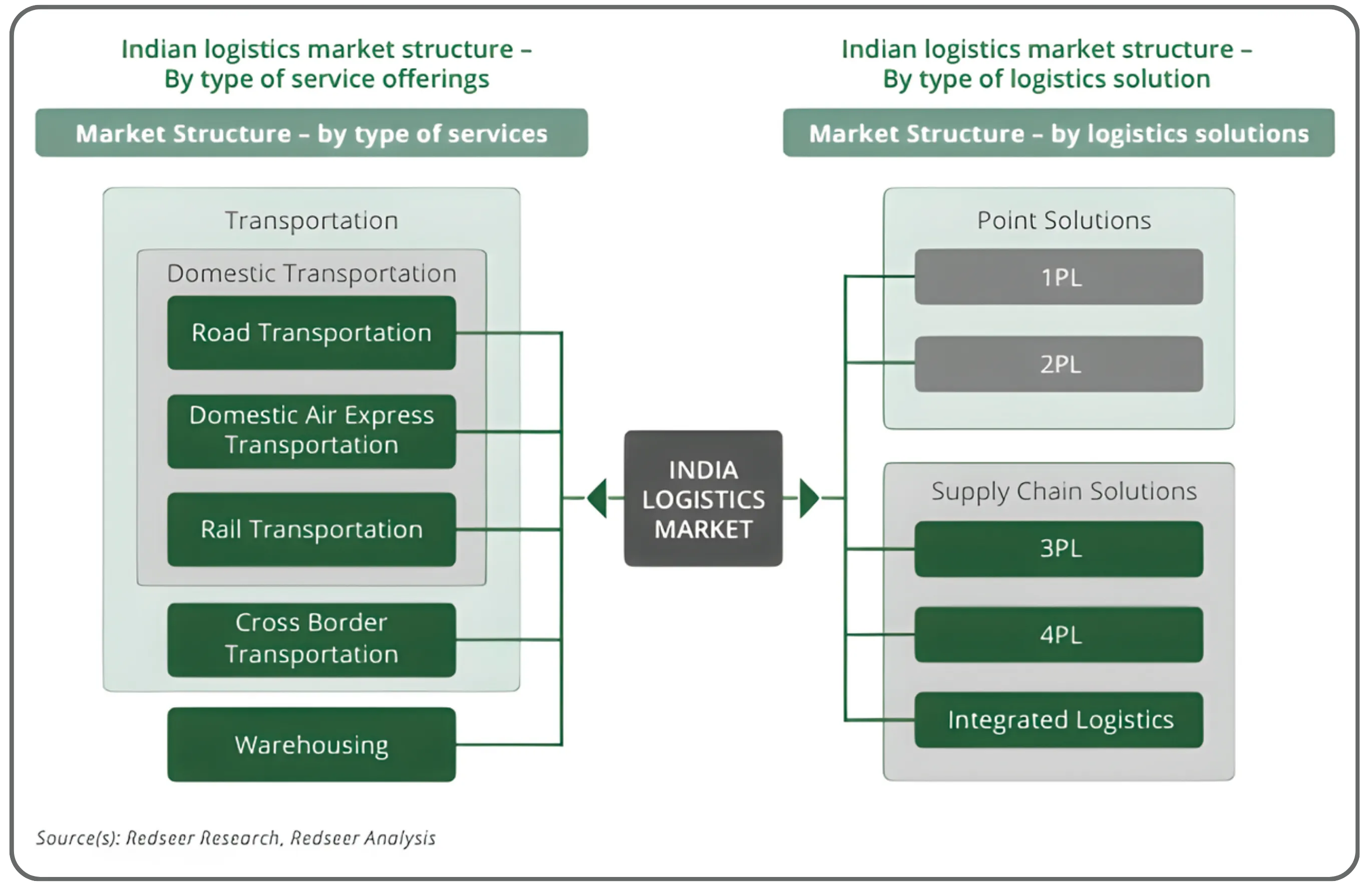

Types of Logistics Businesses: Understanding the Ecosystem

These logistics service providers range from traditional freight forwarders to modern third party logistics (3PL) providers, each offering specialized value added services to meet diverse customer requirements.

1. Contract Logistics and Warehousing

Contract logistics involves comprehensive supply chain management services where companies outsource their entire logistics operations to specialized providers. This segment includes warehousing, inventory management, and distribution services. Modern warehouses in India are evolving from basic storage facilities to sophisticated distribution centers equipped with advanced automation, climate control for sensitive goods, and warehouse management systems for real-time inventory tracking.

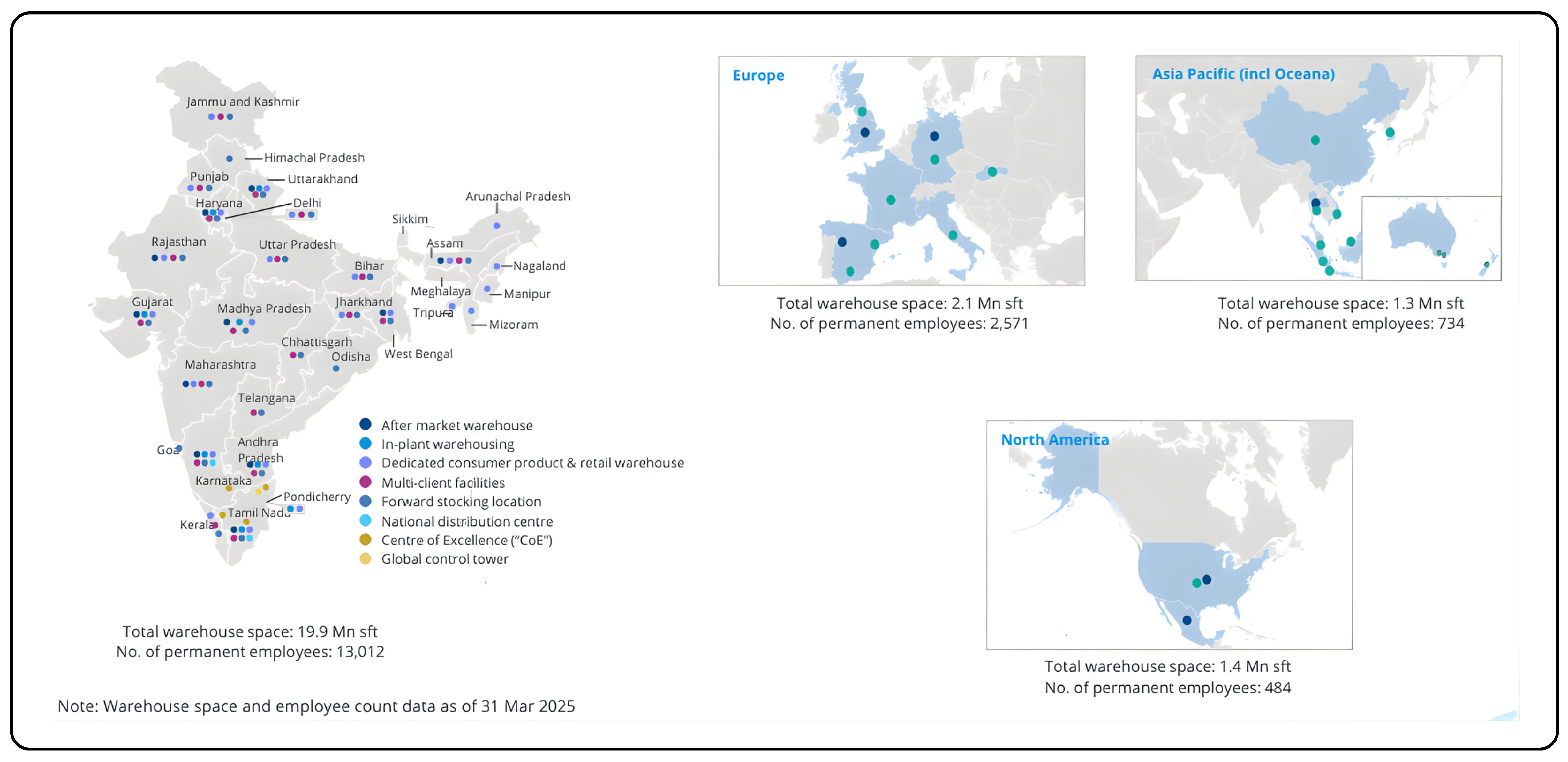

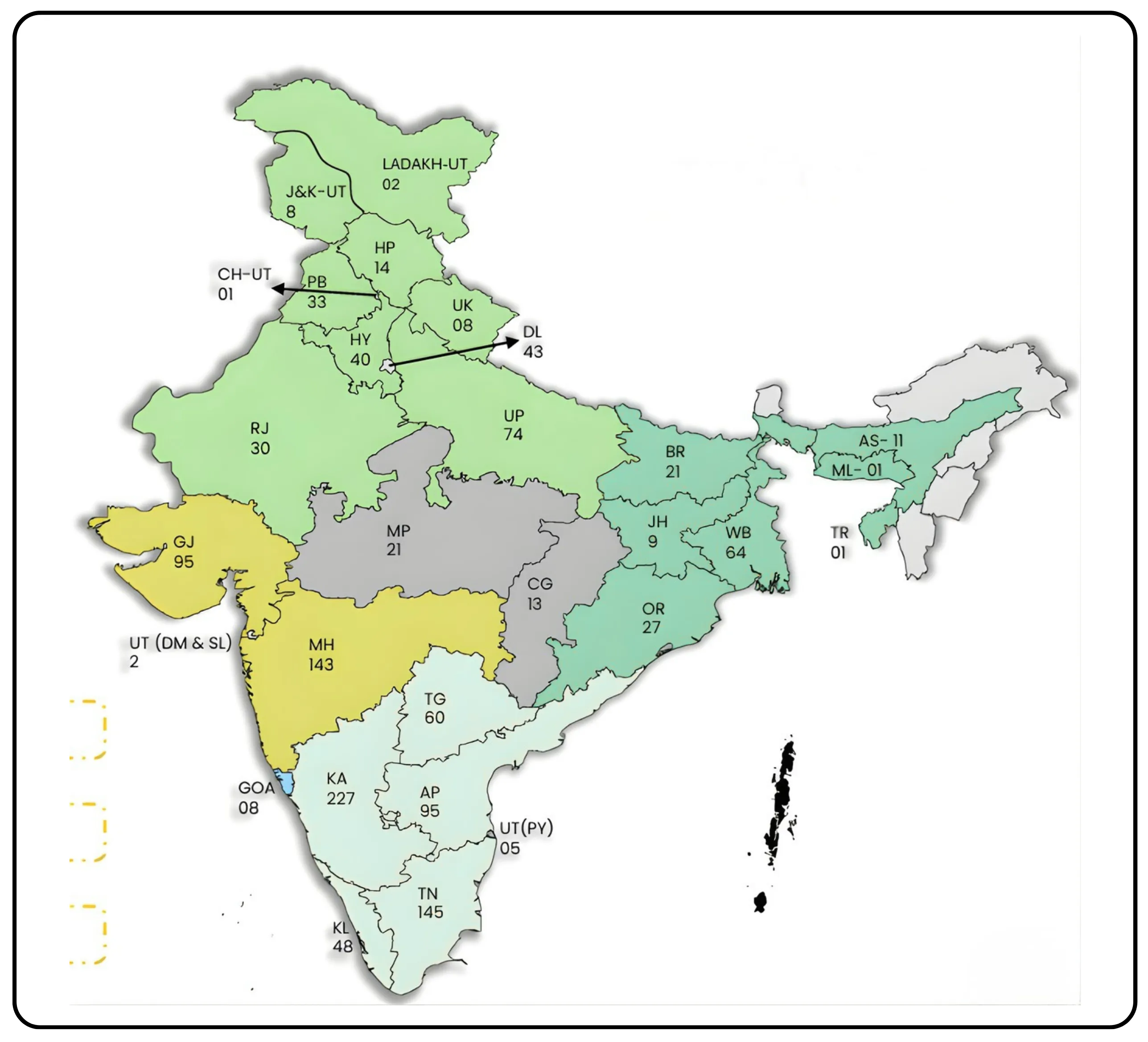

The warehousing sector has witnessed tremendous growth, with organized Grade A warehousing supply reaching 393 million square feet. These premium facilities feature high-quality construction, strategic locations, and advanced material handling equipment. The contract logistics market, supported by warehouse automation to enhance efficiency, is expected to expand at a CAGR of 8-10%, reaching ₹24 lakh crores by 2025-26.

2. Express Logistics and B2B Distribution

Express logistics focuses on time-sensitive deliveries, providing day-definite or time-definite services. Companies like Blue Dart dominate the air freight space in India, operating dedicated air and ground networks to ensure rapid delivery. The B2B express segment is expanding at a robust 15% CAGR, with the market size expected to reach ₹24,000 crores by 2026

3. Less Than Truck Load (LTL) and Full Truck Load (FTL) Transportation

LTL services cater to businesses that don't require an entire truck for their shipments. Multiple customers share truck space, making this a cost-effective solution for small and medium enterprises. Companies like VRL Logistics specialize in LTL operations, operating extensive hub-and-spoke networks across India.

FTL services, on the other hand, dedicate entire trucks to single customers, ideal for large shipments. Road transportation accounts for more than 60% of India's freight transportation by volume, employing millions of truck drivers and operators. The transportation and logistics sector relies heavily on road networks due to their flexibility and last-mile connectivity.

4. Freight Forwarding and International Logistics

Freight forwarding involves managing international trade shipments across ocean, air, and land. This segment has grown significantly with India's expanding global trade footprint and access to international markets. Allcargo Logistics, for instance, holds a dominant 15% market share in the global LCL (Less than Container Load) consolidation business, operating across 2,400 trade lanes worldwide.

Industry estimates suggest the LCL shipping market was valued at USD 9.41 billion in 2023 and is projected to reach USD 13.21 billion by 2030, representing a CAGR of 5.06%. According to market research reports FCL (Full Container Load) shipping market was valued at USD 122.75 billion in 2023 and is projected to reach USD 143.50 billion by 2030.

5. Last-Mile Delivery and Quick Commerce

Last-mile delivery (the final leg of a product's journey from a distribution center to the customer's doorstep) has become increasingly critical with the e-commerce boom, driving rising demand for efficient delivery networks. This segment is the fastest-growing, expanding at 25% CAGR with an estimated market value of ₹36,500 crores by 2026.

Quick commerce, focused on ultra-fast deliveries (often within 10-30 minutes), has emerged as a game-changer, especially in urban areas. Platforms are investing heavily in micro-fulfillment centers and hyperlocal distribution networks to meet growing consumer expectations for instant gratification.

6. Specialized Logistics

This includes temperature-controlled cold chain logistics for pharmaceuticals and perishables, project cargo handling for oversized industrial equipment, hazardous materials transport, and automotive logistics serving the manufacturing sector. These specialized segments command premium pricing due to their complexity and specialized logistics infrastructure requirements.

Want to understand the packaging ecosystem that supports logistics? Read: The Packaging Industry in India – Structure, End-Use Demand, and Industry Dynamics

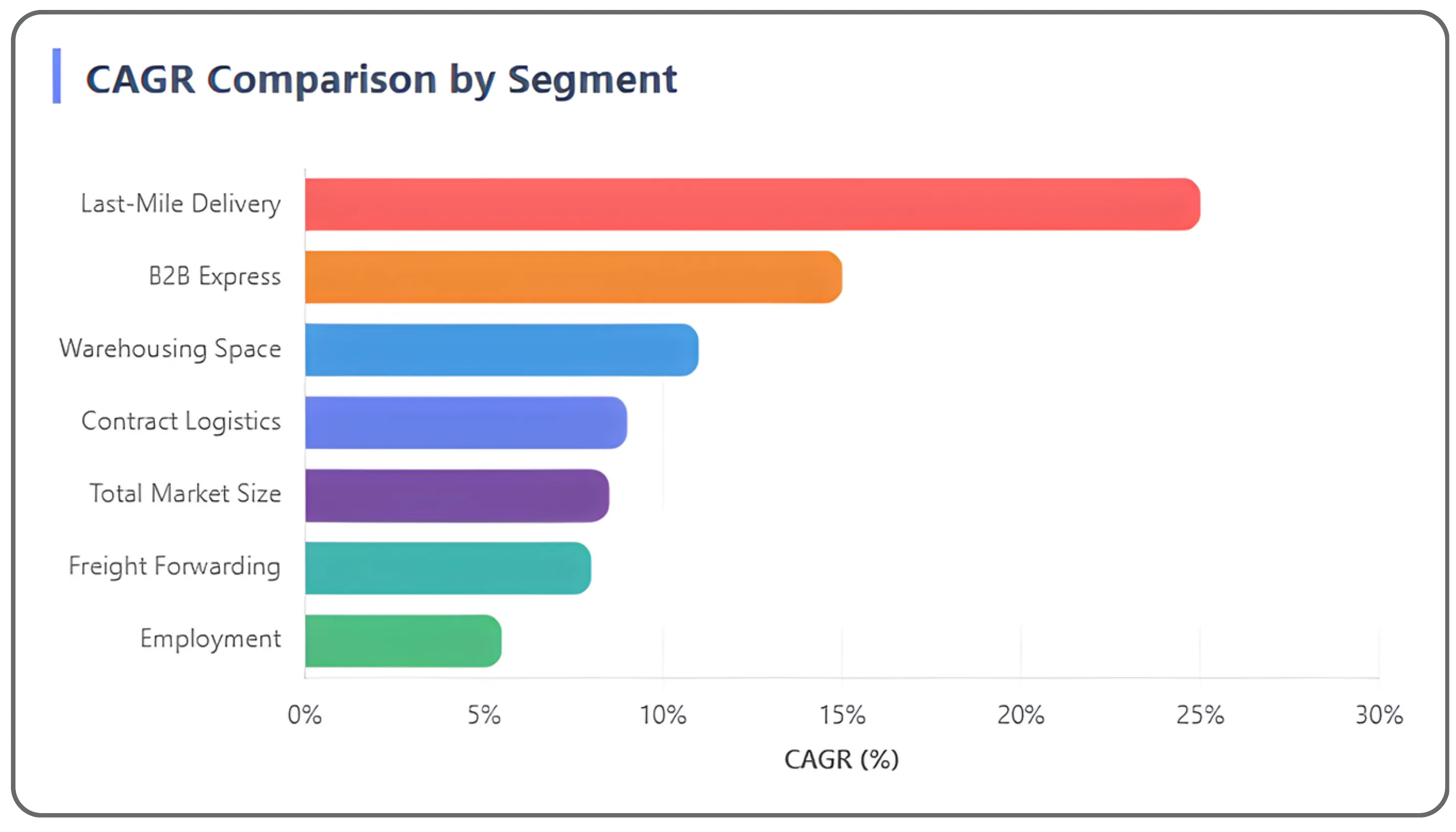

Historical Market Data and Growth Projections

| Parameter | FY 2023 | FY 2024 | FY 2025 (E) | FY 2028–29 (P) | CAGR |

|---|---|---|---|---|---|

| Total Market Size | ₹90 lakh crore | ₹1,05 lakh crore | ₹1,15 lakh crore | ₹1,34–1,50 lakh crore | 8–9% |

| Contract Logistics | ₹9 lakh crore | ₹20 lakh crore | ₹22 lakh crore | ₹24 lakh crore | 8–10% |

| B2B Express | ₹0.18 lakh crore | ₹0.20 lakh crore | ₹0.22 lakh crore | ₹0.24 lakh crore | ~15% |

| Last-Mile Delivery | ₹0.25 lakh crore | ₹0.30 lakh crore | ₹0.33 lakh crore | ₹0.365 lakh crore | ~25% |

| Freight Forwarding | ₹0.40 lakh crore | ₹0.43 lakh crore | ₹0.456 lakh crore | ₹0.53 lakh crore | ~8% |

| Warehousing Space | 350 mn sq ft | 375 mn sq ft | 393 mn sq ft | 500 mn sq ft | 10–12% |

| Employment | 2.0 crore | 2.1 crore | 2.2 crore | 2.5 crore | 5–6% |

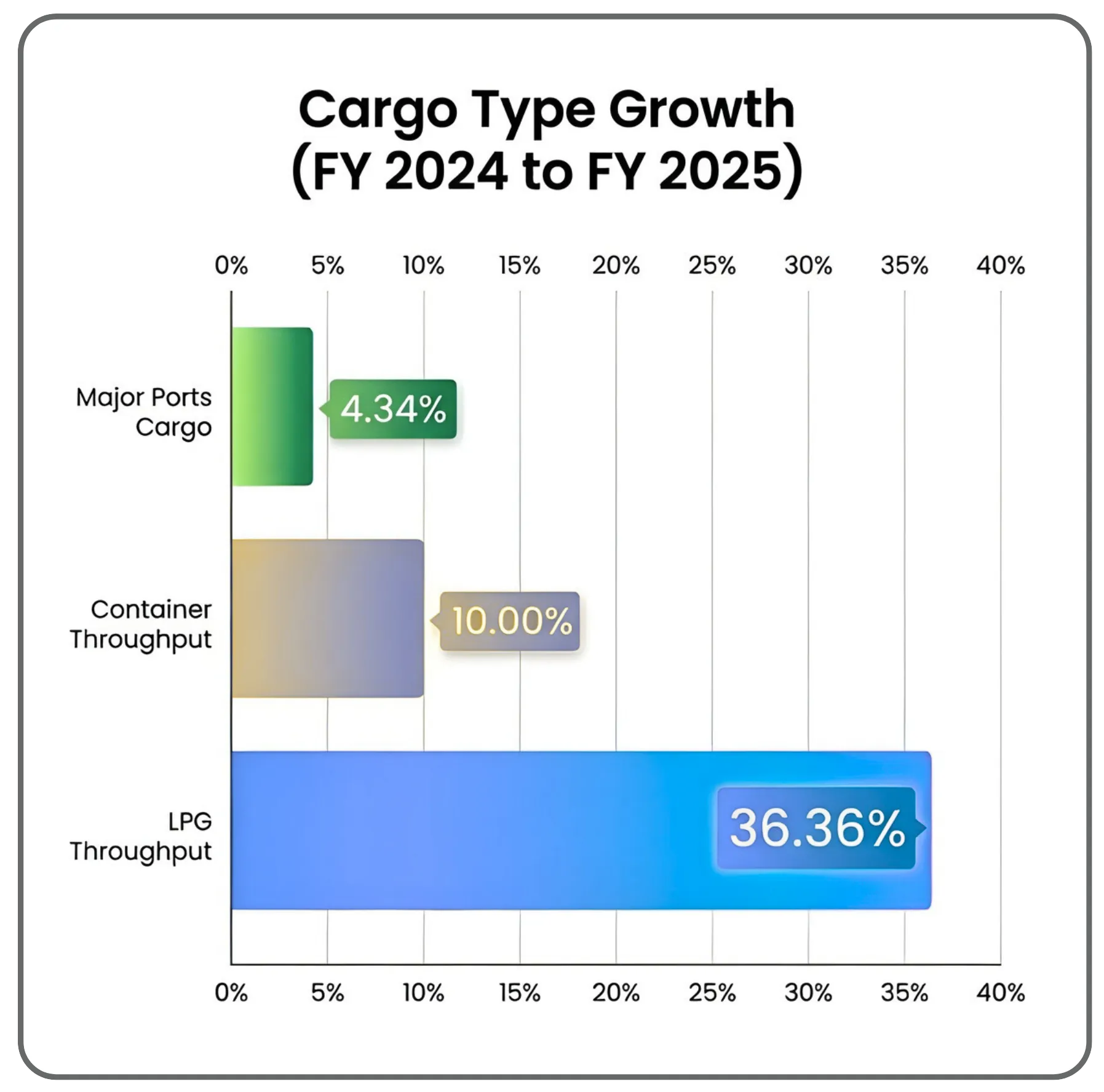

India Logistics Market Overview

India Cargo Throughput Growth

| Cargo Type | FY 2024 | FY 2025 | Growth (%) |

|---|---|---|---|

| Major Ports Cargo | 819.13 million tonnes | 854.86 million tonnes | 4.34% |

| Container Throughput | 12.31 million TEUs | 13.54 million TEUs | 10.00% |

| LPG Throughput | 3.3 MMT | 4.5 MMT | 36.36% |

Want to understand a key segment driving freight movement? Read: India's Fertilizer Industry – Market Trends and Future Prospects

Market Share of Major Players

The Indian logistics industry features both large organized players and thousands of small regional operators. Here's a snapshot of major players and their approximate market positions.

The competitive landscape features a mix of traditional freight logistics companies and modern technology driven solutions providers. While the sector has traditionally faced challenges like skilled workforce shortage and operational costs, leading players are investing in transportation management systems and digital platforms to improve logistics efficiency and achieve customer satisfaction leading to market dominance.

Leading Companies by Segment:

Express Logistics

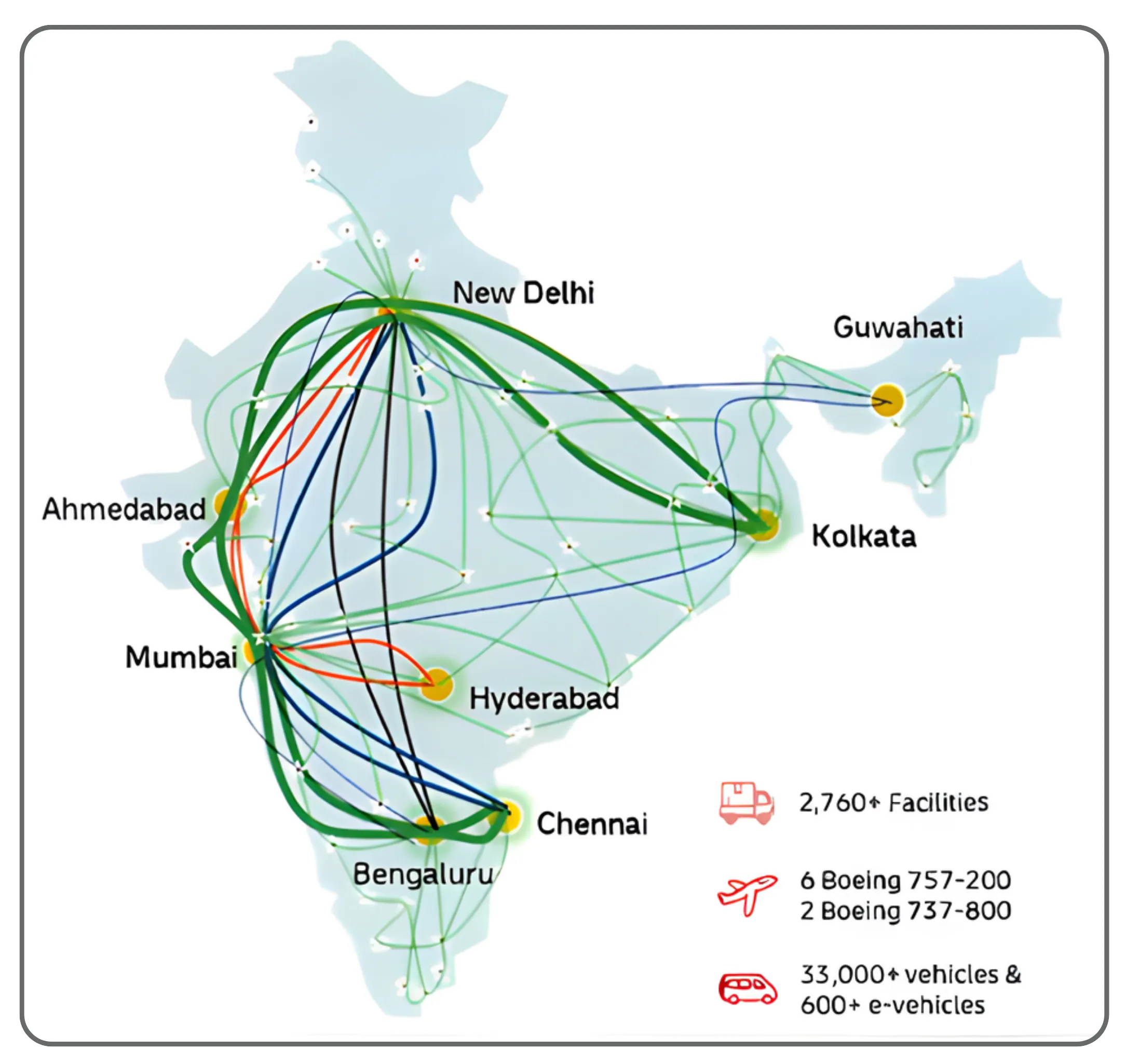

Blue Dart Express: Market leader in air-integrated express logistics, handling 376.92 lakh domestic shipments and 5.72 lakh international shipments annually. Revenue: ₹5,720 crores (FY25). Other significant players: DTDC, Delhivery

International Supply Chain:

Allcargo Logistics: Global leader with 15% market share in LCL consolidation, operating across 2,400 trade lanes. Revenue: ₹16,022 crores (FY25)

Contract Logistics

Mahindra Logistics: One of the largest integrated solutions providers. Revenue: ₹10,029 crores (FY25)

TVS Supply Chain Solutions: Serving 6,277 customers globally including 91 Fortune 500 companies. Revenue: ₹9,996 crores (FY25)

Road Transport (LTL/FTL):

VRL Logistics: Leader in parcel transportation with 6,115 owned vehicles and extensive road transport network, operating 1,253 branches across India. Revenue: ₹3,161 crores (FY25)

Specialized Terminals:

Aegis Logistics: Leading tank terminal operator with LPG and liquid logistics. Group EBITDA: ₹1,120 crores (FY25)

Competitive Landscape Characteristics:

The market remains highly fragmented, especially in road transport where operators with fewer than five trucks constitute more than half of all goods vehicles. However, the organized sector is gaining ground, driven by:

- Stricter GST compliance requirements

- Customer preference for reliable, technology-enabled services

- Access to capital for infrastructure investments

- Ability to operate pan-India networks

These developments are crucial for reducing logistics cost (currently at 13-14% of GDP) and moving India toward lower logistics costs comparable to developed economies. Governmental initiatives and infrastructure investments are creating opportunities for logistics partners to build more efficient networks, while consumer demand continues to drive innovation in service delivery.

As the global logistics industry evolves and India positions itself as a logistics partner for the world, understanding the foundational elements covered in Part 1 becomes essential for stakeholders across the value chain. The sector's transformation (driven by technological advancement, infrastructure investments, and policy reforms) promises sustainable development aligned with national growth objectives.

This concludes Part 1: Industry Overview & Market Landscape, where we mapped the structure, scale, segments, and competitive dynamics of India’s logistics ecosystem.

In Part 2: Opportunities, Challenges & Future Outlook, we shift from understanding the present to evaluating the road ahead, connecting policy, profitability, and long-term sector positioning—helping readers understand where the real opportunities lie and what risks must be navigated.

Turn research into action — trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.